RELATIONSHIP BETWEEN CAPITAL REQUIREMENT, OWNERSHIP STRUCTURE, AND FINANCIAL PERFORMANCE IN SAUDI ARABIAN LISTED COMPANIES

Assistant Professor of Finance, Department of Finance, Faculty of Economics and Administration, King Abdulaziz University, Saudi Arabia.

ABSTRACT

Saudi Arabia’s capital market is highly concentrated due its regulators’ visible role. This study analyses the regulators’ role on the return on assets (ROA) and return on equity (ROE) to examine their impact on the capital market’s growth. Variables including institutional ownership, government ownership, foreign ownership and capital requirements were examined. Data was collected through the TASI Stock Market. The study included a panel dataset to observe 171 private and public listed companies by using the cross-sectional data from 2010 to 2014. Findings illustrated that company ownership concentration had a positive relationship in improving company’s performances, but foreign ownership had minimum significance. Similarly, ROA and ROE had a positive relationship with capital requirements. For various Saudi private and public listed companies, it is important to pay attention to capital market regulation as it plays a crucial role in improving company performance.

Keywords:The regulators’ role, Ownership concentration, Foreign ownership, Capital requirements, Return on asset (ROA), Return on equity (ROE).

JEL Classification:G28; G32; G38.

ARTICLE HISTORY: Received:13 June 2019 Revised: 25 July 2019 Accepted:3 September 2019 Published:30 September 2019.

Contribution/ Originality:This study contributes to the existing literature by analyzing the regulators’ role on the capital market’s growth and development.

1. INTRODUCTION

Various researchers have advocated growth and economic development as the most magnetic stimulators across the globe (Tsitouras et al., 2017![]() ). This interest has perpetuated given the shift towards transition from conventional production and ownership concepts to maximize outputs and distribution of wealth for economic stability (Creel et al., 2015

). This interest has perpetuated given the shift towards transition from conventional production and ownership concepts to maximize outputs and distribution of wealth for economic stability (Creel et al., 2015![]() ). The transition has occurred as a response to globalization where economies are reformed. This transition is most prominent among the developing countries that are accelerating their growth and expanding their market (Alshammary, 2014

). The transition has occurred as a response to globalization where economies are reformed. This transition is most prominent among the developing countries that are accelerating their growth and expanding their market (Alshammary, 2014![]() ).

).

It is essential to investigate the components of capital structure decisions or company financing to comprehend how they finance their operations. A wide range of policy issues are involved in company financing decisions (Migliardo and Forgione, 2018![]() ). Companies are affected by the interest rate, security price determination, regulation, and capital market development (Al-Thuneibat, 2018

). Companies are affected by the interest rate, security price determination, regulation, and capital market development (Al-Thuneibat, 2018![]() ). It is vital to understand that countries have different institutional arrangements, which include the current market for corporate control, banks and securities role, and tax and bankruptcy codes.

). It is vital to understand that countries have different institutional arrangements, which include the current market for corporate control, banks and securities role, and tax and bankruptcy codes.

Ownership structure was considered to influence company performance for several years as a mechanism to increase a company’s efficiency in corporate governance. The stock markets are widely perceived as important for the execution of modern capitalist economies (Niehaus, 2018![]() ). Ownership concentration offer investors the motivation and ability to monitor and control the management as a direct control indicator of the company. The relationship between company financial performance and ownership concentration is still in debate due to its mixed results (Khan et al., 2018

). Ownership concentration offer investors the motivation and ability to monitor and control the management as a direct control indicator of the company. The relationship between company financial performance and ownership concentration is still in debate due to its mixed results (Khan et al., 2018![]() ). It has been suggested that the management would be monitoring the concentrated ownership as per the agency theory, which makes ownership an essential aspect in corporate governance. This enhances company performance (Oino, 2018

). It has been suggested that the management would be monitoring the concentrated ownership as per the agency theory, which makes ownership an essential aspect in corporate governance. This enhances company performance (Oino, 2018![]() ). It has been observed that there is a significant relationship between financial performance and ownership concentration. However, previous studies have disclosed a lack of a significant relationship between financial performance and ownership concentration.

). It has been observed that there is a significant relationship between financial performance and ownership concentration. However, previous studies have disclosed a lack of a significant relationship between financial performance and ownership concentration.

The relationship between financial performance and ownership concentration is as yet unconfirmed in the corporate finance literature. Ownership structure is determined as an endogenous outcome of decisions for a corporation that portray the impact of shareholders and of trading on the share market. A huge gap in knowledge still exists on the relationship between financial structure and ownership structure in the literature. While analyzing the benefit of the listing of private companies, Brau and Fawcett (2006![]() ) found that this practice improves the business valuation in the market. Sheen (2016

) found that this practice improves the business valuation in the market. Sheen (2016![]() ) while analyzing the investment in the chemical sectors found that through listing, private companies could improve their prospects for future acquisition.

) while analyzing the investment in the chemical sectors found that through listing, private companies could improve their prospects for future acquisition.

Considering the emerging economies of the developing countries, the same practices were also observed in Saudi Arabia. This was initially found in its last three Five-Year Saudi National Development Plans (2000– 2014), where significant efforts were being implemented for promoting sustainable growth through reforms in the legal, economical as well as financial sector. Ramady (2010![]() ) has pinpointed that these reforms were made for the diversification of the resources and stabilizing the economic growth in the country to make it parallel with international financial practices. Multiple types of research have been conducted to assess the privatization magnitude, where the emergence of several private programs has been reported. Through the listing of the companies, the capital can be mobilized both inside and outside the company improving the borrowing capacity. It also enhances the flow of the foreign indirect investment which enhances the international investment funds and rapidly increases the number of foreign individuals and institutions trading accounts (Viet, 2013

) has pinpointed that these reforms were made for the diversification of the resources and stabilizing the economic growth in the country to make it parallel with international financial practices. Multiple types of research have been conducted to assess the privatization magnitude, where the emergence of several private programs has been reported. Through the listing of the companies, the capital can be mobilized both inside and outside the company improving the borrowing capacity. It also enhances the flow of the foreign indirect investment which enhances the international investment funds and rapidly increases the number of foreign individuals and institutions trading accounts (Viet, 2013![]() ). This serves as a significant advantage for the country’s economy and accelerates the achievement of the Saudi Vision 2030 goals.

). This serves as a significant advantage for the country’s economy and accelerates the achievement of the Saudi Vision 2030 goals.

The relationship between financial performance and capital structure receives significant attention in the finance literature. The potential problems in capital structure and performance could be understood by studying the effects of financial performance or capital structure. This study will be significant in supplementing empirical studies in the field of corporate governance which has been substantially involved in ownership structure and operations. The study aimed to analyze the regulators’ role on the capital market’s growth and development. The influence of institutional ownership, government ownership, foreign ownership and capital requirements is important and serves as the fundamental part of the discussion. Since previous studies failed to provide a detailed analysis of the idea, the present study’s contributions are even more important. There is no study on the capital developing market through the listing of private and public companies in current literature. By studying this aspect of Saudi Arabia, the economy can be strengthened via the listings. It contributes by filling in the knowledge gap in the literature on the Saudi stock market and the economic growth powered by the listing of public and private companies, which help make radical changes in the capital market.

2. METHODOLOGY

2.1. Selection of Variables and Development of Hypothesis

2.1.1. Dependent Variables

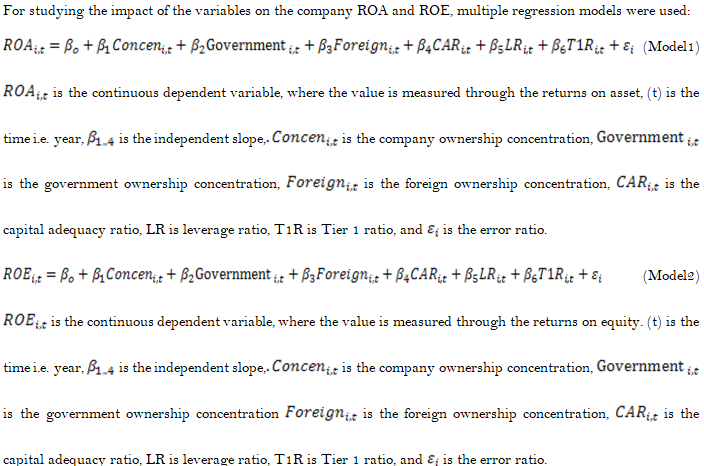

The regulators’ impact was examined by using two significant variables: Return on Asset and Return on Equity (Mwangi et al., 2014![]() ; Yahaya and Lawal, 2018

; Yahaya and Lawal, 2018![]() ).

).

- Return on assets (ROA) is the ratio that shows the company’s efficiency in using its assets. Companies generally enjoy a successful growth by effectively using their fixed assets along with their working capital. Razafindrambinina and Anggreni (2017

) claimed that return on assets (ROA) is the ratio that explains the assets evaluated by sales. For the successful growth of the companies, this ratio must be large. This further concluded that the greater the return on asset (ROA), the higher the profits that are generated by the companies and the investors will thus, purchase more shares. Besides, Wang and Shailer (2018) determined that the performance of the company was significantly affected by the ROA. ROA increases the leverage of the company by enhancing its profit ratios and shares value.

) claimed that return on assets (ROA) is the ratio that explains the assets evaluated by sales. For the successful growth of the companies, this ratio must be large. This further concluded that the greater the return on asset (ROA), the higher the profits that are generated by the companies and the investors will thus, purchase more shares. Besides, Wang and Shailer (2018) determined that the performance of the company was significantly affected by the ROA. ROA increases the leverage of the company by enhancing its profit ratios and shares value. - Return on equity (ROE) is used to examine the equity components of the overall investments of the company. It is used to develop the relationship between remaining earnings for equity investors and is determined by dividing the net income with the equity of shareholder (Damodaran, 2007). Low outcomes of ROE indicate the company’s inefficient management performance. According to Ang et al. (2018) the greater the profits generated by the company, the higher the returns on equity. This further boosts the company stock prices which attracts the attention of investors. Maudos (2017) indicated that the profitability in terms of the return on equity was significant for the companies to operate effectively.

2.1.2. Independent Variables

To calculate the impact of capital requirements’ role on private and public companies, the study used certain independent variables including: the concentration of ownership, government ownership, foreign ownership, and capital requirements (Al-Matari et al., 2017![]() ; Lai, 2017

; Lai, 2017![]() ).

).

- Institutional ownership is defined as a process that involves fewer individuals or organizations in controlling increasing shares. Ozili and Uadiale (2017) determined the relationship between ownership concentration and the return on asset in some companies. Findings indicated a significant and positive association between ownership concentration and the efficiency of the company. A higher return on assets has been identified as a valuable output of ownership concentration. Lepore et al. (2017) evaluated the impact of the ownership concentration on the performance of private companies. The examination of the idea was conducted via the return on assets (ROA). The results indicated that ownership concentration had created a positive influence on a company’s performance. On the other hand, Abdallah and Ismail (2017) conducted a study identifying the influence of the ownership concentration on the profitability of the company in the stock market. The findings indicated that scattered ownership concentration had an impact on the accountancy of the company specifically on return on equity. As the investor’s ownership block increases, the entire performance of the company decreases (Paniagua et al., 2018). Institutional ownership is the extent of company ownership by institutional investors, which includes insurance companies, institutions, banks, investment companies, or other companies. Institutional ownership is the extent or ownership of shares by the domestic institutions (Cui et al., 2019). It positively influences the financial performance of the companies. In addition, the ownership structure significantly influences the earning management (Vu et al., 2018). The study tested the effect of institutional ownership structure on the financial performance of Saudi listed companies. It was expected that:

H1= Institutional ownership would be positively correlated with the company’s ROA and ROE.

- Government ownership is generally associated with lower corporate governance quality in companies. Haider et al. (2018); Aluchna and Kaminski (2017) indicated a negative relationship between government ownership and performance of the company because the government is often found to be uninterested in leveraging the profits of the company. In addition, the existence of government bureaucracy gives rise to greater agency issues. Karanja and Wagana (2017) found a positive relationship between the government ownership and company performance– where the performance of a company was not significantly influenced by government ownership. It was considered that there are different objectives for government-owned companies in creating social and political benefits instead of maximizing profits. It has been observed that there are still differences associated with the government ownership structure influencing the financial performance of the companies. The present study believed that government ownership would provide financial assets to the companies thus, leveraging the performance of the company. Therefore, we assumed that:

H2= Government ownership would negatively correlate with the company’s ROA and ROE.

- Foreign ownership is the control of a business or natural resource in a country by individuals who are not citizens of that country. Chen et al. (2017) in a study concluded that the performance of the multinational enterprises was better than the local companies. Hence, foreign ownership has a positive and significant relationship with companies’ performance. Similarly, McGuinness et al. (2017) examined the performance of US companies that were taken over by foreigners. They stated that there was a positive impact of foreign ownership on corporate performance as foreigners have appropriate corporate governance in the companies’ internal system (Wang and Shailer, 2018). There is a significant and positive relationship between corporate ownership and foreign ownership. In addition, foreign investors can provide easy access to massive resources and management systems. Some companies have superior corporate governance mechanisms as compared to local companies due to foreign ownership, which suggested that there is higher financial performance for foreign owned companies (Zraiq and Fadzil, 2018). Foreign ownership can mean effective monitoring of the company management (Anum, 2010). The provision of organizational knowledge and resources contribute to managerial and organizational capabilities with respect to financial capital (Bykova and Lopez-Iturriaga, 2018). The present study hypothesized a positive and significant relationship between foreign ownership and company performance. Hence, we assumed that:

H3= Foreign ownership would positively correlate with the company’s ROA and ROE.

- Capital requirements (also known as regulatory capital or capital adequacy) are the regulations on the amount of capital in a bank or other financial institutions. Detthamrong et al. (2017) indicated that the company managers tend to establish the capital structure to increase the profits. However, this may lead to conflicts between the managers and the shareholders who pursue the enhance value of the companies thus, resulting in poorer performance. Besides, Tulung and Ramdani (2018) argued that the optimal capital adequacy achieves the threshold level of indebtedness. To facilitate potential losses and protect the debt holders of the financial institution, capital adequacy is the capital level required for maintaining balance with the operational credit, market, and operational risks (Gueyié et al., 2019). The capital risk asset ratio is used by bank supervisors for measuring the capital adequacy. Capital adequacy is one of the management options for dealing with the composition of the balance sheet, ability to access sources of capital, the quality of capital, the volume of capability to acquire loans and assets, and to deal with marginal capital needs (Tulung and Ramdani, 2018). So, we expected that:

H4= Capital requirements (capital adequacy ratio, leverage ratio, Tier 1 ratio) would positively correlate with the company’s ROA and ROE.

2.2. Sample Size and Data Resources

The data in the study was extracted from the TASI stock market. The panel data set was used for observing 171 private and public listed companies along with the use of the cross-sectional data of the companies’ groups from 2010 to 2014. The rationale behind the selection of the panel data was based on it being termed the best and most used types of data Levin et al. (2002![]() ). Table 1 defines the variables used in our model.

). Table 1 defines the variables used in our model.

Table-1. Description of variables.

| Category | Acronyms | Description/Calculation |

| Dependent variables | ||

| Financial performance | ||

| Return on assets | ROA | It is a profitability ratio that measures how well a company is generating profits from its total assets. It is also used to measure the ability of managerial authorities to effectively use assets for generating profitable outputs (Al Nimer et al., 2015 |

| Return on equity | ROE | Return on equity (ROE) is a measure of financial performance calculated by dividing net income by shareholders’ equity It helps in measuring the effectiveness of capital in generating maximum returns (Kijewska, 2016 |

| Independent variables | ||

| Ownership structure | ||

| Institutional ownership | CO | Concentration of company ownership is a process whereby progressively fewer individuals or organizations control increasing shares (Krysthyn27, 2014 |

| Government ownership | GO | Government ownership is generally associated with lower corporate governance quality in companies (Borisova et al., 2012 |

| Foreign ownership | FO | Foreign ownership or control of a business or natural resource in a country by individuals who are not citizens of that country. |

| Capital requirements | ||

| Capital adequacy ratio | CAR | Capital adequacy ratio is also known as capital to risk assets ratio is the ratio of a bank’s capital to its risk (Abdelbary, 2019 |

| Leverage ratio | LR | A leverage ratio is any one of several financial measurements that look at how much capital comes in the form of debt (loans) or assesses the ability of a company to meet its financial obligations (Kenton and Hayes, 2019 |

| Tier 1 ratio | T1R | The tier 1 capital ratio is the ratio of a company’s core tier 1 capital that is its equity capital and disclosed reserves to its total risk-weighted assets (Steven, 2019 |

2.3. Data Analysis

Econometric modeling using EViews was used in the study to analyze the factors that promote the listing of the private and public companies in Saudi Arabia. Data was further analyzed through descriptive statistical analysis, incorporating company ownership concentration, government ownership concentration, foreign ownership concentration, CAR, leverage ratio, tier 1 ratio, return on assets, and return on equity. The testing of the hypothesis was done through the Panel Unit Root Analysis using the Levin, Lin and Chu (LLC) method (Levin et al. (2002![]() )).

)).

3. RESULTS

3.1. Descriptive Statistical Analysis

The method transforms data by rearranging, manipulating and ordering it to make it interpretable for the reader. The methodology is helpful as it restricts the generalization of ideas to a specific group of individuals only. Descriptive statistical analysis is important as it provides significant information regarding uncertainty and variability of data. Table 2 provides the descriptive statistics based on the mean, standard deviation, maximum range, and minimum range. The findings showed that company ownership concentration had the mean value with standard deviation of 65.88 ± 22.86 percent. Similarly, the mean and standard deviation of government ownership concentration was 46.93 ± 12.56 with a minimum value of 16.97 percent and a maximum value of 83.51 percent. Foreign ownership concentration had the mean value of 10.81 ± 6.6.2 percent with a minimum and maximum range of 2.59-25.87 percent.

The table reports descriptive statistics for 80 companies. The variables used in this table include company ownership concentration, government ownership concentration, foreign ownership concentration, capital requirements, return on assets, and return on equity. Descriptive statistics is reported through different parameters including mean, standard deviation, maximum range, minimum range, and observations. Company ownership concentration refers to the amount of stock owned by a company. Government ownership concentration refers to the amount of stock owned by a government. Foreign ownership concentration refers to the amount of stock owned by foreign owners. Capital requirements refer to the amount of capital a bank or other financial institution must hold as required by its financial regulator. Return on assets refers to the percentage of profit a company earns with respect to its overall resources. Return on equity refers to the financial performance calculated by dividing net income by shareholder’s equity.

Table-2. Descriptive statistics.

Variable |

Concentration |

Government |

Foreign |

Capital |

ROA |

ROE |

Unit |

(%) |

(%) |

(%) |

Index |

(%) |

(%) |

Mean |

65.88 |

46.93 |

10.81 |

3.65 |

1.31 |

11.89 |

Standard deviation |

22.86 |

12.56 |

6.62 |

2.07 |

0.87 |

6.78 |

Maximum range |

100.00 |

83.51 |

25.87 |

9.40 |

4.04 |

29.00 |

Minimum range |

36.69 |

16.97 |

2.59 |

1.40 |

-2.07 |

-12.11 |

Observations |

80 |

80 |

80 |

80 |

80 |

80 |

Concentration: Company ownership concentration; government; government ownership concentration; foreign: foreign ownership concentration; capital: capital requirements; ROA: return on assets; ROE: return on equity.

3.2. Test of Hypotheses (Multivariate Analyses) and Research Model

In addition, panel unit root testing was used to analyze the given variables. The methodology however was developed through unit root testing. The panel root analysis of LLC is a three-step procedure that demands normalization and preliminary regression in the cross-sectional heterogeneity. Barbieri (2009![]() ) highlighted that the panel data sets provide high values of time series and number of variables while indicating similar magnitudes.

) highlighted that the panel data sets provide high values of time series and number of variables while indicating similar magnitudes.

The method was significant in testing the null hypothesis since the focus of the study was to provide the relationship between foreign ownership structure, company ownership, government ownership, capital requirements, ROA and ROE in improving the financial performance of firms at differences. The panel root analysis was applied to identify the impact of the given variable at differences in the first variable. The panel unit root test followed by Levin et al. (2002![]() ) provides a significant advantage in rejecting the null hypothesis when it is not correct. Table 3 has presented panel unit root analysis based on the Levin et al. (2002

) provides a significant advantage in rejecting the null hypothesis when it is not correct. Table 3 has presented panel unit root analysis based on the Levin et al. (2002![]() ) method.

) method.

The findings showed that all the variables including company ownership, government ownership concentration, capital requirements, foreign ownership concentration, ROA and ROE were statistically significant at 1st difference but statistically insignificant at level in constant. Similarly, the results showed that all the variables were statistically significant at 1st difference in constant and trend but insignificant at level in constant and trend. The panel unit root reports whether a time series variable is stationary and possesses a unit root. At level shows that the result was stationary when the unit root was applied. Difference at 1st level shows that the unit root was measured along with the constant without the trend and constant means.

Table-3. Panel unit root analysis using Levin et al. (2002![]() ) method.

) method.

| Variables | Constant |

Constant and trend |

||||

Stats. |

Prob. |

Stats. |

Prob. |

|||

| Company ownership concentration | At level | -0.28 |

0.39 |

0.42 |

0.66 |

|

| 1st difference | -2.73 |

0.00 |

-1.94 |

0.03 |

||

| Government ownership concentration | At level | -0.71 |

0.24 |

-0.50 |

0.31 |

|

| 1st difference | -16.58 |

0.00 |

-3.77 |

0.00 |

||

| Capital structure | At level | -0.56 |

0.29 |

-0.17 |

0.43 |

|

| 1st difference | -6.39 |

0.00 |

-3.62 |

0.00 |

||

| Foreign ownership concentration | At level | -0.06 |

0.48 |

-1.01 |

0.16 |

|

| 1st difference | -6.27 |

0.00 |

-8.00 |

0.00 |

||

| Return on assets | At level | -0.04 |

0.49 |

6.06 |

1.00 |

|

| 1st difference | -9.38 |

0.00 |

-7.79 |

0.00 |

||

| Return on equity | At level | -0.32 |

0.38 |

1.78 |

0.96 |

|

| 1st difference | -8.31 |

0.00 |

-10.56 |

0.00 |

||

Table 4 shows the Pedroni panel co-integration analysis based on seven statistics. The findings indicated that only four out of seven statistics were found significant at the 1% level. These statistics included the Panel PP-Statistic, Panel ADF-Statistic, Group PP-Statistic and Group ADF-Statistic.

Table-4. Pedroni (1999![]() ) panel cointegration.

) panel cointegration.

| Test summary | ROA |

ROE |

||

Statistics |

Prob. |

Statistics |

Prob. |

|

| Panel v-statistic | -1.514 |

0.935 |

-1.433 |

0.924 |

| Panel rho-statistic | 2.319 |

0.990 |

2.493 |

0.994 |

| Panel PP-statistic | -8.920 |

0.000 |

-5.427 |

0.000 |

| Panel ADF-statistic | -5.341 |

0.000 |

-3.552 |

0.000 |

| Group rho-statistic | 3.739 |

1.000 |

3.995 |

1.000 |

| Group PP-statistic | -8.948 |

0.000 |

-4.927 |

0.000 |

| Group ADF-statistic | -5.143 |

0.000 |

-2.714 |

0.003 |

Level of Significance: 1%.

This table reports the pedroni panel cointegration test results which include different asymptotic properties. There were seven panel cointegration statistics, and the first part was based on the within dimension approach, including the panel v statistic, the Panel rho Statistic, the Panel PP Statistic and the Panel ADF Statistic; the second part was based on the between-dimension approach, including the Group rho Statistic, the Group PP Statistic and the Group ADF Statistic.

Table 5 shows the Hausman test for correlated random effects. The table reports the Hausman test results for the correlated random effect, which was used to test for model misspecifications in the random effect model. The findings indicated that the cross-sectional data was statistically significant rejecting the null hypothesis of conducting a misspecification. Therefore, the study used the fixed-effect method for pooled OLS technique.

Table-5. Hausman test for correlated random-effect.

Test summary |

Chi-square statistic |

DF |

Prob. |

Cross-section random |

11.51 |

5 |

0.04 |

Table 6 shows the pooled OLS results which were used to test for model misspecifications in fixed-effect model for ROA. The findings showed that company ownership concentration was found to be negatively significant with the ROA (-0.010, p<0.10); but government ownership concentration was negatively significant in relation to the ROA (-0.061, p<0.10). In addition, capital requirement was found to be positively significant in relation to the ROA (0.092, p<0.10); but foreign ownership concentration was negatively insignificant in relation to the ROA (-0.027, p>0.10).

Table-6. Pooled OLS using fixed-effect method (Return on assets).

Variable |

Coefficient |

Std. error |

t-statistic |

Prob. |

Constant |

5.762 |

1.070 |

5.383 |

0.000 |

Company ownership concentration |

0.010 |

0.006 |

-1.757 |

0.084 |

Government ownership concentration |

0.061 |

0.009 |

-6.992 |

0.000 |

Capital structure |

0.092 |

0.038 |

-2.435 |

0.018 |

Foreign ownership concentration |

-0.027 |

0.053 |

-0.521 |

0.605 |

Dependent variable: Return on assets.

R-square = 0.709; Adjusted R-square = 0.602

F-statistics (Prob.) = 6.606 (0.000)

Table 7 shows the results for the pooled OLS using fixed-effect method for the ROE. The findings showed that company ownership concentration was found to be positively significant with the ROE (-0.021, p<0.10); but government ownership concentration was positively significant in relation to the ROE (0.050, p<0.10). In addition, capital requirements were found to be positively significant in relation to the ROE (0.080, p<0.10); but foreign ownership concentration was found to be negatively insignificant in relation to the ROE (0.035, p<0.10).

Table-7. Pooled OLS using fixed-effect method (Return on equity).

| Variable | Coefficient |

Std. error |

t-statistic |

Prob. |

| Constant | 7.526 |

0.181 |

4.823 |

0.000 |

| Company ownership concentration | 0.021 |

0.005 |

-1.475 |

0.064 |

| Government ownership concentration | 0.050 |

0.001 |

-3.287 |

0.000 |

| Capital structure | 0.080 |

0.045 |

-1.534 |

0.000 |

| Foreign ownership concentration | 0.035 |

0.054 |

-0.125 |

0.005 |

Dependent variable: Return on equity.

R-square = 0.715; Adjusted R-square = 0.520.

F-statistics (Prob.) = 5.466 (0.000).

The results showed that there was no direct causal relationship of the ROA with any of the variables as shown in Table 8. However, the ROE has significant unidirectional causal relationship with the concentration of ownership and government ownership. Table 8 reports granger causality, which was used to determine the causality between two variables in a time series.

Table-8. Granger causality (ROE).

| Null hypothesis | F-statistic |

Prob. |

Remarks |

| Concen does not Granger Cause Government | 0.338 |

0.714 |

No causality |

| Government does not Granger Cause Concen | 0.003 |

0.997 |

|

| Foreign does not Granger Cause Government | 4.950 |

0.010 |

Unidirectional |

| Government does not Granger Cause Foreign | 0.652 |

0.525 |

|

| Capital does not Granger Cause Government | 1.329 |

0.273 |

No causality |

| Government does not Granger Cause Capital | 0.701 |

0.500 |

|

| ROE does not Granger Cause Government | 0.367 |

0.695 |

No causality |

| Government does not Granger Cause ROE | 0.007 |

0.993 |

|

| Foreign does not Granger Cause Concen | 1.342 |

0.269 |

Unidirectional |

| Concen does not Granger Cause Foreign | 5.580 |

0.006 |

|

| Capital does not Granger Cause Concen | 1.216 |

0.304 |

No causality |

| Concen does not Granger Cause Capital | 1.194 |

0.310 |

|

| ROE does not Granger Cause Concen | 1.065 |

0.351 |

Unidirectional |

| Concen does not Granger Cause ROE | 8.345 |

0.001 |

|

| Capital does not Granger Cause Foreign | 0.769 |

0.468 |

Unidirectional |

| Foreign does not Granger Cause Capital | 3.671 |

0.032 |

|

| ROE does not Granger Cause Government | 5.947 |

0.004 |

Unidirectional |

| Government does not Granger Cause ROE | 1.468 |

0.239 |

|

| ROE does not Granger Cause Capital | 0.065 |

0.937 |

No causality |

| Capital does not Granger Cause ROE | 0.067 |

0.936 |

4. DISCUSSION

The regulators’ role on companies’ growth and development is key in advocating developments in the capital market. In Saudi Arabia, efforts are now being made to provide efficient support through regulators to foster the reforms in the financial sector. The findings in Table 1 illustrated that company ownership was highly beneficial in providing maximum benefits to the company, with mean and the standard deviation value of 65.88 ± 22.86 percent respectively. The results were supported by Balsmeier and Czarnitzki (2017![]() ) in their study according to which ownership concentration works as a significant variable in the development and growth of companies. Companies undergoing a greater downfall should develop strong ownership to overcome the problems.

) in their study according to which ownership concentration works as a significant variable in the development and growth of companies. Companies undergoing a greater downfall should develop strong ownership to overcome the problems.

The study further illustrated that the role of ownership varies in every company. The findings of the study showed that ownership concentration has a positive relationship with company performance. This is crucial in cases where companies must cope with a weak economy. Soliman et al. (2013![]() ) proposed similar findings, where a hump-shaped relationship between company performance and ownership concentration was found. The results further proposed that the impact of ownership concentration was positive at minimum levels of ownership concentration in improving and modifying company performance. The results proposed through the logistic regression have also supported these findings. For Darmadi (2012

) proposed similar findings, where a hump-shaped relationship between company performance and ownership concentration was found. The results further proposed that the impact of ownership concentration was positive at minimum levels of ownership concentration in improving and modifying company performance. The results proposed through the logistic regression have also supported these findings. For Darmadi (2012![]() ) ownership concentration was visibly high, in cases where share ownership of the highest shareholder reached above the average median value.

) ownership concentration was visibly high, in cases where share ownership of the highest shareholder reached above the average median value.

Similarly, government ownership came in second with a mean and standard deviation percentage of 46.93 ± 12.56. The minimum value provided for the given concentration was 16.97 and 83.51 was the maximum value. However, the findings contrasted with those proposed by Al-Matari et al. (2017![]() ) for whom, government ownership with its mean standard deviation came in first position. This further reflects an idea that in an average company, state ownership has shares with an average of 20% in every other company.

) for whom, government ownership with its mean standard deviation came in first position. This further reflects an idea that in an average company, state ownership has shares with an average of 20% in every other company.

The impact of foreign ownership concentration was found to be negative in relation to the ROE with the values of 0.035, p<0.10. Lai (2017![]() ) in his paper stated that government ownership had significant shares in almost 17 of 76 companies. This indicates that the results proposed in this paper are in line with the literature. Similarly, foreign ownership did not create a visible impact on the ROA, as proposed by Yahaya and Lawal (2018

) in his paper stated that government ownership had significant shares in almost 17 of 76 companies. This indicates that the results proposed in this paper are in line with the literature. Similarly, foreign ownership did not create a visible impact on the ROA, as proposed by Yahaya and Lawal (2018![]() ). This illustrated that the presence of shareholders had the power to monitor and regulate management behavior, which creates a direct impact on a company’s performance.

). This illustrated that the presence of shareholders had the power to monitor and regulate management behavior, which creates a direct impact on a company’s performance.

Other findings related to the return on asset (ROA) proposed that company ownership was negatively concerned with the ROA at a given value of -0.010, p<0.10 respectively. The given results contrasted with those illustrated by Soliman et al. (2013![]() ). The research involved binary logistic procedure to propose results, according to which the ROA was positively related to the ownership concentration, with an explanatory power of 0.227. However, the financial performance of any company which was represented by the ROE also serves as an important variable. The results proposed in our study stated a positive relationship between ownership concentration and the ROE with the given values of (-0.021, p<0.10). However, we accepted that company ownership concentration was positively correlated with a company’s ROA and hence accepted H1, H2 and H3. Yahaya and Lawal (2018

). The research involved binary logistic procedure to propose results, according to which the ROA was positively related to the ownership concentration, with an explanatory power of 0.227. However, the financial performance of any company which was represented by the ROE also serves as an important variable. The results proposed in our study stated a positive relationship between ownership concentration and the ROE with the given values of (-0.021, p<0.10). However, we accepted that company ownership concentration was positively correlated with a company’s ROA and hence accepted H1, H2 and H3. Yahaya and Lawal (2018![]() ) argued that ownership concentration had significantly no impact on the ROE.

) argued that ownership concentration had significantly no impact on the ROE.

Ofori-Sasu et al. (2017![]() ) supported the statement and argued that the largest shareholders in terms of investments have the potential to significantly elevate the profitability of the companies. The impact of the gross size of the shareholders was determined to be insignificant on the efficiency of the company. The association of the ownership structure with the return on equity was found insignificant. Aguenaou et al. (2014

) supported the statement and argued that the largest shareholders in terms of investments have the potential to significantly elevate the profitability of the companies. The impact of the gross size of the shareholders was determined to be insignificant on the efficiency of the company. The association of the ownership structure with the return on equity was found insignificant. Aguenaou et al. (2014![]() ) showed evidence that concentrated ownership was associated with the poorer financial performance of the companies. This is because when the ownership gets more concentrated, the dominating shareholders manipulate the minor shareholders leading to poorer performances. However, there are few other studies which indicated other factors that leverage the profitability as well as enhance the performance of the companies. The study accepted that government ownership concentration was positively correlated with a company’s ROE and ROA and hence accepted H2.

) showed evidence that concentrated ownership was associated with the poorer financial performance of the companies. This is because when the ownership gets more concentrated, the dominating shareholders manipulate the minor shareholders leading to poorer performances. However, there are few other studies which indicated other factors that leverage the profitability as well as enhance the performance of the companies. The study accepted that government ownership concentration was positively correlated with a company’s ROE and ROA and hence accepted H2.

Traditionally, it is accepted that MNEs and foreign owned companies in the developing as well as developed countries work better than the local companies. Guvenen et al. (2017![]() ) argued that the foreign owned companies in US were less profitable than the domestic companies. This is because the US companies possess a low level of R&D incentives and focus more on advertisement. Few researchers such as Liang (2017

) argued that the foreign owned companies in US were less profitable than the domestic companies. This is because the US companies possess a low level of R&D incentives and focus more on advertisement. Few researchers such as Liang (2017![]() ) and Ni et al. (2017

) and Ni et al. (2017![]() ) extended this concept and determined a negative impact of FDI to domestic companies. The log-linear production also identified an insignificant impact of foreign investment on the performance of the local companies as compared to foreign owned companies. Similarly, Li et al. (2013

) extended this concept and determined a negative impact of FDI to domestic companies. The log-linear production also identified an insignificant impact of foreign investment on the performance of the local companies as compared to foreign owned companies. Similarly, Li et al. (2013![]() ) following the statement showed evidence that the ROA of companies that were acquired by foreign ownership was higher (21.37%) than the ROA of the local company (14.50%). Likewise, Karolyi and Liao (2017

) following the statement showed evidence that the ROA of companies that were acquired by foreign ownership was higher (21.37%) than the ROA of the local company (14.50%). Likewise, Karolyi and Liao (2017![]() ) through t-tests found that the ROA of companies that were taken over by the foreign ownership was significantly greater (22.30%) in contrast to domestic companies which was found to be less significant (13.60%). In contrast, Tutu (2017

) through t-tests found that the ROA of companies that were taken over by the foreign ownership was significantly greater (22.30%) in contrast to domestic companies which was found to be less significant (13.60%). In contrast, Tutu (2017![]() ) argued that the significant differences between the foreign owned companies and the domestic companies in terms of the ROA were correspondent. The study accepted that foreign ownership concentration was positively correlated with a company’s ROE (accepts H3) but not with the ROA.

) argued that the significant differences between the foreign owned companies and the domestic companies in terms of the ROA were correspondent. The study accepted that foreign ownership concentration was positively correlated with a company’s ROE (accepts H3) but not with the ROA.

With the increasing demand for shareholder association with the listed companies, the researchers (Ducassy and Guyot, 2017![]() ; Muritala, 2018

; Muritala, 2018![]() ) focused more on the ownership structure and the company performance. In the developing countries, the need for stakeholders is much larger in order to monitor the performance of the corporations. It was argued by Balsmeier and Czarnitzki (2017

) focused more on the ownership structure and the company performance. In the developing countries, the need for stakeholders is much larger in order to monitor the performance of the corporations. It was argued by Balsmeier and Czarnitzki (2017![]() ); Lepore et al. (2017

); Lepore et al. (2017![]() ) that concentrated ownership gives control to the owners over the management of the corporation thus, leading to the enhanced performance of the company. In the study, a significant relationship was present between the return on assets and important shareholders. This relationship was generally used as an indicator for improving the performance of the company. However, the other concentrated indicators such as the ten largest shareholders (TEN LSH) and five largest shareholders (FIVE LSH) indicated an insignificant relationship with the return on assets. This study accepted that capital requirements are positively correlated with a company’s ROE and ROA and hence accepted H4.

) that concentrated ownership gives control to the owners over the management of the corporation thus, leading to the enhanced performance of the company. In the study, a significant relationship was present between the return on assets and important shareholders. This relationship was generally used as an indicator for improving the performance of the company. However, the other concentrated indicators such as the ten largest shareholders (TEN LSH) and five largest shareholders (FIVE LSH) indicated an insignificant relationship with the return on assets. This study accepted that capital requirements are positively correlated with a company’s ROE and ROA and hence accepted H4.

Globalization has resulted in creating significant changes for private companies. This however has provided an open opportunity for individuals to own private enterprises in the business market. The idea is significant in providing a positive output in the company in terms of increased economy and maximum investments. The growing economy is now encouraging the listing of companies depending on the output provided. However, for various business experts, ownership concentration, government ownership, foreign ownership concerns are some variables that create a significant impact on company performance. In certain companies, institutional ownership serves to create a positive impact on the ROA.

5. CONCLUSION

This study showed the impact of regulators on capital market’s growth and development in Saudi Arabia. The relationship was examined through various variables that including institutional ownership, government ownership, foreign ownership and capital requirements. The findings indicated that ownership concentration was important in improving the performance of both public and private companies. Institutional ownership, government ownership, and foreign ownership had a negative relationship with the ROA and ROE. ROE had a positive relationship with capital requirements. The results are not only important for Saudi companies but also other companies globally and may guide future researchers. Private and public companies should improve the efficiency and performances of the variables to enjoy economic success.

| Funding: This study received no specific financial support. |

| Competing Interests: The author declares that there are no conflicts of interests regarding the publication of this paper. |

| Acknowledgement: The author is grateful to all the associated personnel that contributed to this research. |

REFERENCES

Abdallah, A.A.-N. and A.K. Ismail, 2017. Corporate governance practices, ownership structure, and corporate performance in the GCC countries. Journal of International Financial Markets, Institutions and Money, 46: 98-115.

Abdelbary, A., 2019. Changing the game; New framework of capital adequacy ratio (No. 93072). University Library of Munich, Germany.

Aguenaou, S., O. Farooq and H. Di, 2014. Dividend policy and ownership structure: Evidence from the Casablanca stock exchange. GSTF Journal on Business Review, 2(4).

Al-Matari, E.M., Y.A. Al-Matari and S.A. Saif, 2017. Association between ownership structure characteristics and firm performance: Oman evidence. Academy of Accounting and Financial Studies Journal, 21(1).

Al-Thuneibat, A., 2018. The relationship between the ownership structure, capital structure and performance. Journal of Accounting-Business & Management, 1(25): 1-20.Available at: https://doi.org/10.31966/jabminternational.v1i25.326.

Al Nimer, M., L. Warrad and R. Al Omari, 2015. The impact of liquidity on Jordanian banks profitability through return on assets. European Journal of Business and Management, 7(7): 229-232.

Alshammary, M.J., 2014. Financial development and economic growth in developing countries: Evidence from Saudi Arabia. Corporate Ownership & Control, 11(2): 718-742.Available at: https://doi.org/10.22495/cocv11i3c1p6.

Aluchna, M. and B. Kaminski, 2017. Ownership structure and company performance: A panel study from Poland. Baltic Journal of Management, 12(4): 485-502.Available at: https://doi.org/10.1108/bjm-01-2017-0025.

Ang, A., B. Chen, W.N. Goetzmann and L. Phalippou, 2018. Estimating private equity returns from limited partner cash flows. The Journal of Finance, 73(4): 1751-1783.Available at: https://doi.org/10.1111/jofi.12688.

Anum, M.G.N., 2010. Ownership structure, corporate governance and corporate performance in Malaysia. International Journal of Commerce and Management, 20(2): 109-119.Available at: https://doi.org/10.1108/10569211011057245.

Balsmeier, B. and D. Czarnitzki, 2017. Ownership concentration, institutional development and firm performance in Central and Eastern Europe. Managerial and Decision Economics, 38(2): 178-192.Available at: https://doi.org/10.1002/mde.2751.

Barbieri, L., 2009. Panel unit root tests under cross-sectional dependence: An overview. Journal of Statistics: Advances in Theory and Applications, 1(2): 117-158.

Borisova, G., P. Brockman, J.M. Salas and A. Zagorchev, 2012. Government ownership and corporate governance: Evidence from the EU. Journal of Banking & Finance, 36(11): 2917-2934.Available at: https://doi.org/10.1016/j.jbankfin.2012.01.008.

Brau, J.C. and S.E. Fawcett, 2006. Initial public offerings: An analysis of theory and practice. The Journal of Finance, 61(1): 399-436.Available at: https://doi.org/10.1111/j.1540-6261.2006.00840.x.

Bykova, A. and F. Lopez-Iturriaga, 2018. Exports-performance relationship in Russian manufacturing companies: Does foreign ownership play an enhancing role? Baltic Journal of Management, 13(1): 20-40.Available at: https://doi.org/10.1108/bjm-04-2017-0103.

Chen, R., S. El Ghoul, O. Guedhami and H. Wang, 2017. Do state and foreign ownership affect investment efficiency? Evidence from privatizations. Journal of Corporate Finance, 42: 408-421.Available at: https://doi.org/10.1016/j.jcorpfin.2014.09.001.

Creel, J., P. Hubert and F. Labondance, 2015. Financial stability and economic performance. Economic Modelling, 48(C): 25-40.Available at: https://doi.org/10.1016/j.econmod.2014.10.025.

Cui, Y., Y. Zhang, J. Guo, H. Hu and H. Meng, 2019. Top management team knowledge heterogeneity, ownership structure and financial performance: Evidence from Chinese IT listed companies. Technological Forecasting and Social Change, 140: 14-21.Available at: https://doi.org/10.1016/j.techfore.2018.12.008.

Damodaran, A., 2007. Return on capital (ROC), return on invested capital (ROIC) and return on equity (ROE): Measurement and implications. Available from https://ssrn.com/abstract=1105499 or http://dx.doi.org/10.2139/ssrn.1105499.

Darmadi, S., 2012. Ownership concentration, family control, and auditor choice: Evidence from an emerging market. Available from https://ssrn.com/abstract=1999809 or http://dx.doi.org/10.2139/ssrn.1999809 [Accessed February 6, 2012].

Detthamrong, U., N. Chancharat and C. Vithessonthi, 2017. Corporate governance, capital structure and firm performance: evidence from Thailand. Research in International Business and Finance, 42: 689-709.Available at: https://doi.org/10.1016/j.ribaf.2017.07.011.

Ducassy, I. and A. Guyot, 2017. Complex ownership structures, corporate governance and firm performance: The French context. Research in International Business and Finance, 39: 291-306.Available at: https://doi.org/10.1016/j.ribaf.2016.07.019.

Gueyié, J.P., A. Guidara and V.S. Lai, 2019. Banks’ non-traditional activities under regulatory changes: Impact on risk, performance and capital adequacy. Applied Economics, 51(29): 3184-3197.Available at: https://doi.org/10.1080/00036846.2019.1569197.

Guvenen, F., J.R.J. Mataloni, D.G. Rassier and K.J. Ruhl, 2017. Offshore profit shifting and domestic productivity measurement (No. w23324). National Bureau of Economic Research.

Haider, Z.A., M. Liu, Y. Wang and Y. Zhang, 2018. Government ownership, financial constraint, corruption, and corporate performance: International evidence. Journal of International Financial Markets, Institutions and Money, 53: 76-93.Available at: https://doi.org/10.1016/j.intfin.2017.09.012.

Karanja, K. and D. Wagana, 2017. The influence of corporate governance on corporate performance among manufacturing firms in Kenya: A theoretical model.

Karolyi, G.A. and R.C. Liao, 2017. State capitalism's global reach: Evidence from foreign acquisitions by state-owned companies. Journal of Corporate Finance, 42: 367-391.Available at: https://doi.org/10.1016/j.jcorpfin.2016.02.007.

Kenton, W. and A. Hayes, 2019. Leverage ratio definition. Available from https://www.investopedia.com/terms/l/leverageratio.asp.

Khan, H.H., R.B. Ahmad and S.G. Chan, 2018. Market structure, bank conduct and bank performance: Evidence from ASEAN. Journal of Policy Modeling, 40(5): 934-958.

Kijewska, A., 2016. Determinants of the return on equity ratio (ROE) on the example of companies from metallurgy and mining sector in Poland. Metalurgija, 55(2): 285-288.

Krysthyn27, 2014. Media ownership – why does it matter who ‘controls’ the media? Available from https://kristyhn27.wordpress.com/2014/03/30/media-ownership-why-does-it-matter-who-controls-the-media/.

Lai, H., 2017. Ownership concentration, state ownership and company performance: Empirical evidence from the Vietnamese stock market. Doctoral Dissertation, Lincoln University.

Lepore, L., F. Paolone, S. Pisano and F. Alvino, 2017. A cross-country comparison of the relationship between ownership concentration and firm performance: Does judicial system efficiency matter? Corporate Governance: The International Journal of Business in Society, 17(2): 321-340.Available at: https://doi.org/10.1108/cg-03-2016-0049.

Levin, A., C.-F. Lin and C.-S.J. Chu, 2002. Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1): 1-24.Available at: https://doi.org/10.1016/s0304-4076(01)00098-7.

Li, Q., W. Luo, Y. Wang and L. Wu, 2013. Firm performance, corporate ownership, and corporate social responsibility disclosure in China. Business Ethics: A European Review, 22(2): 159-173.

Liang, F.H., 2017. Does foreign direct investment improve the productivity of domestic firms? Technology spillovers, industry linkages, and firm capabilities. Research Policy, 46(1): 138-159.Available at: https://doi.org/10.1016/j.respol.2016.08.007.

Maudos, J., 2017. Income structure, profitability and risk in the European banking sector: The impact of the crisis. Research in International Business and Finance, 39(PA): 85-101.Available at: https://doi.org/10.1016/j.ribaf.2016.07.034.

McGuinness, P.B., J.P. Vieito and M. Wang, 2017. The role of board gender and foreign ownership in the CSR performance of Chinese listed firms. Journal of Corporate Finance, 42: 75-99.Available at: https://doi.org/10.1016/j.jcorpfin.2016.11.001.

Migliardo, C. and A.F. Forgione, 2018. Ownership structure and bank performance in EU-15 countries. Corporate Governance: The international Journal of Business in Society, 18(3): 509-530.Available at: https://doi.org/10.1108/cg-06-2017-0112.

Muritala, T.A., 2018. An empirical analysis of capital structure on firms’ performance in Nigeria. IJAME.

Mwangi, L.W., M.S. Makau and G. Kosimbei, 2014. Relationship between capital structure and performance of non-financial companiescompanies listed in the Nairobi Securities Exchange, Kenya. Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics, 1(2): 72-90.

Ni, B., M. Spatareanu, V. Manole, T. Otsuki and H. Yamada, 2017. The origin of FDI and domestic firms’ productivity—evidence from Vietnam. Journal of Asian Economics, 52: 56-76.Available at: https://doi.org/10.1016/j.asieco.2017.08.004.

Niehaus, G., 2018. Managing capital via internal capital market transactions: The case of life insurers. Journal of Risk and Insurance, 85(1): 69-106.Available at: https://doi.org/10.1111/jori.12143.

Ofori-Sasu, D., J.Y. Abor and A.K. Osei, 2017. Dividend policy and shareholders’ value: Evidence from listed companies in Ghana. African Development Review, 29(2): 293-304.Available at: https://doi.org/10.1111/1467-8268.12257.

Oino, I., 2018. Impact of regulatory capital on European banks financial performance: A review of post global financial crisis. Research in International Business and Finance, 44(C): 309-318.Available at: https://doi.org/10.1016/j.ribaf.2017.07.099.

Ozili, P.K. and O. Uadiale, 2017. Ownership concentration and bank profitability. Future Business Journal, 3(2): 159-171.Available at: https://doi.org/10.1016/j.fbj.2017.07.001.

Paniagua, J., R. Rivelles and J. Sapena, 2018. Corporate governance and financial performance: The role of ownership and board structure. Journal of Business Research, 89: 229-234.Available at: https://doi.org/10.1016/j.jbusres.2018.01.060.

Pedroni, P., 1999. Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxford Bulletin of Economics and Statistics, 61(S1): 653-670.Available at: https://doi.org/10.1111/1468-0084.0610s1653.

Ramady, M.A., 2010. The Saudi Arabian economy: Policies, achievements, and challenges. Springer Science & Business Media.

Razafindrambinina, D. and T. Anggreni, 2017. Intellectual capital and corporate financial performance of selected listed companies in Indonesia. Malaysian Journal of Economic Studies, 48(1): 61-77.

Sheen, A., 2016. Do public and private firms behave differently? An examination of investment in the chemical industry. An Examination of Investment in the Chemical Industry. Available from https://pdfs.semanticscholar.org/3363/e3f2f8a780d2be3d1cad393c05797f8e6ec0.pdf [Accessed March 23, 2016].

Soliman, M.M., M. El Din and A. Sakr, 2013. Ownership structure and corporate social responsibility (CSR): An empirical study of the listed companies in Egypt. Available from https://ssrn.com/abstract=2257816 or http://dx.doi.org/10.2139/ssrn.2257816 [Accessed April 29, 2013].

Steven, N., 2019. Tier 1 capital vs. Tier 2 capital: What’s the difference? Available from https://www.investopedia.com/ask/answers/043015/what-difference-between-tier-1-capital-and-tier-2-capital.asp.

Tsitouras, A., A.D. Koulakiotis, G. Makris and H. Papapanagos, 2017. International trade and foreign direct investment as growth stimulators in transition economies: Does the impact of institutional factors matter?

Tulung, J.E. and D. Ramdani, 2018. Independence, size and performance of the board: An emerging market research. Corporate Ownership & Control, 15(2): 201-208.Available at: https://doi.org/10.22495/cocv15i2c1p6.

Tutu, P.K., 2017. The effects of corporate governance on performance of insurance firms in Ghana. Doctoral Dissertation, University of Ghana.

Viet, P., 2013. Foreign ownership and performance of listed companies: Evidence from an emerging economy. The Bulletin of the Graduate School of Commerce, 77: 285-310.Available at: https://doi.org/10.2139/ssrn.2373508.

Vu, M.-C., T.T. Phan and N.T. Le, 2018. Relationship between board ownership structure and firm financial performance in transitional economy: The case of Vietnam. Research in International Business and Finance, 45: 512-528.Available at: https://doi.org/10.1016/j.ribaf.2017.09.002.

Wang, K.T. and G. Shailer, 2018. Does ownership identity matter? A meta-analysis of research on firm financial performance in relation to government versus private ownership. Abacus, 54(1): 1-35.Available at: https://doi.org/10.1111/abac.12103.

Yahaya, K.A. and R.Y. Lawal, 2018. Effect of ownership structure on financial performance of deposit money banks in Nigeria. The Journal of Accounting and Management, 8(2): 29-38.

Zraiq, M.A.A. and F.H.B. Fadzil, 2018. The impact of ownership structure on firm performance: Evidence from Jordan. International Journal of Accounting, Finance and Risk Management, 3(1): 1-4.Available at: https://doi.org/10.11648/j.ijafrm.20180301.12.

Views and opinions expressed in this article are the views and opinions of the author(s), Asian Economic and Financial Review shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |