ECONOMETRIC ANALYSIS OF EXCHANGE RATE AND EXPORT PERFORMANCE IN A DEVELOPING ECONOMY

1Adjunct Faculty, SDMIMD, Mysuru, India, Department of Accounting, Banking and Finance, Baze University Abuja, Nigeria

ABSTRACT

The study investigated the causal relationship between currency exchange rate (EXR) and export growth (EXP) in Nigeria, Africa’s largest economy and most populous nation. The study used econometric tools for the analysis based on statutory annual data over the period 1970s-2014. It is shown that EXR and EXP are not co-integrated and, hence, a long-run equilibrium relationship may not exist between them. The Granger causality test shows significant absence of short-run nexus between EXR and EXP, but there is a unidirectional causality running from EXR to EXP with no feedback. It is inferred that while the EXR may have significant impact on EXP, EXP in a single commodity (crude oil)-dependent economy like Nigeria, may have very little impact on EXR. Thus, the long-held thesis that if you devalue the currency, you will export more is not empirically supported in the Nigerian case. The implications of these findings for sustainable fiscal policy development and some suggestions for future research are discussed.

© 2017 AESS Publications. All Rights Reserved.

Keywords: Export drive, Financial econometrics, Foreign exchange management, Nigeria, Public finance.

JEL Classification: C10, 58, D51, F43, H1, Z18.

Received: 6 May 2016/ Revised: 17 November 2017/ Accepted: 5 December 2016/ Published: 10 January 2017

Contribution/ Originality

This study documents the causal linkages between foreign exchange rate management and export performance in an emerging market economy and the policy implications for sustainable private sector development. Empirical evidence is provided on the limitation of exchange rate policy to drive export growth in a peculiar developing economy like Nigeria.

1. INTRODUCTION

Goods produced domestically and sold abroad are called exports (Mankiw, 2004). The exchange rate of a currency is its value in terms of another currency or a group of currencies (Barro and Grilli, 1994; Shettima, 2016). It is one of the many prices in the global market for financial assets. In the case of the Naira (Nigeria), the United States dollar (USD) is the commonest benchmark currency. Foreign exchange management is described as a technique that involves the generation and disbursement of foreign exchange (forex) resources so as to reduce destabilizing short-term capital flows (Fapetu and Oloyede, 2014). A country is generally speaking at liberty to fix or float its currency in line with its economic management philosophy or principles – ‘fixed’, ‘market-driven’ or ‘managed float exchange rate fixing system’. However, discerning government tries to monitor the use of scarce forex resources so that the utilization fits into the overall economic management priorities, notably, building up forex reserves to prevent balance of payment problems, and full employment and shared prosperity. To that end, a productive real sector actively in global business is imperative, but, consensus is currently lacking specifically on the impact of exchange rate system on export growth, particularly in a transitional economy like Nigeria. Meanwhile, due largely to decreased revenues resulting from falling oil prices, corruption, and security challenges, Africa’s largest economy, Nigeria, is currently suffering its worst economic crisis in decades, perhaps surpassing the effects of the global financial crisis of 2008. In the emerging scenario of dwindling financial resources, the question of foreign exchange management arises, considering that exchange rate is a pivotal factor in export performance. Some analysts believe that market-driven exchange rate policy has been having undesirable influence on the trend in agricultural share of GDP in Nigeria and that it is imperative for government to fix the rate in order to improve the supply of exports (Oyinbo et al., 2014); others opine differently.

The issues involved in exchange rate management, export performance and international trade can be complicated, particularly in the context of developing economies like Nigeria (Mbah, 2016; The Guardian (Editorial), 2016). International trade can make some businesses worse-off, even as it makes the economy as a whole better-off (Mankiw, 2004). For instance, when Nigeria exports crude oil and imports refined petroleum, the impact on the ordinary Nigerians is not the same as the impact on a Nigerian refined oil importer. Thus, the question of exchange rate and export growth borders on sustainable economic management and this has substantial implications for the development of private wealth, real estate and financial assets (Piketty, 2014). Amidst the debates on the utility of exchange rate policy in driving export growth, there seems to no consensus on the postulate that the Nigerian export potentialities are insulated from the level of exchange rate of the Naira to the dollar. It has been asserted that Naira is largely delinked from the productive capacity of the real sector resulting in the Naira exchange rate being adjudged to be “misaligned” (Shettima, 2016). Nonetheless, the possibility of the presence of negative relationship between EXR and EXP growth (as a proxy for productive capacity of the real sector) has led to the emergence of the issue of causality. Does depreciation or devaluation in the international value of Naira (EXR) lead to rapid growth of export performance (EXP), or does growing export (EXP) have any positive effect on Naira value (EXR)? Neither of these possibilities can be ruled out, hence the need for empirical studies on the subject.

Against this background, this research study was designed to investigate the impact of EXR on EXP in Nigeria over a period of 44 years, 1972 – 2015. The study contends that export performance plays a significant role in achieving a sustainable foreign exchange management of any nation especially given today’s era of increasing globalization. The Vector Error Correction Model (VECM) is first used to estimate the model. Granger Causality test is thereafter applied to identify the presence or otherwise of causality between the two financial time series.

1.1. Significance of Study

The sustainability of Naira exchange rate has received renewed attention in recent times because of the increased volatility of oil prices and depreciation in the value of Naira (Shettima, 2016). Despite various efforts by the government aimed at achieving stable EXR, the Naira has consistently depreciated against the US dollar from the 1980s to date. Thus, the exchange rate issue and performance of export to improve on balance of payments have become paramount for the new administration in Nigeria which seems poised to effect positive ‘changes’ in the economy through concerted diversification away from over-dependence on the volatile oil revenue.

Also, while the vast majority of empirical evidence has touched on sustainability of EXR or EXP in relation to such macroeconomic factors as inflation, interest rate, and Foreign Direct Investment (FDI), it is worth noting that little or no specific investigation of the critical relationship between EXR and EXP growth in the Nigerian context. Domestically, there is a dearth of significant academic work that has critically examined the relationship between EXR and EXP, whereas sound economic management policy on such critical resources as foreign exchange should be based on reliable and up-to-date data and rigorous analysis.

It is against the backdrop that this research study was designed to extend the empirical investigation to the causal analysis of EXR and EXP growth in a developing, oil-exporting economy like Nigeria. Given the highly volatile attributes of global crude oil markets and the potential risk of volatility spillovers of such economies for today’s globally integrated markets, the econometric review is of particular interest for asset managers and policy makers.

This paper consists of five broad sections. The paper begins with this introduction. The conceptual review and highlights of significant studies related to the subject with emphasis on the Nigerian context are presented in the second section. The third section deals with the methodology adopted for the research, describing the essential parameters of the econometric models and techniques, while the fourth section presents the results of the empirical tests to draw appropriate inferences. The paper ends with a summary of the findings, a few policy implications and some suggestions for future studies.

2. REVIEW OF RELEVANT LITERATURE

2.1. Theoretical Basis of the Study

There are many theoretical explanations or perspectives to EXR and EXP which are documented in the literature (Rates, 2016). These include asset approach, portfolio balance theory, central bank sterilization, the roles of news, currency union, and trade balance hypothesis. There has also been emphasis on globalization and financial liberalization theories, among others. Basically, the present contribution is based on the trade balance theory which explains that the intrinsic value of currency or its spot exchange rate is largely based trade flows. A positive balance is known as a trade surplus if it consists of exporting more than it is imported, while a negative balance connotes a trade gap with impact on currency value (Sims, 2014).

2.2. Foreign Exchange Management in Nigeria in Brief

Exchange rate is the price of one country’s currency in relation to another country’s, which is a key variable for robust economic management in every nation (Oloyede, 2002; Fapetu and Oloyede, 2014). It is one of the many prices in the global market for financial assets. Nigeria shifted from fixed exchange rate regime to flexible exchange rate in 1986; consequently, exchange rate of the Naira is presumably left to determination by market forces (Adeniran et al., 2014). Between 1960 and 1986, the fixed exchange rate system was operated. What is prevalent in practice as of now is regarded as dual exchange rate system (Shettima, 2016). Generally, EXRs are difficult to forecast because the forex market is constantly reacting to unexpected news or events.

2.3. Economic Diversification through Enhanced Export Performance

A truly diversified Nigerian economy can widen sources of foreign exchange earnings to remove pressure on the Naira. The prospects of such export-oriented diversification has been documented to include modernization of agriculture, mining, petrochemical industry, energy and education that is focused on science, technology, engineering, mathematics and the creative industry (Tella, 2016). The development of the real sector businesses is reckoned to save trillions of Naira in yearly imports of items such as raw materials that are producible within the domestic economy thereby saving the country the equivalent in foreign exchange requirements (Okere, 2016).

The two major types of exports are ‘manufactured goods’ and ‘raw materials’, the former being the more commonly used to achieve export-led growth (ELG). According to the latest statistics from the National Bureau of Statistics (NBS) (2016) the largest product exported by Nigeria in 2015 was “Mineral products” which accounted for $43 billion or 88.1 percent of the total exports for the year. Exports by continent, showed that Nigeria mainly exported goods to Europe and Asia (notably, India, Spain, and The Netherlands), which accounted for $19.3 billion or 39.7 percent and $14.7 billion or 30.3 percent respectively, of the total export value for 2015. Furthermore, Nigeria exported goods valued at $7 billion or 14.4 percent to the continent of Africa while export to the ECOWAS (West Africa) region totalled $3 billion.

Also, in the Nigerian context, there is a categorization of exports into ‘oil exports’ and ‘non-oil exports’: The main products included in non-oil exports include cotton lint, fermented cocoa bean and goat skin leather which are exported to Malaysia, The Netherlands and Italy respectively (Central Bank of Nigeria [CBN], 2010). In the early 50s / 60s, prior to the ‘oil boom’ of the 70s, Nigeria’s man forex earnings were ground nuts, cotton, cocoa, palm kernel and rubber and all agro/forest resources.

2.4. Export-Led Growth (ELG)

Export-led growth (ELG) denotes a trade and economic policy directed at speeding up the industrialization process of a country by exporting goods for which the nation has a comparative advantage (Oloyede, 2002). China is regarded as a classic example of ELG economy generating US$ 2.9 trillion in output annually versus $2.43 trillion from the US (Sims, 2014). However, as Gibson and War (1992) assert, ELG is not a one-sided affair; it also implies opening domestic markets to foreign competition in exchange for market access in other countries. In this respect, a floating exchange rate mechanism (that may mean devaluation of the national currency) is often employed to facilitate exports, increase employment and overall economic development, but the utility of this mechanism is thought to be unworkable in developing economies like Nigeria which are deficient in real, globally competitive export base, hence the investigation contemplated by this research work.

2.5. Empirical Review of Exchange Rate and Export Growth

It is observed that quantitative analysis of the role of export performance in achieving sustainable exchange rate of the Naira (EXR) has received relatively less attention from researchers. Admittedly, a series of recent academic papers have touched on sustainability of EXR in relation to such factors as FDI, inflation, interest rate, and similar macroeconomic variables, but it is worth noting that little or no emphasis has been given to the critical relationship between EXR and EXP growth in the Nigerian context. Some research has indicated that exchange rate is significant in influencing not only export growth (Omojimite, 2012) indeed several other economic sectors, interest rate, inflation, FDI, and agricultural production (Chukuigwe and Abili, 2008; Alao, 2010; Wafure and Nurudeen, 2010; Enoma, 2011; Ajide, 2014) but EXP growth as a variable was excluded from many of these investigations, hence the present attempt to fill-in the gap. It is further observed that many of the past studies harped on the agricultural sector as the largest employer of labour in Nigeria.

There are perhaps two schools of thoughts concerning the influence of exchange rate on export growth and this may be due to variations in data periods, analytical models and estimation methods. One school of thought argued that fixed exchange rate policy is significant in influencing export growth while the other school of thought postulated that market-driven exchange rate policy was significant in influencing export growth (Amassona et al., 2011). Some analysts believe that market-driven exchange rate policy has been having undesirable influence on the trend in agricultural share of GDP in Nigeria and that it is imperative for government to fix the rate in order to improve the supply of exports (Oyinbo et al., 2014). Other researchers like Chidi and Godwin (2015) sought to model the volatility of the NGN/BPS (Nigerian Naira and the British Pounds Sterling) exchange rate using variants of the GARCH models both Symmetric and Non-Symmetric under different distributional assumptions. The research basically aimed at forecasting ability of the different models which were compared to identify which of the models perform better.

Interestingly, Oyinbo et al. (2014) examined the causal relationship between exchange rate deregulation and the agricultural share of the GDP in Nigeria from an econometric perspective, using time series data spanning a period of 26 years, 1986 – 2011. Data on EXR and GDP were analyzed using Augmented Dickey Fuller unit root test, unrestricted vector auto regression, pair-wise granger causality and vector error correction model. The authors’ results showed the existence of unidirectional causality from exchange rate to agricultural share of GDP and also exchange rate deregulation had negative influence on agricultural share of GDP in Nigeria.

Similarly, Obinwanne et al. (2015) examined EXR and economic growth in Nigeria using Granger causality approach. The paper attempted to model the Nigerian economy as a function of exchange rate and other macroeconomic variables deploying Unit root and Cointegration tests to determine the suitability of the variables. The Vector Autoregressive (VAR) model was used to estimate the model. Granger Causality is used to identify the presence or otherwise of causality among the variables. Also, Adeniran et al. (2014) examined the impact of EXR on the same economic growth in Nigeria from 1986 to 2013 using the correlation and regression analysis of the ordinary least square (OLS) to analyze the data. The result of the work showed that EXR had no significant impact on national economic growth. In the same vein, Fapetu and Oloyede (2014) examined EXR and the Nigerian economic growth from 1970-2012 using CBN data and OLS estimation techniques with error correction model framework, and found out that EXR was not statistically significant.

Ewetan and Okodua (2013) examined the applicability of the Export-Led Growth (ELG) hypothesis for Nigeria using annual secondary time series data on the country’s exports and GDP growth from 1970-2010. The estimation results obtained from the co integration test and granger causality test within the framework of a VAR model did not support the Export-Led Growth hypothesis for Nigeria. The paper concluded that government must diversify the productive base of the economy, promote non-oil exports, and build up an efficient service infrastructure to drive private domestic and foreign investment.

Even in other emerging markets like India, less attention has also been paid to the question of EXR and EXP growth. Raghul and Hariharan (2015) investigated EXR volatility in Indian firms and documented a lengthy list of factors affecting EXR, but EXP was not featured. Similarly, recent contributions from other researchers such as Venkatraja (2015) and Venkatraja and Sriram (2015) have only Granger-tested FDI, capital formation and the GDP in Indian context, indicating that academic inquiry into the actual nexus between EXR and EXP may be a relatively new area of research.

2.6. Research Gap

Perhaps, it can be easily noticed from the foregoing review of the concerning literature that quantitative analysis of the role of EXR in ELG theory has received relatively less attention from researchers. Admittedly, a series of recent papers have touched on sustainability of EXR in relation to such factors as FDI, inflation, interest rate, and similar macroeconomic variables, but it is worth noting that little or no emphasis has been given to the critical relationship between EXR and EXP growth in the Nigerian context. Notably, EXR was peripheral to the inspiring work of Ewetan and Okodua (2013) on EXP and GDP. Even then, the empirical evidence on the causal linkages between severally investigated key variables and economic growth is mixed and warrant in-depth investigation especially in the context of emerging economies. The present contribution is expected to rekindle research interest in this direction for purpose of achieving greater stability and sustainability in foreign exchange management in Nigeria through internationally competitive productivity in Nigeria. It is hypothesized that there is no causal relationship between exchange rate (EXR) and export growth (EXP) in Nigeria.

The import of the present research study is thus to explore the causal link between EXR and EXP growth in Nigeria. The specific objectives are:

- To assess the dynamics of short-term linkages between EXR and EXP growth.

- To explore the presence of long-term equilibrium relationship between EXR and EXP growth.

- To capture the linear inter-dependence between the variables under study in the Nigerian context.

3. METHODOLOGY

Exchange rate of Naira to the US dollar (EXR) and total value of exports (EXP) form the two main variables for the empirical causality analysis. The empirical analysis was based on time series for the period from 1972 to 2015, that is, annual observations of 44 years of secondary data sourced primarily from the various issues of Central Bank of Nigeria Bulletin and National Bureau of Statistics (NBS) which publishes Trade statistics report quarterly. Trade statistics compilation by NBS is largely from secondary data sources. Based on NBS (2016) the data sources for the compilations include: The Nigerian Customs through the Nigeria Integrated Customs Information System (NICIS), Nigerian National Petroleum Corporation (NNPC) and various oil companies in the upstream and downstream sectors of the oil industry, Nigerian Ports, Petroleum Products Pricing and Regulatory Agency, Nigeria Liquefied Natural Gas Ltd and Central Bank of Nigeria. The Standard International Trade Classification (SITC) was used to categorize trade items, while validation, quality assurance, processing and analysis of the primary data are as detailed in NBS (2016).

Data were processed and analyzed by applying econometric tools and techniques supported by EViews statistical package. The analysis comprised of (i) testing the stationarity of data using graphical analysis combined with Augmented Dickey Fuller (ADF) Unit Root Test Method, (ii) testing the co-integration between EXR and EXP growth rate by administering Johansen’s Co-integration Test (JCiT), (iii) fitting a vector error correction model (VECM) if co-integration was established, and (iv) proceeding to testing the presence of causal relationship between EXR and EXP by administering the Granger Causality Test (GCT) upon confirmation of variables being co-integrated. Data visualization by way of line graphing provided an initial clue regarding the likely nature of the series. The above-stated tests were conducted following the standard procedure and decision rules indicated in the literature (Dickey and Fuller, 1981; Engle and Granger, 1987; Granger, 1988; Gujarati and Sangeetha, 2007; Ray, 2012) briefly described below:

After getting an initial feel on the possible nature of the time series between EXR and EXP growth rate, the study proceeded with the next test of stationarity based on Unit Root Test using the ADF which basically consisted of estimating the following regression:

+

+ +

+  … (1)

… (1)

where,  represents the time series to be tested,

represents the time series to be tested,  is the intercept term,

is the intercept term,  is the coefficient of intercept in the URT,

is the coefficient of intercept in the URT,  is the parameter of the augmented lagged first difference of the dependent variable, ,

is the parameter of the augmented lagged first difference of the dependent variable, ,  represents the ith order auto regressive process, and

represents the ith order auto regressive process, and  is the white noise error term. The number of lagged difference terms to include in the autoregressive process was determined empirically so that enough terms were included such that the error term was serially uncorrelated. The stationary condition under ADF test requires that

is the white noise error term. The number of lagged difference terms to include in the autoregressive process was determined empirically so that enough terms were included such that the error term was serially uncorrelated. The stationary condition under ADF test requires that , that is, p value must be less than 1.One-sided p-values were used for the present empirical analysis because they are more powerful than their two-sided counterparts (Demos and Sentana, 1998). Thus, the null hypothesis of non-stationarity would be rejected if

, that is, p value must be less than 1.One-sided p-values were used for the present empirical analysis because they are more powerful than their two-sided counterparts (Demos and Sentana, 1998). Thus, the null hypothesis of non-stationarity would be rejected if  , where

, where  is the critical value obtained from the Table. Contrariwise, if

is the critical value obtained from the Table. Contrariwise, if  , then the null hypothesis that the series is non-stationary would not be rejected.

, then the null hypothesis that the series is non-stationary would not be rejected.

If from the ADF test results, the time series exhibited stationarity and both data sets were integrated at the same order, then the study proceeded to examine whether or not there existed a long-run relationship between EXR and EXP growth by administering JCiT as follows:

… (2)

… (2)

where,  is an

is an  vector of non-stationary I(1) variables,

vector of non-stationary I(1) variables, is an vector of constants, p is the maximum lag length,

is an vector of constants, p is the maximum lag length,  is an

is an  matrix of coefficient and is an vector of white noise terms.The is indicative of the extent of relationship or Cointegration, while the preceding (+ or -) sign to the beta is indicative of whether the long-run relationship is positive or negative.

matrix of coefficient and is an vector of white noise terms.The is indicative of the extent of relationship or Cointegration, while the preceding (+ or -) sign to the beta is indicative of whether the long-run relationship is positive or negative.

Given that EXR and EXP growths are typical time series and that there might be some disturbance or disequilibrium in the short-run, VECM was used to measure the speed of correction or convergence into the long-run steady of equilibrium (Ray, 2012; Fapetu and Oloyede, 2014). JCiT equation (2) had to be converted into a vector error correction equation thus:

… (3)

… (3)

where,  is the first difference,

is the first difference,  is

is , and >

, and > is equal to identity metrics

is equal to identity metrics  .

.

While EXR and EXP growth might be correlated in international trade finance, JCiT would not conclusively provide causality, hence, as earlier noted, testing the presence of causal relationship between the two series was performed by administering the GCT upon confirmation that the time series are, to some extent, co-integrated. The GCT method measures the degree to which information provided by one variable explains the latest value of another variable. Conceptually, if X causes Y, then, changes of X happened first then followed by changes of Y (Granger, 1969). In the present study based on two variables, namely, EXR and EXP, the following equations were applied for the relevant GCTs:

If the causality runs from EXR to EXP growth rate, then the Granger causality regression equation is:

… (4)

… (4)

If the causality runs from EXP growth rate to EXR, then the Granger causality regression equation is:

… (5)

… (5)

From the equation (4),  Granger-causes

Granger-causes  if the coefficient of the lagged values of EXP as a group

if the coefficient of the lagged values of EXP as a group  is significantly different from the zero based on F-test. In the same vein, from equation (5),

is significantly different from the zero based on F-test. In the same vein, from equation (5),  Granger-causes

Granger-causes  if

if  is statistically significant. The “F value” statistic - the ratio of the mean regression sum of squares divided by the mean error sum of squares - tests the overall significance of the regression model. Specifically, it tests the null hypothesis that all of the regression coefficients are equal to zero. Thus, F-value will range from zero to an arbitrarily large number (Parasuraman et al., 2012). If

is statistically significant. The “F value” statistic - the ratio of the mean regression sum of squares divided by the mean error sum of squares - tests the overall significance of the regression model. Specifically, it tests the null hypothesis that all of the regression coefficients are equal to zero. Thus, F-value will range from zero to an arbitrarily large number (Parasuraman et al., 2012). If  is rejected based on the F-test or p-values, then there is a presence of Granger-causality.

is rejected based on the F-test or p-values, then there is a presence of Granger-causality.

The P-value is a number between 0 and 1, where a small p-value (usually 0.05) indicates strong evidence against the null hypothesis, leading to rejection of the null hypothesis. A large p-value (>0.05) suggests weak evidence against the null hypothesis.

The following hypotheses were developed to meet the objectives of the present study:

Exchange rate (EXR) has a unit root.

Exchange rate (EXR) has a unit root.

Export value (EXP) has a unit root.

Export value (EXP) has a unit root.

There is no co-integration between EXR and EXP.

There is no co-integration between EXR and EXP.

EXR does not Granger-cause EXP.

EXR does not Granger-cause EXP.

EXP does not Granger-cause EXR.

EXP does not Granger-cause EXR.

4. RESULTS AND DISCUSSION

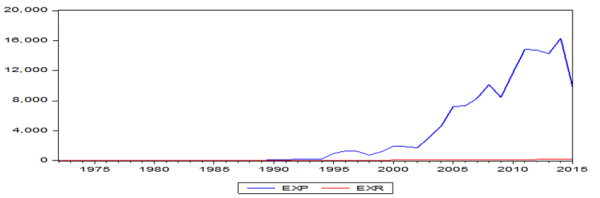

Graphical Analysis: Figure 1 provides the visual trends in EXR and EXP growth in Nigeria over the study period, 1972 – 2015. From the graphics, some visual correlation between EXR and EXP is evident over the more than 40 years of Nigeria’s development trajectory. Notably, from the 1990s/2000s when the exchange rate to the dollar climbed from the single digit regime that existed from the ‘60s to double or more digits, both EXP and EXR had been on a rising trend.

Figure-1. Exchange rate of the Naira to the US dollar and Export performance in Nigeria (N’ billion) in Nigeria, 1972-2015

Source: E-Views graph analysis (2016)

The graphics indicate the possibility that export performance in Nigeria has been influenced by the exchange rate situations. In other words, exchange value of the Naira has had positively affected Nigeria’s export performance, contrary to some of the views canvassed in sections of the Nigerian press (Shettima, 2016). This preliminary finding is hardly surprising, considering that the country’s exports had been substantially (88.1%: 2015) accounted for by volatile crude oil prices in the international markets. However, causality between the two series could not be established, hence the need for further analysis via the unit root test.

Unit Root Test: Table 1 shows the results of the ADF Unit Root Test. The results show that the null hypotheses H1 and H2 that EXR and EXP have unit roots can be rejected since the critical t-value is, in the case of EXR less than 0.05 at first difference (I(1)) at 5 percent significance level. For EXP, the t-value is -2.693, which is lower than the computed ADF critical value (-2.6174) at 10 percent level of significance at second difference. It was therefore concluded that EXR and EXP time series do not have unit root problem and the data good enough to proceed to co-integration test.

Table-1. ADF Unit Root Test for EXR and EXP in Nigeria, 1972 - 2015

|

Particulars |

EXR | EXP | |||||||||||

| t-statistic | Critical Value | P-value | t-statistic | Critical Value | P-value | ||||||||

| At level |

-1.2842 |

1% | -3.5925 |

0.9982 |

-1.7877 |

1% | -3.6210 |

0.3806 |

|||||

| 5% | -2.9314 | 5% | -2.9434 | ||||||||||

| 10% | -2.6039 | 10% | -2.6103 | ||||||||||

|

-4.7423 |

1% | -3.3566 |

0.0004 |

-1.2027 |

1% | -3.6210 |

0.6630 |

||||||

| At first difference | 5% | -2.9332 | 5% | -2.2934 | |||||||||

| 10% | -2.6049 | 10% | -2.6103 | ||||||||||

|

Not applicable |

-2.6930 |

1% | -3.6537 |

0.0863 |

|||||||||

| At second difference | 5% | -2.9571 | |||||||||||

| 10% | -2.6174 | ||||||||||||

Source: Author’s computation using EViews software (2016)

Johansen’s Co-Integration Test: Table 2 presents the results of the JCiT which was conducted to establish whether there was any long-run equilibrium between EXR and EXP in Nigeria over the period 1972 - 2015. The null hypothesis (H3): there is no Cointegration between EXR and EXP – is accepted at 5 percent level of significance since p-value (0.1411) is greater than 0.05, which leads to the rejection of the alternative hypothesis that there is co-integration between EXR and EXP. In essence, trace and Max-eigenvalue tests indicate no Cointegration at the 0.05 level of significance.

Table-2. Results of Johansen Co-integration Test on EXR and EXP growth time series in Nigeria, 1972 - 2015

| Level | Eigen Value | Trace Statistic | Critical Value at 5% | P-values |

| Ho: r = 0 (none)* | 0.2311 | 12.3452 | 15.4947 | 0.1411 |

| H1: r = 1 (at most 1) | 0.0306 | 1.3074 | 3.8415 | 0.2529 |

*denotes rejection of the hypothesis at the 0.05 significance level.

Source: Author’s computation using EViews software (2016)

Vector Error Correction Model (VECM): The next level of analysis involved fitting the series into a VECM and the results, as shown in Table 3 based on the first normalized eigenvector, indicates the presence of negative long-run relationship between EXR and EXP. The estimated co-integrating coefficient for the EXP growth is as follows:

[-8.0103]

The t-statistic of the co-integrating coefficient of EXR is given in the bracket. The coefficient for EXR is negative, which means that increase in EXR can be associated with decline in the EXP growth of Nigeria.

Table-3. Co-integrating Vector of EXR and EXP growth in Nigeria, 1972 - 2015

| Co-integrating Equation | ||

| EXP | EXR | Constant |

| 1.0000 | -95.2610(13.1967)[-8.0103] | 2142.555 |

Standard errors in ( ), and t-statistics in [ ]

Source: Author’s computation using EViews software (2016)

As shown in Table 4, the error correction coefficient term is negative (-0.3380) and statistically significant at 5 percent level of significance; this is indicated by the lower t-statistic value (-0.3553) than the critical value (-1.96) at 5 percent significance level. This evidences the negative long-run equilibrium relation between EXR and EXP growth in the Nigerian context. Thus, it could be inferred that the value of next year’s EXP is greatly influenced by the current year’s EXR at 95 percent confidence level. This finding accords with the reality considering that more than 80 percent of the country’s exports (crude oil) have been tied to the exchange rate over the years.

Table-4. Exchange rate of the Naira (EXR) and Export growth (EXP) in Nigeria, 1972 – 2015: Co-integrating Vector Error Correction Estimates

| Error Correction | D(EXP) | D(EXR) |

| CointEq1 | -0.3380(0.0951)[-3.5525] | -0.0003(0.0009)[-0.3455] |

| D(EXP(-1)) | -0.3624(0.2176)[-1.6657] | 0.0008(0.0021)[0.3826] |

| D(EXP(-2)) | -0.0755(0.2300)[-0.3281] | -0.0019(0.0022)[-0.8513] |

| D(EXR(-1)) | -14.7685(22.5775)[-0.6541] | 0.1093(0.2162)[0.5056] |

| D(EXR(-2)) | -35.3881(22.5871)[-1.5667] | -0.0270(0.2163)[-0.1250] |

| C | 599.4093(264.215)[2.2686] | 4.8072(2.5302)[1.8999] |

( ) error term

[ ] t-value

Source: Author’s computation using EViews software (2016)

Granger Causality Test: The results of Granger causality test are presented in Table 5. The result in Table 5 indicates the possibility of causality between EXR and EXP but it is one-directional; the causality runs from EXR to EXP and not vice-versa. This means that over the 44 years under investigation, export performance in Nigeria has been significantly influenced by the exchange rate situations. In other words, as noted earlier, exchange value of the Naira has had significant influence on Nigeria’s export performance, contrary to some of the views canvassed in sections of the Nigerian press (Shettima, 2016). The finding herein is hardly surprising, given that substantial portion (88.1%: 2015) of the country’s exports had been accounted for by volatile crude oil prices in the international markets. The null hypothesis: EXR does not Granger-cause EXP growth is rejectedas the probability value (0.0064) is smaller than .05 required significance level. However, expectedly, the null hypothesis: EXPgrowth does not Granger-cause EXR is accepted as the probability value (0.8428) is greater than .05 required significance level. This means that to a significant extent, EXP growth does not necessarily have affect exchange rate, as there are many factors that could be responsible for the determination of EXR in any economy (Mankiw, 2004). This finding is also consistent with Adeniran et al. (2014) and Olubanjo et al. (2009) among others which found out limited or negative nexus between real sector (non-oil) economic activities and the exchange rate of the Naira.

However, EXP growth rate is Granger-caused by EXR, and thus the value of EXR can be used to predict future level of EXP growth which is in unanimity with some similar studies, notably, Wafure and Nurudeen (2010); Alao (2010); Enoma (2011) among others.

Table-5. EXR and EXP Growth in Nigeria: Results of Granger Causality Test

| Null Hypotheses | Observations | F-Statistic | Probability | Decision |

| EXR does not Granger-cause EXP growth | 42 | 5.8067 | 0.0064 | Rejected |

| EXP growth does not Granger-cause EXR | 42 | 5.61143 | 0.8428 | Accept |

Source: Author’s computation using EViews software (2016)

4.1. Summary and Findings

The research study explored the empirical relationship between the Naira exchange rate (EXR) and export growth (EXP) in Nigeria using annual time series from 1972 to 2015. After evaluating stationarity of the Naira exchange rate and export growth over the study period, and conducting series of econometric tests to determine co-integration and causality, the following major findings emerge from the study:

- Both EXR and EXP are stationary based on Augmented Dickey Fuller (ADF) test.

- The trace test under Johansen co-integration method indicates no Cointegration at 5 percent level of significance.

- From the VECM result, it is evident that EXR has significant negative long-run impact on EXP growth of the Nigerian economy. The negative long-run relationship between EXR and EXP growth tested statistically significant by a negative coefficient of EXR. This indicates that high level of EXR may lead to a slow-down in export performance in the Nigerian context, as recently experienced between 2014 and 2015: Nigeria’s total exports stood at

N9,728.8 billion at the end of 2015, a decline ofN6,575.2 billion or 40.3 percent over the levels achieved in 2014 (NBS, 2016). - The Granger causality test results showed the presence of one-directional causality; causality runs from EXR to EXP with no feedback. This suggests that, while EXR may be useful in predicting EXP, the current level of EXP in the Nigerian context, serves no predictive purpose for the international value of the local currency.

In essence, the results from the present study suggests that export growth in Nigeria has had very little impact on exchange rate, and this is believed to align with the trade-balance hypothesis and consistent with some empirical positions on the impact of exchange rate on export growth in commodities-dependent economies lie Nigeria (Omojimite, 2012; Ewetan and Okodua, 2013; Oyinbo et al., 2014; Shettima, 2016). For many years, Nigeria has experienced low level of non-oil exports and a situation where changes in the value of the Naira are delinked from the real sector of the economy. Evidently, for Naira value to be sustainable there has to be appreciable improvement in the business environment to facilitate production, processing, and packaging of the country’s products for overseas markets. The idea is that a truly diversified Nigerian economy can widen sources of foreign exchange earnings to remove pressure on the Naira.

5. CONCLUSION

The paper has shown one-directional causality between Naira exchange value and export growth in Nigeria using time series analysis methods, and this has significant policy implications for robust, sustainable export-oriented economic management. The results from the present research study suggests that export performance in Nigeria has had very little impact on exchange rate, and this is believed to align with the trade-balance hypothesis and previous empirical studies especially in the context of commodities-dependent economies like Nigeria (Olubanjo et al., 2009; Omojimite, 2012; Ewetan and Okodua, 2013; Adeniran et al., 2014; Oyinbo et al., 2014). For many years, the country has experienced low level (11.9%: 2015) of non-oil exports, thus the thesis that if you devalue the currency, you will export more, is not empirically supported in a single commodity (crude oil)-dependent emerging market like Nigeria.

For Naira value to be sustainable, non-oil exports have to be boosted in order to help reverse persisting situation where volatility of global commodity prices has had causal influence on Nigerian exports. Additionally, serious entrepreneurs can still drive their domestic businesses without much reliance on the exchange rate of the Naira, as long as such enterprises are not dependent on imported materials. Also, it is imperative for government to create a robust, diversified economic structure focused on providing the citizenry with improved access to microfinance, good roads, stable and adequate power supply, investment-friendly tax regime, flexible exchange rate policy, quality education, among others, so that the sizable and growing number of Micro, Small and Medium Enterprises (MSMEs) in Nigeria can contribute more meaningfully to job creation, exportation, and sustained growth of national prosperity. Based on the findings from this research study, the following recommendations are apposite:

- “Seek ye first a business-friendly environment, and all other things including sustainable exchange rate, will follow”: Policy development should be more focused on promoting exports in more business-friendly environment with adequate security and infrastructural facilities. The state and local governments need to get more involved in the provision of basic amenities such as feeder roads and power supply, to make the business environment much easier for existing and aspiring exporters.

- Given the humongous potentialities in the export and currency markets globally, a renewed focus on agricultural and petrochemical industrialization has become imperative for non-oil export drive so as to maintain sustainable surplus balance of payments that can strengthen the value of the Naira in the long-run. To this end, the Nigerian Export Promotion Council (NEPC) should be reinvigorated towards improved performance of its mandate.

- There is a need to progress beyond the mere mouthing or mantra of promoting patronage for ‘Made-in-Nigeria Goods’ into more visible, commensurate purposeful, relentless actions that can help to significantly reverse the country’s penchant for imported goods and services.

4.2. Scope for Future Research

- Annual time series were adopted for the present study based on ease of data availability. Using more frequent time intervals (quarterly figures) to compliment current findings will remain an important area to explore for the next research.

- The present study examined EXP holistically based on official EXR, i.e. aggregate of oil and non-oil exports as the variable tested against government-fixed EXR. The next research should test non-oil dynamics against parallel market EXR (“black-market” exchange rate) to revalidate current evidence.

| Funding: This study received no specific financial support. |

| Competing Interests: The author declares that there are no conflicts of interests regarding the publication of this paper. |

REFERENCES

Adeniran, J.O., S.A. Yusuf and O.A. Adeyemi, 2014. The impact of exchange rate fluctuation on the Nigerian economic growth: An empirical investigation. International Journal of Academic Research in Business and Social Sciences, 4(8): 224-233. View at Google Scholar | View at Publisher

Ajide, K.B., 2014. Determinants of economic growth in Nigeria. CBN Journal of Applied Statistics, 5(2): 147 – 170. View at Google Scholar

Alao, R.O., 2010. Interest rates determination in Nigeria: An econometric x-ray. International Research Journal of Finance and Econometrics, 47: 43-52.

Amassona, J.D., P.I. Nwosa and A.F. Ofere, 2011. The nexus of interest rate deregulation, lending rate and agricultural productivity in Nigeria. Current Research Journal of Economic Theory, 3(2): 53-61. View at Google Scholar

Barro, R.J. and V. Grilli, 1994. European macroeconomics. London: The Macmillan Press Ltd.

Central Bank of Nigeria [CBN], 2010. 2010 Annual Report: 31st December 2010. Abuja: CBN.

Chidi, O.U. and U.A. Godwin, 2015. Modelling exchange rate volatility of NGN/BPS using GARCH models. Programme Details and Initial Book of Abstracts, International Symposium on Mathematical and Statistical Finance, Training the Next Generation of African Financial Mathematicians, Ibadan, September 1-3, 2015, Paper 23: 15.

Chukuigwe, E.C. and I.D. Abili, 2008. An econometric analysis of the impact of monetary and fiscal policies on non-oil exports in Nigeria: 1974 – 2003. African Economic and Business Review, 6(2): 59-73. View at Google Scholar

Demos, A. and E. Sentana, 1998. Testing for GARCH effects: A one-sided approach. Journal of Econometrics, 86(1): 97 – 127. View at Google Scholar | View at Publisher

Dickey, D.A. and W.A. Fuller, 1981. Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica, 49(4): 1057-1072. View at Google Scholar | View at Publisher

Engle, R.F. and C.W. Granger, 1987. Co-integration and error-correction representation, estimation and testing. Econometrica, 55(2): 251-276. View at Google Scholar | View at Publisher

Enoma, I.A., 2011. Exchange rate depreciation and inflation in Nigeria (1986-2008). Business and Economics Journal, 28: 1-11.

Ewetan, O.O. and H. Okodua, 2013. Econometric analysis of exports and economic growth in Nigeria. Journal of Business Management and Applied Economics, 2(3): 1-14. View at Google Scholar

Fapetu, O. and J.A. Oloyede, 2014. Foreign exchange management and the Nigerian economic growth (1970-2012). European Journal of Business and Innovation Research, 2(2): 19-31.

Gibson, M.L. and M.D. War, 1992. Export orientation: Pathway or artifact? International Studies Quarterly, 36(3): 331-343. View at Google Scholar | View at Publisher

Granger, C.W.J., 1969. Investigating causal relations by econometric models and cross spectral methods. Econometrica, 37(3): 424 – 438. View at Google Scholar | View at Publisher

Granger, C.W.J., 1988. Some recent development in the concept of causality. Journal of Econometrics, 39(1-2): 199 - 211. View at Google Scholar | View at Publisher

Gujarati, D.N. and Sangeetha, 2007. Time series econometrics: Some basic concepts. In basic econometrics. 4th Edn., New Delhi: Tata McGraw-Hill Publishing Company Limited. pp: 811-841.

Mankiw, N.G., 2004. Essentials of economics. 3rd Edn., Mason, Ohio: Thomson South-Western.

Mbah, C., 2016. Why Naira can’t be devalued now – Oshiomhole. Newswatch Times: 4.

National Bureau of Statistics (NBS), 2016. Foreign trade statistics, Fourth Quarter, 2015. No. 517. Abuja: NBS.

Obinwanne, E.E., O.U. Chidi and O.N. Agartha, 2015. Exchange rate and economic growth in Nigeria: A causality approach. Programme Details and Initial Book of Abstracts, International Symposium on Mathematical and Statistical Finance, Training the Next Generation of African Financial Mathematicians, Ibadan, September 1-3, 2015, Paper 25, pp: 17.

Okere, R., 2016. Nigeria loses N2 trillion yearly to petrochemicals import. The Guardian (Nigeria): 6.

Oloyede, J.A., 2002. Principles of international finance. Lagos: Forthright Educational Publishers.

Olubanjo, O.O., S.O. Akinleye and T.T. Ayanda, 2009. Economic deregulation and supply response of cocoa farmers in Nigeria. Journal of Social Science, 21(2): 129-135. View at Google Scholar

Omojimite, B.O., 2012. Institutions, macroeconomic policy and growth of agricultural sector in Nigeria. Global Journal of Human Social Science, 12(1): 1-8. View at Google Scholar

Oyinbo, O., F. Abraham and G.Z. Rekwot, 2014. Nexus of exchange rate deregulation and agricultural share of gross domestic product in Nigeria. CBN Journal of Applied Statistics, 5(2): 49-64. View at Google Scholar

Parasuraman, N.R., P.J. Ramudu and Nusrathuunisa, 2012. Does lintner model of dividend payout hold good? An empirical evidence from BSE SENSEX firms. SDMIMD Journal of Management, 3(2): 63–76. View at Publisher

Piketty, T., 2014. Capital in the twenty-first century. London: The Belknap Press of the Harvard University Press.

Raghul, A. and S.V. Hariharan, 2015. Exchange rate volatility on foreign currency and performance management in various industries. Proceedings of the 4th International Conference on Emerging Trends in Finance and Accounting, August 21-22, 2015. pp: 1-10.

Rates, O.A., 2016. Exchange rate theories. 452-470. Available from http://www.uta.edu/faculty/crowder/papers/Chapter18.pdf [Accessed 24th March 2016].

Ray, S., 2012. Impact of foreign direct investment on economic growth in India: A co-integration analysis. Advances in Information Technology and Management, 2(1): 187 – 201. View at Google Scholar

Shettima, I.B.B., 2016. Depreciation of the Naira: To be or not to be (1). Daily Trust (Nigeria): 49.

Sims, D., 2014. China widens lead as world’s largest manufacturer. Available from http://news.thomasnet.com/imt/2013/03/14/china-widens-lead-as-worlds-largest-manufacturer [Accessed 22nd March 2016].

Tella, S., 2016. Interview. The Punch (Nigeria): 50-51.

The Guardian (Editorial), 2016. How much forex does Nigeria need? The Guardian (Nigeria): 16.

Venkatraja, B., 2015. A causality analysis on the empirical nexus between capital formation and economic growth: Evidence from India. Rajagiri Management Journal, 9(1): 26-42.

Venkatraja, B. and M. Sriram, 2015. A causal nexus between FDI and economic growth of India: An empirical study. Contemporary research in management. Mysore, India: SDMIMD, 4:1 – 34.

Wafure, G.G. and A. Nurudeen, 2010. Determinants of foreign direct investment in Nigeria: An empirical analysis. Global Journal of Human Social Science, 10(1): 26-34. View at Google Scholar

Web sources

Appendix

Exchange Rate (N per US Dollar) and Value of Exports (N' billion) in Nigeria (1972 - 2015)

| Year | Exchange Rate ( |

Value of Exports ( |

| 1972 | 0.66 | 1.40 |

| 1973 | 0.66 | 2.30 |

| 1974 | 0.63 | 5.80 |

| 1975 | 0.62 | 5.00 |

| 1976 | 0.62 | 6.60 |

| 1977 | 0.65 | 7.90 |

| 1978 | 0.61 | 6.40 |

| 1979 | 0.60 | 10.40 |

| 1980 | 0.55 | 14.20 |

| 1981 | 0.61 | 11.00 |

| 1982 | 0.67 | 8.20 |

| 1983 | 0.72 | 7.50 |

| 1984 | 0.77 | 9.10 |

| 1985 | 0.89 | 11.70 |

| 1986 | 2.02 | 8.90 |

| 1987 | 4.02 | 30.40 |

| 1988 | 4.54 | 31.20 |

| 1989 | 7.39 | 58.00 |

| 1990 | 7.39 | 109.90 |

| 1991 | 8.04 | 121.50 |

| 1992 | 9.91 | 205.60 |

| 1993 | 17.30 | 218.80 |

| 1994 | 22.33 | 206.10 |

| 1995 | 21.89 | 950.70 |

| 1996 | 21.89 | 1,309.50 |

| 1997 | 21.89 | 1,241.70 |

| 1998 | 21.89 | 751.90 |

| 1999 | 21.89 | 1,189.00 |

| 2000 | 85.98 | 1,945.70 |

| 2001 | 102.50 | 1,868.00 |

| 2002 | 111.00 | 1,744.20 |

| 2003 | 120.50 | 3,087.90 |

| 2004 | 133.90 | 4,602.80 |

| 2005 | 131.40 | 7,246.50 |

| 2006 | 129.00 | 7,324.70 |

| 2007 | 134.05 | 8,309.80 |

| 2008 | 132.37 | 10,114.70 |

| 2009 | 132.60 | 8,402.20 |

| 2010 | 150.40 | 11,706.70 |

| 2011 | 153.50 | 14,822.60 |

| 2012 | 157.70 | 14,736.10 |

| 2013 | 157.30 | 14,245.27 |

| 2014 | 158.20 | 16,304.04 |

| 2015 | 197.00 | 9,728.80 |

Sources: National Bureau of Statistics and Central Bank of Nigeria

| Views and opinions expressed in this article are the views and opinions of the author(s), Asian Economic and Financial Review shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |