ARE THE ISLAMIC BANKS REALLY MORE PROFITABLE THAN THE CONVENTIONAL BANKS IN A FINANCIAL STABLE PERIOD?

1Researcher, Laboratory of Finance, Governance and Accounting, University of Sfax, Tunisia.

2Associate Professor of Accounting and Finance, Faculty of Economics and Management of Mahdia, Tunisia.

3Director of Finance, Governance and Accounting Laboratory, University of Sfax, Tunisia.

ABSTRACT

The international banking sector is dominated by the conventional banks but the global market share of the Islamic banks is increasing gradually. This study determines which model maximizes a bank’s profitability in several heterogeneous contexts and over a financial stable period (2010-2018). Most previous studies examined banking profitability in commercial conventional and Islamic banks providing a limited literature. We retained three categories for each type of banks (commercial, investment and universal) because of the predominance of these categories in the money market. Within the framework of this study, two samples were taken from two reference populations. Basic populations were composed of all active conventional and Islamic banks existing in the selected countries. The choice of the banks is limited to the countries whose banking structures incorporate simultaneously the two types of banks independently of the proportion of each system in each country banking market. We then reduced the size of each population focusing on qualitative and quantitative filtering criteria, so that each conventional bank had its Islamic equivalence in terms of capital and size in the same country. This restriction reduced the sample size to 63 large banks for each type. The two banks’ samples were selected from sixteen countries and were listed in different stock exchanges around the world. Consequently, the empirical results showed that the conventional banks were more profitable than the Islamic banks during the period of financial stability.

Keywords: Conventional banks, Islamic banks, Profitability, Comparative study, Financial stable period, Conditional data, Decisive banks choice.

JEL Classification: F33; G20; G21; G24; G30.

ARTICLE HISTORY: Received:31 May 2019 Revised:10 July 2019 Accepted:12 August 2019 Published:19 September 2019.

Contribution/ Originality:The study offers the first logical analysis that allows economic agents to differentiate between Conventional Banks (CBs) and Islamic Banks (IBs). It helps them choose the most profitable one based on a single parameter of profitability that reflects a targeted bank characteristic.

1. INTRODUCTION

The conventional and Islamic banking sectors currently play a crucial role of intermediary financing among economic agents worldwide. The governance of the banks’ profitability seems more crucial than in other industries. Poor governance of the banks’ profitability compared to competitors reflects a poor reputation, leading to heavy losses in market share. In this case, according to the directive provisions, management members feel a lack of confidence in the correct management of a bank's assets and liabilities, including deposits and credits (Teresa and Dolores, 2008![]() ). Systemic risk could in turn trigger a crisis of profitability in a banking system or in a bank that ends up destroying the banking fabric in a country or at the international level in the broad sense. The world of monetary exchange has given attention to the importance of controlling and monitoring bank profitability. In contrast, according to the literature review, comparative studies on profitability have revealed mixed results and are inconclusive. They are in some cases identical, but they are, in other cases, discordant or paradoxical.

). Systemic risk could in turn trigger a crisis of profitability in a banking system or in a bank that ends up destroying the banking fabric in a country or at the international level in the broad sense. The world of monetary exchange has given attention to the importance of controlling and monitoring bank profitability. In contrast, according to the literature review, comparative studies on profitability have revealed mixed results and are inconclusive. They are in some cases identical, but they are, in other cases, discordant or paradoxical.

Although in most cases the results of previous studies on the comparison between the profitability of Islamic and conventional banks are mixed or contradictory, through our study, we sought to answer definitively the following question: What type of banks, are the most profitable in this comparative framework?

This information makes it easier for economic agents and decision-makers to detect the best choices of financial backers in savings and financing when investing in a world of financial competitiveness. In addition, our results will help policymakers set better performance targets and enable bank managers to allocate capital more effectively to communicate a clear and definitive answer.

Our study provided an overview of the fragility, vulnerability and instability of conventional and Islamic banking systems, and makes a comparison between the two models. This research work makes it possible to achieve the following objective: establish a radical paradigm of choice between the banking profitabilities that allows us to review its degree of validity and develop more precise, decisive and well-argued conclusions.

As its first contribution to the financial literature, our study filled in the proposed gap. The second contribution of this study was the conditional methodological approach in the choice of the banks’ observations and a severe procedure of application of the statistical tests. Our third contribution was to make a comparison in a stable economic context in sixteen heterogeneous countries across three continents. The fourth contribution was that this study has a potentially powerful empirical demonstration and validation of our hypothesis. Size restriction has required the elimination of small banks that are generally unlisted and this systematically reduces the effect of the categorical homogeneity, the size, the extent of differences, and the particularities of banks structures on the profitability of each sample. In addition, we distinguished between the two types of banks by a very specific parameter of financial performance rarely taken alone in previous studies, and we used a single measure of profitability.

The rest of our comparative study is structured as follows: section two presents the concept of profitability in banks and literature review based on contradictory previous conclusions. Section three describes the methodology and data. Section four discusses the empirical results and gives the implications of the findings. Section five concludes the study.

2. LITERATURE REVIEW AND DEVELOPMENT OF HYPOTHESIS

2.1. Theoretical Approach of Bank Profitability

The history of banks has been marked by a list of successive crises. Following the subprime crisis, the global banking system has faced enormous losses (Stijn et al., 2011![]() ). Some recent developments in the financial economy have been deeply challenged by this crisis, leading to the bankruptcy of several financial institutions around the world (Rodney, 2007

). Some recent developments in the financial economy have been deeply challenged by this crisis, leading to the bankruptcy of several financial institutions around the world (Rodney, 2007![]() ; Loghod, 2008

; Loghod, 2008![]() ; Khamis and Senhadji, 2010

; Khamis and Senhadji, 2010![]() ; Parashar and Venkatesh, 2010

; Parashar and Venkatesh, 2010![]() ; Rashwan, 2010; 2012

; Rashwan, 2010; 2012![]() ; Merchant, 2012

; Merchant, 2012![]() ; Siraj and Pillai, 2012

; Siraj and Pillai, 2012![]() ; Al-smadi et al., 2013

; Al-smadi et al., 2013![]() ) . However, the spread of IBs around the world has prompted researchers to certify the validity of this financial model as an alternative to the conventional banking system, or at least to be well integrated as a completely needed alternative financial system (Iqbal, 2001

) . However, the spread of IBs around the world has prompted researchers to certify the validity of this financial model as an alternative to the conventional banking system, or at least to be well integrated as a completely needed alternative financial system (Iqbal, 2001![]() ; Shamsher et al., 2008

; Shamsher et al., 2008![]() ; Tayyebi, 2009

; Tayyebi, 2009![]() ; Kassim and Majid, 2010

; Kassim and Majid, 2010![]() ) . Hence, several reflections were conducted to explain which is the most profitable model and which generates more satisfaction to stakeholders (De-Jong et al., 2002

) . Hence, several reflections were conducted to explain which is the most profitable model and which generates more satisfaction to stakeholders (De-Jong et al., 2002![]() ; Loghod, 2008

; Loghod, 2008![]() ; Čihák and Hesse, 2010

; Čihák and Hesse, 2010![]() ; Gupta et al., 2013

; Gupta et al., 2013![]() ) .

) .

For a long time, the previous studies dealing with the profitability of IBs were simple research papers on the management of financial instruments inspired from other studies on CBs (Ariff and Khalid, 2000![]() ; Samad and Hassan, 2000

; Samad and Hassan, 2000![]() ). At the beginning, previous studies perpetually used proportional and approximate measures to evaluate the profitability of CBs. Subsequently, researchers adapted the same measures to estimate the profitability of IBs.

). At the beginning, previous studies perpetually used proportional and approximate measures to evaluate the profitability of CBs. Subsequently, researchers adapted the same measures to estimate the profitability of IBs.

The studies comparing the profitability of classical and Islamic banks were subdivided into two categories. The first stated that the joint existence of IBs alongside CBs could let the former operate with their full levels of returns. In fact, the decline in profitability was not only due to the mechanical and systemic inadequacies of IBs, but also to the competition imposed by the conventional banking market; the toxic and restrained financial operations of the conventional banking system; and the contradictions between the particular dimensions of the two banking segments that hindered the smooth functioning of IBs. This does not mean that the success and survival of IBs depends on the existence of a monopoly banking market. IBs can operate with minimal security effectiveness which guarantees its durability even in a conventional banking framework due to its operating system based on the mode of sharing profits and losses. In addition, the management of IBs and the selection of sectors or areas of activity is done judiciously (Rodney, 2007![]() ; Loghod, 2008

; Loghod, 2008![]() ; Parashar and Venkatesh, 2010

; Parashar and Venkatesh, 2010![]() ; Al-smadi et al., 2013

; Al-smadi et al., 2013![]() ).

).

However, the second category of studies considered the lower profitability of IBs to be the origin of the systemic inefficiency of the CBs. The profitability of IBs relative to their conventional counterparts varied from one region to another depending on whether it was an Islamic country or not. This view was justified by the difference between the prudential rules of the transactions applied in the two banking segments. In fact, the level of risk taken by the lender by granting credit via Mushraka or Mudaraba was higher compared to the level of risk generated by the techniques involved in commercial-type financing (Khan, 2012![]() ; Thomi, 2014

; Thomi, 2014![]() ).

).

Other researchers indicated that the profitability of IBs was constantly improving faster than that of CBs over time. The assessment of the IBs’ profitability was often established by specifying the method of financial ratios. They confirmed the progress of IBs from a profitability point of view compared to the CBs of the same regions (Karim and Ali, 1989![]() ; Saiful and Mohd, 2003

; Saiful and Mohd, 2003![]() ; Kader et al., 2007

; Kader et al., 2007![]() ; Moin, 2008

; Moin, 2008![]() ; Olson and Zoubi, 2008

; Olson and Zoubi, 2008![]() ) . However, the shareholders of IB are usually willing to accept lower profitability on equity against a low risk (Salman and Ausaf, 2004

) . However, the shareholders of IB are usually willing to accept lower profitability on equity against a low risk (Salman and Ausaf, 2004![]() ; Hasan and Dridi, 2010

; Hasan and Dridi, 2010![]() ).

).

Another stream of research linked the results of the studies to the factors of the economic situation. During the period of financial crisis, Canbas et al. (2005![]() ) used a multivariate statistical analysis of financial structures. They showed that the profits of CBs reduced until bankruptcy. Similarly, Srairi (2009

) used a multivariate statistical analysis of financial structures. They showed that the profits of CBs reduced until bankruptcy. Similarly, Srairi (2009![]() ) investigated the impact of symptomatic particularities, financial structures, and macroeconomic factors on the profitability of traditional and Islamic commercial banks operating in Middle East countries from1999 to 2006. Their results confirmed that the profitability of Islamic and conventional banks was affected simultaneously by operational efficiency, capital adequacy and credit risk but did not specify the most affected model following the crisis.

) investigated the impact of symptomatic particularities, financial structures, and macroeconomic factors on the profitability of traditional and Islamic commercial banks operating in Middle East countries from1999 to 2006. Their results confirmed that the profitability of Islamic and conventional banks was affected simultaneously by operational efficiency, capital adequacy and credit risk but did not specify the most affected model following the crisis.

The profitability ratios correspond to a category of financial parameters. They are indicators of the banking performance (Ross et al., 2005![]() ). Profitability is an artificial and symbolic measure of financial performance, as it demonstrates, proves and distinguishes between banking systems that withstand economic disruptions during sudden contingent or internal events. Profitability also helps to detect the healthiest banking system during periods of financial stability; when the banking market is in equilibrium. Profitability ratios generally measure a bank’s ability to generate profits as a function of expenses, other relevant costs incurred over a period of time as well as the payment of income taxes (Islam and Salim, 2001

). Profitability is an artificial and symbolic measure of financial performance, as it demonstrates, proves and distinguishes between banking systems that withstand economic disruptions during sudden contingent or internal events. Profitability also helps to detect the healthiest banking system during periods of financial stability; when the banking market is in equilibrium. Profitability ratios generally measure a bank’s ability to generate profits as a function of expenses, other relevant costs incurred over a period of time as well as the payment of income taxes (Islam and Salim, 2001![]() ; Abbas et al., 2012

; Abbas et al., 2012![]() ; Osama et al., 2013

; Osama et al., 2013![]() ) . In other words, this kind of quotient acts as an indicator of management evaluation. A high profitability ratio is a sign of good managerial performance (Norhidayah et al., 2011

) . In other words, this kind of quotient acts as an indicator of management evaluation. A high profitability ratio is a sign of good managerial performance (Norhidayah et al., 2011![]() ).

).

One of the first studies that attempted to discover the main determinants of bank profitability was conducted by Short (1979![]() ) but many other studies were done later on other parameters of profitability (Bourke, 1989

) but many other studies were done later on other parameters of profitability (Bourke, 1989![]() ; Demirguc-Kunt and Huizinga, 2000

; Demirguc-Kunt and Huizinga, 2000![]() ; Abreu and Mendes, 2002

; Abreu and Mendes, 2002![]() ; Micco et al., 2007

; Micco et al., 2007![]() ; Pasiouras and Kosmidou, 2007

; Pasiouras and Kosmidou, 2007![]() ) . Most of the cost-effectiveness studies were conducted in developed countries.

) . Most of the cost-effectiveness studies were conducted in developed countries.

In contrast, studies focusing on comparative performance between Islamic and conventional banks provided data from developing countries. Most of these studies focused on the comparison of returns, using financial ratios (Samad and Hassan, 2000![]() ; Iqbal, 2001

; Iqbal, 2001![]() ; Al-Jarrah and Molyneux, 2003

; Al-Jarrah and Molyneux, 2003![]() ; Hussein, 2004

; Hussein, 2004![]() ; Bader et al., 2007

; Bader et al., 2007![]() ; Kader et al., 2007

; Kader et al., 2007![]() ).

).

Profitability ratios measure a bank’s ability to maximize its resources efficiently. These rapports allow the use of margin analysis to discover the profitability of assets, deposits, placing and securities. The most common ratios used to measure bank profitability are the ROA 1 and the ROE2 (Sinkey, 2002![]() ; Kosmidou, 2008

; Kosmidou, 2008![]() ; Siddiqui, 2008

; Siddiqui, 2008![]() ; Sufian and Habibullah, 2009a

; Sufian and Habibullah, 2009a![]() ) . These two ratios are highly correlated in the banking sector since they give the same indications in terms of financial performance but the difference between these two measures is limited to the method of calculation and the extent of the interpretation of the analyses (Karr, 2005

) . These two ratios are highly correlated in the banking sector since they give the same indications in terms of financial performance but the difference between these two measures is limited to the method of calculation and the extent of the interpretation of the analyses (Karr, 2005![]() ; Castelli et al., 2006

; Castelli et al., 2006![]() ).

).

Some studies uphold the significance of the banks’ assets profitability compared to other financial indicators (Reger et al., 1992![]() ). The profitability of the assets indicates the net profit rate generated on average for all the assets owned by the establishment. It expresses the economic profitability of the entity.

). The profitability of the assets indicates the net profit rate generated on average for all the assets owned by the establishment. It expresses the economic profitability of the entity.

The ROA shows how a bank can convert its assets into net profit. A higher ratio is a good sign of management quality in converting assets recognized into net income (Siddiqui, 2008![]() ). Its main advantage is that it fully covers the activities of the bank. However, its disadvantage appears through the class of total assets on the same level of risk, despite the risks associated with the components of total assets. The ROA reflects the bank’s profitability after subtracting all expenses and taxes (Horne and John, 2005

). Its main advantage is that it fully covers the activities of the bank. However, its disadvantage appears through the class of total assets on the same level of risk, despite the risks associated with the components of total assets. The ROA reflects the bank’s profitability after subtracting all expenses and taxes (Horne and John, 2005![]() ). It answers the question if how a bank can convert its assets into profits (Samad and Hassan, 2000

). It answers the question if how a bank can convert its assets into profits (Samad and Hassan, 2000![]() ). This ratio measures the net income per unit of a given asset. In general, a high ratio means better managerial performance and reflects an efficient use of the bank's assets. A low ratio indicates an inefficient use of assets. Asset profitability can increase either through profit margin growth or asset turnover but not simultaneously due to a trade-off between turnover and margin.

). This ratio measures the net income per unit of a given asset. In general, a high ratio means better managerial performance and reflects an efficient use of the bank's assets. A low ratio indicates an inefficient use of assets. Asset profitability can increase either through profit margin growth or asset turnover but not simultaneously due to a trade-off between turnover and margin.

In addition to the profitability of the assets, there is the profitability of the equity and the ROE is the ratio between the net profit and the equity, (capital, reserves, funds for general banking risks and report again).The ROE expresses the financial profitability of the entity (Samad and Hassan, 2000![]() ). This ratio measures the profitability created on behalf of the bank's shareholders for each monetary unit invested after deducting all expenses and taxes (Horne and John, 2005

). This ratio measures the profitability created on behalf of the bank's shareholders for each monetary unit invested after deducting all expenses and taxes (Horne and John, 2005![]() ). The ROE is an ultimate measure of the strengths of all financial institutions. This ratio also makes it possible to compare banks dissimilar in size and structure.

). The ROE is an ultimate measure of the strengths of all financial institutions. This ratio also makes it possible to compare banks dissimilar in size and structure.

It should be noted that the adoption of ROE is mainly based on the assumption that "the creation of value in the shareholders’ own accounts is positively correlated with the financial performance of a bank" (Lindblom and Koch, 2002![]() ). Roughly, a high ROE represents a sign of a reasonable articulation of good managerial performance as long as profitability on equity is high. This may be due to debt (leverage) or return on assets.

). Roughly, a high ROE represents a sign of a reasonable articulation of good managerial performance as long as profitability on equity is high. This may be due to debt (leverage) or return on assets.

However, financial leverage leads to conflicting results between ROA and ROE as leverage always boosts ROE. This remains valid as long as the gross ROA is above the interest rate on the debt (Ross et al., 2005![]() ).

).

In this sense, Sehrish et al. (2012![]() ) compared the performance of Pakistani classical and Islamic banks from 2007 to 2011. The analysis of profitability measures revealed that there was a statistically significant difference between the profitability of Islamic and conventional banks. They concluded that CBs were more profitable than their Islamic competitors in terms of ROE and PER3 . When looking at the ROA ratio, there was no difference between the two categories of banks. While a thorough analysis of ROE and PER showed the possibility of bringing together the trends of two types of banks soon, they said it was not inconceivable to see the profitability of IBs outperform the profitability of CBs.

) compared the performance of Pakistani classical and Islamic banks from 2007 to 2011. The analysis of profitability measures revealed that there was a statistically significant difference between the profitability of Islamic and conventional banks. They concluded that CBs were more profitable than their Islamic competitors in terms of ROE and PER3 . When looking at the ROA ratio, there was no difference between the two categories of banks. While a thorough analysis of ROE and PER showed the possibility of bringing together the trends of two types of banks soon, they said it was not inconceivable to see the profitability of IBs outperform the profitability of CBs.

The choice of such a ratio depends on the importance of the results of Modell (2004![]() ); Vakkuri and Meklin (2006

); Vakkuri and Meklin (2006![]() ) the inclusiveness, the complementarity, and the precision of this ratio. This ensures the logic of interpretation and is a good means of analysis and an effective method of management (Weick, 1995

) the inclusiveness, the complementarity, and the precision of this ratio. This ensures the logic of interpretation and is a good means of analysis and an effective method of management (Weick, 1995![]() ; De-Kool, 2004

; De-Kool, 2004![]() ). However, research has shown that the simultaneous highlighting of several measures of profitability led to contradictory or non-conclusive conclusions. Table 1 illustrates some recent comparative studies of the profitability of classical and Islamic banks already published in the literature.

). However, research has shown that the simultaneous highlighting of several measures of profitability led to contradictory or non-conclusive conclusions. Table 1 illustrates some recent comparative studies of the profitability of classical and Islamic banks already published in the literature.

With previous comparative studies of bank returns using multiple ratios, we noticed that the conclusions were almost always mixed. They were sometimes similar but they were also often contradictory from one study to another. In both scenarios, the advanced results were inconclusive due to the lack of convincing confirmations and generalization. Since the use of various ratios or the profitability measures were not efficient enough to obtain unique results, we created a new approach in our work. It consisted of testing a single profitability measurement ratio in order to come up with convincing final answers.

2.2. Profitability Measurement Ratio of Conventional and Islamic Banks (Net Profit Margin)

To overcome the phenomenon of the specific opposition and the disparity of the previous results, we focused mainly on the choice of measurement ratios for financial performance. This type of difficulty is met usually with non-substitutable measures such as ROA and ROE, or cash flows and evolving indicators such as turnover, revenues and profits. This was one reason why we chose a last-stage evaluation ratio in the financial cycle. This rapport is more accurate than the others, thus containing the details of the intermediate calculations and the variations of the other parameters.

We used the Net Profit Margin 4. It is obtained by dividing net income as a percentage of income. This ratio measures how much a bank actually retains from each monetary unit of income (Sujan et al., 2013![]() ). The higher the net marginal profit of a bank compared to its competitors, the better the bank concerned. This indicator is considered the best measure of profitability since it reflects the actual situation of the financial health of the bank and is often followed by all the stakeholders, specifically the shareholders, because it shows how much a bank is capable to convert its income into shareable dividends available to shareholders. Marginal net profit also attracts the attention of investors from Islamic or conventional banks as it represents a good sign of wealth maximization for disciplined administrators. This measure implies the success of accompanying a monetary policy to meet the commitments of the bank. In addition, the NPM is expressed as a percentage rather than a monetary unit. This measure makes it possible to compare the profitability of two or more banks, regardless of any differences in their sizes. In this section, as shown in Table 2, we reviewed some of the previous and recent studies that measured the bank profitability by the NPM ratio.

). The higher the net marginal profit of a bank compared to its competitors, the better the bank concerned. This indicator is considered the best measure of profitability since it reflects the actual situation of the financial health of the bank and is often followed by all the stakeholders, specifically the shareholders, because it shows how much a bank is capable to convert its income into shareable dividends available to shareholders. Marginal net profit also attracts the attention of investors from Islamic or conventional banks as it represents a good sign of wealth maximization for disciplined administrators. This measure implies the success of accompanying a monetary policy to meet the commitments of the bank. In addition, the NPM is expressed as a percentage rather than a monetary unit. This measure makes it possible to compare the profitability of two or more banks, regardless of any differences in their sizes. In this section, as shown in Table 2, we reviewed some of the previous and recent studies that measured the bank profitability by the NPM ratio.

Table-1. Methods of profitability evaluation in previous studies.

| Researcher(s) | Context | Period | Mesurement | Results of research |

| Samad and Hassan (2000 |

Malaysia | (1984-1997) | ROA and ROE. | The IB has shown significant progress on ROA and ROE. So, BIMB is relatively more profitable than those of CBs. |

| Iqbal (2001 |

10 countries5 | (1990-1998) | FRA 6 method | IBs are more profitable and more stable than their conventional counterparts. |

| Hassoune (2002 |

Middle East region | (1992-2001) | ROA and ROE | With the same balance sheet structure, IBs have verified more affordable profitability than CBs. He explained the swelling of profits by the degree of operational efficiency manifesting by the imperfection of risk concentration and investment opportunities on the Islamic banking market (Ansari and Rehman, 2011 |

| Samad (2004b |

Bahrain | (1992-2001) | FRA method | There is no significant difference between interest-free banks and banks whose activities are based on profitability interests. CBs are less profitable, less liquid and are characterized by a higher level of credit risk than IBs. |

| Saleh and Zeitun (2006 |

Jordan | (1989-2003) | FRA method | These two banks played an important role in financing projects in Jordan as they increased the extent of its investments. But, IBs have higher profitability and a higher growth rate in credit facilities. They focused on short-term investment rather than long-term investment. This conclusion was justified by the strong capital structure of IBs. |

| Olson and Zoubi (2008 |

GCC countries | (2000-2005) | FRA method | The product structure of IBs is different from that of CBs because it is based on the obligation of exchange or financing more than instruments and real assets. CBs remunerate the collection of deposit funds by a predefined interest rate, while deposit funds at the level of IBs are subject to the principle of sharing different types of risk (Zeitun, 2012 |

| Ariss (2010 |

13 countries 7 | (2000-2006) | ROA, ROE, loans to assets and equity to assets | IBs are better capitalized than their conventional counterparts. They have allocated a very large portion of their assets to lending activities, which implies greater exposure to credit risk. The global Islamic banking market is characterized by more concentration and less competition, making the Islamic banking sector less profitable than the conventional banking sector. They discovered that the profitability of IBs has increased significantly, but it has remained consistently lower than that of CBs. |

| Hasan and Dridi (2010 |

8 countries8 | (2007-2009) | FRA method | In 2008, IBs held up better than CBs in all countries except Qatar, UAE and Malaysia. In Saudi Arabia, Bahrain (with large shares), Jordan and Turkey, the variability of Islamic profitability was significantly more favorable than that of CBs. A comparison between the average profitability level of (2008-2009) and its 2007 level (cumulative effect) revealed the superiority of the average resistance of IBs compared to CBs in most countries, with the exception of Bahrain, United Arab Emirates and Qatar. |

| Rashwan (2010 |

15 countries9 | (2007- 2009) | FRA method (ROA, ROE, net loan on total assets, and gross loan loss reserve | IBs outperformed CBs in 2007. By contrast, in 2008, there was no significant difference between the two banking systems. In 2009, both types of banks performed well. He concluded that the financial crisis has impacted both banking systems, but, the depth of the impacts on IBs is limited to lower yields. |

| Viverita (2011 |

Indonesia | (2004-2008) | FRA method (two cost efficiency ratios, a revenue efficiency ratio and two profit efficiency ratios) | Cost effectiveness ratios were lower in IBs than in CBs. IBs generate higher asset income and profits than CBs. In addition, the net interest margin of IB is higher than the net interest margin of CBs. Moreover, the operating income of average assets in CBs is lower than that of IBs. In total, he concluded that Indonesian IBs are more profitable and effective than their traditional counterparts. |

| Omar and Muhammad (2012 |

12 countries | (2006-2010) | ROA and ROE | Capital adequacy, asset lending and asset management have a significantly positive effect on the ROA and ROE of IBs. As a result, Asset size has a positive and significant impact on the profitability of IBs. |

| Kassim and Abdulle (2012 |

Bahrain | (1991-2001) | FRA method | There is no significant difference between IBs and CBs in terms of profitability. |

| Siraj and Pillai (2012 |

GCC region | (2005-2010) | FRA method (OER 10, NPR11, ROA, ROE, operating expense, profit, assets, operating income, deposits and total equity) | CBs experienced revenue growth over the study period not because profitability did not improve but due to higher provisions for credit losses and impairment losses. While IBs are more equity financed than CBs. |

| Hanif et al. (2012 |

Pakistan | (2003-2007) | ROA, ROE, and Cost Income Ratio. | IB is less profitable than its conventional counterparts. They argued that the conclusions refer to the seniority and market share of Islamic financial assets compared to the share held by CBs. |

| Onakoya and Onakoya (2013 |

United Kingdom | (2007-2011) | ROA, ROE and PER | CBs outperformed their Islamic counterparts although IBs appeared to be as profitable. IBs need to hire a qualified staff to strengthen innovation and differentiation of its products. |

| Moin (2013 |

Pakistan | (2003-2007) | FRA method | The position of profitability was the same in both types of banks. |

| Sujan et al. (2013 |

Bangladesh | (2008-2012) | FRA method | CBs are more profitable than IBs. CBs are more active than IBs because their careers and their advantages of banking experience. They held a dominant share in Bangladesh's financial sector compared to the most recent IBs. |

| Zarrouk (2014 |

MENA countries | (2005-2010) | FRA method | IBs are not immune from the effects of the crisis. After the crisis, the profitability of IBs in the countries of the GCC have decreased drastically. The findings further pointed out that IBs in non-GCC countries were more efficient, more liquid, more profitable and less risky during and after the period of the financial crisis than those in the GCC countries. |

| Hossain et al. (2014 |

Bangladesh | (2009-2011) | ROA and ROE | Despite the considerable proportion of Muslims in Bangladesh, consumption of Islamic banking products is still low. Although the total number of Islamic units in Bangladesh has grown. CBs are more profitable than IBs. They explained that the difference was the adoption of certain specific commercial policies and the mode of operation of each segment of banks. |

| Mousa (2015 |

Bahrain | (2010-2013) | FRA method (ROA, ROE and earnings per share) and DEA 12 method | The ratios have shown oscillating ratios by period, by bank and by ratio, and the results of the DEA method have shown that only 2 banks are fully profitable and efficient at the same time. During the period, other banks are less profitable and less efficient with technical efficiency scores below one. |

| Islam and Ashrafuzzaman (2015 |

Bangladesh | (2009-2013) | FRA method | Capital adequacy in IBs reflects their ability to absorb unexpected losses no matter what happens. IBs have benefited from a large number of investments whose high earnings are transformed into high net income. While, the management quality of operating expenses in CBs is more efficient. |

| Ola and Suzanna (2015 |

United Arab Emirates | (2008-2014) | FRA method | IBs are, on average, less profitable than their conventional competitors. |

| Bilal and Amin (2015 |

Pakistan | (2007-2012) | ROA and ROE | CBs are more profitable than IBs. IBs are expected to improve their returns by taking the necessary precautions during the investment, which helps IBs managers to detect the most profitable business segment that contributes more to the bank’s profitability. |

| Sghaier (2015 |

MENA region | (2005-2011) | ROAA 13 and ROAE14 | CBs perform better than IBs. |

| Rashid and Khaleequzzaman (2015 |

Pakistan | (2006- 2012) | CAMEL ratio | CBs ranked first, while most IBs ranked after 12th. However, IBs have achieved better results in terms of progress report, profitability, and productivity because of the age and the experience (IBs began to work from 2003, whereas the CBs are older). In addition, the Islamic money market is virtually absent. In addition, IBs have sometimes provided for the transmission of commercial risk through the reinvestment of their profit shares in savings accounts and investment deposits, while the reinvestment rate of CBs may exceed the yield of IBsAhmed (2010 |

| Shahab et al. (2016 |

Pakistan | (2006-2014) | FRA (Average ratios) | IBs are more profitable than CBs. The functional system of IBs ensures their capitals and maximizes the collection of deposits. According to the specific provisions, where the distribution of profit must be based on justice and equity, IBs have distributed a portion of profits to lower depositors than that distributed by CBs to its depositors, despite the similar sizes of IBs and CBs. |

| Alharthi (2016 |

37 countries | (2005-2012) | (ROA, ROE and Net Interest Margin) | CBs have achieved better ROAs and ROEs than their Islamic counterparts because of the benefits of maximizing their revenues. |

| Elgadi (2016 |

Sudan | (2005-2013) | Regression method | The empirical model revealed that PLS modes of financing have a positive impact on profitability through its Modarabah and Mosharakah products. However, the management quality of Sudanese IBs is insufficient to predict and avoid the risk associated with leverage. |

| Qasim et al. (2017 |

Jordan | (2010-2013) | FRA, DEA and MI 15 methods | They used a sample of three Jordanian IBs (JIBFI, IIAB and JDIB). Significant results showed that JDIB Bank achieved the highest ranking, followed by IIAB, while JIBFI was ranked 3rd. |

| Ferhi (2017 |

23 countries | (2005-2015) | Financial profitability (ROA and ROE), economic profitability (loan rates, capitalization, credit risk, inefficiency and inflation) | During the period of the financial crisis, the two types of banks were affected, but, the financial crisis has affected more negatively and more deeply the profitability of CBs than that of IBs. The practice of real assets and the respect of sharing profits and losses principle has offered more stability to the Islamic banking system. The profitability of IBs and CBs in the Gulf region is higher than those in Southwest Asia and North Africa. The author explained the benefit of financial strength by owning an extensive network of subsidiaries. |

Table-2. Profitability evaluation by Net Profit Margin in previous studies.

| Researcher(s) | Context | Period | Mesurement | Results of research |

| Bashir (2000 |

Middle East countries | (1993-1998) | Profits generated by overheads, short-term customer financing and non-interest bearing assets. | The reprocessing of deposits in IBs in the form of shares allows to reduce the amount of available funds destined to wards. Afterwards, the funds turn into need of reserves held by the banks. |

| Hassan and Bashir (2003 |

21 countries16 | (1994-2001) | Several operating performance indicators 17. | Efficiency indicators have shown that IBs are well capitalized, which improves their profitability. However, the excessive agreement of customer loans as well as the total assets held have had a negative impact on profitability. IBs are more profitable and better capitalized since they have allocated a large amount of their assets to financing activities like Moucharaka, Mudaraba and Ijara, in comparison with its classic peers (Alimshan, 2009 |

| Toumi et al. (2008 |

18 countries | (2004-2008) | ROA, ROE, Net Margin Ratio and Dividend payout. | There is no significant difference between the profitability of assets and the return on equity of IBs and CBs. Also, NMR has shown that IBs are less profitable than their conventional counterparts. IBs relied more on shareholder capital to structure their capital, while CBs relied more on debt. As a result, IBs are less profitable compared to these competitors. |

| Ramadan (2011 |

Jordan | (2000-2010) | Regression method18. | IBs are well capitalized, characterized by efficient management and a very high credit risk which allows to maximize the profitability of assets. In addition, credit risk, management efficiency and management of operating expenses positively impacted the profit margin of Jordanian IBs. |

| Siraj and Pillai (2012 |

GCC region | (2005-2010) | Several operating performance indicators 19. | IBs perform better than CBs, despite declining performance indicators. First, IBs are financed by equity, while CBs are financed by borrowed funds. In addition, CBs recorded revenue growth and maintained the same level of profitability due to higher provisions for credit losses and impairments. Secondly, the net profits of CBs are higher than the net profits of IBs. While the trend in operating profits has risen faster in IBs than in CBs. Then, the profitability of assets is higher in IBs. However, they reported the opposite for the return on equity. Finally, total profit as a percentage of customer deposits, customer deposits as a percentage of equity, and total equity as a percentage of total assets are higher in IBs than in CBs. |

| Atyeh et al. (2015 |

Kuwait | (2006-2012) | ROA, ROE, Return on Capital, Net Profit Margin and Spread in Interest Rate, the trend, government regulation. | The overall profitability of the banking sector has increased significantly in the first two years. However, bank profitability showed a downward trend in the rest of the period due to economic slowdown. This has resulted in lower profitability of assets and equity. Despite adverse economic conditions, Kuwaiti banks have been able to continue their operations and protect their capital due to low leverage. |

The exclusion of interest by the Islamic mode of financing in all the activities of the banks does not necessarily mean that the financier cannot make a profit (Djojosugito, 2008![]() ). Only, that the financier must ensure that gains made on the initial amount are directly subject to risk on the investment (Siddiqui, 1987

). Only, that the financier must ensure that gains made on the initial amount are directly subject to risk on the investment (Siddiqui, 1987![]() ). For this reason, we have assumed that the best hypothesis to verify is the following proposition:

). For this reason, we have assumed that the best hypothesis to verify is the following proposition:

Hypothesis: IBs are more profitable than CBs in a stable financial period.

To overcome the theoretical confusion of this subject and to answer the problem posed in the literature review, in the next section, we empirically demonstrated the evolutionary aspects of the profitability of Islamic and conventional banks from a comparative perspective.

3. METHODOLOGICAL FRAMEWORK: PRESENTATION OF THE DATA AND COMPARISON BETWEEN THE BANKING PROFITABILITIES

In the light of the above and previous studies on this topic, we tested the empirical validity of the hypothesis already proposed and to qualify the interdependence, which may exist, between the profitability of CBs and that of IBs. Several studies have confirmed the strength of IBs since they support shocks and resist against international financial crises and economic collapses (Jouini and Pastre, 2009![]() ; Siddiqui, 2009

; Siddiqui, 2009![]() ). Indeed, similar studies have demonstrated the stability of the Islamic financial system and its continued ability to ensure a sustainable improvement in the profitability of IBs even after the occurrence of the crisis. However, a third set of studies has proved that the assumption of financial strength/fragility of Islamic and classical banks has been destroyed during periods of financial crisis/stability.

). Indeed, similar studies have demonstrated the stability of the Islamic financial system and its continued ability to ensure a sustainable improvement in the profitability of IBs even after the occurrence of the crisis. However, a third set of studies has proved that the assumption of financial strength/fragility of Islamic and classical banks has been destroyed during periods of financial crisis/stability.

This section is structured as follows: the first section will present the methodological choices made, while the second section will focus on the verification of assumptions before analyzing and interpreting the comparative results between the profitability of the conventional banks and that of Islamic banks.

In this section, we highlight the operational approach of comparing the profitability ratios of conventional and Islamic banks. We adopted the most effective method applied after an adaptation procedure and a convergent methodological demonstration: the financial ratios analysis method in which each sample parameter is explained by a single ratio.

There are several reasons for this choice. First, all measures of performance are calculated from ratios that would not offer decisive and clear conclusions (Teker et al., 2011![]() ; Rashid and Khaleequzzaman, 2015

; Rashid and Khaleequzzaman, 2015![]() ). Second, because the profitability specific data of traditional and Islamic banks are not easily collected and extracted from its annual reports, the reduction of the size of our samples was necessary since the requested information on profitability was not always disclosed. Finally, given the available banking information, we conducted a conditional study, in which the selection of observations was both a methodological contribution to obtain high quality results and a basic limit already encountered during data collection. The preliminary observations taken into account had the effect of the assumptions placed on them in advance, so that the observation that did not comply with the rules of play was eliminated taking into account the order of the following assumptions and so on, until we got the two final samples. Our contribution was to use a single profitability ratio.

). Second, because the profitability specific data of traditional and Islamic banks are not easily collected and extracted from its annual reports, the reduction of the size of our samples was necessary since the requested information on profitability was not always disclosed. Finally, given the available banking information, we conducted a conditional study, in which the selection of observations was both a methodological contribution to obtain high quality results and a basic limit already encountered during data collection. The preliminary observations taken into account had the effect of the assumptions placed on them in advance, so that the observation that did not comply with the rules of play was eliminated taking into account the order of the following assumptions and so on, until we got the two final samples. Our contribution was to use a single profitability ratio.

3.1. Description of the Samples Studied

3.1.1. Constitution of the Samples

Both samples tested were taken from two base populations. These populations consisted of 1788 conventional financial institutions and 467 Islamic financial institutions from three continents: Europe, Asia and Africa. Sixteen countries were involved in our work: Egypt, Bangladesh, Indonesia, Pakistan, Malaysia, Turkey, United Kingdom, Bahrain, Jordan, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, South Africa and Sri Lanka.

However, we excluded all specific financial institutions operating with specific regulations. The tested samples contained only purely conventional or Islamic banks. In addition, given the difficulties in collecting information on profitability, we excluded banks for which we detected certain observations, variables or missing data. In addition, we also removed multi-type mutated banks (IB with conventional windows and CB with Islamic windows). These three conditions led us to eliminate 337 traditional financial institutions and 231 Islamic financial institutions. Subsequently, the number of remaining banks of each type of bank was purified based on qualitative filtering criteria (equality of samples, type of activity, similarity of country’s origin, bank width) so that every CB in a country had its closest Islamic equivalence taken from the same country, in terms of capital and size. This restriction reduced the size of our samples to 63 banks each. Finally, after several eliminations and deletion steps, we obtained two pairs of equal samples (n1= n2).

3.1.2. Data Collection

The data was collected from the data stream database. In order to better understand the dissimilarities between the two groups of banks and to improve the clarity and the truthfulness of the results, the choice of the observations related essentially to individual data, even if the bank belonged to a group of banks. However, the accuracy of the results required following a data filtering procedure so that observations containing some missing data were eliminated. For this reason, we were careful to remove financial institutions that did not qualify as banks. In addition, we also omitted the banks belonging to the same sample whose types were heterogeneous in order to obtain a sample of CBs which was almost similar to its Islamic counterparts and vice versa.

Similarity meant that the CBs’ sample size was equal to IBs’ sample size. In addition, the number of IBs chosen or each country was equal to the number of CBs in the same country. As shown in Table 3 , the affinity meant that a classical or Islamic bank (commercial type (CoB), investment type (InB) or universal type (UnB)) in each country of the first sample had to have its counterpart of the second sample located in the same country with a probability of 94.7%~(95%). After filtering, for each sample, we had a total 63 observations of banks collected from 2010 to 2018.The following table summarizes the process followed as well as the different stages of the observation selection process.

Table-3. The samples filtering process of conventional and Islamic banks.

| Gait | Number of CBs |

Number of IBs |

||||

| Populations of initial financial institutions. | 1788 |

467 |

||||

| Exclusion of non-bank financial institutions and banks whose data are not published, available or have missing data as well as non-conventional or Islamic banks. | 1451 |

236 |

||||

| Exclusion of additional banks at the limit of choice of similar banks and converge. | 274 |

168 |

||||

| Final sample. | 63 |

63 |

||||

| Bank type. | CoB |

InB |

UnB |

CoB |

InB |

UnB |

| Number of banks. | 41 |

15 |

7 |

36 |

19 |

8 |

| Proportion of total sample. | 65.08% |

23.81% |

11.11% |

57.14% |

30.16% |

12.70% |

| Similarity rate. | 92.06% |

93.65% |

98.41% |

92.06% |

93.65% |

98.41% |

| Difference rate. | 7.94% |

6.35% |

1.59% |

7.94% |

6.35% |

1.59% |

3.2. Measurement of the Variables to be Compared

Since the findings in the literature were inconclusive due to the heavy use of financial ratios, we symbolized the profitability by a single ratio. Our ratios choice was justified by two main reasons. On the one hand, in practice, a deep contention arose. The large CBs listed adopt accounting rules established by international standard setters (IASB) and (FASB). The prohibition of using interest meant that some conventional accounting practices were not always applicable in Islamic financial institutions, therefore, not all measures were valid for performing a comparative study between banking systems.

In this case, the choice of a single ratio to assess the profitability situation provided conclusive results that better reflected the bank’s reality, whatever its type. On the other hand, the two models differed in terms of the asset valuation method, the drafting of financing contracts, the recognition and treatment of income (Ahmed, 2002![]() ). Therefore, the financial ratios of two models were not calculated in the same way and the informational content of its measures were not treated and interpreted identically.

). Therefore, the financial ratios of two models were not calculated in the same way and the informational content of its measures were not treated and interpreted identically.

To remedy these problems, the A.A.O.I.F.I20 has issued custom-tailored accounting and auditing standards in coordination with other specific agencies for use by listed and unlisted IB. This does not mean that existing conventional accounting measures and concepts will all be ignored or adopted. But, concepts inconsistent with Sharia rules have been rejected or modified, while concepts converging with Sharia principles have been incorporated into the norms A.A.O.I.F.I (Lewis and Algaoud, 2001![]() ).

).

Although each country has its own accounting framework that is more/less different from other countries, this is the theoretical proof that avoids the lack of clarity related to differences in the application of accounting standards. Before determination of the financial ratios, the constitutional and functional differences between CBs and IBs must be taken into account. Practically, the functions of IBs resemble those of CBs. Islamic scholars have compared the discrepancies to develop similar products to those of CB, allowing to replace interest rate payments and update fees (Beck et al., 2013![]() ) and Ada and Dalkilic (2014

) and Ada and Dalkilic (2014![]() ). For example, Waseem (2008

). For example, Waseem (2008![]() ) argued that financing costs were almost the same in IBs and CBs. His argument was that interest rates take into account administrative costs, the sharing of profits and record ancillary costs.

) argued that financing costs were almost the same in IBs and CBs. His argument was that interest rates take into account administrative costs, the sharing of profits and record ancillary costs.

In particular, Turen (1996![]() ) has provided an assimilation of methods for calculating financial ratios between the two types of banks. He suggested that the functioning of an IB depends on the combined effect of three laws governing the degree of the gap between the two banking models. First, the deposits holders at the level of CBs are replaced by the shareholders of IBs. Second, interest paid to depositors is converted by shared profits or losses. Third, loans to traditional bank customers are converted into equity investments in IBs. Compliance with these three principles indicates that most financial ratios in the two categories of banks are defined in the same way. However, the net income of an IB includes the conventional net income before taxes, plus Zakat, which has been supplemented by the income tax. In addition, interest expenses are replaced by commission income and expenses. Indeed, the loans and advances granted by the CBs are essentially equivalent to the investments according to the technique of Mudaraba, Murabaha and Moucharaka. As a result, all researchers tended to evaluate the major sections of the financial statements of two types of banks and found that the main elements were almost similar.

) has provided an assimilation of methods for calculating financial ratios between the two types of banks. He suggested that the functioning of an IB depends on the combined effect of three laws governing the degree of the gap between the two banking models. First, the deposits holders at the level of CBs are replaced by the shareholders of IBs. Second, interest paid to depositors is converted by shared profits or losses. Third, loans to traditional bank customers are converted into equity investments in IBs. Compliance with these three principles indicates that most financial ratios in the two categories of banks are defined in the same way. However, the net income of an IB includes the conventional net income before taxes, plus Zakat, which has been supplemented by the income tax. In addition, interest expenses are replaced by commission income and expenses. Indeed, the loans and advances granted by the CBs are essentially equivalent to the investments according to the technique of Mudaraba, Murabaha and Moucharaka. As a result, all researchers tended to evaluate the major sections of the financial statements of two types of banks and found that the main elements were almost similar.

To measure bank profitability, we defined this notion with a single indicator. Table 4 summarizes all the information needed to qualify this variable.

Table-4. Clarification, description and symbolization of bank profitability.

| CBs rating | IBs rating | Measurement | Previous studies |

| Rtc(NPMc) | Rti(NPMi) | Net Profit Margin= Marginal Profit / Total Revenues | Hassan and Bashir (2003 Tandelilin et al. (2007 Sujan et al. (2013 Atyeh et al. (2015 Ogbeide and Akanji (2018 |

3.3. Operative Method of Interpreting the Comparison Results between Profitabilities of the Islamic and Conventional Banks

The review of the literature assessed the resistance of conventional or Islamic banking institutions to financial shocks and allowed us to draw two conclusions.

In previous studies, researchers have in most cases applied either a deterministic or a demonstrative approach, but they have never tested the exploratory approach. In addition, they conducted either single-sector impact studies encompassing only CBs, only IBs or exceptional case studies, the objective being to demonstrate the effect of financial crises or other bank characteristics on a profitability parameter, or comparative studies between two or more models.

At first sight, they justified the bankruptcy of CBs independently of their competitors in the banking market and without performing causal linear reasoning (De-Jong et al., 2002![]() ; Gupta et al., 2013

; Gupta et al., 2013![]() ). Researchers in the previous studies have shown that CBs have been hit hard because of the rapid decline in the value of their assets (Furceri and Mourougane, 2009

). Researchers in the previous studies have shown that CBs have been hit hard because of the rapid decline in the value of their assets (Furceri and Mourougane, 2009![]() ; Stijn et al., 2011

; Stijn et al., 2011![]() ). Some institutions went bankrupt while other institutions were saved because of public bailouts. The Islamic banking institutions, in all cases, even if they had been impacted, had lowered their financial performances and were not widely affected (Loghod, 2008

). Some institutions went bankrupt while other institutions were saved because of public bailouts. The Islamic banking institutions, in all cases, even if they had been impacted, had lowered their financial performances and were not widely affected (Loghod, 2008![]() ; Mirakhor and Krichene, 2009

; Mirakhor and Krichene, 2009![]() ; Hasan and Dridi, 2010

; Hasan and Dridi, 2010![]() ; Khamis and Senhadji, 2010

; Khamis and Senhadji, 2010![]() ; Parashar and Venkatesh, 2010

; Parashar and Venkatesh, 2010![]() ; Rashwan, 2010; 2012

; Rashwan, 2010; 2012![]() ; Merchant, 2012

; Merchant, 2012![]() ; Siraj and Pillai, 2012

; Siraj and Pillai, 2012![]() ) .

) .

We chose the constructivist analysis approach. This approachwasa key factor and a necessary tool for successful recognition and legitimization of a research. The proposed approach was the most appropriate for assessing knowledge and suggesting new thinking. Constructivism was defined by Perret and Seville (2003![]() ) as "an approach to knowledge in terms of ethical validity, that is, based on criteria and methods that can be discussed".

) as "an approach to knowledge in terms of ethical validity, that is, based on criteria and methods that can be discussed".

Our study aimed to reveal the most profitable banking model during a period of economic stability, after a comparative analysis between two heterogeneous samples of Islamic and classical banks. The choice of an empirical process hada direct effect on the trends in the synthesis results and the interpretations quality, which was why we had established a specific and original method of sample composition.

The evaluation technique of associated bank profitability commonly used in comparative studies between IBs and CBs is the "Financial Ratio Analysis Method" (O'Connor, 1973![]() ; Chen and Shimerda, 1981

; Chen and Shimerda, 1981![]() ; Hempel and Simonson, 1998

; Hempel and Simonson, 1998![]() ; Iqbal, 2001

; Iqbal, 2001![]() ; Rosly and Mohd, 2003

; Rosly and Mohd, 2003![]() ; Haron, 2004

; Haron, 2004![]() ; Samad, 2004b

; Samad, 2004b![]() ; Olson and Zoubi, 2008

; Olson and Zoubi, 2008![]() ) . Our contribution consists in adopting a single parameter to express the bank profitability, Rt.

) . Our contribution consists in adopting a single parameter to express the bank profitability, Rt.

The statistical interpretation began with the verification of the distributions’ normality. Then, we tested the averages comparison. However, the application of such a parametric test relies on autonomous conditions before its adoption. In addition, the implementation of the comparison test between the averages of two or more samples required the satisfaction of certain approved conditions. The choice varies according to the case depending on the close link with the type of sample (independent or matched sample), the type of variables (qualitative or quantitative) and if the variables to be tested are quantitative, it is necessary to make sure of the normality of distributions. In this case, before testing the hypotheses, we first checked the normality of the variables of each sample. Finally, based on empirical results, we decided on the most profitable group of banks.

Since the two samples were independent, the comparison could not be made without testing the equality between the two groups. In other words, whether the two samples came from the same reference population or belonged to two distinct populations. We needed to know in advance whether the average profitability normally distributed of CBs was higher (or lower) than the average profitability of IBs under the same law.

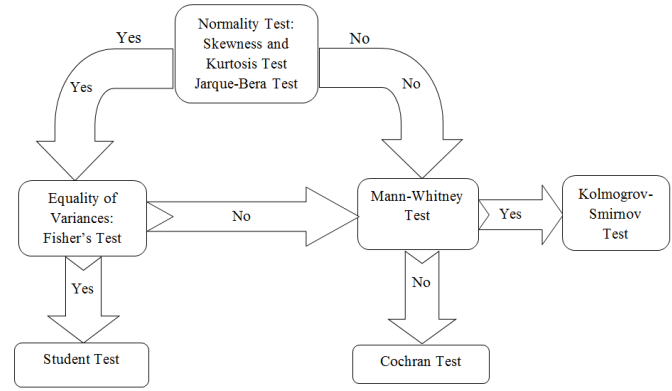

3.3.1. Test of Normality

Through this test, we wanted to know if there was a significant difference between the two types of banks and determine the meaning of the correlation if it existed. First, we verified the distributions’ normality of the variables explained (Skewness and Kurtosis test or the Kolmogorov-Smirnov test). Next, we had to perform an analysis of the results of the Mean-to-Mean comparison tests (Student’s test and variance comparison test) or a Mann-Whitney Test, if necessary. It all depended on the outputs of the necessary statistical tests and the rigorous approach to compare two independent samples.

The selection of one test instead of another was determined by two conditions:

- Variables distributions’ normality of the two samples or the non-satisfaction of the simultaneous normality condition of the variables to be compared.

- Variances’ equality of similar variables to test two by two (homoscedasticity).

Figure 1 illustratesthe process of choosing the appropriate test according to the data collected and the results of the statistical tests obtained:

Figure-1. Method of choosing the appropriate comparison test to the results of the normality test.

For all the variables that follow the normal law, before applying the Student test, the procedure of this test requires the verification of the equality of the variances. In other words, the estimation of the depth difference between the average measures of profitability via the Student’s test, depends on the acceptance of the hypothesis of equality between profitability variances. If this was not the case, we would need to apply another substitute test. In case some variables do not satisfy the normality condition, the parametric tests are no longer valid. To solve this problem, we can use either the Mann-Whitney test or the Cochran test.

In practice, normality scanning is mandatory if the size of the test is less than 30 observations. This restriction is not essential when the sample exceeds 30 observations which is the minimum size sufficient to ensure the quasi-normality of the sampling distributions.

However, the size of our sample of CBs as well as that of IBs was 63 banks. We worked on 315 observations. To ensure the quality of the results and the reliability of interpretations, we verified the normality of distributions. We chose the Skewness and Kurtosis test. Our approach consisted of testing two sets of variables that explain the bank profitability. One set of variables symbolizes the CBs, and the other represents the IBs.

The hypothesis test rejects the normality proposition when the probability associated with the Kurtosis coefficient is less than or equal to 5%. According to Table 5, the p-value (0.0061) specific to the CBs’ profitability showed a value of less than 5%. Otherwise, the normality test allowed us to state, with a certainty of 95%, the non-normality of the data distribution.

Table-5. Detection normality of the profitability relative to the sample of CBs.

Bank type |

CBs / Number of observations = 315 |

|||||

Mesurement |

Skewness |

Pr (SK) |

Kurtosis |

Pr (KUR) |

Prob >χ2 p-value |

Normality |

Rtc (NMc) |

-4.95273≠0 |

0.0000 |

17.42613≠3 |

0.0000 |

0.0061 |

No |

Similarly, Table 6 revealed that the test of Skewness and Kurtosis specific to the IBs’ profitability generated a p-value (0.0000) less than 5%. Therefore, we rejected the null hypothesis, which indicatedthat the profitability of IBsdidnot follow the normal law.

Table-6. Detection normality of the profitability relative to the sample of IBs.

Bank type |

IBs / Number of observations = 315 |

|||||

Mesurement |

Skewness |

Pr (SK) |

Kurtosis |

Pr (KUR) |

Prob >χ2 p-value |

Normality |

Rtc (NMi) |

-4.18604≠0 |

0.0000 |

37.95881 ≠3 |

0.0000 |

0.0000 |

No |

3.3.2. Analysis of the Non-Parametric Test Results for Comparability of Two-Sample Profitabilities (Mann-Whitney Test)

Almost all statistical tests assume the normality of the random variables studied, but this condition is not always confirmed. For variables that do not follow normality, it is possible to apply the Mann-Whitney test (U-test). This non-parametric test compares two samples from two independent populations. The Mann-Whitney test replaces the Student’s test, but never relies on the parameters of frequency distributions and the estimation of mean and variance.

When the distributions are far from normal, the Mann-Whitney test is appropriate and effective. This test is widely applicable regardless of the samples’ size, even if they are not subject to the normality requirement. If the profitability ratio does not meet the normality test for one of two samples, it abandons the application of the Student test even if the normality assumption is satisfied for the same variable in the other sample. The distribution of Rt wasn’t normal for both types of banks, so the Mann-Whitney test was implemented automatically.

Table 7 showed the existence of a considerable difference between the couple of parameters of bank profitability. We noticed that the P-value (0.0004) of the Rt ratio was less than 5%. For this reason, we confirmed the rejection of H0. So, there was a significant difference between the CBs’ profitability and that of IBs over the period from 2010 to 2018.

Table-7. Mann-Whitney and Kolmogorov-Smirnov test for the detection of differences between the profitability of conventional and Islamic banks.

Mesurement |

Kolmogorov-Smirnov |

p-value |

Mann-Whitney NBC = 315/NBI=315 |

p-value |

Comparison test between averages |

|

Rtc and Rti |

0.1863 |

0.012<5% |

2.387 |

0.0004<5% |

H0 Rejected |

|

4. ANALYSIS OF THE COMPARATIVE RESULTS BETWEEN THE PROFITABILITY OF THE CLASSICAL AND ISLAMIC BANKS

In order to make a final judgment on the difference between the financial performances, we analysed the profitability via the NPM (Total Revenues-Total Expenses-Taxes/Total Revenues). The NPM is the percentage of the remaining income after the deduction of all expenses of all receipts. The NPM is a measure of the overall success of the bank. A high rate indicates that the bank managed its products properly and exercised good cost control. This measure summarizes the bank’s adequacy to cover its concerns, meet its commitments and maximize its revenues in the short, medium and long term. Depending on the study period, all indicators contribute to ensuring smooth functioning and financial stability in order to maintain the viability and sustainability of the traditional or Islamic banking sector.

The NPM ratio helps banks to establish a planning, managing and distributing system for expenditures and revenues that provide a favorable framework for balancing jobs and resources. The planned and predicted long-term sustainable model can only be achieved through the combination of financial policy measures and the implementation of the necessary actions. This ratio reflects the optimal and efficient use of the assets since the profits cannot be increased unless there is an increase in income, profit margins or following the assets rotation. However, this cannot happen at the same time because of competition and trade-offs between turnover and profit margins on the products offered and, because of the endowment, depreciation and profit.

The NPM shows how much a bank can convert its income into available profits. The profits, in turn, will be shared elsewhere between shareholders in the form of dividends. Therefore, this variable is often followed by all stakeholders and specifically by shareholders. Also, the NPM attracts the attention of investors from Islamic or conventional banks, as it represents a good sign of maximizing wealth. In favor of disciplined administrators, the maximization of this measure implies the adoption of a successful, useful and effective policy capable of satisfying the bank's commitments successfully. The NPM is explained in percentage rather than in monetary unit. It is valid to compare the profitability of two or more banks, regardless of their differences in size.

The NPM is a means of analyzing the variation of revenues and expenses, a rate higher than 10% is considered excellent. Buta small NPM may be acceptable in some sectors, depending on the structure and size of the bank. The Mann-Whitney test provideda low risk of H0 release (0.0004 <5%). Therefore, referring to Table 8, we rejected with certainty the null hypothesis confirming that there was a significant difference between the NPM of two types of banks (0.381>5%).

On average, the NPM of CBswas 14.758% >5% which was higher than the NPM of IB -9.732%, which led us to reject incontestably the forecast of the higher profitability of IBs. As a result, we have stated that CBs that were components of our classical sample were more profitable than their Islamic counterparts between 2010 and 2018. These results were consistent with previous literature results (Metwally, 1997![]() ; Moin, 2008

; Moin, 2008![]() ; Jaffar and Manarvi, 2011

; Jaffar and Manarvi, 2011![]() ; Hanif et al., 2012

; Hanif et al., 2012![]() ; Fayed, 2013

; Fayed, 2013![]() ; Osama et al., 2013

; Osama et al., 2013![]() ; Ola and Suzanna, 2015

; Ola and Suzanna, 2015![]() ) .

) .

Table-8. Comparison between the profitability ratio of classical and Islamic banks.

Mesurement |

Hypothesis test of comparison between the profitability ratios |

Decision |

Rtc and Rti |

P(Rtc>Rti) = 0.381> 0.05 H Accepted |

H1 rejected presence of significant difference |

Conversely, it is possible to earn a high NPM just to generate enough cash flow because it is necessary to accelerate cash flows, to facilitate the purchase of fixed assets or to pay working capital. A comparative study between the profitability of classical and Islamic banks as an essential component of performance required the revising of many structural factors before the effectiveness of the results. Thus, a high average value of bank profitability does not necessarily imply that efficient and effective use of resources can create wealth.

Islamic and conventional banks generate their revenue and expenditure items in accordance with various accounting standards. As each country adopts different local and international standards from other countries, this automatically leads to diverging results. The NPM can be easily and radically manipulated through the management of exceptionally high non-operational gains or losses. For example, a significant gain on the sale of a division could create a significant NPM, while the results of the banks’ operations were poor. The bank’s management could deliberately reduce expenses that could affect the bank’s long-term competitiveness, such as equipment maintenance, research and development and bank marketing, in order to increase the NPM. These expenses are called discretionary expenses.

Table 9 showed that the CBs’ profitability of our first sample was not efficient enough (-0.0193), although its index had signaled the creation of additional profits. Also, all the topical reasoning of the link between the sum of receipts, the sum of disbursements and the liquidity of banks normally signaled the creation of profits, followed by an improvement in liquidity or a growth in their loan offers, even the reaching the extreme level of solvency. If not, the results indicated that the situation shows a poor profitability that needs to be addressed.

To better justify our argument, Aduda and Gitonga (2011![]() ) examined the type of relationship between credit risk and the CBs’ profitability as an indicator of financial performance. They proclaimed that there was a reasonable dependence between credit risk management and the commercial banks profitability. However, in our study, the results for CBs revealed the opposite, the solvency (-0.0048) was negatively correlated with the net profit see Table 9.

) examined the type of relationship between credit risk and the CBs’ profitability as an indicator of financial performance. They proclaimed that there was a reasonable dependence between credit risk management and the commercial banks profitability. However, in our study, the results for CBs revealed the opposite, the solvency (-0.0048) was negatively correlated with the net profit see Table 9.

Normally, low profits are due to the rigidity of loan distribution policies and the strict conditions for obtaining credit (Sarwar and Asif, 2011![]() ). In addition, the liquidity obtained is weakly correlated with the after-tax profits. The supervision of a banking system is based on several pillars, one of which predicts that the increase in the volume of credits is accompanied by an increase in banks’ capital requirements. This conclusion has shown the fragility of the liquidity of the system. This was consistent with the fallout from a large accumulation of abnormal liquidity and the high probability of the presence of accounting and financial manipulations.

). In addition, the liquidity obtained is weakly correlated with the after-tax profits. The supervision of a banking system is based on several pillars, one of which predicts that the increase in the volume of credits is accompanied by an increase in banks’ capital requirements. This conclusion has shown the fragility of the liquidity of the system. This was consistent with the fallout from a large accumulation of abnormal liquidity and the high probability of the presence of accounting and financial manipulations.

Table-9. Correlation matrix between measures of the financial performance of CBs.

IC sample |

Rtc |

Etc |

Ltc |

Stc |

Mesurement |

||||

Rtc |

1.0000 |

|||

Etc |

-0.0193 |

1.0000 |

||

Ltc |

0.0492 |

-0.0965 |

1.0000 |

|

Stc |

-0.0048 |

-0.0344 |

0.3851 |

1.0000 |

Table-10. Correlation matrix between measures of the financial performance of IBs.

IB sample |

Rti |

Eti |

Lti |

Sti |

Mesurement |

||||

Rti |

1.0000 |

|||

Eti |

0.8264 |

1.0000 |

||

Lti |

0.1917 |

-0.0172 |

1.0000 |

|

Sti |

0.1356 |

-0.1461 |

-0.0350 |

1.0000 |