MODERATING EFFECT OF INTERNAL CONTROL SYSTEM ON THE RELATIONSHIP BETWEEN GOVERNMENT REVENUE AND EXPENDITURE

1,2Department of Accountancy, ModibboAdama University of Technology Yola, Yola, Adamawa State, Nigeria

ABSTRACT

The study aims at examining the moderating effect of internal control system on the relationship between government revenue (statutory allocation and internally generated revenue) and expenditure. All the sixteen (16) local governments in Taraba state of Nigeria were considered the population and were as well maintained as the sample size of the study. Secondary data was gathered from the official websites of Federal Ministry of Finance and office of the Accountant General of the Federation, and others from annual accounts and reports of the population of this study. The study utilizes ex-post facto research design to examine the relationship between the study variables. Descriptive statistics, correlation, and hierarchical multiple regression analyses were carried out to answer the research questions raised in this study. The study finds that statutory allocation and internally generated revenue are positively related to government expenditure, which may cause more government spending that may leads to fiscal imbalances. When further analysis was conducted, the result reveals that internal control system moderates both statutory allocation and internally generated revenue towards government expenditure, but internal control system is not effectively applied in the local governments. Therefore, this study suggests that government should strategize ways to improve revenue generation on one hand, and control expenditure excesses on the other hand so as meet its objectives.

© 2017 AESS Publications. All Rights Reserved.

Keywords:Government revenue, Statutory allocation, Internally generated revenue, Government expenditure, Internal control system, Local government.

JEL Classification: H27, H71, H76, H83.

Received: 7 October 2016/ Revised: 24 November 2016/ Accepted: 14 December 2016/ Published: 21 January 2017

Contribution/ Originality:

This study significantly contributes to the existing literature by testing the moderating effect of internal control system on the relationship between government revenue and expenditure in Nigeria. The study believes that internal control system may impact on government expenditure, and may moderates the effect of government revenue on its expenditure, hence, the need to carry out such study.

1. INTRODUCTION

Every government has numerous objectives to achieve that include securing of lives and properties, provision of infrastructure and other social amenities, creating an enabling business environment, employments creation and jobs protection among others, to its citizens. These objectives which are expenditures of the government could be achieved through revenues accruing to the government over a given period of time. Specifically, government can raise revenues by either through tax or non-tax mechanisms (e.g., licensing of motor vehicles, medical fees, court fines, rent of government properties, earnings and sales etc.). In this effect, unless the revenues raised are effectively and efficiently utilized for the intended objective, generating of all these sources may have a deterrent effect on the dwindling revenue of government and performance of the economy (Adenugba and Ogechi, 2013; Muhammed and Asfaw, 2014).

However, revenue as opined by Hamid (2008) encompasses receipts from tax and non-tax sources which are also generated from sale of government properties or from other interests on loans and returns from investments. Revenues accruing to government are basically derived from two major sources; internally generated revenue and statutory allocation from federation account (Oladoyin et al., 2005; Adams, 2006). At the second tier and third tier levels of government, revenues which are derived from within the state or local government are referred to as ‘internally generated revenue’ while externally generated revenues are those derived from federation account allocation, excess crude oil, value added tax among others (Adams, 2006; Abba et al., 2015).

It is worthy to mention that in whatever way revenue is defined or classified, the central theme is the role that it plays in engineering growth and development of an economy. To this end, no government can effectively discharge its responsibilities to the public without sufficient revenue in place. To obtain sufficient revenue and ensure its effective and efficient utilization towards government intended purposes, there is need for effective control. In regards to this, Adams (2006) postulates that revenue control could be defined as the strings of coordinated actions that must be embarked upon in order to ensure that the streams of income accruing to the organization remained unaltered if it cannot be increased.

Nevertheless, government expenditures include money spent on safeguarding lives and properties, employment creation, payment of salaries, payment of contracts, health care services, maintenance of law and order, and building of schools and provision of educational facilities among others. Adams (2006) posits that public (government) expenditure refers to the expenses that are incurred by government in order to run it affairs. Government expenditures are the expenses incurred for maintenance of good governance in the interests of the society as well as the economy in general (Adejoh and Sule, 2013).

According to Adenugba and Ogechi (2013) government expenditures will have a significant impact on internally generated revenues of municipalities if well and adequately managed by enhancing the allocation of scarce resources on the basis of established objectives. Consequently, Ukah (2009) asserts that there is an urgent need for efficient management and control of government expenditure to ensure that optimality is attained. In addition, all government spending has to be approved by the legislatures in order to mitigate misappropriations. Therefore, all these could be achieved through generated revenues of government and a well-established system of internal control.

Coherently, Adams (2006)stresses that the revenue control system in the public sector is designed to include elements like: periodic monitoring, policing the administration system to ensure that services are not rendered without charges, timely issuance of demand notices and follow-up actions to track debts, timely issuance of controlled forms, and receipts books and documents. Additionally, other elements include: promptly lodgment into the bank of all revenue received, establishment of authority limits, establishment of cash limits, and above all, establishment of functional system of internal controls. With effective system of internal controls in function, it is presumed that the revenues accruing to government will be enhanced as well be controlled and managed.

Internal control provides an independent appraisal of the effectiveness of the management in carrying out the responsibilities assigned to them for better revenue generation. In the same vein, Baltaci and Yilmaz (2006) reported that internal control system is a process that guide organizations (private and public) towards achieving their predetermined objectives. Therefore, an effective internal control system undoubtedly correlates with organizational success in attaining targeted revenue level (Fadzil et al., 2005). For the purpose of this study, an effective internal control system can be viewed as established control measures by an organization (private or public) which aims at safeguarding its resources and ensure effective compliance with relevant policies and procedures for the betterment of the organization.

The increasing costs of running government, coupled with dwindling revenue have led various state governments in Nigeria into formulating strategies to improve the revenue base. Moreover, the near collapse of the national economy has initialized a grave financial situation in the three tiers of government in Nigeria (Adenugba and Ogechi, 2013). However, despite the numerous revenue sources at the doors of the various tiers of government as specified in the Nigerian 1999 constitution, since the 1970 till now, over 80% of the annual revenue of the three tiers of government comes from crude oil. Adenugba and Ogechi further stressed that the serious decline in the price of oil in recent years decreases the funds available for redistribution to various states. Therefore, the need for states and local governments to generate adequate revenue internally has become necessary and a matter of significant importance. This need underscores the eagerness on part of the states and local governments and even the federal government to look for new sources of revenue or to become more concerned and innovative in the mode of collecting revenue from existing sources.

Furthermore, section 162(6) of 1999 constitution of the Federal Republic of Nigeria requires that each state shall have a special account to be referred as ‘state joint local government account’. Therefore, Taraba state operates the Joint Account Committee, which is a committee responsible for allotting of funds to local governments. Through this committee, statutory deductions (e.g., deductions for financing the activities of local government service commission, Universal Basic Education, local government Pension Board, among others) are made as required by section 162(6) of Nigerian constitution. Yet, the deductions made the statutory allocation grossly inadequate to finance the activities of the local governments (Abba et al., 2015). For this reason, local governments in a state need to find ways to enhance their internal development fund as suggested by scholars like: Abba et al. (2015); Adenugba and Ogechi (2013); Muhammad (2012); Mbedzi and Gondo (2010); Garko (2009); Ukah (2009); Yunusa (2009) and Abba et al. (2008).

Consequently, local governments in Nigeria are faced with myriads of problems ranging from corruption and embezzlement, poor financing, mismanagement of funds to poor leadership (Adejoh and Sule, 2013). These have therefore deterred the development of local government in Nigeria. As a result, it has become necessary to conduct an analysis on revenue generation and government expenditure of Taraba state. Moreover, previous studies have examined the effect and relationship between Internally Generated Revenue and Government expenditure, internal control and internally generated revenue, or internal control system and government expenditure (e.g., (Abba et al., 2008; Garko, 2009; Ukah, 2009; Yunusa, 2009; Mbedzi and Gondo, 2010; Muhammad, 2012; Adenugba and Ogechi, 2013; Abba et al., 2015) ). This study will therefore fill the flaws in previous researches by introducing internal control system as a moderator to the effect of revenue generation on government expenditure in Taraba state.

Therefore, the objectives of this study is to: (1) examine the relationship between total revenue (statutory allocation and internally generated revenue) and government expenditure; (2) identify the extent of applying effective internal control system in Taraba state; and (3) examine the moderating effect of internal control system on the relationship between government revenue and expenditure.

2. PRIOR STUDIES AND HYPOTHESES DEVELOPMENT

The causal relationship between government expenditures and it revenues has inspired a vast literature both at the theoretical and empirical level. An effective understanding of this relationship might contribute to the formulation of specific policies regarding deficits management and sustainability of fiscal policies of countries having huge fiscal imbalances. An empirical study by Sani (2005) indicates revenue and expenses on infrastructural facilities have positive relationship, and as well, a positive relationship exists between and public spending on infrastructural facilities and economic growth.

While Obioma and Ozughalu (2015) in their study on examination of the relationship between public revenue and public expenditure in Nigeria found that changes in government revenue induce changes in government expenditure. Based on their empirical findings, they suggested that for government to increase spending, efforts should be made to enhance government revenue which should also be escorted with a proper public expenditure reform for the attainment of a bearable economic growth.

Abba et al. (2015) examined the relationship between Expenditure and Internally Generated Revenue at local government level in Adamawa state. They found that expenditure has significant impact on local government internally generated revenue. Their study recommends that Proper accountability and transparency should be adopted in incurring expenditure (capital and recurrent) in the local government. This may include community participation on project to be executed in the local government, disclosing what has been generated as IGR over a period of time. They also recommend that capital expenditure in the local government should be encouraged. Some of the recurrent expenditure that does not contribute significantly to the revenue generation in the local government should be minimized. Such recurrent expenditures are those in the office of the chairman, secretary, legislative arm and personal management should be minimized, so that the amount can be allocated for capital expenditure. Edogbanya and Ja’afaru (2013) reported that there is a significant relationship between revenue generated and developmental effort of government. Olusola (2011) using ordinary least square found out that revenue sources like rates, fines, fees and licenses, and rent are factors that significantly influence the generating of revenue internally of local governments in Ogun State.

More so, it has been noted that out of the major internal revenue sources to Local governments, the combination of rates, fees, fines, local license, and earnings accruing from saleable undertakings accounted for about 75% of Local Government internally generate recurrent revenues (Ola and Tonwe, 2005). Oseni (2013) finds that states that get supplementary revenue as derivation from statutory allocations have lower proportions of internally generated revenue to their aggregate revenues than others. While lowest internally generated revenue for the periods goes to states where insurgency had been threatening. Dependence by states on the statutory allocations does not necessarily explain an effective dividend of democracy, because internally generated revenues are a means to develop the states.

Adesoji and Chike (2013) reported that there is a positive relationship between infrastructural development and internally generated revenue. The study also reveals the various methods of generating internal revenue are contribution, creation of public enlighten and the use of tax personnel via enforcement. However, their study suggests that there is need to overhaul the revenue administration agencies in order to promote revenue generation in the country. Moreover, allocation of revenue to the tiers of government does not normally follow the norms to fulfill the expenditure requirements of each of the three tiers of government, hence, the federal government can be viewed as a surplus-spending unit.

However, despite the numerous empirical studies (e.g., (Fayemi, 1991; Ola and Tonwe, 2005; Sani, 2005; Olusola, 2011; Adesoji and Chike, 2013; Edogbanya and Ja’afaru, 2013; Ndungu, 2013; Oseni, 2013; Abba et al., 2015; Obioma and Ozughalu, 2015) ) conducted to examine the relationship between revenue and expenditure, internal control and revenue or internal control and expenditure, yet less attention have been paid on the use of internal control as a moderating variable to strengthen the relationship between revenue and expenditure. Based on the foregoing, this study therefore hypothesized that:

H1: Total revenue of government has no significant relationship with government expenditure.

H2: Internal control system does not moderate the effect of total revenue on government expenditure.

3. METHODS

For the purpose of this study, the entire 16 local governments in Taraba State of Nigeria are considered as sample. Data for this study was gathered through secondary source for the period of 6 years ranging from 2010 through 2015. In essence, data on statutory allocation was collected from the official website of the Nigerian Ministry of Finance. However, data on internally generated revenue, expenditure, and internal control was collected from the annual accounts and reports of the 16 local governments in Taraba state. In the case of internal control system, the data was generated using content analysis. Content analysis is referring to as the coding and analyzing of textual or visual data to determine meaningful patterns, and it is a technique that summarizes any type of content by counting several parts of the contents (Weber, 1990). Notably, analyzing data through contents enable researchers to process large amount of data with relative affluence and in a more systematic fashion, and in analyzing the patterns and trends in documents (Stemler, 2001).

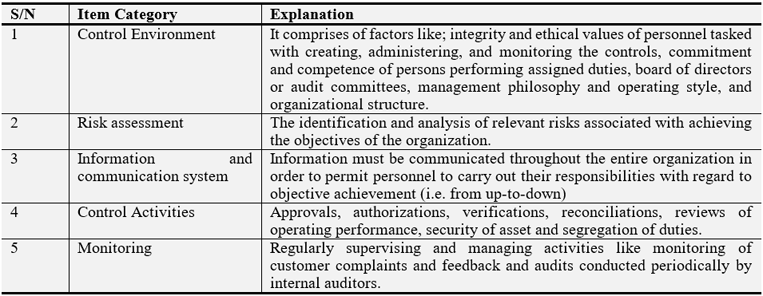

In this regard, a score index was developed for the components of internal control system. The index involves a 5-item category: control environment, risk assessment, information and communication system, control activities, and monitoring. Where a total score of ‘0’ indicates no Internal Control System (ICS) effectiveness, ‘1’ is very weak ICS effectiveness, ‘2’ is weak ICS effectiveness, ‘3’ is moderated ICS effectiveness, ‘4’ is strong ICS effectiveness, and ‘5’ is very strong ICS effectiveness. The score template is provided in the following table as thus:

Table-1. A Score Index for Internal Control System

Source: Designed by the authors for this study.

Moreover, explanations to the above are provide in Table 2, following Aikins (2011); Aldridge and Colbert (1994); Bowrin (2004); Karagiorgos et al. (2009); Ndungu (2013); Theofanis et al. (2011); Rezaee et al. (2001).

Table-2. Components of Internal Control as Score Index Explained

Source: Designed by the authors for this study.

For analysis purpose, this study utilizes descriptive statistics such as mean, frequencies, and standard deviation, inferential statistics such as the Pearson product-moment correlation (Pearson’s ‘r’) and Hierarchical multiple regression in answering the research questions for this study. The analysis was carried out using Statistical Package for Social Science (SPSS) package version 20.0. The models used in this study are specified as thus:

Multiple Regression Models (Before inclusion of moderating variable)

Expit = α0 + β1LIGRit + β2STALLit + εit

Where;

α = Constant

i = Local government

t = time period

εit = error term of local government i on time t

Expit = Government Expenditure

LIGRit = Local government IGR

STALLit = Statutory Allocation

Hierarchical Moderated Multiple Regression Model (with moderating variable):

The equation with the moderating and interaction variables is:

Expit = α0 + β1LIGRit + β2STALLit + β1LIGRit* ICSit + β2STALLit* ICSit + εit

Where;

α = Constant

i = Local government

t = time period

εit = error term of local government i on time t

Expit = Government Expenditure

LIGRit = Local government IGR

STALLit = Statutory Allocation

Moderating variable: ICS = Internal Control System.

4. RESULTS

4.1. Descriptive StatisticsTable 3 provides the descriptive statistics of the variables for this study. The result shows that government expenditure (EXP) has a mean value of 4.779 which indicates that the average spending of a local government in Taraba state is N4,779,000,000) annually. The minimum and maximum expenditures remained 2.957 (N2,957,000,000) and 8.202 (8,202,000,000) respectively, while the standard deviation stands at 1.173 (N1,173,000,000). This indicates that there is a wide variation in local governments’ spending in Taraba state, this may be due to the number of staff employed over various local governments in the state.

Moreover, the result also indicates that statutory allocations (STA) has a mean value of 2.017, that is N2,017,000,000 is the average amount of statutory allocation for a local government per annum in Taraba state. The minimum statutory allocation stands at 1.152 (N1,152,000,000), and the maximum is 3.132 (N3,132,000,000). The standard deviation is .448 (N448,000,000), meaning that the variation in statutory allocations between the 16 local governments in Taraba state is moderate.

Table-3. Descriptive Statistics

Note:EXP = Expenditure; STA = Statutory Allocation; and IGR = Internally Generated Revenue. The values are recorded in billions of Naira (Nigerian currency).

While the mean value for internally generated revenue (IGR) is .193 (N193,000,000) per local government per annum. The minimum and maximum IGR values are .050 (N50,000,000) and .337 (N337,000,000), whereas the standard deviation remains .008 (N8,000,000), meaning that there is minimum variation between the local governments in Taraba state in terms of generating IGR.

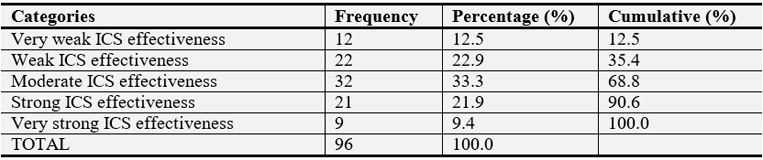

Nevertheless, in an attempt to determine the extent of implementing effective internal control system in the 16 local governments of Taraba state, the frequencies of the score index were presented under various titles as; very weak ICS effectiveness, weak ICS effectiveness, moderated ICS effectiveness, strong ICS effectiveness, and very strong ICS effectiveness. The frequencies are presented in Table 4 where the result depicts that ‘very strong ICS effectiveness’ appears 9 times (i.e. 9.4%), while ‘moderate ICS effectiveness’ has the highest appearances of 32 times (33.3%). In addition, ‘very weak ICS effectiveness’ appears 12 times (12.5%), ‘weak ICS effectiveness’ appears 22 times (22.9%), and ‘strong ICS effectiveness’ appears 21 times (21.9%). The result depicts that there is an average effectiveness of internal control system in local governments of Taraba state because amassing ‘strong and very strong ICS effectiveness’ will give 30 appearances (31.3%).

Table-4. Frequencies of Internal Control System (ICS) Effectiveness

Source: Authors’ Analysis (2016) from SPSS V.20 output

4.2. CorrelationIn order to determine the relationship between the variables in this study, a Pearson’s correlation analysis was conducted. The correlation result from Table 5 shows that the relationship between government expenditure (EXP) and statutory allocation (STA) is strongly positive with a coefficient value of 0.429 representing (42.9%) at 1% significant level. Meanwhile, internally generated revenue (IGR) is strongly positive related with expenditure (EXP) with a correlation value of 0.742 representing (74.2%) at 1% significance level. On the other hand, the moderating variable (internal control system, ICS) has a weak and positive relationship with government expenditure (EXP), having a correlation value of 0.234 representing (23.4%) at 5% significance level. However, statutory allocation (STA) has a strong positive relationship with internally generated revenue (IGR) with a correlation value of 0.453 (45.3%), whereas, STA has a moderate negative relationship with ICS with correlation value of -0.383 (-38.3%). On the other hand, internally generated revenue (IGR) has a weak positive relationship with ICS, having a correlation value of 0.240 (24.0%).

Table-5. Pearson Correlation Coefficient of the Variables

Note:**. Correlation is significant at the 0.01 level (2-tailed) *. Correlation is significant at the 0.05 level (2-tailed). EXP = Government Expenditure; STA = Statutory Allocation; IGR = Internally Generated Revenue; ICS = Internal Control System.

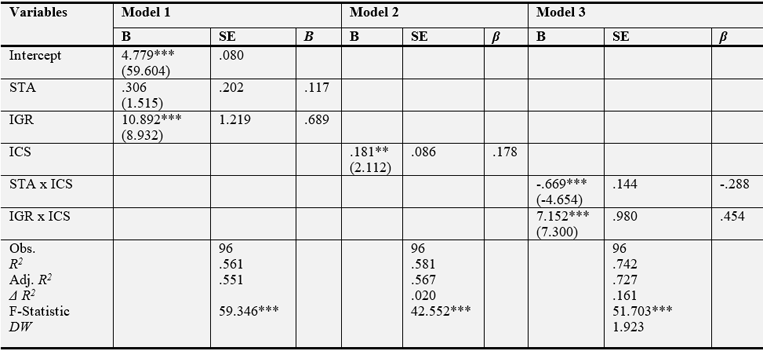

4.3. Regression AnalysisA 3 step hierarchical regression was conducted to ascertain the association between government expenditure as dependent variable, statutory allocation and internally generated revenue as independent variables, while internal control system moderates the relationship between the independent variables and the dependent variable. Step 1 includes only the independent variables (statutory allocation and internally generated) and the dependent variable (expenditure). In the second step, ICS as the moderator variable was entered to determine its significant direct impact on expenditure. While in step 3, the interaction terms of ICS with statutory allocation and ICS with internally generated revenue were entered (see Table 6).

The regression result in Table 6 reveals that in Model 1, statutory allocation and internally generated revenue contributed significantly to the regression model, F (2, 93) = 59.346, p< .001) and accounted for 55.1% of the variation in government expenditure. In Model 2, internal control system was entered, the result remains significance, F (3, 92) = 42.552, p<.001 and accounted for 56.7% variation in government expenditure. This shows that the moderating variable (internal control system) has significant impact on the dependent variable (government expenditure), and has fulfilled the step 2 of conducting analysis on moderation as opined by Baron and Kenny (1986). However, in Model 3, the interaction terms (that is, the products of moderating variable and the independent variables) are entered, where the result explained an additional 16.1% variation in government expenditure and this change in R2 (Δ R2) was significant, F (5, 90) = 51.703, p < .001. As such, internal control system moderates the effect of government revenue (STA and IGR) on expenditure as expected by hypothesis 2 of this study.

Table-6. Hierarchical Multiple Regression Result with Expenditure as Dependent Variable

Note:**p<.05; ***p<.001, t-statistics are in parentheses. STA = Statutory Allocation; IGR = Internally Generated Revenue; ICS = Internal Control System; DW = Durbin-Watson; Obs. = Observations.

4.4. DiscussionThe purpose of this study was to examine the relationship between the relationship between total government revenue (proxied by statutory allocation and internally generated revenue) and government expenditure moderated by internal control system. The result obtained in this study reveals that statutory allocation (STA) has a statistically and positive relations with government expenditure, r (96) = .429, p < .001. In the same vein, internally generated revenue (IGR) has a statistically significant relation with government expenditure, r (96) = .742, p < .001, meaning that an increase in total revenue of Taraba state government will leads to an increase in its expenditure. Moreover, the hierarchical multiple regression result reveals that an increase in statutory allocation by 1, will lead to an increase in government expenditure by .306 (unstandardized beta coefficient). Moreover, an increase in internally generated revenue by 1, will lead to an increase in government expenditure by 10.892 (unstandardized beta coefficient). In effect, this is consistent with the revenue-spend hypothesis of Friedman (1978) who reports that raising revenue will lead to more government spending, hence, leads to fiscal imbalances.

Moreover, the correlation result shows that internal control system is positively related to government expenditure, r (96) = .234, p < .05. Whereas, the regression result discloses that internal control system has significant direct impact on government expenditure, with unstandardized beta value of .181, p < .001. This has fulfilled the requirements of Baron and Kenny (1986) in testing moderations. In addition, the result of frequencies from Table 4 depicts that there is moderate internal control system effectiveness (33.3%), and this needs to be strengthen in order to boost revenue and control expenditure excesses. Additionally, the interaction terms of statutory allocation and internal control system have a statistical negative effect on government expenditure with unstandardized beta coefficient of -.669, p< .001. This is an indication that when internal control system moderate statutory allocation by 1, government expenditure will reduce by .669. However, the result reveals that the interaction terms of internally generated revenue and internal control system have a statistical positive effect on government expenditure with unstandardized beta coefficient of 7.152, p < .001. This means that as internal control system moderates internally generated revenue, government expenditure will increase.

5. CONCLUSION

The study makes an attempt to examine the relationship between the moderating effect of internal control system on the relationship between government revenue and expenditure in Taraba state of Nigeria. The study finds that Government revenue (statutory allocation and internally generated revenue) is highly related to government expenditure. But, statutory allocation unlike internally generated revenue has lower relationship with Taraba state government expenditure. This may be due to fluctuations in the allocations from federal government that heavily relies on oil monies, of which their sources are affected by the fluctuations and slashed in global oil prices. This means that most of the objectives of the government cannot be met due to shortage of funds, hence, may significantly affect the livelihood of the masses.

Moreover, the study reveals that internal control system is moderately applied in the overall sixteen (16) local governments of Taraba state. This may affect revenue generations of the government, and as well, leads to expenditure excesses of the government. Additionally, internal control system is found to be significantly related with government expenditure, thereby moderating relationships between government revenue (statutory allocation and internally generated revenue) government expenditure. As such, well-defined and implemented internal control effectiveness may have a significant impact on the way Taraba state government generates revenues and spend its resources.

Consequently, the study suggests that government should strategize ways or establish more mechanisms to improve revenue generation so as to meet its objectives of providing various services to the teeming population. Moreover, as government revenue has positive relation with its expenditure (moving in the same direction), fiscal imbalances may arise (Friedman, 1978) and may causes expenditure excesses. Therefore, government should try to balance between its revenue generation and its expenditure. There is also a need to put in place an effective internal control system that will conform to the components of effective internal control system which involve control environment, risk assessment, information and communication system, control activities, and monitoring. This will in a long way assist government in controlling its expenditures, which may lead to more savings, and may, engineered the government to be more focus on its objectives.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Abba, M., A.B. Bello and I.H. Bakari, 2008. An assessment of internally generated revenue in Kano State. Finance and Accounting Research Monitor, 2(1): 80-87.

Abba, M., A.B. Bello and S.A. Modibbo, 2015. Expenditure and internally generated revenue relation: An analysis of local governments in Adamawa State. Journal of Arts, Science and Commerce, 6(3): 67-77. View at Google Scholar

Adams, R.A., 2006. Public sector accounting and finance: Made simple, (Rev. Ed.), Lagos, Nigeria: Corporate Publishers Ventures.

Adejoh, E. and J.G. Sule, 2013. Revenue generation: It’s impact on government developmental effort (A Study of Selected Local Council in Kogi East Senatorial District). Global Journal of Management and Business Research Administration and Management, 13(4): 17-25. View at Google Scholar

Adenugba, A.A. and C.F. Ogechi, 2013. The effect of internal revenue generation on infrastructural development. A study of Lagos State internal revenue service. Journal of Educational and Social Research, 3(2): 419. View at Google Scholar | View at Publisher

Adesoji, A.A. and F.O. Chike, 2013. The effect of internal revenue generation on infrastructural development. A study of Lagos State internal revenue service. Journal of Educational and Social Research, 3(2): 419-436. View at Google Scholar | View at Publisher

Aikins, S., 2011. An examination of role of government internal audits' improving financial performance. Public Finance and Management, 11(4): 306-337. View at Google Scholar

Aldridge, R. and J. Colbert, 1994. Management's report on internal control, and the accountant's response. Managerial Auditing Journal, 9(7): 21-28. View at Google Scholar | View at Publisher

Baltaci, M. and S. Yilmaz, 2006. Keeping an eye on subnational governments: Internal control and audit at local levels. Washington, D: World Bank Institute.

Baron, R., M. and D.A. Kenny, 1986. The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6): 1173-1182. View at Google Scholar |View at Publisher

Bowrin, A.K., 2004. Internal control in Trinidad and Tobago religious organizations. Accounting, Auditing and Accountability Journal, 17(1): 121-152. View at Google Scholar | View at Publisher

Edogbanya, A. and G.S. Ja’afaru, 2013. Revenue generation: It’s impact on government developmental effort (A Study of Selected Local Council in Kogi East Senatorial District). Global Journal of Management and Business Research Administration and Management, 13(4). View at Google Scholar

Fadzil, F.H., H. Haron and M. Jantan, 2005. Internal auditing practices and internal control system. Managerial Auditing Journal, 20(8): 844-866.View at Google Scholar | View at Publisher

Fayemi, O.A., 1991. Principle of local government accounting. Yaba – Lagos: Chapter Ten Publication Ltd.

Friedman, M., 1978. The limitations of tax limitation. Policy Review, 5: 7. View at Google Scholar

Garko, S.J., 2009. An assessment of internally generated revenue in Kano State. Nigerian Journal of Accounting and Finance, 1(2): 85-94. View at Google Scholar

Hamid, K.T., 2008. SWOT analysis on sources of revenue at state government level. A Paper Presented at the Bi- Annual Conference of the Federal and State Auditors- General Held at Tahir Guest Palace, Kano.

Karagiorgos, T., G. Drogalas, Ε. Gotzamanis and I. Tampakoudis, 2009. The contribution of internal auditing to management. International Journal of Management Research and Technology, 3(2): 417-427. View at Google Scholar

Mbedzi, E. and T. Gondo, 2010. Fiscal management in Dangila municipality, Ethiopia. Performance and policy implications. Theoretical and Empirical Research in Urban Management, 14: 95. View at Google Scholar

Muhammad, I.M., 2012. The impact of skilled personnel on effective internal revenue generation in selected local governments in Yobe State. Nigerian Accounting Horizon, 5(1): 75-90.

Muhammed, A. and M. Asfaw, 2014. Government expenditure management and control in Ethiopia. Research Journal of Finance and Accounting, 5(11): 84-92.

Ndungu, H., 2013. The effect of internal controls on revenue generation: A case study of the university of Nairobi enterprise and services limited. A Project for the Award of a Degree in Master of Science Finance, University of Nairobi, Reg. No.: D63/67044/2011.

Obioma, E.C. and U.M. Ozughalu, 2015. Industrialization and economic development: A review of major conceptual and theoretical issues. In Challenges of Nigerian Industrialization: A Pathway to Nigeria Becoming a Highly Industrialized Country in the Year 2015, Selected Papers for the Annual Conference of Nigerian Economic Society (NSE).

Ola, R.O. and D.A. Tonwe, 2005. Local administration and local government in Nigeria. Lagos: Amfitop Nig Ltd.

Oladoyin, M.A., O.D. Elumilade and O.T. Ashaolu, 2005. Transparency, accountability and ethical violations in financial institutions in Nigeria. Journal of Social Science, 11(1): 21-28. View at Google Scholar

Olusola, O.O., 2011. Boosting internally generated revenue of local governments in Ogun State, Nigeria (A Study of Selected Local Governments in Ogun State). European Journal of Humanities and Social Sciences, 8(1): 336-348. View at Google Scholar

Oseni, M., 2013. Internally generated revenue (IGR) in Nigeria: A panacea for state development. European Journal of Humanities and Social Sciences, 21(1). View at Google Scholar

Rezaee, Z., R. Elam and A. Sharbatoghlie, 2001. Continuous auditing: The audit of the future. Managerial Auditing Journal, 16(3): 150-158. View at Google Scholar | View at Publisher

Sani, A., 2005. Contentious issues in tax administration and policy in Nigeria: A governor’s perspective, first national retreat on taxation. Lagos: Joint Tax Board.

Stemler, S., 2001. An overview of content analysis. Practical Assessment, Research & Evaluation, 7(17): 137-146. View at Google Scholar

Theofanis, K., G. Drogalas and N. Giovanis, 2011. Evaluation of the effectiveness of internal audit in Greek hotel business. International Journal of Economic Sciences and Applied Research, (1): 19-34. View at Google Scholar

Ukah, O.C., 2009. Government expenditure management and control within the framework of Ethiopian economy. African Research Review Journal, 3(1). View at Google Scholar | View at Publisher

Weber, R.P., 1990. Basic content analysis (No. 49). USA: Sage University Press.

Yunusa, A.A., 2009. An assessment of internal revenue generation capacity of local governments in Nigeria. Nigerian Journal of Accounting and Finance, 1(2): 51-68.