MANAGING OPTIMAL WORKING CAPITAL AND CORPORATE PERFORMANCE: EVIDENCE FROM VIETNAM

1Thuongmai University, Vietnam.

2Hanoi University of Industry, Vietnam.

3,4 National Economics University, Vietnam.

ABSTRACT

This paper examined the impact of working capital management (WCM) on corporate performance (CP) in Vietnam. We considered whether there exists an optimal cash conversion cycle (CCC), an optimal net trade cycle (NTC) and how WCM affects CP. We also considered the effect of WCM on CP under financial constraints. This research uses the GLS regression method with research data from listed companies on Vietnam’s stock market from 2009 to 2018, with 5383 business observations in ten years. Initially, this study discovered that CCC and NTC were statistically significant and inversely related to corporate performance (measured by ROA and Tobin's q). However, when continuing to use quadratic functions to analyze data, the study discovered that optimal CCC and NTC have not a linear but an inverted U shape instead. Research results have determined the level of optimal CCC, and NTC affecting CP (measured by ROA); though it was not meaningful when CP is measured by Tobin's q. WCM was also considered in the case of companies with limited financial conditions.

Keywords: Working capital management, Cash conversion cycle, Net trade cycle, Corporate performance, Nonlinear regression.

JEL Classification: G30; G31; G32.

ARTICLE HISTORY: Received:29 May 2019 Revised:5 July 2019 Accepted:8 August 2019 Published:16 September 2019.

Contribution/ Originality: This study fully and comprehensively examines the impact of working capital management through CCC and NTC on corporate performance. This study was carried out by collecting data from listed companies on Vietnam's stock market, which is an emerging economy that can demonstrate the optimal threshold of both CCC and NTC’s impact on CP.

1. INTRODUCTION

A growing economy brings many benefits to businesses, so that they can expand their market, improve their management methods and business mechanisms. There will also be management challenges for businesses, forcing them to restructure their production processes, diversify investments and adjust daily business activities. In the process of dealing with these competitive challenges, corporate finance and working capital management (WCM) are big issues that business managers must be aware of. Nowadays, research on working capital management is a common topic and WCM is considered one of the most important factors in financial decisions.

Vietnam's economy is deeply integrated and competition pressure is growing so Vietnamese companies face instabilities and potential risks. In recent years, there are a growing number of Vietnamese enterprises that delay production, close or fall into financial difficulties. Therefore, when implementing working capital management strategies, those companies depend heavily on external funding. If companies face difficulties in accessing external funding sources or the cost of using external funding is too high compared to the cost of internal funding, how does WCM increase corporate performance (CP)? We conducted this research to clarify the effect of WCM on CP and consider whether optimal cash conversion cycles (CCC) and net trade cycles (NTC) exist.

Although this study is not a new topic, it still is important. From the findings on the relationship between WCM and CP, as well as the impact of financial constraints on businesses, the research results will contribute to the theoretical and experimental research on WCM in Vietnam. Through this research, we expect to change the perception chief financial officers have of WCM, so they can develop a working capital management strategy in the most effective suitable way for the company’s financial situation.

This study implemented both simple and complex models. With model 1, the study considered an existence of a linear relationship between both CCC and NTC to CP (measured by ROA and Tobin’s q); and whether those relationships were positive or negative. Next, with model 2, the study considered the nonlinear regression model (function level 2) to find any optimal level for CCC and NTC. Finally, the study considered the effect of WCM on CP under financial constraints.

2. THEORETICAL BASIS

2.1. Working Capital Management

WCM is often the trade-off between risk and profit. Basically, WCM policy is divided into three categories: risky, harmonious and conservative. The policy of venture capital is characterized by high risks and high profits. Working capital policies compromise low risks and low profits, and ultimately conservative strategies accept the lowest risk over profit ratio. To effectively manage working capital, companies need to pay attention to four short-term accounts which are receivables, inventory, cash on hands and short term securities (Brealey et al., 2006![]() ). Working capital in the broad sense is the value of all mobile assets and assets that are associated with the company's business cycle. In each business cycle, working capital transforms through all forms of existence from cash to inventory, receivables and return to the original basic form of cash. Working capital is also cyclical: cash - production reserves - semi-finished products - finished products - cash. Working capital can be divided into operational working capital and financial working capital. Operational working capital includes receivables, inventories and payables, which can be optimized and influenced by company activities. The rest, including cash, market securities, prepaids and all other short-term debts, constitute the financial working capital of the company. This study will focus entirely on operational working capital, which can be simply defined as the combination of receivables plus inventories minus the payables.

). Working capital in the broad sense is the value of all mobile assets and assets that are associated with the company's business cycle. In each business cycle, working capital transforms through all forms of existence from cash to inventory, receivables and return to the original basic form of cash. Working capital is also cyclical: cash - production reserves - semi-finished products - finished products - cash. Working capital can be divided into operational working capital and financial working capital. Operational working capital includes receivables, inventories and payables, which can be optimized and influenced by company activities. The rest, including cash, market securities, prepaids and all other short-term debts, constitute the financial working capital of the company. This study will focus entirely on operational working capital, which can be simply defined as the combination of receivables plus inventories minus the payables.

The more working capital a company has, the lower its liquidity. In other words, effective working capital management needs to allow companies to invest in future growth, repay short-term financing and reduce financial costs. However, it is not easy to optimize working capital utilization. The company cannot reduce its working capital to a minimum without affecting growth and future sales. An optimal level of working capital creates a balance between risks and profits (Filbeck and Krueger, 2005![]() ) so companies need to determine the working capital in accordance with the business context and situation.

) so companies need to determine the working capital in accordance with the business context and situation.

The WCM measurement can be based on the CCC or the NTC. According to Richards and Laughlin (1980![]() ) the Cash Conversion Cycle (CCC) is calculated by the Days Sales Outstanding (DSO) + Days Inventory Outstanding (DIO) – Days Payables Outstanding (DPO). The CCC reflects the number of days needed from the purchase of raw materials until the collection of semi-finished products. According to Shin and Soenen (1998

) the Cash Conversion Cycle (CCC) is calculated by the Days Sales Outstanding (DSO) + Days Inventory Outstanding (DIO) – Days Payables Outstanding (DPO). The CCC reflects the number of days needed from the purchase of raw materials until the collection of semi-finished products. According to Shin and Soenen (1998![]() ) the Net Trade Cycle (NTC) is basically similar to the CCC, but the NTC is considered to be easier to use than the CCC, because it presents different components of the CCC as the percentage of sales.

) the Net Trade Cycle (NTC) is basically similar to the CCC, but the NTC is considered to be easier to use than the CCC, because it presents different components of the CCC as the percentage of sales.

2.2. Receivables Management

Credit sale is a form of transaction that extends a credit line to the customers and delivers receivables to the sellers. Depending on the repayment terms, the company may receive money after several weeks or even months. Receivables management is a way of managing credit, including decisions regarding terms of sales, credit analysis, debt decisions and policies. The easing of the receivables policy means that the company is expanding commercial credit to its consumers.

According to Emery (1984![]() ) there are several reasons behind the company's commercial credit expansion. First, expanding commercial credit is merely due to the flexibility in how businesses operate. The author explained that customers' needs do not follow a principle, because the market is inherently imperfect. There is always a difference in the expected demand, which can make production boom. The temporary easing of commercial credit allows account receivables to fluctuate according to the difference in demand, which means stimulating customer purchases, and illustrates the formation of a trend of sales priority instead of focusing on customers or products.

) there are several reasons behind the company's commercial credit expansion. First, expanding commercial credit is merely due to the flexibility in how businesses operate. The author explained that customers' needs do not follow a principle, because the market is inherently imperfect. There is always a difference in the expected demand, which can make production boom. The temporary easing of commercial credit allows account receivables to fluctuate according to the difference in demand, which means stimulating customer purchases, and illustrates the formation of a trend of sales priority instead of focusing on customers or products.

Second, the expansion of commercial credits allows suppliers opportunities to gain more profit due to the expansion of customer base. However, commercial credit also brings risks, such as: (i) customers may fall into insolvency crisis, which will cause their commercial credit to become bad debt; and, (ii) the company will lose the interest rate between the time of sale and the time of repayment from the customer. If the receivables are too high, the company's interest is tied to these receivables. This means that when companies need cash to buy goods or raw materials, they are forced to borrow and have to bear additional costs of debt. Thus, in theory, enterprises should lower their selling standards to an acceptable level so that profits are generated by a natural increase in sales.

There is a trade-off between increased profits and increased receivables-related costs due to lowering the selling standard. The problem is the question of when exactly businesses should loosen selling standards and when they should not. In order to achieve effective working capital management, there are two factors that need to be focused on. The company needs to know which credit policy is suitable for the company's business model. Credit policy provides the company with a guide on how to settle liabilities and how much credit provided to customers is considered appropriate. The company also needs to be aware that with a harsh credit policy, the operational safety and liquidity may increase but the company's profitability will be lower. However, achieving the optimal level of safety and profitability is a duty of financial managers. It has been proven by observation that a risky receivables management policy, although bringing higher revenue and profit, will damage the business with bad debt and an interest rate risk.

2.3. Inventory Management

In any industry, inventory is always one of the most valuable assets of a business. The value of inventories usually accounts for a high percentage of the total asset value. Therefore, good inventory control is always necessary and essential in managing working capital. Inventory is the bridge between production and consumption. Every vendor wants to raise inventory levels to respond quickly to customer needs. However, high levels of inventory also have a significant impact on businesses as it reduces liquidity and the funds available for other expenses.

Managing and optimizing inventory levels are tasks that require a balance between revenue and capital. If inventory levels are too low, companies may miss potential sales when the demand arises or may not be able to deliver goods on time. However, investing too much in inventory may cause a shortage in cash that could be used in other projects that bring more effectivity.

Business inventory has tended to decrease over the past decades (Brealey et al., 2006![]() ). Inventory management now prefers a time-based method called just-in-time, which means that inventory is kept to a minimum level and optimal supply chain processes allow for inventory to be circulated in the most efficient way.

). Inventory management now prefers a time-based method called just-in-time, which means that inventory is kept to a minimum level and optimal supply chain processes allow for inventory to be circulated in the most efficient way.

2.4. Short-Term Cash and Securities Management

The trade-off theory argues that companies maximize their value by considering the marginal costs and marginal benefits of holding cash. The marginal benefit of holding cash is reducing the risk of financial exhaustion, allowing the company to implement its targeted investment policy, and avoiding (reducing) costs associated with mobilizing external capital or liquidation of assets. Because the companies operate in an imperfect market, they may have difficulty accessing external capital or incur a high cost of borrowing. Holding cash is a buffer between the company’s source of funding and the use of resources. The marginal cost of holding cash is the opportunity cost of using capital.

According to Miller and Orr (1966![]() ) and Tobin (1956

) and Tobin (1956![]() ), companies store cash when the costs of borrowing increase and opportunity costs related to cash shortages are higher. With a precautionary engine built on the impact of asymmetric information on capital mobilization, it is suggested that even if companies can mobilize capital from the external capital market, they can still avoid doing so because of market problems (for example, when the market is undervaluing company securities). In addition, the trade-off theory emphasizes that companies with large cash reserves can achieve optimal investment policies even when they face financial difficulties.

), companies store cash when the costs of borrowing increase and opportunity costs related to cash shortages are higher. With a precautionary engine built on the impact of asymmetric information on capital mobilization, it is suggested that even if companies can mobilize capital from the external capital market, they can still avoid doing so because of market problems (for example, when the market is undervaluing company securities). In addition, the trade-off theory emphasizes that companies with large cash reserves can achieve optimal investment policies even when they face financial difficulties.

Miller and Orr (1966![]() ) and Kim and Chung (1990

) and Kim and Chung (1990![]() ) developed the trade-off theory to determine the optimal level of cash holding by balancing the cost of cash depletion and cash holding with no interest. Ferreira and Vilela (2004

) developed the trade-off theory to determine the optimal level of cash holding by balancing the cost of cash depletion and cash holding with no interest. Ferreira and Vilela (2004![]() ) argued that holding cash reduces the probability of a financial crisis due to unexpected losses. Thus, even if cash holdings do not generate more profits, companies still have to maintain a certain amount of cash for trading purposes and to meet daily transactions.

) argued that holding cash reduces the probability of a financial crisis due to unexpected losses. Thus, even if cash holdings do not generate more profits, companies still have to maintain a certain amount of cash for trading purposes and to meet daily transactions.

2.5. Payables Management

When a company provides commercial credit to customers, they create receivables. When a company is approved for commercial credit, it will create a payable amount. Payables represent the obligation of the enterprise to pay all of its short-term debt to creditors. Payables appear when companies buy credit-based goods and services. Payables allow the company to utilize the seller’s capital while saving its working capital for other spending purposes. Maximizing payables and prolonging payment terms can become a competitive advantage of companies. By trying to extend the payment term as long as possible, companies have more time to generate cash to pay for payables and more time to effectively manage their businesses.

However, there is a high risk of maximizing the payables by holding a long-term credit from the supplier, such as losing the benefit of a possible discount from the transaction that is fully paid. Consequently, it could undermine the business relationship between the company and its supplier.

Businesses should not incur late payment on payables. If this event happens more than once or twice, suppliers will start to doubt the company's ability to repay and may stop signing future contracts or require the company to pay the full amount in advance for everything. Ultimately, it will affect the profitability of the business. Some available tools such as payables policies, policy implementation and payment monitoring can help managers to ensure the effectiveness of accounts payable management.

3. RESEARCH OVERVIEW

3.1. Empirical Research Shows the Inverse Relationship between Working Capital Management and Corporate Performance

Jose et al. (1996![]() ) studied the relationship between WCM and CP by using the research sample of 2,718 enterprises operating from 1974 to 1993. The strength of the research was in the data abundance with a study period of nearly twenty years and controlling for different industry factors and scales. The research results showed that the CCC has an inverse relationship with CP, which was represented by the rate of return on total assets (ROA) and the rate of return on equity (ROE). The implication was that shortening the cash cycle could increase the profitability of businesses. Therefore, corporate executives could increase business performance by offering reasonable working capital management strategies.

) studied the relationship between WCM and CP by using the research sample of 2,718 enterprises operating from 1974 to 1993. The strength of the research was in the data abundance with a study period of nearly twenty years and controlling for different industry factors and scales. The research results showed that the CCC has an inverse relationship with CP, which was represented by the rate of return on total assets (ROA) and the rate of return on equity (ROE). The implication was that shortening the cash cycle could increase the profitability of businesses. Therefore, corporate executives could increase business performance by offering reasonable working capital management strategies.

Shin and Soenen (1998![]() ) also studied the relationship between WCM and CP. The authors used correlation and regression analysis for a large sample of 58,895 US companies from 1975 to 1994. Experimental results also found a negative relationship between WCM and CP and concluded that managers could create more value for shareholders by reducing the cash cycle to a reasonable minimum.

) also studied the relationship between WCM and CP. The authors used correlation and regression analysis for a large sample of 58,895 US companies from 1975 to 1994. Experimental results also found a negative relationship between WCM and CP and concluded that managers could create more value for shareholders by reducing the cash cycle to a reasonable minimum.

Similar studies were implemented in developed countries such as Wang (2002![]() ) in Japan and Taiwan; Deloof (2003

) in Japan and Taiwan; Deloof (2003![]() ) in Belgium; Nobanee et al. (2011

) in Belgium; Nobanee et al. (2011![]() ) in Japan, Juan García-Teruel and Martinez-Solano (2007

) in Japan, Juan García-Teruel and Martinez-Solano (2007![]() ) in Spain; Mansoori and Muhammad (2012

) in Spain; Mansoori and Muhammad (2012![]() ) in Singapore; and, Tauringana and Adjapong Afrifa (2013

) in Singapore; and, Tauringana and Adjapong Afrifa (2013![]() ) in the United Kingdom. These results showed a negative relationship between the cash conversion cycle and the cash cycle components such as the receivables period, the inventory period and the payables period with CP. Accordingly, corporate executives could increase profits by effectively managing working capital.

) in the United Kingdom. These results showed a negative relationship between the cash conversion cycle and the cash cycle components such as the receivables period, the inventory period and the payables period with CP. Accordingly, corporate executives could increase profits by effectively managing working capital.

Meanwhile, some studies in developing countries such as research by Lazaridis and Tryfonidis (2006![]() ) in Greece; Mathuva (2010

) in Greece; Mathuva (2010![]() ) in Kenya; Ching et al. (2011

) in Kenya; Ching et al. (2011![]() ) in Brazil; and, Afeef (2011

) in Brazil; and, Afeef (2011![]() ) in Pakistan showed that WCM had a definite negative influence on CP. As a result, business managers could reduce the CCC, receivables period and inventory period to a reasonable minimum.

) in Pakistan showed that WCM had a definite negative influence on CP. As a result, business managers could reduce the CCC, receivables period and inventory period to a reasonable minimum.

3.2. Experimental Research Shows a Positive Relationship between Working Capital Management and Corporate Performance

Although the majority of empirical evidence showed a statistically significant and negative relationship between working capital management and corporate performance, there were some other experimental studies that revealed a positive relationship between the two.

Gill et al. (2010![]() ) studied the relationship between WCM and CP when surveying 88 companies listed on the New York stock exchange from 2005 to 2007. The research results found a positive relationship between the CCC and the company's profitability. This showed that companies could increase operational efficiency by increasing the CCC.

) studied the relationship between WCM and CP when surveying 88 companies listed on the New York stock exchange from 2005 to 2007. The research results found a positive relationship between the CCC and the company's profitability. This showed that companies could increase operational efficiency by increasing the CCC.

Sharma and Kumar (2011![]() ) studied the impact of working capital on the profitability ratio of 263 listed companies on the Bombay Stock Exchange from 2000 to 2008 and analyzed the data with the multi-factor regression of OLS. The research results found a positive correlation between WCM (receivables period, CCC) and the company's profits. This may stem from the fact that the Indian market is an emerging market. In order to increase competitiveness, Indian companies expand their sales policies to attain more customers.

) studied the impact of working capital on the profitability ratio of 263 listed companies on the Bombay Stock Exchange from 2000 to 2008 and analyzed the data with the multi-factor regression of OLS. The research results found a positive correlation between WCM (receivables period, CCC) and the company's profits. This may stem from the fact that the Indian market is an emerging market. In order to increase competitiveness, Indian companies expand their sales policies to attain more customers.

Meanwhile, Akinlo and Olufisayo (2011![]() ) studied the effect of working capital on the profitability of 66 Nigerian enterprises from 1999 to 2007. Experimental results showed a positive relationship between the inventory period, receivables period and the CCC with business profitability. Therefore, businesses could create value for shareholders by increasing the level of commercial credit to customers and increasing inventory reserves to the reasonable extent. In addition, the research results also showed a negative relationship between the payable period and the business profitability, which was in line with the fact that businesses with low profitability often take more time to pay off debt.

) studied the effect of working capital on the profitability of 66 Nigerian enterprises from 1999 to 2007. Experimental results showed a positive relationship between the inventory period, receivables period and the CCC with business profitability. Therefore, businesses could create value for shareholders by increasing the level of commercial credit to customers and increasing inventory reserves to the reasonable extent. In addition, the research results also showed a negative relationship between the payable period and the business profitability, which was in line with the fact that businesses with low profitability often take more time to pay off debt.

Baveld (2012![]() ) studied the relationship between working capital management and the profits of 37 largest companies in the Netherlands from 2004 to 2006 and the financial crisis of 2008 and 2009. Experimental results showed a positive correlation between the receivables period and the company’s profits. In the crisis period, these companies used sales policies to help customers to overcome the difficult time. In addition to increasing prestige for the company, this line of customers was also a source of revenue growth in the future when the economy recovered.

) studied the relationship between working capital management and the profits of 37 largest companies in the Netherlands from 2004 to 2006 and the financial crisis of 2008 and 2009. Experimental results showed a positive correlation between the receivables period and the company’s profits. In the crisis period, these companies used sales policies to help customers to overcome the difficult time. In addition to increasing prestige for the company, this line of customers was also a source of revenue growth in the future when the economy recovered.

3.3. Experimental Study Shows Nonlinear Relationship between Working Capital Management and Corporate Performance

Most of the empirical results from previous research believed that working capital management has an important impact on a company's profitability. However, this impact is both positive and negative.

In the first scenario, working capital management has a positive impact on corporate performance. There are many ways to explain this relationship. First, investing in increasing inventory can increase a company’s profitability. Ordering more inventory will help businesses get discounts from suppliers, reducing the cost of goods and services. When prices of raw materials fluctuate erratically, large inventory reserves help businesses stabilize input costs. In addition, large inventory reserves also help businesses to prevent disruption in the production process that can lead to failing to meet the pre-signed contracts and losing credibility with partners. When the product is scarce or the demand suddenly increases, enterprises will not lose any orders.

Second, increasing the level of commercial credit can help businesses to increase sales. Customers can consider the line of credit as appealing as a discount, which encourages them to buy goods and services at the time of low demand, helping businesses have good relationships with customers by allowing them some time before the final payment. Since commercial credit reduces information asymmetry between buyers and sellers, it is an important supplier selection criterion when it is impossible to distinguish the differences between products.

Finally, from the point of view of the accounts payable, early payments to suppliers will help businesses receive more discounts. Businesses delaying or paying suppliers late will cause suppliers to stop delivery, disrupting the production process and adversely affecting the performance of the businesses.

In the second scenario, investing in too much working capital causes an adverse impact on the corporate performance. When working capital is low, the increase in working capital which is based on internal funding at low cost, leads to an increase in business efficiency. When companies aggressively increase working capital and exhaust the internal financial resources, companies will have to rely on external funding and increase the cost of financing. The excessive increase in inventory reserves makes other expenses soar, such as warehousing, insurance and security costs. Additionally, using debt to invest too much in floating capital, means businesses face more credit risks which then increases the cost of financial exhaustion and increases the risk of bankruptcy. A high level of working capital means corporate assets are concentrated in working capital and may hinder the company's ability to participate in valuable projects.

The positive and negative effects of WCM on CP show that investing wisely in working capital can only help businesses increase profitability to a certain level. If the working capital of the enterprise exceeds this certain level, the increase in working capital will adversely affect the profitability of the business.

Based on the above arguments, some studies suggest that the relationship between working capital management and corporate performance is a nonlinear relationship (an inverted U shape) instead of a linear relationship. There exists an optimal working capital to maximize the performance of the business.

The study of Baños‐Caballero et al. (2010![]() ) uses the samples of 4,076 small and medium non-financial companies in Spain between 2001 and 2005. The main goal of the study is to analyze and determine the factors that affect the cash conversion cycle for small and medium-sized companies to find the target cash cycle length in which the profit of the business is maximized. The research results showed that the CCC is longer for older and larger cash-flow-companies.

) uses the samples of 4,076 small and medium non-financial companies in Spain between 2001 and 2005. The main goal of the study is to analyze and determine the factors that affect the cash conversion cycle for small and medium-sized companies to find the target cash cycle length in which the profit of the business is maximized. The research results showed that the CCC is longer for older and larger cash-flow-companies.

Similar to that idea, Baños-Caballero et al. (2012![]() ) continued to expand the study of the relationship between working capital management and company profits for 1,008 medium and large companies in Spain from 2002 to 2007. Unlike previous studies, this paper examined the nonlinear relationship between WCM and CP to test the profit and risk trade-offs between different working capital strategies. The results showed that there is a concave relationship between WCM and CP, which means that there will be optimal working capital for companies to balance the benefits, costs and maximize the company’s value. In addition, the study has done a solid test of the above results to make sure that profits will decrease as working capital moves away from the optimal level.

) continued to expand the study of the relationship between working capital management and company profits for 1,008 medium and large companies in Spain from 2002 to 2007. Unlike previous studies, this paper examined the nonlinear relationship between WCM and CP to test the profit and risk trade-offs between different working capital strategies. The results showed that there is a concave relationship between WCM and CP, which means that there will be optimal working capital for companies to balance the benefits, costs and maximize the company’s value. In addition, the study has done a solid test of the above results to make sure that profits will decrease as working capital moves away from the optimal level.

Most recently, Baños-Caballero et al. (2014![]() ) used the research sample of 258 UK businesses from 2001 to 2007, examining the relationship between WCM and CP. With the same approach of Baños-Caballero et al. (2012

) used the research sample of 258 UK businesses from 2001 to 2007, examining the relationship between WCM and CP. With the same approach of Baños-Caballero et al. (2012![]() ), Baños-Caballero et al. (2014

), Baños-Caballero et al. (2014![]() ) used Tobin's q to measure corporate performance instead of traditional profit measures, because Tobin's q reflects expectations about the market value of company profits. In fact, their experimental results found a nonlinear relationship (inverted U shape) between WCM and CP, proving that there exists an optimal working capital level at which the equilibrium between the cost and benefit of WCM can maximize operational efficiency for businesses.

) used Tobin's q to measure corporate performance instead of traditional profit measures, because Tobin's q reflects expectations about the market value of company profits. In fact, their experimental results found a nonlinear relationship (inverted U shape) between WCM and CP, proving that there exists an optimal working capital level at which the equilibrium between the cost and benefit of WCM can maximize operational efficiency for businesses.

3.4. Experimental Study for the Nonlinear Relationship between Working Capital Management and Corporate Performance under the Impact of Financial Constraints

The study of Baños-Caballero et al. (2014![]() ) used various financial constraint measures in the form of dividends, cash flows, to check the optimal level of working capital between any company with and without financial restrictions. The results showed that this optimal level was lower for companies with financial constraints. In particular, allowing the reaffirmation of previous research results, they found that investment decisions in working capital depended on the availability of internal funding, external financing costs, capital market access and the company's financial situation. Modigliani and Miller (1958

) used various financial constraint measures in the form of dividends, cash flows, to check the optimal level of working capital between any company with and without financial restrictions. The results showed that this optimal level was lower for companies with financial constraints. In particular, allowing the reaffirmation of previous research results, they found that investment decisions in working capital depended on the availability of internal funding, external financing costs, capital market access and the company's financial situation. Modigliani and Miller (1958![]() ) argued that in the ideal world, companies could always get external funding without encountering any obstacles, so their investment was not dependent on the availability of internal capital. However, the capital market is not perfect due to information asymmetry and representative costs. Therefore, the cost of using external funds is usually higher than that of internal funds (Jensen and Meckling, 1976

) argued that in the ideal world, companies could always get external funding without encountering any obstacles, so their investment was not dependent on the availability of internal capital. However, the capital market is not perfect due to information asymmetry and representative costs. Therefore, the cost of using external funds is usually higher than that of internal funds (Jensen and Meckling, 1976![]() ). When businesses face financial constraints with limited internal funding, in order to increase working capital, enterprises are forced to reach for external funding at higher costs. This can contribute to reducing the business performance. Therefore, when increasing working capital, it will cost more for enterprises that are facing financial constraints than enterprises with less financial constraints. This leads to lowering working capital levels for businesses facing financial constraints compared to the ones that are not.

). When businesses face financial constraints with limited internal funding, in order to increase working capital, enterprises are forced to reach for external funding at higher costs. This can contribute to reducing the business performance. Therefore, when increasing working capital, it will cost more for enterprises that are facing financial constraints than enterprises with less financial constraints. This leads to lowering working capital levels for businesses facing financial constraints compared to the ones that are not.

In order to assess whether the above comments are appropriate when applied to research practice in Vietnam, where the capital market is not as developed as the countries in previous research papers, this study will perform a test of the effect of financial constraints on the nonlinear relationship between WCM and CP to help corporate managers come up with reasonable working capital management strategies, based on their accessibility to capital.

4. RESEARCH METHODS

4.1. Database

The research data is taken from the STOXPLUS websites, including the financial data on the audited financial statements, the number of outstanding shares and the stock prices of the listed companies on Vietnam Stock Exchange for ten years, from 2009 to 2018. Companies in the selected sample were active during the study period. The study excluded companies that lacked financial data, did not have enough data, and companies operating in the financial sector such as banks, insurance companies, securities companies and investment funds. Financial companies have their own specificity so it is difficult to determine the components of working capital. The final sample is presented in Table 1.

Industry/ Year |

RE and constructions |

Technology |

Industrial |

Services |

Consumer goods |

Energy |

Agriculture |

Raw materials |

Health |

Total |

2009 |

170 |

13 |

46 |

55 |

40 |

30 |

39 |

43 |

15 |

451 |

2010 |

185 |

15 |

54 |

61 |

43 |

36 |

41 |

48 |

17 |

500 |

2011 |

186 |

14 |

57 |

60 |

42 |

34 |

43 |

49 |

18 |

503 |

2012 |

185 |

16 |

61 |

61 |

40 |

35 |

46 |

52 |

18 |

514 |

2013 |

192 |

16 |

65 |

64 |

41 |

37 |

50 |

56 |

20 |

541 |

2014 |

196 |

20 |

67 |

65 |

46 |

39 |

51 |

56 |

18 |

558 |

2015 |

206 |

21 |

73 |

66 |

47 |

39 |

53 |

62 |

19 |

586 |

2016 |

208 |

20 |

72 |

64 |

46 |

43 |

49 |

57 |

19 |

578 |

2017 |

216 |

22 |

75 |

67 |

47 |

40 |

49 |

56 |

19 |

591 |

2018 |

201 |

20 |

72 |

64 |

40 |

45 |

49 |

52 |

18 |

561 |

Total |

1,945 |

177 |

642 |

627 |

432 |

378 |

470 |

531 |

181 |

5,383 |

Source: Author collected from STOXPLUS.

4.2. Research Models and Variables

In order to answer the research question, we used three different models. The first model studied the effects of WCM through the CCC and the NTC on CP (measured by ROA and Tobin’s q). The second model studied the impact of WCM on CP by finding a nonlinear relationship (inverted U shape), meaning that there would be an optimal working capital level to balance benefits and costs and maximize the performance of the company. The third model was used to assess the impact of financial constraints on the nonlinear relationship between WCM and CP, and whether there was a difference between the optimal working capital for the company with and without financial constraints.

4.2.1. Model to Study the Relationship between Working Capital Management and Corporate Performance

Working capital management was based on the CCC and the NTC. Some other variables were included in the regression model to control the effects of other factors on CP. Specifically, they were business size variables (SIZE), financial leverage (LV), growth opportunities (GROWTH), and liquidity coverage ratio (CR). Therefore, the specific research model was proposed as follows:

The measured variables in the model are shown in Table 2.

Table-2. Summary of variables measurement and hypotheses in the research model.

| Variables | Type | Code | Measurement | Expected sign |

| Corporate performance | Dependent | ROA | ROA = Net income after taxes/Total assets | |

| Dependent | Tobin’s q | Tobin’s q = (Market value + Total liabilities)/Total assets | ||

| Cash conversion cycle | Independent | CCC | Average receivables * 365 / Revenue + Average inventory * 365 / Cost of goods - Average payables * 365 / Cost of goods | +/- |

| Net trade cycle | Independent | NTC | (Average accounts receivable + Average inventory - Average payables) * 365 / Revenue | +/- |

| Business size | Controlled | SIZE | Log (Total assets) | + |

| Capital structure | Controlled | LV | Total liabilities/ Total assets | - |

| Sales growth | Controlled | GROWTH | (Salest - Salest-1)/ Sales t | + |

| Liquidity coverage ratio | Controlled | CR | Short term assets/ Short term liabilities | + |

4.2.2. Model to Study the Nonlinear Relationship between Working Capital Management and Corporate Performance

According to previous studies of Baños-Caballero et al. (2014![]() ) it was possible that the relationship between WCM and CP is a nonlinear relationship (inverted U shape). Therefore, this study was conducted to test whether there was a nonlinear (inverted U-shaped) relationship between WCM and CP of businesses in Vietnam, meaning an optimal working capital level at which the business can balance costs and benefits in WCM to maximize CP. Based on the study of the authors, the research model used quadratic functions to check the nonlinear relationship. WCM was based on the CCC and the squared cash conversion cycle (CCC2); and the NTC and the squared net trade cycle (NTC2) were used to verify the nonlinear relationship between WCM and CP. Therefore, the model of two specific studies was proposed as follows:

) it was possible that the relationship between WCM and CP is a nonlinear relationship (inverted U shape). Therefore, this study was conducted to test whether there was a nonlinear (inverted U-shaped) relationship between WCM and CP of businesses in Vietnam, meaning an optimal working capital level at which the business can balance costs and benefits in WCM to maximize CP. Based on the study of the authors, the research model used quadratic functions to check the nonlinear relationship. WCM was based on the CCC and the squared cash conversion cycle (CCC2); and the NTC and the squared net trade cycle (NTC2) were used to verify the nonlinear relationship between WCM and CP. Therefore, the model of two specific studies was proposed as follows:

4.2.3. Model to Study the Effect of Financial Constraints on the Nonlinear Relationship between Working Capital Management and Corporate Performance

In this section, we continued to test whether there as a difference between the optimal working capital level for enterprises that were facing financial constraints and for those that were less likely to face financial constraints. In this section, the research model was developed based on the model in Equation 2, by combining a DFC dummy variable (distinguishing between enterprises facing financial constraints and ones that were not) on two criteria of the CCC and the NTC and the squared cash conversion cycle (CCC2) and the squared net trade cycle (NTC2). These two criteria were directly related to determining the optimal working capital of the business. Therefore, the research model used had the following form:

By developing the above Equation 3, enterprises that were less likely to face financial constraints have the extreme point of the NTC of –β1 / 2β2, which was also their optimal working capital. As for businesses facing financial constraints, there was an extreme point of the NTC equalling - (β1 + δ1) / 2 (β2 + δ2), which was also their optimal working capital.

DFC: This was a financial dummy variable that had a value of 1 for businesses facing financial constraints and a value of 0 for businesses that faced 0 financial constraints. There were a number of measures to limit the financial constraints used in previous studies to distinguish between businesses that were facing financial constraints and those that were not. However, it is still controversial to determine which criteria is the best to use. Therefore, this paper classified companies according to the following financial constraints:

Dividend payment: Financially constrained enterprises tend not to pay dividends (or pay low dividends) to reduce the risk of future internal funding shortages and reduce the obligation to mobilize external capital. Based on research by Fazzari et al. (1988![]() ), Almeida et al. (2004

), Almeida et al. (2004![]() ), and Faulkender and Wang (2006

), and Faulkender and Wang (2006![]() ) this study classified the level of financial constraints of enterprises according to the dividend payout ratio (Dividends/ Par value). Therefore, companies with a higher dividend payout ratio than the median of the sample were less likely to be financially constrained compared to firms with a smaller dividend payout ratio. Enterprises with a high dividend payout ratio above the median level corresponded to a DFC of 0, and companies in contrast had a DFC of 1.

) this study classified the level of financial constraints of enterprises according to the dividend payout ratio (Dividends/ Par value). Therefore, companies with a higher dividend payout ratio than the median of the sample were less likely to be financially constrained compared to firms with a smaller dividend payout ratio. Enterprises with a high dividend payout ratio above the median level corresponded to a DFC of 0, and companies in contrast had a DFC of 1.

Cash flow: According to Moyen (2004![]() ) enterprises often prioritize the use of cash flow to finance investment activities. A decline in cash flow will lead to a reduction in investment. Therefore, enterprises with low cash flow were more likely to be facing financial constraints (DFC close to 1). Enterprises with a greater cash flow than the average of the sample were less likely to face financial constraints (DFC value of 0). The cash flow indicator was determined by the ratio of income before tax and interest plus the depreciation divided by the total assets.

) enterprises often prioritize the use of cash flow to finance investment activities. A decline in cash flow will lead to a reduction in investment. Therefore, enterprises with low cash flow were more likely to be facing financial constraints (DFC close to 1). Enterprises with a greater cash flow than the average of the sample were less likely to face financial constraints (DFC value of 0). The cash flow indicator was determined by the ratio of income before tax and interest plus the depreciation divided by the total assets.

4.3. Method of Estimation

We use the generalized least squares method (GLS), which has the advantage of overcoming the defects of autocorrelation, variance change, etc. so the research results were more reliable.

5. RESEARCH RESULTS AND DISCUSSION

Descriptive statistics provide an overview of the data, detect the differences observed in the sample size, and are presented in Table 3. The results indicated the scope, mean value and standard deviation of the CCC and the NTC in this study. The CCC from 2009 to 2018 averaged 216.217 days, with a standard deviation of 288.122 days with the lowest value 0.038 days and the highest 2,371.685 days. Meanwhile, the average NTC was 193.453 days lower than the CCC and the standard deviation was 238.98 days with the lowest value 0.339 days and the highest 3,113.426 days.

Table-3. Descriptive statistics.

Variables |

Observations |

Average |

Standard deviation |

Min. |

Max. |

CCC |

5383 |

216.217 |

288.122 |

0.038 |

2371.685 |

NTC |

5383 |

193.453 |

238.980 |

0.339 |

3113.426 |

Source: Authors’ calculation from Stata 14.0.

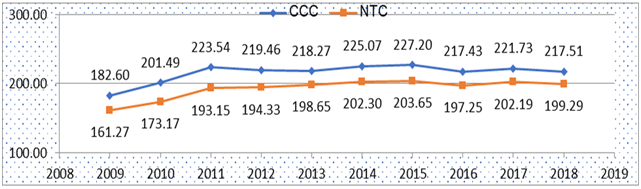

Figure 1 shows that the CCC and the NTC have fluctuations from 2009 to 2018. Specifically, from 2009 to 2011, the CCC saw a sharp increase from 182.60 days in 2009 to 223.54 days in 2011; then, there were several steady increases/ decreases before it remained at 220 days. The fluctuation of NTC was similar, in 2009 it was 161.27 days and after increasing to 193.15 days, it maintained a slight fluctuation around 200 days.

Figure-1. Cash conversion cycle, net trade cycle in the period 2009-2018.

Source: Authors’ calculation from Stata 14.0.

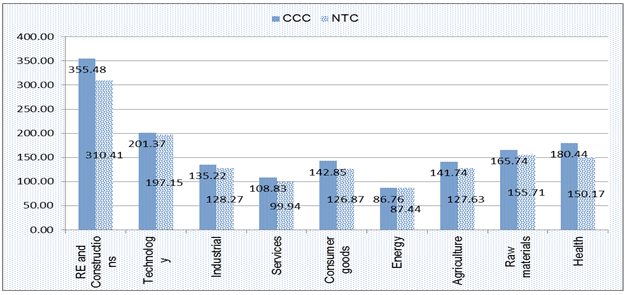

Figure-2. Cash conversion cycle, net trade cycle between sectors.

Source: Authors’ calculation from Stata 14.0.

Figure 2 shows that the cash conversion cycle and the net trade cycle differed significantly between sectors. The industry with the largest CCC and NTC was the real estate and construction industry with the respective rotation of 355.48 days and 310.41 days, followed by the technology industry. In contrast, the industry with the lowest CCC and NTC was the energy sector with 86.76 days, 87.44 days respectively, followed by the services industry.

Statistics in Table 4 show that the average return on total assets (ROA) was 6.0%, and the average Tobin’s Q was 1,087. Because the CCC and the NTC had a value of greater than 0 and a large variation, the study used logarithms of the CCC and the NTC. The value after the logarithms of the CCC and the NTC were 4.789 and 4.749 respectively. The business size (SIZE) measured in logarithms of the average total assets was 11.716; enterprises with financial structure (LV) were 50.1% on average; the revenue growth rate (GROWTH) was 26.7%; and liquidity coverage ratios (CR) were 2.115.

Table-4. Descriptive statistics.

Variables |

Observations |

Average |

Standard deviation |

Min. |

Max. |

roa |

5383 |

0.069 |

0.080 |

-0.520 |

0.810 |

tobinq |

5383 |

1.087 |

0.610 |

0.216 |

4.495 |

logCCC |

5383 |

4.789 |

1.159 |

-3.271 |

7.771 |

logNTC |

5383 |

4.749 |

1.051 |

-1.083 |

8.043 |

SIZE |

5383 |

11.715 |

0.619 |

10.275 |

13.439 |

LV |

5383 |

0.501 |

0.219 |

0.009 |

0.993 |

GROWT |

5383 |

0.267 |

0.894 |

-0.757 |

7.255 |

CR |

5383 |

2.115 |

1.964 |

0.388 |

19.032 |

Source: Authors’ calculation from Stata 14.0.

roa |

tobinq |

logCCC |

logNTC |

SIZE |

LV |

GROWT |

CR |

|

roa |

1 |

|||||||

tobinq |

0.3804 |

1 |

||||||

logCCC |

-0.2335 |

-0.1817 |

1 |

|||||

logNTC |

-0.274 |

-0.2089 |

0.9769 |

1 |

||||

SIZE |

-0.0562 |

0.0026 |

0.108 |

0.1164 |

1 |

|||

LV |

-0.4095 |

-0.1611 |

0.1267 |

0.1531 |

0.3274 |

1 |

||

GROWT |

0.0781 |

-0.0161 |

0.0528 |

0.0649 |

0.0492 |

0.0063 |

1 |

|

CR |

0.2742 |

0.1527 |

0.0211 |

0.0013 |

-0.1944 |

-0.6043 |

0.0053 |

1 |

Source: Authors’ calculation from Stata 14.0.

Table-6. Model 1 regression results.

ROA(1a) |

Tobin’s q(1b) |

ROA(1c) |

Tobin’s q(1d) |

||||

logCCC |

-0.0140*** |

-0.0946*** |

|||||

[-16.53] |

[-13.39] |

||||||

logNTC |

-0.0180*** |

-0.119*** |

|||||

[-19.36] |

[-15.25] |

||||||

SIZE |

0.0126*** |

0.0743*** |

0.0129*** |

0.0759*** |

|||

[7.63] |

[5.39] |

[7.87] |

[5.54] |

||||

LV |

-0.136*** |

-0.261*** |

-0.132*** |

-0.234*** |

|||

[-23.52] |

[-5.40] |

[-22.91] |

[-4.86] |

||||

GROWT |

0.00771*** |

-0.00703 |

0.00811*** |

-0.00454 |

|||

[7.13] |

[-0.78] |

[7.56] |

[-0.51] |

||||

CR |

0.00292*** |

0.0356*** |

0.00307*** |

0.0364*** |

|||

[4.70] |

[6.88] |

[4.99] |

[7.07] |

||||

_cons |

0.0483** |

0.727*** |

0.0608*** |

0.804*** |

|||

[2.54] |

[4.58] |

[3.21] |

[5.08] |

||||

N |

5383 |

5383 |

5383 |

5383 |

|||

| t statistics in brackets * p<0.1, ** p<0.05, *** p<0.01 | |||||||

Source: Authors’ calculation from Stata 14.0.

According to Table 5, the analysis of correlation coefficients was aimed at examining the close relationship between two or more variables, with the absolute value of the correlation coefficients of 1 showing a rather close correlation. If the correlation coefficient was lower than 0.8, the discriminant value existed between the two variables. The correlation coefficients between variables fluctuated in the range of -0.4095 to 0.3274 (lower than the condition index of 0.8) were less likely to occur multicollinearity.

Table-7. Model 2 regression results.

ROA(2a) |

Tobin’s q(2b) |

ROA(2c) |

Tobin’s q(2d) |

||||

logCCC |

0.0118*** |

0.0301 |

|||||

[3.70] |

[1.13] |

||||||

logCCC2 |

-0.00296*** |

-0.0143*** |

|||||

[-8.41] |

[-4.86] |

||||||

logNTC |

0.0257*** |

0.0334 |

|||||

[5.30] |

[0.82] |

||||||

logNTC2 |

-0.00479*** |

-0.0167*** |

|||||

[-9.18] |

[-3.79] |

||||||

SIZE |

0.0140*** |

0.0811*** |

0.0141*** |

0.0802*** |

|||

[8.49] |

[5.87] |

[8.66] |

[5.84] |

||||

LV |

-0.135*** |

-0.253*** |

-0.131*** |

-0.229*** |

|||

[-23.39] |

[-5.25] |

[-22.83] |

[-4.76] |

||||

GROWT |

0.00794*** |

-0.00588 |

0.00835*** |

-0.00369 |

|||

[7.39] |

[-0.65] |

[7.84] |

[-0.41] |

||||

CR |

0.00313*** |

0.0366*** |

0.00332*** |

0.0372*** |

|||

[5.06] |

[7.08] |

[5.43] |

[7.24] |

||||

_cons |

-0.021 |

0.392** |

-0.0493** |

0.421** |

|||

[-1.02] |

[2.27] |

[-2.21] |

[2.25] |

||||

N |

5383 |

5383 |

5383 |

5383 |

|||

t statistics in brackets * p<0.1, ** p<0.05, *** p<0.01 |

|||||||

Source: Authors’ calculation from Stata 14.0.

The results of the study in Table 6 show that WCM, through the CCC and the NTC, had a negative impact on CP and is significant at the 1% level. The CCC and the NTC represented the time since the company paid for raw materials until the money was collected from customers’ purchases of final products. The shorter the CCC and the NTC were, the higher the CP.

With model 1, using the linear regression model, the study considered whether the greater the CCC and NTC, the lower the CP. In order to find the answer to this question, the study continued to analyze the data in the form of nonlinear regression according to model 2. The regression results of model 2 are presented in Table 7.

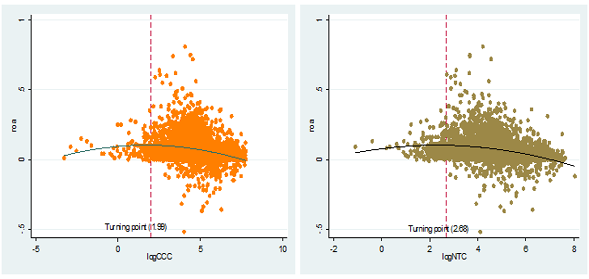

The results of the GLS regression model Table 7 for model 2a and model 2c show that the CCC and the NTC positively impact on CP (measured by ROA). Particularly, if the CCC and the NTC are extended by one unit (calculated according to logarithms), the CP (according to ROA) will increase by 0.0118, 0.0257 with 1% statistical significance. Meanwhile, the CCC2 has the opposite impact on CP (measured by ROA).

The sign of the coefficients β1 (β1> 0) and β2 (β2 <0) implied that the relationship between the CCC, the NTC and CP (measured by ROA) is a Parabolic relationship with an inverted U-shape. The maximum value of the CCC (inflection point) was equal to -β1/2β2 = 1.99; and the maximum value of the NTC (inflection point) was equal to -β1/2β2 = 2.68 as shown in Figure 3. Initially when the CCC and the NTC are extended, it will contribute to the increase of CP. However, when the NTC exceeds the threshold of 1.99 and 2.68, it will cause the opposite effect on CP. It is obvious that when the working capital level is higher than the value of the inflection point, increasing working capital contributes to decreased corporate performance and vice versa. The increase in CP can be explained by expanding commercial credit to encourage business operations (Brennan et al., 1988![]() ), (Petersen and Rajan, 1997

), (Petersen and Rajan, 1997![]() ) which encourages customers to buy more goods at the time of low demand (Emery, 1984

) which encourages customers to buy more goods at the time of low demand (Emery, 1984![]() ) and allows buyers to evaluate the quality of products and services before final payment (Smith, 1987

) and allows buyers to evaluate the quality of products and services before final payment (Smith, 1987![]() ). However, it does not mean that the continuous increase in working capital will create a continuous increase in CP. When the level of working capital exceeds the optimal level (inflection point), it creates the opposite effect on CP. Maintaining high inventories can increase storage, insurance and security costs (Kim and Chung, 1990

). However, it does not mean that the continuous increase in working capital will create a continuous increase in CP. When the level of working capital exceeds the optimal level (inflection point), it creates the opposite effect on CP. Maintaining high inventories can increase storage, insurance and security costs (Kim and Chung, 1990![]() ). Maintaining high working capital raises the need for external capital, so the company may incur higher interest payments (Kieschnick et al., 2013

). Maintaining high working capital raises the need for external capital, so the company may incur higher interest payments (Kieschnick et al., 2013![]() ) and possibly higher credit risk. However, keeping working capital at a high level means money is being detained instead of investing in other attractive projects that could help increase CP.

) and possibly higher credit risk. However, keeping working capital at a high level means money is being detained instead of investing in other attractive projects that could help increase CP.

Figure-3. Optimal WCM to CP (measured by ROA).

Source: Authors’ calculation from Stata 14.0.

When examining model 2b and model 2d, the CCC and the NTC were positively related, as measured by Tobin’s q, yet were not statistically significant. However, the CCC2 and NTC2 values were inversely related to CP as measured by Tobin’s q and statistically significant at the 1% level.

In addition, from the regression results in Table 7, the study also found evidence of controlled variables affecting CP. The variables SIZE, GROWTH, and CR had positive effects on CP at the 1% significance level. These results also agreed with the studies of Dang et al. (2018![]() ) and Ha et al. (2019

) and Ha et al. (2019![]() ). The variable LV had the opposite effect on CP (measured by ROA) at the 1% significance level, which agreed with the study by Dang et al. (2019

). The variable LV had the opposite effect on CP (measured by ROA) at the 1% significance level, which agreed with the study by Dang et al. (2019![]() ).

).

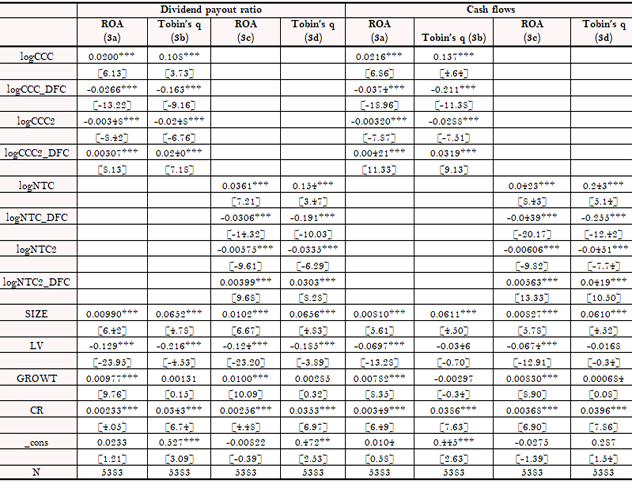

Table 8 shows the regression results for businesses with less financial constraints. This result once again confirmed the inverted-U relationship between WCM and CP. The CCC and the NTC had a statistically significant impact on CP (measured by ROA and Tobin’s q) in both financial constraint models classified according to dividend payout ratio and cash flow. Meanwhile, the CCC2 and the NTC2 variables had the opposite relationship with CP in both financial constraint models.The CCC*DFC and the NTC*DFC had the same meaning as the CCC and the NTC. They had a negative impact on CP and ere statistically significant in both financial constraint models. The CCC2*DFC and the NTC2*DFC ere statistically significant in both financial constraint models and had a positive impact on CP (measured by ROA and Tobin’s q).

After determining the value of working capital to maximize CP and to the balance of costs and benefits, the study examined whether the optimal level of capital varied among enterprises that had different financial situation or not. Equation - β1/2β2 measured the optimal working capital of a company that was less likely to be financially constrained, and - (β1 + δ1) / 2 (β2 + δ2) measured the optimal working capital level of an enterprise that was more likely to be financially constrained.

6. CONCLUSIONS AND RECOMMENDATIONS

6.1. Conclusion

This paper examined the empirical relationship between working capital management and corporate performance, and incorporated the financial constraint factors in studying the above relationship for listed non-financial companies in Vietnam from 2009 to 2018. The key difference in this study was the use of GLS model to control autocorrelation and constant errors that could seriously affect the results of previous studies in Vietnam. Initial research questions were answered. First, this paper showed that the relationship between WCM and CP was not merely a linear relationship as many previous studies have shown. The relationship between them is nonlinear (inverted U shape). This means that there is an optimal working capital level that balances benefits, costs and maximizes the corporate performance. As the current working capital deviates from the optimal working capital, the efficiency of the company decreases, which was consistent with the previous study by Baños‐Caballero et al. (2010![]() ) for the medium and small companies in Spain; and research by Baños-Caballero et al. (2014

) for the medium and small companies in Spain; and research by Baños-Caballero et al. (2014![]() ) for companies in the UK. This supports the idea that business opportunities will open up by increasing commercial credit for customers. Increasing inventory makes input costs less subject to price fluctuations and preventing production disruption. Investing heavily in working capital also means reducing the accounts payable to suppliers, which can help businesses earn early payment discounts, while reducing input costs and tightening close relationships with suppliers. However, when the level of working capital increases to a high level exceeding the optimal level, it will cause adverse impacts on CP due to additional cost factors such as warehouse rental costs, insurance costs and security expenses. Keeping working capital too high also involves increasing interest expenses, credit risks and higher bankruptcy probabilities and at the same time losing other investment opportunities that may bring profit for the businesses. Therefore, managers should manage working capital effectively, keeping it close to the optimal level and try to avoid any adverse impact of deviating from this optimal capital level.

) for companies in the UK. This supports the idea that business opportunities will open up by increasing commercial credit for customers. Increasing inventory makes input costs less subject to price fluctuations and preventing production disruption. Investing heavily in working capital also means reducing the accounts payable to suppliers, which can help businesses earn early payment discounts, while reducing input costs and tightening close relationships with suppliers. However, when the level of working capital increases to a high level exceeding the optimal level, it will cause adverse impacts on CP due to additional cost factors such as warehouse rental costs, insurance costs and security expenses. Keeping working capital too high also involves increasing interest expenses, credit risks and higher bankruptcy probabilities and at the same time losing other investment opportunities that may bring profit for the businesses. Therefore, managers should manage working capital effectively, keeping it close to the optimal level and try to avoid any adverse impact of deviating from this optimal capital level.

Second, the paper also pointed out the sensitivity of the WCM – CP relationship under various financial constraint conditions. The results showed that the nonlinear relationship still exists and that the optimal level of capital of the company that is more likely to be financially constrained is smaller than those that are less likely to be financially constrained. The financial constraints that the company faces will limit the ability to access capital markets and will increase the cost of debt. As a result, businesses will face difficulties in attaining working capital. In contrast, when businesses have a strong financial background, it is easier for them to access the capital market at a cheaper cost. Thus, they can maintain a higher working capital level than businesses that suffer from financial constraints.

6.2. Recommendations

The research has many implications for business managers facing difficulties and information asymmetry in Vietnam stock market.

First, managers should focus on WCM, because they will bear higher costs when working capital levels move away from the optimal level. If that occurs, businesses would face an adverse effect on corporate performance through the loss of revenue or loss of possible discount from suppliers. It is possible to increase CP by optimizing the CCC and the NTC or in other words, managing working capital at optimal level. Good working capital management will increase liquidity and thus have positive impact on the company's financial position.

WCM can increase other forms of financing because credit institutions will consider and evaluate the company's balance sheet structure when making funding decisions. They will of course prioritize funding for companies with stronger financial management. It is also noted that the impact of WCM on CP depends very much on the specific characteristics of each enterprise as analyzed above, in terms of internal funding sources, financing costs when mobilizing external capital, capital market access and financial deprivation status. Therefore, business managers need to determine the financial situation of their business in order to control working capital investment in the most effective way.

Table-8 . Model 3 regression results.

t statistics in brackets * p<0.1, ** p<0.05, ***p<0.01.

Source: Authors’ calculation from Stata 14.0

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Afeef, M., 2011. Analyzing the impact of working capital management on the profitability of SME's in Pakistan. International Journal of Business and Social Science, 2(22): 173-183.

Akinlo, O. and O. Olufisayo, 2011. The effect of working capital on profitability of firms in Nigeria: Evidence from general method of moments (GMM). Asian Journal of Business and Management Sciences, 1(2): 130-135.

Almeida, H., M. Campello and M.S. Weisbach, 2004. The cash flow sensitivity of cash. The Journal of Finance, 59(4): 1777-1804.

Baños-Caballero, S., P.J. García-Teruel and P. Martínez-Solano, 2012. How does working capital management affect the profitability of Spanish SMEs? Small Business Economics, 39(2): 517-529. Available at: https://doi.org/10.1007/s11187-011-9317-8.

Baños-Caballero, S., P.J. García-Teruel and P. Martínez-Solano, 2014. Working capital management, corporate performance, and financial constraints. Journal of Business Research, 67(3): 332-338. Available at: https://doi.org/10.1016/j.jbusres.2013.01.016.

Baños‐Caballero, S., P.J. García‐Teruel and P. Martínez‐Solano, 2010. Working capital management in SMEs. Accounting & Finance, 50(3): 511-527. Available at: https://doi.org/10.1111/j.1467-629X.2009.00331.x.

Baveld, M.B., 2012. Impact of working capital management on the profitability of public listed firms in The Netherlands during the financial crisis (Master's Thesis, University of Twente).

Brealey, R.A., S.C. Myers and Allen, F. 2006. Corporate finance. New York: Irwin Mc Graw-Hill.

Brennan, M.J., V. Maksimovics and J. Zechner, 1988. Vendor financing. The Journal of Finance, 43(5): 1127-1141. Available at: https://doi.org/10.1111/j.1540-6261.1988.tb03960.x.

Ching, H.Y., A. Novazzi and F. Gerab, 2011. Relationship between working capital management and profitability in Brazilian listed companies. Journal of Global Business and Economics, 3(1): 74-86.

Dang, H.N., V.T.T. Vu, X.T. Ngo and H.T.V. Hoang, 2019. Study the impact of growth, firm size, capital structure, and profitability on enterprise value: Evidence of enterprises in Vietnam. Journal of Corporate Accounting & Finance, 30(1): 144-160. Available at: https://doi.org/10.1002/jcaf.22371.

Dang, N.H., D.C. Pham and T.B.H. Vu, 2018. Effects of financial statements information on firms’ value: Evidence from Vietnamese listed firms. Investment Management and Financial Innovations, 15(4): 210-218. Available at: 10.21511/imfi.15(4).2018.17.

Deloof, M., 2003. Does working capital management affect profitability of Belgian firms? Journal of Business Finance & Accounting, 30(3‐4): 573-588. Available at: https://doi.org/10.1111/1468-5957.00008.

Emery, G.W., 1984. A pure financial explanation for trade credit. Journal of Financial and Quantitative Analysis, 19(3): 271-285. Available at: https://doi.org/10.2307/2331090.

Faulkender, M. and R. Wang, 2006. Corporate financial policy and the value of cash. The Journal of Finance, 61(4): 1957-1990. Available at: https://doi.org/10.1111/j.1540-6261.2006.00894.x.

Fazzari, S., R.G. Hubbard and B. Petersen, 1988. Investment, financing decisions, and tax policy. The American Economic Review, 78(2): 200-205.

Ferreira, M.A. and A.S. Vilela, 2004. Why do firms hold cash? Evidence from EMU countries. European Financial Management, 10(2): 295-319. Available at: https://doi.org/10.1111/j.1354-7798.2004.00251.x.

Filbeck, G. and T.M. Krueger, 2005. An analysis of working capital management results across industries. American Journal of Business, 20(2): 11-20. Available at: https://doi.org/10.1108/19355181200500007.

Gill, A., N. Biger and N. Mathur, 2010. The relationship between working capital management and profitability: Evidence from the United States. Business and Economics Journal, 10(1): 1-9.

Ha, T.V., N.H. Dang, M.D. Tran, T.T. Van Vu and Q. Trung, 2019. Determinants influencing financial performance of listed firms: Quantile regression approach. Asian Economic and Financial Review, 9(1): 78-90. Available at: 10.18488/journal.aefr.2019.91.78.90.

Jensen, M.C. and W.H. Meckling, 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4): 305-360. Available at: https://doi.org/10.1016/0304-405x(76)90026-x.

Jose, M.L., C. Lancaster and J.L. Stevens, 1996. Corporate returns and cash conversion cycles. Journal of Economics and Finance, 20(1): 33-46. Available at: https://doi.org/10.1007/BF02920497.

Juan García-Teruel, P. and P. Martinez-Solano, 2007. Effects of working capital management on SME profitability. International Journal of Managerial Finance, 3(2): 164-177. Available at: https://doi.org/10.1108/17439130710738718.

Kieschnick, R., M. Laplante and R. Moussawi, 2013. Working capital management and shareholders’ wealth. Review of Finance, 17(5): 1827-1852. Available at: https://doi.org/10.1093/rof/rfs043.

Kim, Y.H. and K.H. Chung, 1990. An integrated evaluation of investment in inventory and credit: A cash flow approach. Journal of Business Finance & Accounting, 17(3): 381-389.

Lazaridis, I. and D. Tryfonidis, 2006. Relationship between working capital management and profitability of listed companies in the Athens stock exchange. Journal of Financial Management and Analysis, 19(1): 1-12.

Mansoori, D.E. and D. Muhammad, 2012. The effect of working capital management on firm’s profitability: Evidence from Singapore. Interdisciplinary Journal of Contemporary Research in Business, 4(5): 472-486.

Mathuva, D., 2010. The influence of working capital management components on corporate profitability. Research Journal of Business Management, 4(1): 1-11. Available at: https://doi.org/10.3923/rjbm.2010.1.11.

Miller, M.H. and D. Orr, 1966. A model of the demand for money by firms. The Quarterly Journal of Economics, 80(3): 413-435. Available at: https://doi.org/10.2307/1880728.

Modigliani, F. and M.H. Miller, 1958. The cost of capital, corporation finance and the theory of investment. The American Economic Review, 48(3): 261-297.

Moyen, N., 2004. Investment–cash flow sensitivities: Constrained versus unconstrained firms. The Journal of Finance, 59(5): 2061-2092. Available at: https://doi.org/10.1111/j.1540-6261.2004.00692.x.

Nobanee, H., M. Abdullatif and M. AlHajjar, 2011. Cash conversion cycle and firm's performance of Japanese firms. Asian Review of Accounting, 19(2): 147-156. Available at: https://doi.org/10.1108/13217341111181078.

Petersen, M.A. and R.G. Rajan, 1997. Trade credit: Theories and evidence. The Review of Financial Studies, 10(3): 661-691.

Richards, V.D. and E.J. Laughlin, 1980. A cash conversion cycle approach to liquidity analysis. Financial Management, 9(1): 32-38. Available at: http://www.jstor.org/stable/3665310.

Sharma, A. and S. Kumar, 2011. Effect of working capital management on firm profitability: Empirical evidence from India. Global Business Review, 12(1): 159-173. Available at: https://doi.org/10.1177/097215091001200110.

Shin, H.-H. and L. Soenen, 1998. Efficiency of working capital management and corporate profitability. Financial Practice and Education, 8(1): 37-45.

Smith, J.K., 1987. Trade credit and informational asymmetry. The Journal of Finance, 42(4): 863-872. Available at: https://doi.org/10.1111/j.1540-6261.1987.tb03916.x.

Tauringana, V. and G. Adjapong Afrifa, 2013. The relative importance of working capital management and its components to SMEs' profitability. Journal of Small Business and Enterprise Development, 20(3): 453-469. Available at: https://doi.org/10.1108/jsbed-12-2011-0029.

Tobin, J., 1956. The interest-elasticity of transactions demand for cash. The Review of Economics and Statistics, 38(5): 241-247.

Wang, Y.-J., 2002. Liquidity management, operating performance, and corporate value: Evidence from Japan and Taiwan. Journal of Multinational Financial Management, 12(2): 159-169. Available at: https://doi.org/10.1016/s1042-444x(01)00047-0.

Views and opinions expressed in this article are the views and opinions of the author(s), Asian Economic and Financial Review shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |