FINANCIAL PERFORMANCE ANALYSIS OF ISLAMIC BANKS IN TUNISIA

1Faculté des Sciences Economiques et de Gestion de Sfax, Unité de recherche, Economie Appliquée(URECA), Tunisie

2 Département Gestion Institut Supérieur d’Administration des Affaires de Sfax, Tunisie

ABSTRACT

This research investigates the financial performance of the Islamic banking sectors in Tunisia from year 2010-2014. The Islamic banking in Tunisia is new as compared to the conventional banking. The literature review shows that no such analysis has been dedicated to Islamic banking in Tunisia before this study. Therefore, to give a clear picture of Islamic banks to the stakeholders, the financial position of the two Islamic banks in Tunisia has been analyzed. The Performance estimates of individual banks in profitability, liquidity, risk and solvency are evaluated using the most significant financial ratios analysis. The study assesses also the overall stability of each bank. The descriptive statistical measurements (mean, standard deviation and coefficient of variation) were used to classify the performance, measuring the dispersion and the variability of these ratios. The results indicated that both banks are holding a robust financial performance position in banking industry during the period studied. Whereas al Baraka bank has slightly better levels of profitability and risk management as compared to Zitouna bank. Overall, two Islamic banks are financially stable, however al Baraka bank is in a greatest position than the Zitouna bank in terms of stability.

Keywords:Islamic banks, Financial performance, Financial ratio analysis, Tunisia.

JEL Classifications :G21, G39, C39.

ARTICLE HISTORY: Received:31 March 2017 Revised:16 May 2017 Accepted:30 May 2017Published:29 June 2017

Contribution/ Originality:: This study is one of the few studies which have analyzed the performance of Islamic banking industry in Tunisia. Also it contributes in the existing literature by employing the parametric approach to evaluate banking performance. The finding of this study will attract the attention of Islamic financial practitioners, policy makers and academicians.

1. INTRODUCTION

The recent financial crisis has shown that an efficient banking system is essential for certain fundamental aspects of the economy, such as the supply of credit, and its important role in contributing to economic stability.

Since its beginnings, the purpose of Islamic finance is to develop banking services and financial products compatible with the prescription of Sharia. Islamic finance is brought to play a social role while investing in the countries in the process of development, sustainable development and in projects with utility public. The key stage allowing the Islamic development of banking in Tunisia was by the creation of the first Islamic bank “Al Baraka bank” which is also the first in the Maghreb. Conventional banking sector is dominating banking sector in Tunisia. Currently, there are two Islamic banks. These are Al Baraka Bank of Tunisia (Established in 1983) and Zitouna Bank (Established in 2009). Since there have been limited studies investigating Tunisian Islamic banks' performance, the objective of this study is to analyze their financial performance during the period 2010-2014.

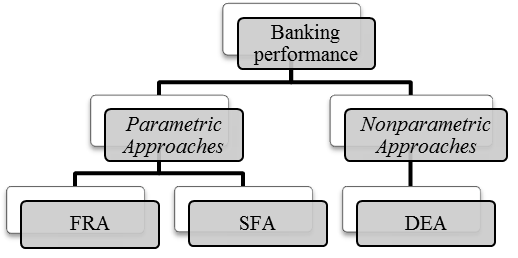

After political change in Tunisia, national authorities and investors intervened to evoke Islamic finance, an aspect long omitted by the entire Tunisian banking corporation, as an effective way to boost investment in Tunisia. The main challenges facing the Islamic financial institution are the need to attract more savers, improve the profitability of its activities and contribute to the development of the national economy. In the banking sector in general, there are a large number of entrepreneurs who are convinced that banking interests are usurious and are not in accordance with the precepts of the Sharia. As a result, a potential flow occurs outside conventional banks. So the new Tunisian government introduces regulatory texts 1 to organize Islamic banking and encourage investors to invest their funds in all types of finance that are based on Sharia principles. Thus, the BCT2 offers to Islamic banks the same operating conditions made available to the traditional Tunisian banks, in order to guarantee the requirements of fair competition. Evaluate the performance of financial institutions has acquired academic considerations over the years. Different approaches have been used to determine the financial performance. These approaches generally fall under two types: nonparametric approaches, such as Data Envelopment Analysis (DEA), and parametric approaches, such as Financial Ratios Analysis (FRA) and The Stochastic Frontier Approach (SFA).

Figure-1. Evaluate banking performance

Source: Berger and Humprey (1997) and authors’ own research

The objectives of this research is to evaluate the financial performance of two Islamic banks in Tunisia using three groups of financial ratios that will indicates the performance developments over the period 2010-2014. Furthermore, this research is going to assess the financial stability of the two banks using the z-score indicator. The data was gathered from balance sheets and income statements of each bank, which are available on their official website. The descriptive statistical analysis is used to classify the performance, measuring the dispersion and the variability of the ratios.

2. LITERATURE REVIEW

The Islamic bank is an institution whose main activity is the mobilization of funds from the surplus agents (savers) and the supply of these funds to the deficit agents (company, businessmen). It performs these functions using several Sharia-compliant modes of financing (Al-Jarhi and Iqbal, 2001). These characteristic traits of Islamic banks have attracted the attention of the scientific community, seeking to see whether by respecting the principles of Islam, these financial institutions are able to hold a strong financial performance position. On the empirical level, it seems that the number of study concentrated in the comparison of financial performance between Islamic banks or between Islamic and conventional banks is actually undergoing a thrust (Samad, 1999; Tarawneh, 2006; Abdul-Hamid and Azmi, 2011; Masruki et al., 2011). There are various studies in the existing literature that have been used financial ratios analysis, which is the simplest and most popular method for measuring performance of Islamic banks (Samad and Hassan, 2000; Hassan and Bashir, 2003; Samad, 2004; Saleh and Zeitun, 2006; Olson and Zoubi, 2008). This research model is most optimal to realize the objectives of this study. In the economic and financial literature, two key indicators have been put forward to measure bank profitability: ROA and ROE. These two profitability ratios have been used in most studies of the performance of Islamic banks (Samad and Hassan, 2000; Saleh and Zeitun, 2006; Al-Tamimi, 2010; Akhter et al., 2011; Abduh et al., 2013; Ajlouni and Hamed, 2013; Azouzi and Letaief, 2013; Muda et al., 2013; Ibrahim, 2015; Odeduntan et al., 2016).

Samad and Hassan (2000) analyzed the intertemporal and interbank performance of Malaysian Islamic bank (Bank Islamic Malaysia Berhad) during 1994-1997 by applying the financial ratios. The performance is measured in terms of profitability, liquidity, risk and solvency, and community involvement. The findings described that the bank is relatively more liquid and less risky compared to a group of 8 conventional banks. Also, evaluating the inter-temporal comparison of BIMB's performance show that Islamic bank made statistically significant progress on profitability ratios (ROA and ROE) over the period of the study.

Saleh and Zeitun (2006) in order to evaluate the Islamic banks’ performance in Jordon, examine and analyze the experience of two Islamic banks, Jordan Islamic Bank for Finance and Investment (JIBFI), and Islamic International Arab Bank (IIAB). The research reveals that the efficiency of both banks has increased and they have played an important role in financing projects in Jordan. Also, the Bank for Finance and Investment (JIBFI) is found to have high profitability. The study concludes that Islamic banks have great development in the credit facilities and in profitability.

Azouzi and Letaief (2013) compared the efficiency of Islamic banks in a number of developing countries, while focusing on the countries of the Arab Maghreb Union, Algeria, Mauritania and Tunisia. The study covered the years 2005-2009 to assess the financial performance of the seventeen Islamic banks. The results obtained in the light of the ratios analysis revealed that, while the overall performance of the sample is declining, that of the Tunisian and Algerian banks is increasing and that of the Mauritanian bank is stable. Ajlouni and Hamed (2013) investigate and compare the development of three Jordanian Islamic banks performance over time 2005-2009. They authors used two different approaches: Malmquist Data Envelopment Analysis and Financial Ratio Analysis. They found that those Jordanian Islamic banks are constantly efficient. Moreover, it is recommended that Jordanian Islamic banks managers should increase their banks efficiency by improving recourse utilization to produce optimal outputs.

Akhter et al. (2011) studied the efficiency and performance of Islamic bank in relation to two conventional banks in Pakistan. They used the financial ratios to measure profitability, liquidity risk and credit risk for the years 2006-2010. The results showed that no significant difference is observed between the two types of banks in respect of profitability and a divergence in liquidity and credit performance.

Abduh et al. (2013) investigated the efficiency and performance of five Islamic banks in Bangladesh for the years 2006-2010. Data are collected through their published annual reports. They measured the performance and efficiency of Islamic banks using ratio analysis and data envelopment analysis respectively. Their finding showed that Shajalal Islami Bank limited is better than other Islamic banks in terms of ratio analyzed. Moreover, the result of Data envelopment analysis concluded that all Islamic banks have shown an improvement on their efficiency level.

Ibrahim (2015) measured the financial performance of two Islamic banks in United Arab Emirates for the period of 2003 to 2007. the financial ratios is used to measure liquidity, profitability, management capacity, capital structure and share performance ratios and make a comparison between these two banks . The research evaluates also the financial stability of the two banks. The results showed that the overall performance of both banks Islamic banks is satisfactory both. Moreover, Dubai Islamic bank has better levels of profitability and liquidity its rival. However, the analysis of four ratios of share performance reveals that Abu Dhabi bank is better off than Dubai Islamic bank. Finally, Abu Dhabi bank had a high level of stability than Dubai Islamic bank.

Odeduntan et al. (2016) analyzed the financial stability of sixteen Islamic banks in Malaysia, using Z-score analysis, Liquidity ratio, Nonperforming financing as well as Credit risk ratio for the years 2008-2012. Their finding reveals that the Z-score is relatively high and thus conclude that Islamic banks are financially stable. However, the results show that Islamic banks currently provide excessive financing in relation to the total assets they invest in financing. Despite this, auteurs argued that Islamic banks are not likely to experience financial mess in the immediate term if their liquidity ratios and loan to deposit ratios are regularly monitored.

Cihak and Hesse (2010) evaluated the relative financial strength of Islamic banks. They used Z-score as a measure of stability on individual Islamic and commercial banks in 19 banking systems. The results revealed that (a) small Islamic banks tend to be financially stronger than small commercial banks; (b) large commercial banks tend to be financially stronger than large Islamic banks; and (c) small Islamic banks tend to be financially stronger than large Islamic banks. They found also, that the market share of Islamic banks does not have a significant impact on the financial strength of other banks.

3. ANALYSIS AND FINDINGS

This research evaluates the financial performance of Islamic banks in Tunisia, Al Baraka Bank Tunisia (Established in 1983) and Zitouna Bank (Established in 2009). The annual financial data used in this study has been gathered and analyzed from the balance sheets and income statements which are available in the annual reports of the concerned banks. Generally, financial ratio analysis has been applied to measure the performance of a bank. In order to see how Islamic Bank in Tunisia performed over 5 years, this study approaches an analysis of nine financial ratios3 . These ratios are grouped under three broad categories: profitability, liquidity, risk and solvency (Samad and Hassan, 2000). Moreover, this study examines the overall stability of each bank by using Z-Score indicator.

3.1. Profitability Ratio

As profit of a firm is the amount by which its revenues are more than the cost. Profitability ratios can be used to evaluate the capacity of a bank to generate earnings that are higher as compared to all the costs and expenses of the bank. In our study, the profitability of the two Islamic banks is measured through ROA, ROE (Samad and Hassan, 2000).

3.1.1. Return on Asset (ROA)

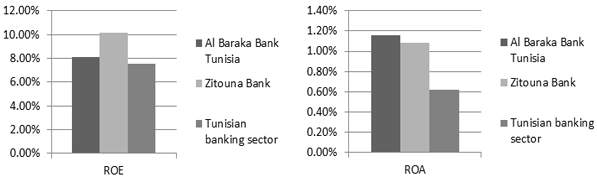

It shows how a bank can convert its asset into net earnings. Based on the analysis in Table 1, Al Baraka Bank captured high level of profitability with a mean percentage of 1.16 % against Zitouna Bank with 1.08 %. This has been associated with more stability level based on the coefficient of variation. However, these two Islamic banks enjoy high profitability than the Tunisian conventional banking sector which has a percentage mean of 0.6% as it shown in Figure 2.

3.1.2. Return on Equity (ROE)

It is net earnings per unit of equity capital. The high ratio indicates the more efficient management in utilizing its equity and the better return to investors. Tables 1 demonstrate that Zitouna Bank has the higher level of profitability with a mean percentage of 10.14% comparing with Al Baraka Bank with 8.13%, and it may attract more investors to invest their money in this bank, especially it is associated with high dispersion. Figure 2 show thatthe mean ROE of Islamic banks has remained higher as compared to the banking sector in Tunisia which has a percentage mean of 7.56%.

Table-1. Computation of Profitability (Amount in %)

Year |

2010 |

2011 |

2012 |

2013 |

2014 |

Mean |

Standard deviation |

Coefficient of variation |

|

ROA |

|||||||||

Al Baraka Bank |

2.2 |

1.2 |

0.84 |

0.85 |

0.72 |

1.16 |

0.6 |

0.52 |

|

Zitouna Bank |

1.6 |

2.9 |

0.17 |

0.17 |

0.56 |

1.08 |

1.17 |

1.08 |

|

ROE |

|||||||||

Al Baraka Bank |

14.4 |

7.6 |

5.6 |

6.8 |

6.25 |

8.13 |

3.58 |

0.44 |

|

Zitouna Bank |

11.9 |

26.23 |

2.11 |

2.95 |

7.5 |

10.14 |

9.81 |

0.96 |

|

Source: Annual Reports

Figure-2. Comparison between profitability of Islamic banks and banking sector in Tunisia** (during 2010-2014)

Source: CENTRAL BANK OF TUNISIA: Report on Banking Supervision (2011 p62; 2013 p51; 2015 p72) * Mean percentage **Indicator of 22 resident banks.

3.2. Liquidity Ratio

It provides a measure of banks ability to generate cash to meet its immediate obligations (Alrawashedh et al., 2014). Liquidity risk arises from difficulties in mobilizing funds (increase in liabilities) at a reasonable cost (borrowing) or in selling financial assets. So, when withdrawal exceeds new deposit significantly over a short period, banks get into liquidity trouble. Liquidity measures has following ratio (Samad and Hassan, 2000; Irfan and Zaman, 2014).

3.2.1. CDR (Cash to Deposit Ratio)

A higher cash to deposit ratio means that a bank is relatively more liquid than a bank which has lower CDR. Zitouna Bank has the higher level of liquidity (CDR) with a mean percentage of 8.13% comparing with Al Baraka Bank with 3.91%. This has been associated with more stability level based on the coefficient of variation as it shown in Tables 2.

3.2.2. LDR (Loan to Deposit Ratio)

If the ratio is too high, it means that banks take more financial stress by making excessive loan and it indicates a potential source of illiquidity and insolvency. Based on mean measure, the below Table 2, show that al Baraka Bank has lower level of Loan to Deposit Ratio with a mean of 88.3% than Zitouna bank with a mean ratio of 94.82% over the years of study except in 2011. In addition, the standard deviation and the coefficient of variation of al Baraka Bank indicate the higher dispersion and instability level of this ratio over the time in al Baraka Bank than in Zitouna bank.

3.2.3. CR (Current Ratio)

This ratio measures bank's ability to pay short-term and long-term obligations. Therefore, Depositors' trust to bank is reinforced when a bank maintains a higher CR. The mean measurement of Current Ratio is slightly different between the two banks as it shown in Table2. Al Baraka Bank has higher CR with a mean of 83.02% than Zitouna bank with a mean ratio of 59.86%. The coefficient of variance clearly indicates that Al Baraka bank has a less variability levels in this ratio comparing the Zitouna Bank.

3.2.4. CA (Current Asset Ratio)

A higher ratio is a sign that a bank has more liquid asset. However, a low ratio indicates the illiquidity as more of the assets are long term. Based on the mean measure, the Tables 2 demonstrate al Baraka Bank has more liquid asset with a mean percentage of 71.75% than Zitouna Bank with 53.29%. Therefore, this bank benefits a higher level of liquidity than its rival bank. This has been associated with less variability level based on the coefficient of variation.

In general, Tunisian Islamic banks adequately control their liquidity risk despite the absence of assets easily mobilizable from the central bank or negotiable in the financial Market.

Table-2. Computation of Liquidity (Amount in %)

Year |

2010 |

2011 |

2012 |

2013 |

2014 |

Mean |

Standard Deviation |

Coefficient of Variation |

|

CDR |

|||||||||

Al Baraka Bank |

2.37 |

1.69 |

2.38 |

11.8 |

1.3 |

3.91 |

4.44 |

113.5 |

|

Zitouna Bank |

7.84 |

4.91 |

9.58 |

8.31 |

10 |

8.13 |

2.01 |

24.72 |

|

CR |

|||||||||

Al Baraka Bank |

78.8 |

93.1 |

88.5 |

73 |

81.5 |

83.02 |

7.96 |

9.59 |

|

Zitouna Bank |

82.4 |

59.21 |

56.9 |

51.2 |

15.5 |

59.86 |

13.23 |

22.11 |

|

CA |

|||||||||

Al Baraka Bank |

75.3 |

78.3 |

75.1 |

63.8 |

66.2 |

71.75 |

6.35 |

8.86 |

|

Zitouna Bank |

68.7 |

52.6 |

51.4 |

48.2 |

45.5 |

53.29 |

9.05 |

16.99 |

|

LDR |

|||||||||

Al Baraka Bank |

85.2 |

97.7 |

92.1 |

75.9 |

90.7 |

88.3 |

8.24 |

9.32 |

|

Zitouna Bank |

95.9 |

95.2 |

92.7 |

94.7 |

95.6 |

94.82 |

1.27 |

1.34 |

|

Source: Annual Reports

3.3. Risk and Insolvency Ratio

3.3.1. Debt Equity Ratio (DER)

This ratio represents the weight of a bank's liabilities relative to its equity. It indicates the proportion in which a bank finances: external sources (total liabilities) and inside sources (shareholder’s equity). Higher ratio is critical because it show the level of solvency of an institution and its possible risk of failure. A lower DER ratio is a good sign for a bank.

Tables 3 demonstrate that al Baraka Bank has low ratio than Zitouna Bank, as it has a mean of 5.10 comparing with Zitouna Bank with a mean of 9.61. On average, Zitouna bank’s creditors provided 9.61 dinars in financing for every Dinar contributed by shareholders, comparing to 5.10 Dinars for al Baraka Bank. Based on the coefficient of variation, the analysis also shows that al Baraka bank has managed to control this ratio better than Zitouna bank.

3.3.2. Debt to Total Asset Ratio (DTAR)

This ratio measures the financial strength of a bank to pay off its debt with its assets. A higher ratio indicates that the creditors have more claims on the bank’s assets, thus it can increases the insolvency risk. Based on Table 3, it is al Baraka Bank managed to reduce this ratio over the years with a mean percentage of 73 % and low level of variability against a mean percentage of 84% for Zitouna Bank.

3.3.3. Equity Multiplier (EM)

It represents the amount of a bank's assets that are financed by its shareholders. Therefore, a higher EM means that an important part of asset financing is being done through debt witch imply a greater risk for a bank. Equity Multiplier is calculated by dividing total assets by the shareholders’ equity. Table 3 demonstrates that al Baraka Bank has a higher equity multiplier than Zitouna Bank, as it has a mean of 11.4 comparing with Zitouna Bank with a mean of 10.7. This indicates that Al Baraka Bank uses equity to finance 8.77% of its assets and the remaining 91.23% is financed by debt. A lower EM is preferred because it indicates that a bank is taking on less debt to finance its assets. In this case, the two Islamic banks in Tunisia are using more debt to finance its asset purchases. The standard deviation and the coefficient of variation show less dispersion and more stability of this ratio for al Baraka bank.

Table-3. Computation of Risk and insolvency ratio

Year |

2010 |

2011 |

2012 |

2013 |

2014 |

Mean |

Standard Deviation |

Coefficient of variation |

|

DER (times) |

|||||||||

Al Baraka Bank |

4.66 |

5.14 |

5.07 |

4.61 |

6.02 |

5.1 |

0.56 |

0.11 |

|

Zitouna Bank |

5.5 |

7.03 |

10 |

14.5 |

10.9 |

9.61 |

3.54 |

0.37 |

|

DTAR (%) |

|||||||||

Al Baraka Bank |

0.8 |

0.8 |

0.77 |

0.58 |

0.7 |

0.73 |

0.09 |

0.13 |

|

Zitouna Bank |

0.76 |

0.78 |

0.8 |

0.83 |

0.84 |

0.81 |

0.03 |

0.04 |

|

EM (times) |

|||||||||

Al Baraka Bank |

10.5 |

11.8 |

12.3 |

15.2 |

7.06 |

11.4 |

2.59 |

0.26 |

|

Zitouna Bank |

7.41 |

7.29 |

9.87 |

14.1 |

14.9 |

10.7 |

3.64 |

0.34 |

|

Source: Annual Reports

3.3.4. Z-Score (Bank Stability Measure)

Z-score is one of the popular measures of bank soundness and stability (Yeyati and Alejandro, 2007; Demirguc-Kunt and Detragiache, 2009; Cihak and Hesse, 2010). The Z-score is inversely associated to the probability of a bank’s insolvency. Therefore, a higher z-score implies a lower risk of insolvency. Where![]() is the ratio of total equity over total assets of the bank and

is the ratio of total equity over total assets of the bank and ![]() is the expected return on assets.

is the expected return on assets. ![]() is a proxy for the volatility of ROA, all of which are calculated on the basis of accounting data (Boyd and al, 2006). Tables 4 show that two Islamic banks are financially stable. Moreover, the z-score of al Baraka bank is slightly higher than of Zitouna Bank for individual years and for the whole period 2010-2014.

is a proxy for the volatility of ROA, all of which are calculated on the basis of accounting data (Boyd and al, 2006). Tables 4 show that two Islamic banks are financially stable. Moreover, the z-score of al Baraka bank is slightly higher than of Zitouna Bank for individual years and for the whole period 2010-2014.

Table-4. Z-score Measurement

Year |

2010 |

2011 |

2012 |

2013 |

2014 |

Z-Score: 2010-2014 |

Al Baraka Bank |

31.53 |

27.27 |

26 |

21.85 |

20.05 |

25.34 |

Zitouna Bank |

13.04 |

11.84 |

6.86 |

4.96 |

6.94 |

8.73 |

Source: Annual Reports

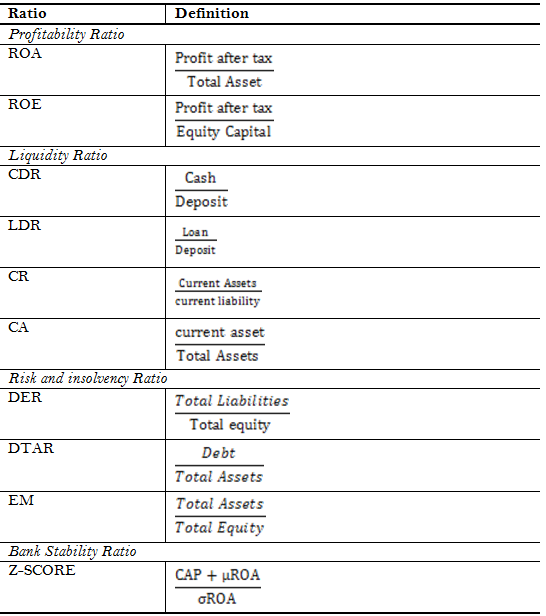

Table-5. Definition of financial analysis ratios

Source: Samad and Hassan (2000); Cihak and Hesse (2010) and authors’ own research

4. CONCLUSION

The current economic crisis in Europe, the United States and the rest of the world is closely linked to financial crises caused by financial products with interest rates and speculative products prohibited by the Sharia. In the case of Tunisia, the Islamic banking sector show high levels of performance during 2010-2014. This is supported by our results which are detailed below.

This study conducts a comparative performance of two Islamic banks in Tunisia for the period of 2010-2014. It used three groups of parameters to measure profitability, liquidity, Risk and insolvency. The Financial Ratio Analysis results show that both banks are holding a sustainable financial performance position in banking industry. The results indicate also that there is no significant difference in the profitability levels of both Islamic banks. However Zitouna Bank has high level of instability. As far as liquidity in various measures, the analysis shows that Al Baraka Bank has higher ratio than Zitouna Bank. The research findings declared that al Baraka Bank has managed to control their risk and insolvency ratio better than Zitouna bank. Finally, the study of the z-scores seem to suggest that two Islamic banks are financially stable, however al Baraka bank is in a greatest position than the Zitouna bank in terms of overall stability.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: Both authors contributed equally to the conception and design of the study. |

REFERENCES

Abduh, M., S. Hasan and A. Pananjung, 2013. Efficiency and performance of islamic banks in Bangladesh. Journal of Islamic Banking and Finance, 30(2): 94-106. View at Google Scholar

Abdul-Hamid, M. and S. Azmi, 2011. The performance of banking during 2000-2009. International Journal of Economics and Management Sciences, 1(1): 9-19. View at Google Scholar

Ajlouni, M.d.M. and O.O. Hamed, 2013. Performance efficiency of the Jordanian islamic banks using data envelopment analysis and financial ratios analysis. European Scientific Journal. View at Google Scholar

Akhter, W., A. Raza and M. Akram, 2011. Efficiency and performance of islamic banking: The case of Pakistan. Far East Journal of Psychology and Business, 2(2): 54-71. View at Google Scholar

Al-Jarhi, M. and M. Iqbal, 2001. Islamic banking: Answers to some frequently asked questions. Islamic Research and Training Institute.

Al-Tamimi, H.A.H., 2010. Factors influencing performance of the UAE islamic and conventional national banks. Global Journal of Business Research, 4(2): 1-9.

Alrawashedh, M., S.R.M. Sabri and M.T. Ismail, 2014. The significant financial ratios of the islamic and conventional banks in Malaysia region. Research Journal of Applied Sciences, Engineering and Technology, 7(14): 2838-2845. View at Google Scholar | View at Publisher

Azouzi, D. and A. Letaief, 2013. Les banques islamiques du maghreb souffrent-elles d’un retard d’efficience ? Une analyse par les ratios et la window analysis. Etudes en Economie Islamique, 7(1): 1-30. View at Google Scholar

Berger, A. and D. Humprey, 1997. Efficiency of financial institutions: International survey and directions for future research. European Journal of Operational Research, 98(2): 175-212. View at Google Scholar | View at Publisher

Cihak, M. and H. Hesse, 2010. Islamic banks and financial stability: An empirical analysis. Journal of Financial Services Research, 38(2-3): 95-113. View at Google Scholar | View at Publisher

Demirguc-Kunt, A. and E. Detragiache, 2009. Basel core principles and bank soundness: Does compliance matter ? Policy Research Working Paper Series 5129, The World Bank.

Hassan, M.K. and A.H.M. Bashir, 2003. Determinants of islamic banking profitability. 10th ERF Annual Conference, Morocco. pp: 16-18.

Ibrahim, M., 2015. Measuring the financial performance of islamic banks. Journal of Applied Finance and Banking, 5(3): 93-104.View at Google Scholar

Irfan, M., Y. and K. Zaman, 2014. The performance and efficiency of islamic banking in South Asian countries. Economia Seria Management, 17(2): 223-237. View at Google Scholar

Masruki, R., N. Ibrahim, E. Osman and H. Abdul-Wahab, 2011. Financial performance of Malaysian founder islamic banks versus conventional banks. Journal of Business and Policy Research, 6(2): 67-79. View at Google Scholar

Muda, M., A. Shaharuddin and A. Embaya, 2013. Comparative analysis of profitability determinants of domestic and foreign islamic banks in Malaysia. International Journal of Economics and Financial Issues, 3(3): 559-569. View at Google Scholar

Odeduntan, A., A. Adewale and S. Hamisu, 2016. Financial stability of islamic banks: Empirical evidence. Journal of Islamic Banking and Finance, 4(1): 39-46. View at Google Scholar | View at Publisher

Olson, D. and R. Zoubi, 2008. Using accounting ratios to distinguish between islamic and conventional banks in the GCC region. International Journal of Accounting, 43(1): 45-65. View at Google Scholar | View at Publisher

Saleh, A.S. and R. Zeitun, 2006. Slamic banking performance in the Middle East: A case study of Jordan. Working Paper No. 06-21, Department of Economics, University of Wollongong.

Samad, A., 1999. Comparative efficiency of the islamic bank Malaysia vis-à-vis conventional banks. IIUM Journal of Economics and Management, 7(1): 1-27.View at Google Scholar

Samad, A., 2004. Performance of interest-free Islamic banks vis-à-vis interest-based conventional banks of Bahrain. IIUM Journal of Economics and Management, 12(2): 1-15. View at Google Scholar

Samad, A. and M.K. Hassan, 2000. The performance of Malaysian islamic bank during 1984-1997: An exploratory study. International Journal of Islamic Financial Services, 1(3).

Tarawneh, M., 2006. A comparison of financial performance in the banking sector: Some evidence from omani commercial banks. International Research Journal of Finance and Economics, 3(3): 101-112. View at Google Scholar

Yeyati, E.L. and M. Alejandro, 2007. Concentration and foreign penetration in Latin American banking sectors: Impact on competition and risk. Journal of Banking and Finance, 31(6): 1633–1647. View at Google Scholar | View at Publisher

Views and opinions expressed in this article are the views and opinions of the author(s), Asian Economic and Financial Review shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |

Footnotes:

3. See Table 5 p 9