EFFECT OF DISAGREEMENT ON CORPORATE FINANCING POLICY AND INVESTMENT LEVEL

International School of Business, Beijing International Studies University, Beijing, China

ABSTRACT

This study models firm’s financing policy and investment level when manager and outside investors has disagreement. It shows that the firm is more likely to over invest when the level of disagreement is high, and prefers debt financing; while under invests with lower disagreement level and tends to equity financing. Compared with self-financing, investment at firm level decreases, the over (under) investment level also declines and the threshold of disagreement rises when the firm chooses external financing. The numerical simulation also verifies the theoretical findings.

© 2017 AESS Publications. All Rights Reserved.

Keywords:Disagreement, Heterogeneous beliefs, Debt financing, Share issuance, Over investment, Under investment.

ARTICLE HISTORY: Received:10 November 2016 Revised:6 December 2016 Accepted:27 December 2016Published:10 January 2017

Contribution/ Originality:: In the circumstances of disagreement between manager and outside investors, the paper theoretically find that firm prefers debt financing and more likely to over invest with higher disagreement level. Compared with self-financing, total investment and over (under) investment level declines, and the threshold of disagreement rises when choosing external financing.

1. INTRODUCTION

Difference in opinion among market participant is one of the natures of financial market. Hong and Stein (2007) summarize three mechanisms that form disagreement, i.e. graduation information flow, limited attention and heterogeneous priors. Plenty of literatures have proved that heterogeneous beliefs among investors will cause asset prices deviating from its fundamental value, managers then take advantage of the situation in the form of market timing or catering, hence affect firms’ financial policies. While managers may also be more optimistic of the assets’ future payoff, overconfident of their capabilities and prefer empire building to fulfill personal achievement etc., together with the existence of information asymmetry, these will definitely cause disagreement with outside investors on firms’ market value or future payoff, thus influence firms’ financial policies as well. Related researches are as follows.

In financing area, Baker and Wurgler (2002) empirically find that capital structure is the cumulative outcome of past attempts to time the equity market. Bigus (2003) finds that mixed debt-equity financing outperform both pure debt and pure equity if investors have more pessimistic beliefs than entrepreneurs on firm’s future returns. Fairchild (2005) demonstrates that the effect of overconfidence is ambiguous in the moral hazard model as it has a positive effect by inducing higher managerial effort but may lead to excessive use of debt. Dittmar and Thakor (2007) predict that managers use equity to finance projects when they believe that investors’ views about project payoffs are likely to be aligned with theirs, thus maximizing the likelihood of agreement with investors, otherwise they use debt. Lee (2009) shows that poor accounting information quality is associated with higher flotation costs in terms of larger underwriting fees, larger negative seasoned equity offerings (SEO) announcement effects, and a higher probability of SEO withdraws. Yang (2013) builds a dynamic trade-off model of corporate financing with differences in belief between manager and outside investors, and finds that the optimal leverage not only depends on differences of opinion but also differ significantly from that in standard trade-off models. Wang et al. (2013) analyze the impact of heterogeneous beliefs and short sale constraints on security issuance decisions, and find that the increase in heterogeneity in investors’ beliefs results in an increased likelihood of equity issuance over debt when public signal is favorable. In general, disagreements do have significant influence on firm’s financing choice.

As for firm’s investment, most literatures build on manager’s irrational bias, overconfidence in particular. Roll (1986) is one of the first papers to explicitly introduce overconfidence into a corporate-finance context, and argues that managerial “hubris” can explain a particular form of over-investment, namely overpayment by acquiring firms in takeovers. Heaton (2002) thinks that managerial over-confidence can lead managers to be less disciplined about capital outlays when they perceive they have resources to spare. This is consistent with Myers and Majluf (1984) view, i.e. there will be little external equity financing, and investment will increase with internal resources. Malmendier and Tate (2005) provide evidence linking corporate investment to overconfidence on the part of CEOs, and also find that investment is particularly sensitive to cash flow when resources are relatively constrained. Ben-David et al. (2007) find that firms with over-confident CFOs tend to adopt lower return investment projects, pay dividends less often, and repurchase stock more frequently than do other firms. Shibata and Nishihara (2010) show that manager-shareholder conflicts over-investment policy increase not only the investment and default triggers but also coupon payments, which lead to a decrease in the equity value; while debt financing increases investment and decreases total social welfare; thus, there is a trade-off between the efficiency of investment and total social welfare with debt financing. Smith (2014) supports the hypothesis that low disagreement followed by high investment. Baker et al. (2016) demonstrate that the impact of investors’ heterogeneous beliefs on aggregate consumptions and investment is consistent with business cycle.Some other researches pay attention to firm’s payout policy. For instance, Chen and Liu (2007) develop a model regarding an optimal investment-payout policy to maximize a firm’s value with divergent types of shareholders, and show that an optimal payout policy does exist under a heterogeneous beliefs framework. However, they didn’t take disagreement and firm’s financing into consideration. Thanatawee (2011) shows that paying dividends is a dominated strategy for the high-quality firm when there are information asymmetry and moral hazard, there exists a separating equilibrium in which the high-quality firm invests in new project while the low-quality firm pays dividends in efficient market, and vice versa if investors under react to share repurchase announcements. Banerjee et al. (2013) find that overconfident CEOs tend to over-estimate their firm’s cash flows and under-estimate the underlying risk, hence their repurchase activities are mainly motivated as a way to correct this “perceived” under-valuation of their company’s float, rather than a way to return any excess cash to shareholders. This paper will analyze the effect of disagreement between manager and investors on corporate financing policy and investment level under the general equilibrium framework. More specifically, the optimal investment amount under circumstances of self financing and external financing will be modeled respectively, and then discuss disagreement’s impact on firm’s investment level and financing choice. The rest of the paper proceeds as follows. Section 2 describes the basic assumptions. Section 3 analyzes the investment level with self financing. Section 4 discusses firm’s investment amount and financing choice with external financing. Section 5 provides numerical simulation to prove the models’ results. Section 6 presents our conclusions.

2. BASIC ASSUMPTIONS

The basic assumptions are as follows.

3. INVESTMENT LEVEL WITH SELF FINANCING

If the firm has enough cash flow, the investment demand can be self financed. Since manager and outside investors are risk sharing and the aim is to maximize firm value, the simple social welfare function is a suitable way of portraying the objective, which is to attach weights to the interests of each group proportional to the values of their holdings.

4. SECURITY ISSUANCE AND INVESTMENT LEVEL WITH EXTERNAL FINANCING

This section will discuss the situation when the firm chooses external debt financing and equity financing respectively.

(4) Compared with the results in Section 3, it can be implied that firm’s investment amount and over (under) investment level with external financing is lower than that of self financing, while the threshold of disagreement level increases to some extent. This means that when there are more outside investors, firm’s investment level tends to be reasonable and disagreement’s effects on firm’s financial policies decrease.

5. NUMERICAL SIMULATION

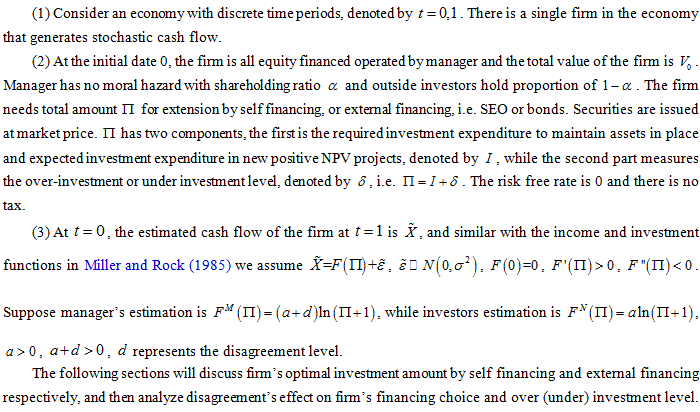

Fig-1. Total investment amount with disagreement under self financing

Fig-2. Over (under) investment level with disagreement under self financing

Fig-3. Firm’s expected value with disagreement under self financing

Fig. 1 and Fig. 3 show that firm’s total investment amount and expected value increase with the disagreement level under self financing. Fig. 2 indicates that if the disagreement between manager and investor exceed some level, the firm will have tendency towards over-investment, and vice versa.

Fig-4. Total investment amount with disagreement under external financing

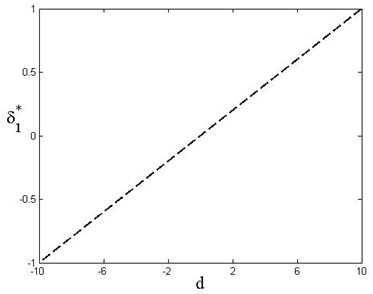

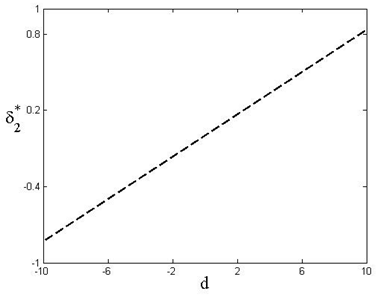

Fig-5. Over (under) investment level with disagreement under external financing

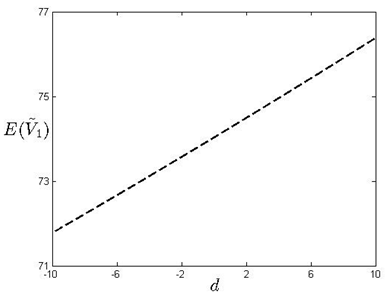

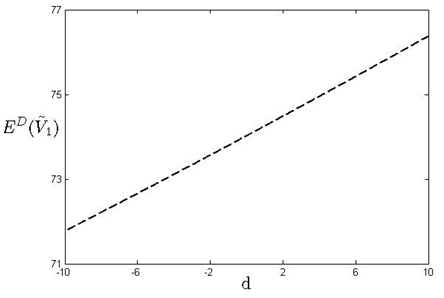

Fig-6. Firm’s expected value with disagreement under external debt financing

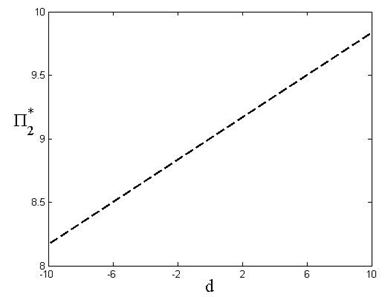

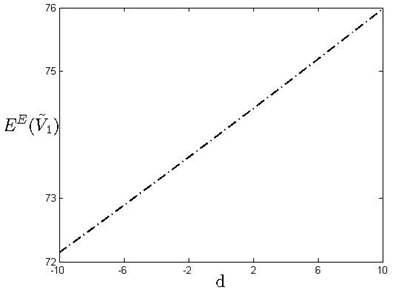

Fig-7. Firm’s expected value with disagreement under external equity financing

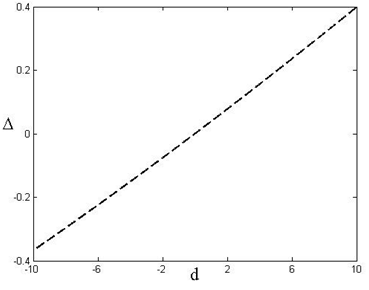

Fig-8. Difference between firm’s expected value with disagreement under external financing

Compared with self financing, Fig. 4, Fig. 6 and Fig. 7 show that firm’s total investment amount and expected value increase with the disagreement level under external financing. Fig. 5 also indicates that if the disagreement between manager and investor exceed some level, the firm will have tendency towards over-investment, and vice versa. According to Fig. 8, if d>0, i.e. investors are more pessimistic, firm’s expected value under debt financing is lower than equity financing, which makes the latter a better option. While if d>0, i.e. investors are more optimistic, manger may prefer debt financing since firm’s expected value under debt financing is higher than equity financing.

6. CONCLUSIONS

This paper models disagreement’s effect on firm’s financing choice and investment level. Based on the analysis of firm’s optimal investment amount with self financing and external financing respectively, we find that if there is a higher the disagreement level, the firm will have a tendency towards over investment. In contrast, with a lower disagreement level, the firm may under invest. Besides, the extent of disagreement’s impact is related with manager’s shareholding proportion.

Similar to the current research outputs, when the firm needs external financing, if the disagreement between manager and investor exceed some level, the firm will have tendency towards debt financing, otherwise, the firm will prefer equity financing.

Compared with self financing, firm’s investment amount and over (under) investment level with external financing is lower, while the threshold of disagreement level increases to some extent. This means that when there are more outside investors, firm’s investment level tends to be reasonable and disagreement’s effects on firm’s financial policies decrease. The numerical simulation also verifies the model’s theoretical findings.

Future research can also extend the analysis by discussing firm’s financial policies with bankruptcy and financing costs, as well as manager’s moral hazard.

| Funding: This work is supported by the Scientific Research Project Foundation of Beijing International Studies University (Grant No. 212016). |

| Competing Interests: The author declares that there are no conflicts of interests regarding the publication of this paper. |

REFERENCES

Baker, M. and J. Wurgler, 2002. Market timing and capital structure. Journal of Finance, 57(1): 1-32.View at Google Scholar

Baker, S.D., B. Hollifield and E. Osambela, 2016. Disagreement, speculation, and aggregate investment. Journal of Financial Economics, 119(1): 210-225. View at Google Scholar | View at Publisher

Banerjee, S., M. Humphery-Jenner and V. Nanda, 2013. CEO overconfidence and share repurchases. UNSW Australian School of Business Research Paper No. 2013 BFIN 04, 26th Australasian Finance and Banking Conference.

Ben-David, I., J.R. Graham and C.R. Harvey, 2007. Managerial overconfidence and corporate policies. NBER Working Paper No. 13711.

Bigus, J., 2003. Heterogeneous beliefs, moral Hazard, and capital structure. Schmalenbach Business Review, 55(2): 136-160.View at Google Scholar

Chen, C.J. and V.W. Liu, 2007. Investment policy with heterogeneous beliefs of investors. Economics Letters, 94(3): 356-360. View at Google Scholar | View at Publisher

Dittmar, A. and A. Thakor, 2007. Why do firms issue equity? Journal of Finance, 62(1): 1-54.View at Google Scholar | View at Publisher

Fairchild, R.J., 2005. The effect of managerial overconfidence, asymmetric information, and moral Hazard on capital structure decisions. Institute of Chartered Financial Analysts of India (ICFAI) Journal of Behavioral Finance, 2(4): 46-68. View at Google Scholar

Heaton, J.B., 2002. Managerial optimism and corporate finance. Financial Management, 31(2): 33-45. View at Google Scholar | View at Publisher

Hong, H. and J.C. Stein, 2007. Disagreement and the stock market. Journal of Economic Perspectives, 21(2): 109-128.View at Google Scholar | View at Publisher

Lee, M., 2009. Seasoned equity offerings: Quality of an accounting information and expected flotation costs. Journal Financial Economics, 92(3): 443-469.

Malmendier, U. and G. Tate, 2005. CEO overconfidence and corporate investment. Journal of Finance, 60(6): 2661-2700. View at Google Scholar | View at Publisher

Miller, M.H. and K. Rock, 1985. Dividend policy under asymmetric information. Journal of Finance, 40(4): 1031-1051. View at Google Scholar | View at Publisher

Myers, S. and N. Majluf, 1984. Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2): 187-221. View at Google Scholar | View at Publisher

Roll, R., 1986. The hubris hypothesis of corporate takeovers. Journal of Business, 59(2): 197-216.View at Google Scholar | View at Publisher

Shibata, T. and M. Nishihara, 2010. Dynamic investment and capital structure under manager-shareholder conflict. Journal of Economic Dynamics & Control, 34(2): 158-178.View at Google Scholar | View at Publisher

Smith, J., 2014. Does the market matter for more than investment? Journal of Empirical Finance, 25: 52-61.View at Google Scholar | View at Publisher

Thanatawee, Y., 2011. Payout policy and real investment under asymmetric information. International Journal of Economics and Finance, 3(5): 250-261. View at Google Scholar | View at Publisher

Wang, Y., F. Xu and A. Hu, 2013. Impact of heterogeneous beliefs and short sale constraints on security issuance decisions. Economic Modelling, 30: 539-545.View at Google Scholar | View at Publisher

Yang, B., 2013. Dynamic capital structure with heterogeneous beliefs and market timing. Journal of Corporate Finance, 22: 254-277. View at Google Scholar | View at Publisher