FIRMS’ ATTRIBUTES, CORPORATE SOCIAL RESPONSIBILITY DISCLOSURE AND THE FINANCIAL PERFORMANCE OF LISTED COMPANIES IN NIGERIA

Senior Lecturer and Ag.Head, Department of Accounting, Delta State University, Abraka, Nigeria.

ABSTRACT

The legitimacy theory gives credence to why firms strive to ensure that their overall value system does not oppose those of the larger society in which they operate while simultaneously enhancing their performance and narrowing the presumed gap between their activities and societal expectations. Therefore, hinged on the legitimacy theory, this study focused on assessing the interrelationship between firms’ attributes, corporate social responsibility (CSR) disclosure and measures of financial performance of firms. Secondary data were collated from the financial reports of a sample of 29 listed Nigerian firms in the financial service sector over a 10-year period (2009-2018). Estimation was based on the structural equation modeling (SEM) technique. We observed that measures of firm performance, firm value and capital structure exert significant influence on CSR disclosure respectively; but the same was not the case for ownership structure and board attributes. We also found that firm value, capital structure, ownership structure and board attributes do not have significant influence on the financial performance of firms. We therefore recommend that while eschewing from financing asset acquisition through debts, reporting entities should be more involved in environmental engagements; and costs associated with such engagements should be reported alongside their respective mainstream financial reports.

Keywords:Financial performance, Corporate governance, Capital structure, Strategic planning, Structural equation modeling, Business performance, Board attributes, CSR Disclosure.

JEL Classification:L25; M14; M41; G34.

ARTICLE HISTORY: Received: 25 March 2020, Revised: 8 May 2020, Accepted: 10 June 2020, Published: 24 June 2020

1. INTRODUCTION

The strategic architecture of reporting entities has advanced from the primary goal of maximizing the overall wealth of shareholders to embracing the idea that corporate entities must be socially responsible to themselves and particularly, to their immediate operating environment. Arguably, while the operations and performances of companies are believed to have been affected by the prevailing activities of their immediate environment, the general view of a growing body of literature is that the operations of companies may have also affected and may currently be affecting amongst others, the economy, activities and lifestyles of the people in their respective immediate/operating environment (Abdulrahman, 2014![]() ; Ajide & Aderemi, 2014

; Ajide & Aderemi, 2014![]() ; Ashafoke & Ilaboya, 2017

; Ashafoke & Ilaboya, 2017![]() ; Duke & Kankpang, 2013

; Duke & Kankpang, 2013![]() ; Iwata & Okada, 2011

; Iwata & Okada, 2011![]() ; Ngwakwe, 2008

; Ngwakwe, 2008![]() ).

).

Given the above, companies have been called upon to veer from the presumed overbearing focus on the primary goal of shareholders’ wealth maximization and possibly integrate into their respective mainstream reports and strategic plans, social and environmental issues that are largely affecting companies and their hosts (Salaudeen & Abiola, 2018![]() ). This presumably may not only help in building the reputation of organizations, but also improve the financial and other operating performance of companies This accounts for why the idea of reporting all costs associated with social and environmental issues/engagements by companies has gained global recognition because any attempt to neglect the social impact of companies on their respective operating environment/hosts is highly risky and may have pessimistic consequences on firms’ performance and by extension, the relationship between reporting entities and their respective stakeholders (Ilaboya & Omoye, 2013

). This presumably may not only help in building the reputation of organizations, but also improve the financial and other operating performance of companies This accounts for why the idea of reporting all costs associated with social and environmental issues/engagements by companies has gained global recognition because any attempt to neglect the social impact of companies on their respective operating environment/hosts is highly risky and may have pessimistic consequences on firms’ performance and by extension, the relationship between reporting entities and their respective stakeholders (Ilaboya & Omoye, 2013![]() ).

).

In parts of Nigeria for instance, there is evidence of negative consequences on the environment of host communities in several forms: pollution (air and water), oil spillage, environmental degradation, depletion of natural resources, destruction of aquatic lives, deforestation, amongst others (Asuquo, Dada, & Onyeogaziri, 2018![]() ; Salaudeen & Abiola, 2018

; Salaudeen & Abiola, 2018![]() ). These negative consequences are the results of neglect and marginalization of their respective host communities, and a total failure by companies to be environmentally friendly since there is a direct link between host communities’ environmental challenges and the activities of companies operating within the areas currently experiencing such environmental challenges (Udo, 2019

). These negative consequences are the results of neglect and marginalization of their respective host communities, and a total failure by companies to be environmentally friendly since there is a direct link between host communities’ environmental challenges and the activities of companies operating within the areas currently experiencing such environmental challenges (Udo, 2019![]() ). The perceived neglect of host communities has birthed agitators (sometimes referred to as militants) whose past and current activities had negative manifestations on companies’ performances and operations due to acts of sabotage on the operations and intentional destruction of companies’ facilities which ultimately affected the level of productivity of companies within the region.

). The perceived neglect of host communities has birthed agitators (sometimes referred to as militants) whose past and current activities had negative manifestations on companies’ performances and operations due to acts of sabotage on the operations and intentional destruction of companies’ facilities which ultimately affected the level of productivity of companies within the region.

However, in resolve to practically arrest and/or reduce the negative consequences of the imperious activities of militants/agitators and to further avert the total loss of support from all stakeholders, companies have been admonished to take all the necessary steps of being environmentally friendly while simultaneously integrating social and/or environmental reports to their respective mainstream financial reports (Tang & Li, 2011![]() ).

).

To date, prior Nigerian studies have either examined the statistical link between performance and environmental/social/sustainability costs or have focused on assessing the determinants of CSR disclosure practices amongst firms; predominantly in the oil and/or manufacturing sector(s) (Bessong & Tapang, 2012![]() ; Dabor & Dabor, 2015

; Dabor & Dabor, 2015![]() ; Enahoro, Akinyomi, & Olutoye, 2013

; Enahoro, Akinyomi, & Olutoye, 2013![]() ; Umoren, Isiavwe-Ogbari, & Atolagbe, 2017

; Umoren, Isiavwe-Ogbari, & Atolagbe, 2017![]() ). Despite these interests, research output on the interrelationship between firms’ attributes, corporate social responsibility (CSR) disclosure and the performance of firms using the structural equation modeling approach while simultaneously obtaining evidence from a highly regulated sector - the financial services sector (comprising an amalgam of data from commercial banks, insurance companies, mortgage banks etc) seems scarce. Yet, a clearer understanding of the association between CSR and various firm specific attributes (firm value, capital structure, ownership concentration and board attributes) and/or the relationship between CSR and financial performance or the link between financial performance and firm attributes and vice versa will provide insights on the key drivers of firms’ financial performance and CSR disclosure of firms in such important sector.

). Despite these interests, research output on the interrelationship between firms’ attributes, corporate social responsibility (CSR) disclosure and the performance of firms using the structural equation modeling approach while simultaneously obtaining evidence from a highly regulated sector - the financial services sector (comprising an amalgam of data from commercial banks, insurance companies, mortgage banks etc) seems scarce. Yet, a clearer understanding of the association between CSR and various firm specific attributes (firm value, capital structure, ownership concentration and board attributes) and/or the relationship between CSR and financial performance or the link between financial performance and firm attributes and vice versa will provide insights on the key drivers of firms’ financial performance and CSR disclosure of firms in such important sector.

The researcher’s belief is that the results of this current study invariably presents a schema that will support management in designing policies and future strategic plans for their respective companies. This informed the current study which examined the interrelationship between firm specific attributes, CSR disclosure practices and the financial performance of listed Nigerian companies in the financial service sector.

1.1. Statement of the Problem

In recent time, there has been increased interest in full disclosure by firms due to recorded cases of worrisome financial scandals locally and internationally. The migration from reporting with local standards to reporting with global sets of international standards like the IFRSs has further renewed the interest in full disclosure by firms. Consequently, studies have shown that for firms to fully disclose their overall well being vis a vis their entire activities, disclosures on environmental and social concerns should form part of or be integrated into the various financial reports.

Surprisingly, indications from prior research evidence suggest that while a good number of firms now voluntarily disclose costs and related issues that are associated with CSR activities (Makori & Jagongo, 2013![]() ; Siueia, Wang, & Deladem, 2019

; Siueia, Wang, & Deladem, 2019![]() ) there are instances where companies eschew from reporting unfavourable outcomes on CSR and environmental concerns. This possibly is attributable to arguments that reporting negative externalities may have consequences on firms, hence, the minimal or non-disclosure of CSR and associated costs by most companies in Nigeria and other developing countries (Dibia & Onwuchekwa, 2015

) there are instances where companies eschew from reporting unfavourable outcomes on CSR and environmental concerns. This possibly is attributable to arguments that reporting negative externalities may have consequences on firms, hence, the minimal or non-disclosure of CSR and associated costs by most companies in Nigeria and other developing countries (Dibia & Onwuchekwa, 2015![]() ).

).

If companies must be environmentally/socially responsible, there would be need for studies to assess specific firms’ attributes that drives how environmental, economic, and social activities are recognized, and accounted for in the books. This however informed this current empirical investigation. The researcher hopes that the knowledge of any link between the disclosure of CSR and associated costs, firms’ attributes and performance will help the management of companies in designing and developing strategic policies/plans targeted at repositioning organizations in their respective success paths.

Additionally, we noticed that prior studies in accounting and related fields on CSR disclosures particularly in Nigeria concentrated more on how variables like corporate governance (board and audit committee attributes) determines CSR disclosure by firms; or the relationship between CSR costs and the performance of oil and gas or manufacturing companies (Agbiogwu, Ihendinihu, & Okafor, 2016![]() ; Ali & Attan, 2013

; Ali & Attan, 2013![]() ; Hassan & Ahmad, 2013

; Hassan & Ahmad, 2013![]() ; Jeroh & Okoro, 2016

; Jeroh & Okoro, 2016![]() ; Udo, 2019

; Udo, 2019![]() ; U. Uwuigbe & Egbide, 2013

; U. Uwuigbe & Egbide, 2013![]() ). While the focus of most prior studies within and outside Nigeria was on how performance indices of firms are affected by CSR disclosure (Belasri, Gomes, & Pijourlet, 2020

). While the focus of most prior studies within and outside Nigeria was on how performance indices of firms are affected by CSR disclosure (Belasri, Gomes, & Pijourlet, 2020![]() ; Bhattacharyya & Rahman, 2019

; Bhattacharyya & Rahman, 2019![]() ; Siueia et al., 2019

; Siueia et al., 2019![]() ), much concern was not directed at understanding how performance may possibly drive CSR disclosure or how firm performance may reinforce the effect of firms’ attributes like firm value, capital structure, ownership concentration and board attributes on CSR disclosure. This further created a lacuna which this study attempted to fill and stands different from existing studies in Nigeria and beyond. Efforts were made to obtain empirical evidence from a panel of firms which were intentionally drawn from the financial service sector. Specifically, we attempted to:

), much concern was not directed at understanding how performance may possibly drive CSR disclosure or how firm performance may reinforce the effect of firms’ attributes like firm value, capital structure, ownership concentration and board attributes on CSR disclosure. This further created a lacuna which this study attempted to fill and stands different from existing studies in Nigeria and beyond. Efforts were made to obtain empirical evidence from a panel of firms which were intentionally drawn from the financial service sector. Specifically, we attempted to:

- Ascertain the interrelationship between measures of firm value and financial performance of listed financial service companies in Nigeria.

- Analyse the link between measures of capital structure and financial performance of listed financial service companies in Nigeria.

- Examine how ownership concentration affects financial performance of listed financial service companies in Nigeria.

- Determine the relationship between measures of board attributes and financial performance of listed companies in Nigeria.

- Examine the interrelationship between measures of firm value and CSR disclosure of listed financial service companies in Nigeria.

- Analyse the link between measures of capital structure and CSR disclosure of listed financial service companies in Nigeria.

- Assess the interrelationship between ownership concentration and CSR disclosure of listed financial service companies in Nigeria.

- Determine the influence of board attributes on CSR disclosure of listed financial service companies in Nigeria.

- Examine the interrelationship between measures of financial performance and CSR disclosure of listed financial service companies in Nigeria.

2. CONCEPTUAL AND THEORETICAL FRAMEWORK

2.1. Conceptual Overview and Hypotheses Development

2.1.1. Financial Performance

The concept of “financial performance” describes how well organizations have fared in prescribed periods or years. Most analysts examine financial performance by obtaining data for reported indices in the financial statements of firms and expressing same in forms of financial ratios. According to Oshoke and Sumaina (2015![]() ), financial ratios, being the oldest instrument of analyzing firms’ performance, are the arithmetic expression of the relationship between variables and/or items reported in the financial statements of entities. They are mainly used as indicants of firms’ performances so that meaningful comparisons are made between certain measures/indicators and other related variables, either by looking at present or past/similar indicator(s) for a particular firm or similar firms in an industry (Kabajeh, Nu’aimat, & Dahmash, 2012

), financial ratios, being the oldest instrument of analyzing firms’ performance, are the arithmetic expression of the relationship between variables and/or items reported in the financial statements of entities. They are mainly used as indicants of firms’ performances so that meaningful comparisons are made between certain measures/indicators and other related variables, either by looking at present or past/similar indicator(s) for a particular firm or similar firms in an industry (Kabajeh, Nu’aimat, & Dahmash, 2012![]() ; Karakus & Bozkurt, 2017

; Karakus & Bozkurt, 2017![]() ).

).

Al-Matari, Al-Swidi, and Fadzil (2014![]() ) stated that in theory, the concept of financial performance forms the core of strategic management. Thus, in empirically assessing the strategies and processes of firms, several strategic studies have based their enquiry on the construct of business performance with emphasis on the drivers of financial performance of firms. While we agree with prior studies that costs associated with CSR are probable drivers of performance (Bhattacharyya & Rahman, 2019

) stated that in theory, the concept of financial performance forms the core of strategic management. Thus, in empirically assessing the strategies and processes of firms, several strategic studies have based their enquiry on the construct of business performance with emphasis on the drivers of financial performance of firms. While we agree with prior studies that costs associated with CSR are probable drivers of performance (Bhattacharyya & Rahman, 2019![]() ; Lin, Hung, Chou, & Lai, 2019

; Lin, Hung, Chou, & Lai, 2019![]() ; Siueia et al., 2019

; Siueia et al., 2019![]() ; Wang, Wang, Wang, & Yang, 2020

; Wang, Wang, Wang, & Yang, 2020![]() ), our concern on the possible effect which indicators of firms’ performance may have on the level of CSR disclosure among firms inspired this current study. Additionally, by obtaining empirical evidence from a panel of companies drawn from a highly regulated sector in Nigeria (financial service firms), this study examined how firms’ attributes (firm value, capital structure, ownership concentration and board attributes) affect firm performance and CSR disclosure.

), our concern on the possible effect which indicators of firms’ performance may have on the level of CSR disclosure among firms inspired this current study. Additionally, by obtaining empirical evidence from a panel of companies drawn from a highly regulated sector in Nigeria (financial service firms), this study examined how firms’ attributes (firm value, capital structure, ownership concentration and board attributes) affect firm performance and CSR disclosure.

2.1.2. CSR Disclosure and Firm Performance

CSR disclosure focus on helping entities to meet the ever increasing information needs of stakeholders generally. In essence, CSR reporting or disclosure provides opportunities for companies to identify and report costs associated with environmental and social engagements alongside the reports of their various economic activities. Through such reports, stakeholders can ultimately assess the two-way effect and related impacts of the activities of firms and their hosts.

By the propositions of the stakeholders’ theory, companies are indebted to several factions of individuals in the society in which they operate, thus making profitability and ethical behavior to be mutually inclusive (Belasri et al., 2020![]() ). Hence, companies are believed to have a duty to prepare financial reports capable of demonstrating financial value by detailing the impact of their overall activities on the society and vice versa. While several incentives for CSR disclosure exist (Bae, El Ghoul, Guedhami, Kwok, & Zheng, 2018

). Hence, companies are believed to have a duty to prepare financial reports capable of demonstrating financial value by detailing the impact of their overall activities on the society and vice versa. While several incentives for CSR disclosure exist (Bae, El Ghoul, Guedhami, Kwok, & Zheng, 2018![]() ; Belasri et al., 2020

; Belasri et al., 2020![]() ; Huang & Watson, 2015

; Huang & Watson, 2015![]() ; Mathuva & Kiweu, 2016

; Mathuva & Kiweu, 2016![]() ; Ting, 2020

; Ting, 2020![]() ; Umoren et al., 2017

; Umoren et al., 2017![]() ), the arguments in favour of full disclosure by firms have led to several studies on CSR reporting within the last few years. Despite the interests in CSR disclosure among firms, we observed that studies have not been conducted in Nigeria to examine the effect which firm performance would have on CSR disclosure, rather; the reverse has been the concern of the bulk of Nigerian studies in this domain. We therefore hypothesized that:

), the arguments in favour of full disclosure by firms have led to several studies on CSR reporting within the last few years. Despite the interests in CSR disclosure among firms, we observed that studies have not been conducted in Nigeria to examine the effect which firm performance would have on CSR disclosure, rather; the reverse has been the concern of the bulk of Nigerian studies in this domain. We therefore hypothesized that:

HO1: measures of firm performance do not have significant effect on CSR disclosure among Nigerian firms.

2.1.3. Firm Value, Financial Performance and CSR Disclosure

Studies have shown that the effort of management which is mainly targeted at maximizing the overall wealth of identifiable shareholders goes a long way to increase the value of firms. Most likely, the value of firms clearly indicates their level of prosperity. This is why most investors concern themselves more on the concept of firm value (Shuaibu, Ali, & Moh’Amin, 2019![]() ). As noticed from the outcome of prior studies, firm value can be analyzed from different perspectives; hence, several proxies have been developed to measure the concept (Adeyemi & Oboh, 2011

). As noticed from the outcome of prior studies, firm value can be analyzed from different perspectives; hence, several proxies have been developed to measure the concept (Adeyemi & Oboh, 2011![]() ; Aggarwal & Padhan, 2017

; Aggarwal & Padhan, 2017![]() ; Gupta, Kennedy, & Weaver, 2009

; Gupta, Kennedy, & Weaver, 2009![]() ; Oh & Kim, 2016

; Oh & Kim, 2016![]() ). The common proxies for firm value found in extant studies includes Tobin’s Q, share price, and market price to book value. While studies outside Nigeria have continuously produced mixed findings on the link between several measures of firm value and measures of financial performance, much has not been documented on the relationship between firm value and CSR disclosure. On this premise, we thus hypothesized that:

). The common proxies for firm value found in extant studies includes Tobin’s Q, share price, and market price to book value. While studies outside Nigeria have continuously produced mixed findings on the link between several measures of firm value and measures of financial performance, much has not been documented on the relationship between firm value and CSR disclosure. On this premise, we thus hypothesized that:

HO2: measures of firm value does not exert significant influence on the financial performance of Nigerian firms.

HO3: there is no significant relationship between firm value and CSR disclosure among Nigerian firms.

2.1.4. Capital Structure, Financial Performance and CSR Disclosure

Capital structure which accentuates on the debt and equity mix among firms has attracted several studies. Its application to the mitigation of agency costs while simultaneously increasing companies’ performances have received notable academic debates (Abeywardhana, 2015![]() ; Ardalan, 2018

; Ardalan, 2018![]() ; Manawaduge, Zoysa, & Chandrakumara, 2010

; Manawaduge, Zoysa, & Chandrakumara, 2010![]() ; Nenu, Vintila, & Gherghina, 2018

; Nenu, Vintila, & Gherghina, 2018![]() ; Nguyen, Ho, & Vo, 2019

; Nguyen, Ho, & Vo, 2019![]() ). According to Salam and Shourkashti (2019

). According to Salam and Shourkashti (2019![]() ), capital structure refers to the financial structure of identified firms and includes a mix of such firms’ debt and equities’ components. Capital structure sometimes explains the proportion of a company’s capital that may have been obtained from outside sources and employed in financing the company’s overall asset base. To date, while extant studies have drawn a link between companies’ capital structure and their respective dividend policies and financial performances (Abor, 2005

), capital structure refers to the financial structure of identified firms and includes a mix of such firms’ debt and equities’ components. Capital structure sometimes explains the proportion of a company’s capital that may have been obtained from outside sources and employed in financing the company’s overall asset base. To date, while extant studies have drawn a link between companies’ capital structure and their respective dividend policies and financial performances (Abor, 2005![]() ; Manawaduge et al., 2010

; Manawaduge et al., 2010![]() ; Muritala, 2012

; Muritala, 2012![]() ), little concern has been placed on the effect that a firm’s capital structure may have on CSR disclosure. On this note, we proposed the following:

), little concern has been placed on the effect that a firm’s capital structure may have on CSR disclosure. On this note, we proposed the following:

HO4: Capital structure does not have significant influence on the financial performance of Nigerian firms.

HO5: There is no significant relationship between capital structure and CSR disclosure among Nigerian firms.

2.1.5. Ownership Structure, Financial Performance and CSR Disclosure

Ownership structure, otherwise known as ownership concentration remains one vital internal mechanism of corporate governance that focus primarily on the proportion of block ownership or shareholding that has the incentives and/or available resources and capabilities to discipline management and monitor their respective activities (Boerkamp, 2016![]() ; Madhani, 2016

; Madhani, 2016![]() ; Onder, 2003

; Onder, 2003![]() ; Pathirawasam & Wickremasinghe, 2012

; Pathirawasam & Wickremasinghe, 2012![]() ; Vintilă & Gherghina, 2014

; Vintilă & Gherghina, 2014![]() ; Vintilă, Gherghina, & Nedelescu, 2014

; Vintilă, Gherghina, & Nedelescu, 2014![]() ; Wrońska-Bukalska & Golec, 2015

; Wrońska-Bukalska & Golec, 2015![]() ). Ownership concentration explains the extent to which owners of companies, given the proportion of their shareholding could, in the best interests of shareholders, control the actions of management. Prior studies have categorized ownership concentration into block holders ownership, institutional ownership, government ownership, family ownership, foreign ownership, bank ownership amongst others (Boerkamp, 2016

). Ownership concentration explains the extent to which owners of companies, given the proportion of their shareholding could, in the best interests of shareholders, control the actions of management. Prior studies have categorized ownership concentration into block holders ownership, institutional ownership, government ownership, family ownership, foreign ownership, bank ownership amongst others (Boerkamp, 2016![]() ; Dakhlallh, Rashid, Abdullah, & Dakhlallh, 2019

; Dakhlallh, Rashid, Abdullah, & Dakhlallh, 2019![]() ; Horobet, Belascu, Curea, & Pentescu, 2019

; Horobet, Belascu, Curea, & Pentescu, 2019![]() ; Madhani, 2016

; Madhani, 2016![]() ; Onder, 2003

; Onder, 2003![]() ; Vintilă & Gherghina, 2014

; Vintilă & Gherghina, 2014![]() ).

).

Wahab, How, and Verhoeven (2008![]() ) maintained that institutional investors are more sensitive to the reporting practices of firms. This partly accounts for the conclusion that ownership structure may possibly influence companies’ policies, regarding voluntary disclosure and by extension, CSR and sustainability reporting. Consequently, Chrysostom, Freire, and Parente (2013

) maintained that institutional investors are more sensitive to the reporting practices of firms. This partly accounts for the conclusion that ownership structure may possibly influence companies’ policies, regarding voluntary disclosure and by extension, CSR and sustainability reporting. Consequently, Chrysostom, Freire, and Parente (2013![]() ) believed that if firms’ ownership structures have direct influence on their policies, the possibility of drawing a link between CSR disclosure and ownership structure cannot be ruled out.

) believed that if firms’ ownership structures have direct influence on their policies, the possibility of drawing a link between CSR disclosure and ownership structure cannot be ruled out.

Dam and Scholtens (2013![]() ) maintained that stock control exerts a negative influence on the disclosure policies of firms since higher ownership concentration may result in lower levels of disclosures. Given the above, this study also assessed the relationship between ownership structure and CSR disclosures of listed firms by drawing evidence from Nigeria and based on the following postulations:

) maintained that stock control exerts a negative influence on the disclosure policies of firms since higher ownership concentration may result in lower levels of disclosures. Given the above, this study also assessed the relationship between ownership structure and CSR disclosures of listed firms by drawing evidence from Nigeria and based on the following postulations:

HO6: The ownership structure of firms does not have significant influence on the financial performance of Nigerian firms.

HO7: There is no significant relationship between ownership structure and CSR disclosure among Nigerian firms.

2.1.6. Board Attributes, Financial Performance and CSR Disclosure

The aftermath of recorded cases of corporate collapse was the increase in repeated calls for the institution of discipline, high regulation and the monitoring of entities and their respective management through corporate governance. An important measure of good corporate governance among firms is the structure of their respective Boards since management’s actions are mostly informed by the decisions reached at boardroom (Abu, Okpeh, & Okpe, 2016![]() ; Kajola, Onaolapo, & Adelowotan, 2017

; Kajola, Onaolapo, & Adelowotan, 2017![]() ). Apparently, board attributes/structure will mostly be assessed with reference to their sizes, levels of independence, diligence, gender diversity, amongst others (Ghabayen, Mohamad, & Ahmad, 2016

). Apparently, board attributes/structure will mostly be assessed with reference to their sizes, levels of independence, diligence, gender diversity, amongst others (Ghabayen, Mohamad, & Ahmad, 2016![]() ; Joshi & Hyderabad, 2019

; Joshi & Hyderabad, 2019![]() ; Naseem, Rehman, Ikram, & Malik, 2017

; Naseem, Rehman, Ikram, & Malik, 2017![]() ). \

Results on the presumed relationship between measures of board attributes and performance or between board attributes and CSR disclosure have remained contradictory and mixed over time. While studies have argued that larger boards facilitates the prompt completion of key routine functions of the board and consequently impact positively on performance, a school of thought believes that larger boards encounter agency and communication problems and often times lack proper coordination which invariably plummet firm’s overall long-run performance (Anis, Chizema, Lui, & Fakhreldin, 2017

). \

Results on the presumed relationship between measures of board attributes and performance or between board attributes and CSR disclosure have remained contradictory and mixed over time. While studies have argued that larger boards facilitates the prompt completion of key routine functions of the board and consequently impact positively on performance, a school of thought believes that larger boards encounter agency and communication problems and often times lack proper coordination which invariably plummet firm’s overall long-run performance (Anis, Chizema, Lui, & Fakhreldin, 2017![]() ; Borlea, Achim, & Mare, 2017

; Borlea, Achim, & Mare, 2017![]() ; Ghosh & Ansari, 2018

; Ghosh & Ansari, 2018![]() ). Additionally, the effects which the level of independence and boardroom diversity may have on performance have been examined by prior studies (Aifuwa & Embele, 2019

). Additionally, the effects which the level of independence and boardroom diversity may have on performance have been examined by prior studies (Aifuwa & Embele, 2019![]() ; Anis et al., 2017

; Anis et al., 2017![]() ; Borlea et al., 2017

; Borlea et al., 2017![]() ; Ng, Teh, Ong, & Soh, 2016

; Ng, Teh, Ong, & Soh, 2016![]() ) yet with mixed findings.

) yet with mixed findings.

In the Nigerian context, while the bulk of such studies in the financial service sector relied only on data from commercial banks, data from other classes of companies like mortgage banks and insurance companies which are also listed in the financial service sector have largely been avoided. Reliance on data across all business types/operations and/or companies in the financial service sector distinguishes this study from extant studies in Nigeria.

No doubt, studies have also examined how board attributes affect CSR disclosures (Esa & Zahari, 2016![]() ; Ghabayen et al., 2016

; Ghabayen et al., 2016![]() ; Joshi & Hyderabad, 2019

; Joshi & Hyderabad, 2019![]() ; Naseem et al., 2017

; Naseem et al., 2017![]() ). These studies have not established whether or not firm performance has the capacity of reinforcing the effect that board attributes may have on CSR disclosure.

). These studies have not established whether or not firm performance has the capacity of reinforcing the effect that board attributes may have on CSR disclosure.

Given this this study postulated thus:

HO8: Board attributes does not have significant influence on the financial performance of Nigerian firms.

HO9: There is no significant relationship between board attributes and CSR disclosure among Nigerian firms.

2.2. Theoretical Framework

This study was based on the arguments of the legitimacy theory. The legitimacy theory which was propounded by Max Weber in 1947 and further developed by Lindblom (1994![]() ) and Suchman (1995

) and Suchman (1995![]() ) pointed out that legitimacy is a condition that drives entities to ensure that their respective value system remains congruent with the value system of a larger society or social system in which they operate (Ghabayen et al., 2016

) pointed out that legitimacy is a condition that drives entities to ensure that their respective value system remains congruent with the value system of a larger society or social system in which they operate (Ghabayen et al., 2016![]() ; Naseem et al., 2017

; Naseem et al., 2017![]() ; Uwalomwa Uwuigbe & Jimoh, 2012

; Uwalomwa Uwuigbe & Jimoh, 2012![]() ).

).

According to Aghdam (2015![]() ) the legitimacy theory explains companies’ considerations, concerns and expectations in relation to their actions/activities which ought to be legitimate in the views of stakeholders who at all time expect that companies would conduct themselves in a socially, acceptable and safe manner. As organizations continue to operate within the domain and norms of the society, it is believed that they will use several disclosure strategies to preserve their respective images of being socially responsible corporate citizens. This is necessary as it possibly will guarantee continued access to resources needed for the success of the business. It is on this note that the legitimacy theory was adopted to underpin this research as it seeks to explain how companies conduct themselves and carry out their operations in ways that will not harm the society, while simultaneously enhancing their financial performance and narrowing the gap between companies’ actions and social expectations.

) the legitimacy theory explains companies’ considerations, concerns and expectations in relation to their actions/activities which ought to be legitimate in the views of stakeholders who at all time expect that companies would conduct themselves in a socially, acceptable and safe manner. As organizations continue to operate within the domain and norms of the society, it is believed that they will use several disclosure strategies to preserve their respective images of being socially responsible corporate citizens. This is necessary as it possibly will guarantee continued access to resources needed for the success of the business. It is on this note that the legitimacy theory was adopted to underpin this research as it seeks to explain how companies conduct themselves and carry out their operations in ways that will not harm the society, while simultaneously enhancing their financial performance and narrowing the gap between companies’ actions and social expectations.

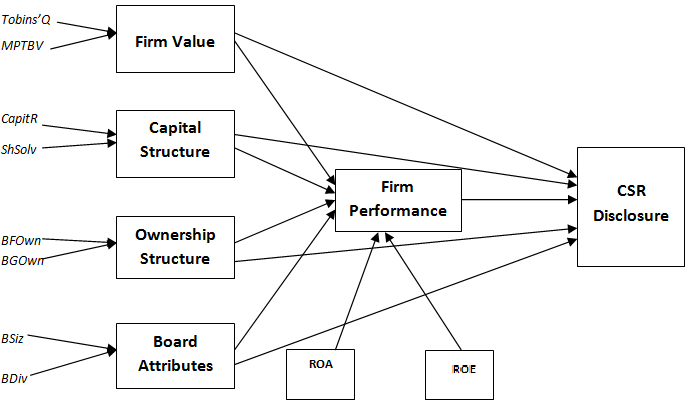

2.3. Conceptual Framework

This study which examined the interrelationship between measures of firm attributes, performance and CSR disclosure was anchored on the conceptualized framework depicted in Figure 1.

Figure-1. Conceptual Framework of the study.

3. RESEARCH METHODS

This study was driven by the ex-post facto research design. The data sourced were secondary in nature and collated from the financials of 29 listed firms in the financial service sector over the study period (2009 to 2018). The sampled 29 firms were purposely selected without bias and included in the study based on data availability for the variables of interest. Before arriving at the sample size of 29 companies, all listed firms in the sector that failed to consistently report data for the variables used in the study over the study period were dropped. Table 1 presents the distribution of the sampled firms across their business types/operations. The decision to focus on the financial service sector was justified by the existence of scanty prior empirical evidence in Nigeria in this area of discourse. Additionally, it was believed that this sector is highly regulated; yet, bothers less on environmental and social responsibility concerns given the nature of their businesses and operational activities.

We used relevant quantitative techniques in analyzing the collated data. However, since our primary concern was not on describing the nature or behavior of the dataset obtained, results for descriptive statistics were not included for discussion in this study. To confirm whether the study’s model met the required rules for estimations, the data were subjected to tests of goodness of fit (GOF) – equation level and overall. In testing our hypotheses, we adopted the SEM for its ability to correct errors which may have resulted from errors of measurements.

Table-1. Distribution of sampled financial service firms

| S/N | Category/ Nature of Firm's Business | Frequency |

| 1 | Commercial Banks | 12 |

| 2 | Life Insurance | 1 |

| 3 | Mortgage Banks | 1 |

| 4 | Multiline Insurance | 4 |

| 5 | Non-Life Insurance | 10 |

| 6 | Re-Insurance | 1 |

| Total | 29 | |

Table-2. Variables and measurements.

| Variable Name | Label | Defintion |

| CSR Disclosure | CSRD | CSR disclosure of firms (Measured by dummy variable of 1 representing the presence of environmental section in the annual reports of each firm, otherwise, 0) |

| Firm Performance | Fperf | The performance of firm in terms of growth in revenue base |

| Firm Value | Fval | The value of each firm as measured by the Last Day Share price of each company. |

| Capital Structure | Capstrct | Each firm's capital structure as measured by the ratio of debt to total assets for each year. |

| Ownership Structure | Ownstrct | The ownership structure of each firm as measured by the block ownership concentration which is measured as the percentage of all the block shareholders with a controlling interest of about 5% and above |

| Board Atrributes | BoardAttr | Board characteristics of firm as measured by the level of independence of each firm's board of directors in each year. |

| Tobins'Q | Tobins'Q | Tobins’ Q as measured by (the ratio of each firm's market capitalization plus Total liabilities less cash flows) divided by total assets |

| Market Price To Book Value of shares | MPTBV | This is the ratio of the Market price of each firm's shares to their respective book values |

| Long Term Debt to Asset Ratio | CapitR | This is a measure of capital structure measured as the ratio of long term debt to total assets of each firm |

| Short Term Debt to Asset Ratio | ShSolv | This is another measure of capital structure measured as the ratio of short term debt to total assets of each firm |

| Block Family Ownership | BFOwn | This is measured as the percentage of single individual shareholding that is 5% and above. |

| Block Government Ownership | BGOwn | This is measured as the percentage of government shareholding that is 5% and above. |

| Board Size | Bsiz | Board Size (measured by the number of board members) |

| Board Diversity | Bdiv | Board gender diversity (measured by the ratio of the number of women in each board to the total number of board members |

| Return on Asset | ROA | ROA as measured by Profit After Tax divided by Total Assets |

| Return on Equity | ROE | ROE as measured by Profit After Tax divided by Total Equity |

3.1. Correlation Analysis

The correlation analysis of all measures/proxies of the variables of interest in this study was conducted and the results shown in Table 3.

Table-3. Correlation result.

Variables |

CSRD |

Tobins'Q |

MPTBV |

CapitR |

ShSolv |

BFOwn |

BGOwn |

BSiz |

BDiv |

ROA |

ROE |

CSRD |

1.000 |

0.156 |

0.007 |

0.001 |

0.243 |

-0.001 |

0.093 |

0.224 |

-0.054 |

-0.097 |

0.071 |

Tobin's Q |

1.000 |

0.367 |

0.218 |

0.368 |

-0.007 |

0.047 |

0.186 |

-0.084 |

-0.223 |

-0.048 |

|

MPTBV |

1.000 |

-0.157 |

0.182 |

0.091 |

-0.074 |

-0.024 |

0.170 |

0.053 |

-0.296 |

||

CapitR |

1.000 |

-0.606 |

0.020 |

0.041 |

-0.177 |

0.022 |

-0.067 |

0.038 |

|||

ShSolv |

1.000 |

-0.129 |

-0.125 |

0.502 |

-0.047 |

-0.175 |

-0.072 |

||||

BFOwn |

1.000 |

-0.031 |

-0.247 |

-0.141 |

0.242 |

0.057 |

|||||

BGOwn |

1.000 |

0.014 |

-0.114 |

-0.073 |

-0.015 |

||||||

Bsiz |

1.000 |

-0.008 |

-0.176 |

-0.034 |

|||||||

BDiv |

1.000 |

0.085 |

0.079 |

||||||||

ROA |

1.000 |

0.344 |

|||||||||

ROE |

1.000 |

Table 3 reveals the result of the correlation analysis of the measures of the entire variable set. As revealed in the table, the variables were either positively correlated or negatively correlated. CSRD for instance was positively correlated with measures of firm value (Tobins’Q and MPTBV), capital structure (CapitR and ShSolv), and then BGOwn, BSiz and ROE, while simultaneously recording a negative correlation with BFOwn, BDiv and ROA respectively. This means that a unit increase in the value of each of the variables (Tobins’Q, MPTBV, CapitR, ShSolv, BGOwn, BSiz and ROE) will result in increase in the level or extent of CSR disclosure by firms, though depending on the coefficient reported for each of the variable. Similarly, every unit increase in block family ownership (BFOwn), board diversity (BDiv) and ROA will result in a decrease in the level of CSRD disclosure by firms.

A closer look at the coefficients indicates that (not minding the signs) the correlation values reported ranged between 0.001 (correlation coefficient between BFOwn and CSRD) and 0.606 (correlation coefficient between ShSolv and CapitR). With 0.606 as the highest coefficient among the variables, we concluded that the problem of multicollinearity was not evident among our data set. It became necessary for us to proceed with our analysis by further conducting a Goodness of Fit (GOF) test to establish the fitness of the study’s model. The outcome of the GOF test is presented in the next section of this paper.

3.2. Goodness of Fit (GOF)

In testing the suitability of the data generated for this study vis a vis the fitness of the model, the equation level and overall goodness of fit tests were conducted. In this light, several indicators were applied to establish the level of fitness and of course, the justification of the overall suitability of our data and model. Table 4 presents the results of the GOF test.

Table-4. GOF index.

| Overall GOF | ||||

| GOF Indicator/Index | Fit Criteria |

Result |

p-value |

Decision |

| Likelihood Ratio (L-R) - chi2_ms(54) | 308.708 |

0.000** |

Good Fit |

|

| Likelihood Ratio (L-R) - chi2_bs(92) | 3051.191 |

0.000** |

Good Fit |

|

| Standardized Root Mean Squared Resid. | ≤ 0.08 |

0.078 |

Good Fit |

|

| Comparative-Fit Index (CFI) | > 0.8 |

0.914 |

Good Fit |

|

| Tucker-Lewis Index (TLI) | > 0.8 |

0.853 |

Good Fit |

|

| Equation Level GOF | ||||

| Observed Variables | Fitted values |

Variance Predicted |

Residual |

R-Squared |

| Firm value | 49.7733 |

13.2578 |

36.5155 |

0.2663 |

| Capital Structure | 758.0387 |

757.8859 |

0.1528 |

0.9998 |

| Ownership Structure | 0.0513 |

0.0060 |

0.0453 |

0.1172 |

| Board Attributes | 145.8677 |

14.0720 |

131.7957 |

0.0965 |

| Firm Performance | 1411.975 |

57.8886 |

1354.086 |

0.0410 |

| CSR Disclosure | 0.2201604 |

0.0384 |

0.1817 |

0.1747 |

| Overall | 0.9999 |

|||

| Decision | Good Fit |

|||

In judging by the results from the entire GOF index, it was evident that this study’s data and model met the overall suitability criteria. For instance, the L-R chi2 obtained for both the model and baseline (308.708 and 3,051.191 respectively) had p-values of 0.000 respectively. Similarly, results for the baseline comparison (CFI and TLI) presented values (0.914 and 0.853 respectively) that were greater than the minimum required threshold of 0.80. Also, the SRMSR of 0.078 was less than the required threshold of 0.08 (see Purusottama (2020![]() )). Additionally, the results of the equation level GOF (for all variables) further confirmed the result of the overall GOF. We therefore concluded that the model and data are appropriate and usable for this study. Further results from the SEM output regarding the tests of hypotheses are presented in the next section.

)). Additionally, the results of the equation level GOF (for all variables) further confirmed the result of the overall GOF. We therefore concluded that the model and data are appropriate and usable for this study. Further results from the SEM output regarding the tests of hypotheses are presented in the next section.

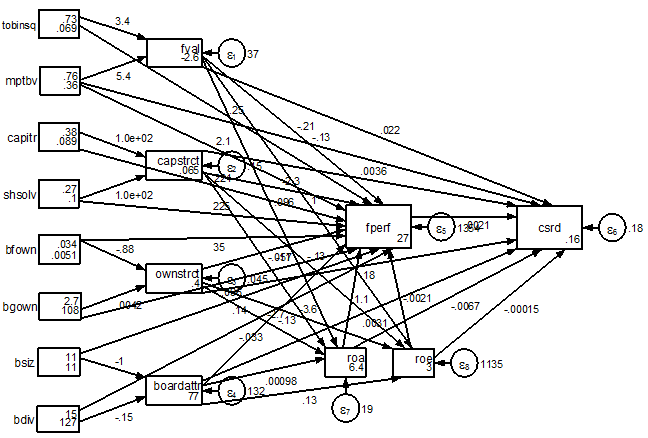

3.3. Tests of Hypotheses

Considering the variables of interest, this study advanced nine (9) hypotheses which were tested and the results presented in Table 5 and Figure 1 respectively. From the results, only 3 (HO1, HO3 and HO5) out of the 9 hypotheses were consistent with the a-priori expectation and were rejected. Thus, we could not reject 6 hypotheses (HO2, HO4, HO6, HO7, HO8 and HO9) because the relationships/constructs produced | z | values which were below the required minimum when matched with their respective table values. Additionally, the p-values generated respectively for HO2, HO4, HO6, HO7, HO8 and HO9 were 0.625, 0.687, 0.318, 0.133, 0.517 and 0.155. These values were above the maximum required (p<0.05); an indication that the relationship among the constructs were not significant at the 95% confidence level.

Table-5. Results of tests of hypotheses.

Hypothesis |

Relationship |

Coefficient |

Z |

p > | z | |

Decision |

HO1 |

Fperf ---> CSRD |

0.0021296 |

3.14 |

0.002** |

Rejected |

HO2 |

Fval ---> Fperf |

-0.2126858 |

-0.49 |

0.625 |

Not Rejected |

HO3 |

Fval ---> CSRD |

0.0223138 |

4.64 |

0.000** |

Rejected |

HO4 |

Capstrct ---> Fperf |

-2.269271 |

-0.40 |

0.687 |

Not Rejected |

HO5 |

Capstrct ---> CSRD |

0.0035826 |

3.47 |

0.001** |

Rejected |

HO6 |

Ownstrct ---> Fperf |

-11.110840 |

-1.00 |

0.318 |

Not Rejected |

HO7 |

Ownstrct ---> CSRD |

0.1762376 |

1.50 |

0.133 |

Not Rejected |

HO8 |

BoardAttr ---> Fperf |

-0.1282424 |

-0.65 |

0.517 |

Not Rejected |

HO9 |

BoardAttr ---> CSRD |

0.0031004 |

1.42 |

0.155 |

Not Rejected |

Note:**significant.

Figure-2. SEM Output.

4. DISCUSSIONS

The results from the tested hypotheses gave insights on the link between the variables assessed in this study. As shown in Table 5 and Figure 2 respectively, with a coefficient of approximately 0.0021296, and a z-score of 3.14 (p>| z | = 0.002) for hypothesis 1, the relationship between firm performance and CSR disclosure was positive and significant; hence, the hypothesis that measures of firm performance (Fperf) do not have significant effect on CSR disclosure (CSRD) among Nigerian firms was rejected.

While this finding supports arguments that a significant relationship exists between firm performance and CSR disclosure (Belasri et al., 2020![]() ; Bhattacharyya & Rahman, 2019

; Bhattacharyya & Rahman, 2019![]() ; Kao, Yeh, Wang, & Fung, 2018

; Kao, Yeh, Wang, & Fung, 2018![]() ; Lin et al., 2019

; Lin et al., 2019![]() ; Siueia et al., 2019

; Siueia et al., 2019![]() ; Umoren et al., 2017

; Umoren et al., 2017![]() ; Wang et al., 2020

; Wang et al., 2020![]() ) we however emphasize that managements’ decision to fully disclose issues bordering on CSR is significantly influenced by the level of their respective financial performance. This implies that firms whose performance indices are below the industry average may likely embark on lesser CSR activities and subsequently left with little or no disclosure on CRS concerns. Thus, we conclude that every unit increase or improvement in the performance of firms will ultimately result to an increase in the level of CSR disclosure among firms.

) we however emphasize that managements’ decision to fully disclose issues bordering on CSR is significantly influenced by the level of their respective financial performance. This implies that firms whose performance indices are below the industry average may likely embark on lesser CSR activities and subsequently left with little or no disclosure on CRS concerns. Thus, we conclude that every unit increase or improvement in the performance of firms will ultimately result to an increase in the level of CSR disclosure among firms.

We observed from the result of hypothesis 2 that the relationship between measures of firm value and firm performance was negative and not significant. This was evident from the reported coefficient of -0.2126858 and a z-score of -0.49 (p>| z | = 0.625). With this result, the hypothesis that measures of firm value does not exert significant influence on the financial performance of Nigerian firms was not rejected. This means that even though prior studies have shown that the performance of firms have significant influence on firm value (Birgili & Düzer, 2010![]() ; Karakus & Bozkurt, 2017

; Karakus & Bozkurt, 2017![]() ; Vedd & Yassinski, 2015

; Vedd & Yassinski, 2015![]() ) our study proved that the reverse was not the case, as measures of firm value could not exert significant influence on the financial performance of firms. Conclusively, higher firm values do not increase the financial performance of Nigerian firms.

) our study proved that the reverse was not the case, as measures of firm value could not exert significant influence on the financial performance of firms. Conclusively, higher firm values do not increase the financial performance of Nigerian firms.

Additionally, going by the result of hypothesis 3, with a coefficient of approximately 0.0223138, and a z-score of 4.64 (p>| z | = 0.000), the relationship between firm value and CSR disclosure was positive and significant; hence, the hypothesis that there is no significant relationship between firm value (Fval) and CSR disclosure (CSRD) among Nigerian firms was rejected. This research evidence was in line with several studies (Anggraini, 2006![]() ; Moeljadi, 2014

; Moeljadi, 2014![]() ). This implied that an increase in firm value stimulates CSR disclosure among firms. This may possibly be linked with the belief that an increased market share in addition to increase in the market price to book value of companies largely spur entities to be more environmentally friendly; thereby, increasing their costs/expenditure on environmental engagements/concerns. No doubt, where firms incur huge environmental costs the need to disclosure such cost in their respective financial statements need not be overemphasized.

). This implied that an increase in firm value stimulates CSR disclosure among firms. This may possibly be linked with the belief that an increased market share in addition to increase in the market price to book value of companies largely spur entities to be more environmentally friendly; thereby, increasing their costs/expenditure on environmental engagements/concerns. No doubt, where firms incur huge environmental costs the need to disclosure such cost in their respective financial statements need not be overemphasized.

However, the result for hypothesis 4 suggested that the relationship between measures of capital structure and firm performance was negative and not significant. This was revealed from the reported coefficient of -2.269271 and a z-score of -0.40 (p>| z | = 0.687). Thus, we could not reject the hypothesis that capital structure does not have significant influence on the financial performance of Nigerian firms. This finding supported that of Ahmed and Ibrahim (2015![]() ) but was at variance with those of Nenu et al. (2018

) but was at variance with those of Nenu et al. (2018![]() ) and Alghusin (2015

) and Alghusin (2015![]() ). The above further suggests that the decision of firms to finance asset acquisition through debt may be counter-productive; thereby exerting negative influence on firms’ financial performance. This is because funds that would have been channeled to more productive ventures would otherwise be used to either repay outstanding debts/loans or service the associated costs of borrowing.

). The above further suggests that the decision of firms to finance asset acquisition through debt may be counter-productive; thereby exerting negative influence on firms’ financial performance. This is because funds that would have been channeled to more productive ventures would otherwise be used to either repay outstanding debts/loans or service the associated costs of borrowing.

We also sought to examine the association between capital structure and CSR disclosure among firms. In this light, the result for hypothesis 5 produced a coefficient of 0.0035826 alongside a z-score of 3.47 (p>| z | = 0.001); thus indicating that capital structure exerts significant and positive influence on CSR disclosure among Nigerian firms. Despite prior research evidence that CSR exerts no or negative impact on the leverage of firms (Sheikh, 2018![]() ) the outcome of our analysis led to the rejection of hypothesis 5; thus suggesting that components of firms’ capital structure has significant influence on CSR disclosure among firms.

) the outcome of our analysis led to the rejection of hypothesis 5; thus suggesting that components of firms’ capital structure has significant influence on CSR disclosure among firms.

Based on hypothesis 6, we examined the relationship between ownership structure and firms’ financial performance. Results in this regards as revealed in Figure 1 and in Table 5 indicated that with a coefficient of -11.110840 and a computed z-score of -1.00 (p>| z | = 0.318), the hypothesis that ownership structure of firms does not have significant influence on the financial performance of Nigerian firms was not rejected. This was contrary to the findings of Ciftci, Tatoglu, Wood, Demirbag, and Zaim (2019![]() ) who assert that companies whose ownership is more concentrated in the hands of family members tend to experience increased financial performance.

) who assert that companies whose ownership is more concentrated in the hands of family members tend to experience increased financial performance.

In establishing the link between ownership structure and CSR disclosure, we refer to the result for hypothesis 7 which produced a correlation coefficient of 0.1762376 and a computed z-score of 1.50 (p>| z | = 0.133). We could not reject the hypothesis that there was no significant relationship between ownership structure and CSR disclosure among Nigerian firms. Thus, contrary to the earlier findings of Madden, McMillan, and Harris (2020![]() ) and Tang, Yang, and Yang (2020

) and Tang, Yang, and Yang (2020![]() ) our conclusion was that firms’ ownership does not significantly influence CSR engagement and/or disclosure. The implication was that even though owners may have the capacity to influence companies’ policies; their level of sensitivity to reporting practice may not be a significant determinant of CSR disclosure by firms. This position was in line with the views of Choi, Han, and Kwon (2019

) our conclusion was that firms’ ownership does not significantly influence CSR engagement and/or disclosure. The implication was that even though owners may have the capacity to influence companies’ policies; their level of sensitivity to reporting practice may not be a significant determinant of CSR disclosure by firms. This position was in line with the views of Choi, Han, and Kwon (2019![]() ).

).

From the result of hypothesis 8 the relationship between measures of Board attributes and firms’ financial performance was examined and reported as negative and not significant. This was revealed from the reported coefficient of -0.1282424 and a z-score of -0.65 (p>| z | = 0.517). With this result, we could not reject the hypothesis that board attributes does not have significant influence on the financial performance of Nigerian firms. Given the above result, this study however argues that larger boards exert negative influence on the financial performance of firms. Similarly, having a more diversified board along gender delineations does not guarantee higher levels of financial performance in organizations. This may be attributable to agency and communication problems common with larger and more diversified boards as identified in prior literature.

Finally, with the postulation in hypothesis 9, we examined the relationship between board attributes and CSR disclosure among Nigerian firms. The result revealed a correlation coefficient of 0.0031004 and a computed z-score of 1.42 (p>| z | = 0.155), thus suggesting that the relationship between board attributes and CSR disclosure was positive, but not significant. This means that an increase in the size and/or level of diversity among corporate boards would not significantly increase the level of CSR disclosure among firms.

5. CONCLUSION AND RECOMMENDATIONS

This study empirically examined the interrelationship between firms’ attributes, CSR disclosure and the financial performance of listed companies. Data were sourced from the financials of 29 listed firms in the financial service sector over a 10-year period (2009 – 2018). The SEM estimation techniques were carefully applied to estimate the link and interrelatedness among the constructs of the study based on 9 postulated hypotheses. We observed that variables like firm performance, firm value and capital structure of firms had significant influence on the level of CSR disclosures among listed financial service firms in Nigeria. Further results from our estimations indicated that ownership structure and board attributes do not exert significant influence on CSR disclosure among firms. Similarly, firm value, capital structure, ownership structure and board attributes were found to have negative and insignificant relationship with the performance of financial service firms in Nigeria. With these results, we recommend as follows:

- Since performance significantly drives the level of CSR disclosure, the management of firms are therefore admonished to strategically expand their market share through improved products that will increase their overall earnings; and by extension, CSR engagements.

- Also, since higher firm value does not automatically transmit into higher levels of performance, investors and investment analysts should be more systematic when using firm value in assessing future prospects/performance of firms.

- Corporate organizations should eschew from financing asset acquisition through debts.

- Entities should be more involved in environmental engagements; and costs associated with such engagements should be reported in the financial statements alongside the mainstream reports.

- In assessing the prospects/performances of firms, management and stakeholders should concentrate less on variables like capital structure, firm value, ownership structure and board attributes as they have proved to have no significant influence on performance or revenue growth of firms.

Funding: This study received no specific financial support. |

Competing Interests: The author declares that there are no conflicts of interests regarding the publication of this paper. |

REFERENCES

Abdulrahman, S. (2014). The effect of corporate social responsibility on total assets of quoted conglomerates in Nigeria. Journal of Educational Policy and Entrepreneurial Research, 1(2), 69-79.

Abeywardhana, Y. D. (2015). Capital structure and profitability: An empirical analysis of SMEs in the UK. Journal of Emerging Issues in Economics, Finance and Banking, 4(2), 1661-1675.

Abor, J. (2005). The effect of capital structure on profitability: An empirical analysis of listed firms in Ghana. The Journal of Risk Finance, 6(5), 438-445.

Abu, S. O., Okpeh, A. J., & Okpe, U. J. (2016). Board characteristics and financial performance of deposit money banks in Nigeria. International Journal of Business and Social Science, 7(9), 159-173.

Adeyemi, S. B., & Oboh, C. S. (2011). Perceived relationship between corporate capital structure and firm value in Nigeria. International Journal of Business and Social Science, 2(19), 131-143.

Agbiogwu, A., Ihendinihu, J., & Okafor, M. (2016). Impact of environmental and social costs on performance of Nigerian manufacturing companies. International Journal of Economics and Finance, 8(9), 173-180.Available at: https://doi.org/10.5539/ijef.v8n9p173.

Aggarwal, D., & Padhan, P. C. (2017). Impact of capital structure on firm value: Evidence from Indian hospitality industry. Theoretical Economics Letters, 7(4), 982-1000.Available at: https://doi.org/10.4236/tel.2017.74067.

Aghdam, S. A. (2015). Determination of voluntary environment disclosure. The case of Iran. International Journal of Basic Science and Applied Research, 4(6), 343-349.

Ahmed, S. F., & Ibrahim, M. (2015). Firm attributes and earnings quality of listed oil and gas companies in Nigeria. Research Journal of Finance and Accounting, 5(17), 23-31.

Aifuwa, H. O., & Embele, K. (2019). Board characteristics and financial reporting quality. Journal of Accounting and Financial Management, 5(1), 30-49.

Ajide, F. M., & Aderemi, A. A. (2014). The effects of corporate social responsibility activity disclosure on corporate profitability: Empirical evidence from Nigerian commercial banks. IOSR Journal of Economics and Finance (IOSRJEF), 2(6), 17-25.Available at: https://doi.org/10.9790/5933-0261725.

Al-Matari, E. M., Al-Swidi, A. K., & Fadzil, F. H. B. (2014). The measurements of firm performance’s dimensions. Asian Journal of Finance & Accounting, 6(1), 24-49.Available at: https://doi.org/10.5296/ajfa.v6i1.4761.

Alghusin, N. A. S. (2015). The impact of financial leverage, growth, and size on profitability of Jordanian industrial listed companies. Research Journal of Finance and Accounting, 6(16), 86-93.

Ali, M. A., & Attan, R. H. (2013). The relationship between corporate governance and corporate social responsibility disclosure: A case of high Malaysian sustainability companies and global sustainability companies. South East Asia Journal of Contemporary Business, Economics and Law, 1(3), 39-48.

Anggraini, F. R. R. (2006). Disclosure of social information and affecting factors disclosure of social information in annual financial statements: Empirical studies of companies listed in the Jakarta stock exchange. Paper presented at the National Accounting Symposium 9, 23rd -26th August.

Anis, M., Chizema, A., Lui, X., & Fakhreldin, H. (2017). The impact of board characteristics on firms financial performance – evidence from the Egyptian listed companies. Global Journal of Human-Social Science: H-Interdisciplinary, 17(5), 57-75.

Ardalan, K. (2018). Capital structure theory: Reconsidered. Research in International Business and Finance, 39(PB), 696–710. Available at: https://doi.org/10.1016/j.ribaf.2015.11.010.

Ashafoke, T. O., & Ilaboya, J. (2017). Board characteristics and environmental disclosure in Nigeria banking sector. ICAN Journal of Accounting and Finance, 6(1), 87-102.

Asuquo, A. I., Dada, E., & Onyeogaziri, U. (2018). The effect of sustainability reporting on corporate performance of selected quoted brewery firms in Nigeria. International Journal of Business & Law Research, 6(3), 1-10.

Bae, K. H., El Ghoul, S., Guedhami, O., Kwok, C. Y. C., & Zheng, Y. (2018). Does corporate social responsibility reduce the costs of high leverage? Evidence from capital structure and product markets interactions. Journal of Banking and Finance. 100(C), 135-150. Available at: https://doi.org/10.1016/j.jbankfin.2018.11.007.

Belasri, S., Gomes, M., & Pijourlet, G. (2020). Corporate social responsibility and bank efficiency. Journal of Multinational Financial Management., 54(March), 100612. Available at: https://doi.org/10.1016/j.mulfin.2020.100612.

Bessong, P. K., & Tapang, A. T. (2012). Social responsibility cost and its influence on the profitability of Nigerian banks. International Journal of Financial Research, 3(4), 33-45.Available at: https://doi.org/10.5430/ijfr.v3n4p33.

Bhattacharyya, A., & Rahman, M. L. (2019). Mandatory CSR expenditure and firm performance. Journal of Contemporary Accounting & Economics, 15(3), 100163.Available at: https://doi.org/10.1016/j.jcae.2019.100163.

Birgili, E., & Düzer, M. (2010). The relationship between the rates and firm value used in financial analysis: An application in ISE. Accounting and Finance Magazine, 46(April), 74-83.

Boerkamp, E. (2016). Ownership concentration, ownership identity and firm performance: An empirical analysis of Dutch listed firms. Paper presented at the 7th IBA Bachelor Thesis Conference, Enschede, The Netherlands, July 1st, 2016.

Borlea, S. N., Achim, M. V., & Mare, C. (2017). Board characteristics and firm performances in emerging economies. Lessons from Romania. Economic Research, 30(1), 55-75.Available at: https://doi.org/10.1080/1331677x.2017.1291359.

Choi, Y. K., Han, S. H., & Kwon, Y. (2019). CSR activities and internal capital markets: Evidence from Korean business groups. Pacific-Basin Finance Journal, 55, 283-298.Available at: https://doi.org/10.1016/j.pacfin.2019.04.008.

Chrysostom, V. L., Freire, F. S., & Parente, P. H. N. (2013). Ownership concentration favors corporate social responsibility of Brazilian firm. Paper presented at the Congress of the National Association of Graduate Programs in Accounting Sciences - ANPCONT, Fortaleza, CE, Brazil, 7.

Ciftci, I., Tatoglu, E., Wood, G., Demirbag, M., & Zaim, S. (2019). Corporate governance and firm performance in emerging markets: Evidence from Turkey. International Business Review, 28(1), 90-103.Available at: https://doi.org/10.1016/j.ibusrev.2018.08.004.

Dabor, E. L., & Dabor, A. O. (2015). Social corporate responsibility disclosure of selected quoted companies in Nigeria. Ilorin Journal of Marketing, 2(1), 122-132.

Dakhlallh, M. M., Rashid, N. M. N. N. M., Abdullah, W. A. W., & Dakhlallh, A. M. (2019). The effect of ownership structure on firm performance among Jordanian public shareholders companies: Board independence as a moderating variable. International Journal of Academic Research in Progressive Education and Development, 8(3), 13-31.

Dam, L., & Scholtens, B. (2013). Ownership concentration and CSR policy of European multinational enterprises. Journal of Business Ethics, 118(1), 117-126.Available at: https://doi.org/10.1007/s10551-012-1574-1.

Dibia, N. O., & Onwuchekwa, J. C. (2015). Determinants of environmental disclosures in Nigeria: A case study of oil and gas companies. International Journal of Finance and Accounting, 4(3), 145-152.

Duke, J., & Kankpang, K. (2013). Implications of corporate social responsibility for the performance of Nigerian firms. Advances in Management and Applied Economics, 3(5), 73-87.

Enahoro, J. A., Akinyomi, O. J., & Olutoye, A. E. (2013). Corporate social responsibility and financial performance: Evidence from Nigerian manufacturing sector. Asian Journal of Management Research, 4(1), 153-162.

Esa, E., & Zahari, A. R. (2016). Corporate social responsibility: Ownership structures, board characteristics & the mediating role of board compensation. Procedia Economics and Finance, 35, 35-43.Available at: https://doi.org/10.1016/S2212-5671(16)00007-1.

Ghabayen, M. A., Mohamad, N. R., & Ahmad, N. (2016). Board characteristics and corporate social responsibility disclosure in the Jordanian banks. Corporate Board: Role, Duties & Composition, 12(1), 84-100.Available at: https://doi.org/10.22495/cbv12i1c1art2.

Ghosh, S., & Ansari, J. (2018). Board characteristics and financial performance: Evidence from Indian cooperative banks. Journal of Co-operative Organization and Management, 6(2), 86-93.Available at: https://doi.org/10.1016/j.jcom.2018.06.005.

Gupta, P. P., Kennedy, D. B., & Weaver, S. C. (2009). Corporate governance and firm value: Evidence from Canadian capital markets. Corporate Ownership & Control, 6(3), 293-307.Available at: https://doi.org/10.22495/cocv6i3c2p4.

Hassan, S. U., & Ahmad, N. (2013). Firm characteristics and financial reporting quality of listed manufacturing firms in Nigeria. International Journal of Accounting, Banking and Management, 1(6), 47-63.

Horobet, A., Belascu, L., Curea, Ș. C., & Pentescu, A. (2019). Ownership concentration and performance recovery patterns in the European Union. Sustainability, 11(4), 1-31.Available at: https://doi.org/10.3390/su11040953.

Huang, X. B., & Watson, L. (2015). Corporate social responsibility research in accounting. Journal of Accounting Literature, 34(1), 1-16.Available at: https://doi.org/10.1016/j.acclit.2015.03.001.

Ilaboya, O. J., & Omoye, A. S. (2013). Corporate social responsibility and firm performance. Journal of Asian Development Studies, 2(1), 6-19.

Iwata, H., & Okada, K. (2011). How does environmental performance affect financial performance? Evidence from Japanese manufacturing firms. Ecological Economics, 70(9), 1691-1700.Available at: https://doi.org/10.1016/j.ecolecon.2011.05.010.

Jeroh, E., & Okoro, G. (2016). Effect of environmental and dismantling costs on firm performance among selected oil and gas companies in Nigeria. Sahel Analyst: Journal of Management Sciences, 14(5), 14-26.

Joshi, G. S., & Hyderabad, R. L. (2019). The influence of board characteristics on CSR disclosure: Evidence from Indian companies. International Journal of Management, Technology and Engineering, 9(1), 1706-1720.

Kabajeh, M. A. M., Nu’aimat, S. M. A., & Dahmash, F. N. (2012). The relationship between ROA, ROE and ROI ratios with Jordanian insurance public companies market share prices. International Journal of Humanities & Social Science, 2(11), 115-120.

Kajola, S. O., Onaolapo, A. A., & Adelowotan, M. O. (2017). The effect of corporate board size on financial performance of Nigerian listed firms. Nigerian Journal of Management Sciences, 6(1), 204-213.

Kao, E. H., Yeh, C.-C., Wang, L.-H., & Fung, H.-G. (2018). The relationship between CSR and performance: Evidence in China. Pacific-Basin Finance Journal, 51, 155-170.Available at: https://doi.org/10.1016/j.pacfin.2018.04.006.

Karakus, R., & Bozkurt, I. (2017). The effect of financial ratios and macroeconomic factors on firm value: An empirical analysis in Borsa Istanbul. Paper presented at the RSEP International Conferences on Social Issues and Economic Studies 4th Multidisciplinary Conference, Prague, Czechia, 29-30 June.

Lin, L., Hung, P.-H., Chou, D.-W., & Lai, C. W. (2019). Financial performance and corporate social responsibility: Empirical evidence from Taiwan. Asia Pacific Management Review, 24(1), 61-71.Available at: https://doi.org/10.1016/j.apmrv.2018.07.001.

Lindblom, C. (1994). The implications of organizational legitimacy for corporate social performance and disclosure. Paper presented at the Critical Perspectives in Accounting Conference, New York.

Madden, L., McMillan, A., & Harris, O. (2020). Drivers of selectivity in family firms: Understanding the impact of age and ownership on CSR. Journal of Family Business Strategy, 100335 (February). Available at: https://doi.org/10.1016/j.jfbs.2019.100335.

Madhani, P. M. (2016). Ownership concentration, corporate governance and disclosure practices: A study of firms listed in Bombay stock exchange. The IUP Journal of Corporate Governance, 15(4), 7-36.

Makori, D. M., & Jagongo, A. (2013). Environmental accounting and firm profitability: An empirical analysis of selected firms listed in bombay stock exchange, India. International Journal of Humanities and Social Science, 3(18), 248-256.

Manawaduge, A. S., Zoysa, A. D., & Chandrakumara, P. M. K. A. (2010). Capital structure and its implications: Empirical evidence from an emerging market in South Asia. Paper presented at the Proceeding of GSMI Third Annual International Business Conference.

Mathuva, D. M., & Kiweu, J. M. (2016). Cooperative social and environmental disclosure and financial performance of savings and credit cooperatives in Kenya. Advances in Accounting, 35, 197-206.Available at: https://doi.org/10.1016/j.adiac.2016.09.002.

Moeljadi, S. (2014). Factors affecting firm value: Theoretical study on public manufacturing firms in Indonesia. South East Asia Journal of Contemporary Business, Economics and Law, 5(2), 6-15.

Muritala, T. A. (2012). An empirical analysis of capital structure on firms’ performance in Nigeria. International Journal of Advances in Management and Economics, 1(5), 116-124.

Naseem, M. A., Rehman, R. U., Ikram, A., & Malik, F. (2017). Impact of board characteristics on corporate social responsibility disclosure. Journal of Applied Business Research, 33(4), 801-810.

Nenu, E. A., Vintila, G., & Gherghina, Ş. (2018). The impact of capital structure on risk and firm performance: Empirical evidence for the Bucharest stock exchange listed companies. International Journal of Financial Studies, 6(2), 1-29.Available at: https://doi.org/10.3390/ijfs6020041.

Ng, S. H., Teh, B. H., Ong, T. S., & Soh, W. N. (2016). The relationship between board characteristics and firm financial performance in Malaysia. Corporate Ownership & Control, 14(1), 259-268.Available at: http://dx.doi.org/10.22495/cocv14i1c1p9 .

Nguyen, H. H., Ho, C. M., & Vo, D. H. (2019). An empirical test of capital structure theories for the Vietnamese listed firms. Journal of Risk and Financial Management, 12(3), 1-11.Available at: https://doi.org/10.3390/jrfm12030148.

Ngwakwe, C. C. (2008). Environmental responsibility and firm performance: Evidence from Nigeria. International Journal of Social, Management, Economics and Business Engineering, 2(10), 187-194.

Oh, S., & Kim, W. S. (2016). Effect of ownership change and growth on firm value at the issuance of bonds with detachable warrants. Journal of Business Economics and Management, 17(6), 901-915.Available at: https://doi.org/10.3846/16111699.2015.1072109.

Onder, Z. (2003). Ownership concentration and firm performance: Evidence from Turkish firms. METU Studies in Development, 30(2), 181-203.

Oshoke, A. S., & Sumaina, J. (2015). Performance evaluation through ratio analysis. Journal of Accounting and Financial Management, 1(8), 1-10.

Pathirawasam, C., & Wickremasinghe, G. (2012). Ownership concentration and financial performance: The case of Sri Lankan listed companies. Corporate Ownership and Control, 9(4), 170-177.Available at: https://doi.org/10.22495/cocv9i4c1art3.

Purusottama, A. (2020). Rural entrepreneurship capital and firm performance: A youth perspective. Journal of Economics and Business, 23(1), 1-20.

Salam, Z. A., & Shourkashti, R. (2019). Capital structure and firm performance in emerging market: An empirical analysis of Malaysian companies. International Journal of Academic Research in Accounting, Finance and Management Sciences, 9(3), 70-82.Available at: http://dx.doi.org/10.6007/IJARAFMS/v9-i3/6334

Salaudeen, H. A., & Abiola, I. B. (2018). Board quality and corporate social responsibility disclosure of listed manufacturing firms in Nigeria. International Journal of Accounting and Finance, 7(1), 20-33.