DETERMINANTS OF DIGITAL BANKING SERVICES IN VIETNAM: APPLYING UTAUT2 MODEL

1,3,4Faculty of Banking and Finance, Foreign Trade University, Vietnam.

2Vietnam-Japan Institute for Human Resource Department (VJCC), Foreign Trade University, Vietnam.

ABSTRACT

Digital banking is one of the latest applications that integrates all services of traditional banks via digitized technology. Its pivotal role in the development of banking industry has been recently recognized, especially in emerging countries such as Vietnam. This paper identified the determinants of Vietnamese consumers’ behavioural intention to adopt or use digital banking . By using the Modified Unified Theory of Acceptance and Use of Technology (UTAUT2), the eight constructing factors have been selected to examine their influences on the Vietnamese customers’ behaviour: performance expectancy (PE), effort expectancy (EE), social influences (SI), facilitating conditions (FC), hedonic motivation (HM), price value (PV), habit (HT), and trust (TR). The findings suggested that performance expectancy, effort expectancy, hedonic motivation, habit, and trust significantly and positively influence the behavioural intention of digital banking services. The intention of adoption services, together with habit and facilitating conditions are three significant factors capturing the usage intention under the context of Vietnam. The empirical results not only made a valuable contribution to the existing research on banking innovation, but also provided benefits to policy-makers, bank supervisors, and bank managers concerning how to develop and improve the customers’ recognition and intention to use new banking services.

Keywords:Digital banking, Banking innovation, Technology acceptance, Behavioural intention, Usage intention, UTAUT2.

JEL Classification:O33; G21.

ARTICLE HISTORY: Received:17 March 2020, Revised: 27 April 2020, Accepted: 29 May 2020, Published: 22 June 2020

Contribution/ Originality: This study is one of very few studies which have investigated the key factors influencing Vietnamese customers’ behaviour in adopting and using digital banking services. The findings from UTAUT2 model showed that the usage intention was determined by the intention of adoption services, habit and facilitating conditions.

1. INTRODUCTION

Consumer habits and preferences are changing, along with the development of the Internet and next-generation mobile devices equipped with mobile bandwidths (3G and 4G) at a competitive price. Consumers increasingly adapt to the interactions using digital media, helping them share information, make transactions and go shopping online, and access new services. Consumers now demand financial services anytime, anywhere that are compatible with their daily social networks. The role of social networks significantly increases as many industries adopt "digitization" as an extension of traditional social interaction (Skinner, 2014![]() ). Facebook, one of the biggest social networks worldwide, has 2.45 billion active users as of the 2019 third quarter (Clement, 2020

). Facebook, one of the biggest social networks worldwide, has 2.45 billion active users as of the 2019 third quarter (Clement, 2020![]() ).

).

Another important factor driving the digital transformation process is the expansion and development of mobile devices. According to Skinner (2014![]() ) the average penetration rate of mobile phones worldwide is approaching 70%, creating the foundation for the development of new mobile applications. This is exemplified by a survey for consumers from 22 countries in which the use of mobile banking applications has increased by 19 percentage during the period 2013-2014, while the usage of Internet banking services remained virtually unchanged (Bain & Company, 2014

) the average penetration rate of mobile phones worldwide is approaching 70%, creating the foundation for the development of new mobile applications. This is exemplified by a survey for consumers from 22 countries in which the use of mobile banking applications has increased by 19 percentage during the period 2013-2014, while the usage of Internet banking services remained virtually unchanged (Bain & Company, 2014![]() ).

).

The period from 2011 to 2016 has been highlighted with the launching of a variety of products, services and sales channels in the banking industry in Vietnam. Although the performance of credit institutions in general have many positive changes, the competition among commercial banks has been also increased following the trend of international economic integration. To deal with the rising challenges in the banking industry, each commercial bank has been motivated to seek new opportunities to grow its profit, such as enhancing interaction with customers by innovated services integrated with real experience.

In the digital era, traditional services provided by banks have been no longer meet the changes in consumer behaviour. More and more customers prefer the simple and the convenience of products and services, while the information about products and services can be found easily via mobile devices and tablets. Grasping the value of the digital revolution, commercial banks no longer encapsulate in the traditional model of operating through branches. According to McKinsey’s report, the impact of digital technology has brought the bank's net profit opportunities to range from 43% - 48% in 2014. Many banks have targeted digital banking as their strategic goal and competitive advantage.

Acknowledging the significance of digital banking development in Vietnam, however, the major obstacle for the success of this technology application is how to persuade customers to use it as an alternative for traditional services (Laukkanen, Sinkkonen, Kivijärvi, & Laukkanen, 2007![]() ). Since the implementation of digital banking in Vietnam is in the early stage, only a few studies have addressed it.

). Since the implementation of digital banking in Vietnam is in the early stage, only a few studies have addressed it.

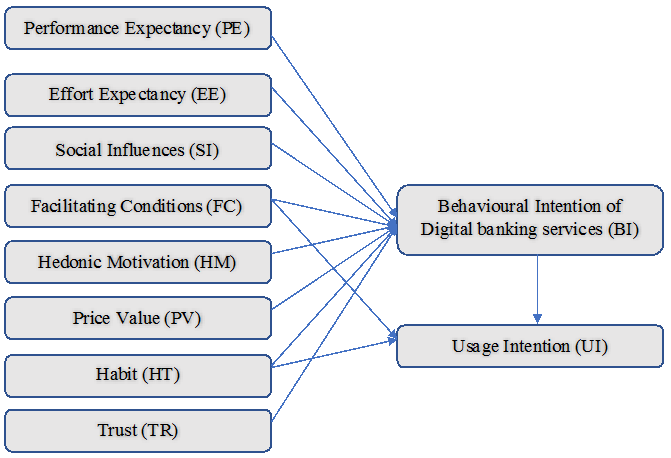

Hence, based on the results of 300 questionnaires, this paper identified influences on the intention and adoption of using digital banking services for Vietnamese customers. The paper used the UTAUT2 method proposed by Venkatesh, Thong, and Xu (2012![]() ) for testing the impact of eight selected factors (comprising of performance expectancy (PE), effort expectancy (EE), social influences (SI), facilitating conditions (FC), hedonic motivation (HM), price value (PV), habit (HT), and trust (TR)) on the Vietnamese customers’ behaviour of adopting digital banking services (BI). The behaviour of using those services was then analysed under the influences of behavioural intention (BI), habit (HT), and facilitating conditions (FC).

) for testing the impact of eight selected factors (comprising of performance expectancy (PE), effort expectancy (EE), social influences (SI), facilitating conditions (FC), hedonic motivation (HM), price value (PV), habit (HT), and trust (TR)) on the Vietnamese customers’ behaviour of adopting digital banking services (BI). The behaviour of using those services was then analysed under the influences of behavioural intention (BI), habit (HT), and facilitating conditions (FC).

2. OVERVIEW OF DIGITAL BANKING SYSTEM IN VIETNAM

Digital banking can be defined as a technology-based operating model for exchanging information and carrying out transactions between banks and customers. Instead of generating transactions in the traditional way (i.e. face-to-face transactions), customers and banks can interact with each other by electronic devices such as smartphones, tablets and Internet web applications. Additionally, digital banking is a new and higher development form of electronic banking. If e-banking is a service channel that banks provide to customers to support other traditional services (i.e. Internet Banking, SMS Banking and Mobile Banking services), digital banking is a whole platform that affects the entire system of a bank, from organizational structure, working processes, products and services provision, to legal issues and methods of dealing with customers.

It is estimated that 57% of Vietnamese people are using the Internet (Doan, 2020a![]() ), whereas 34% of the population used smartphones in 2018 (Doan, 2020b

), whereas 34% of the population used smartphones in 2018 (Doan, 2020b![]() ). The proportion of Vietnamese individuals with bank transaction accounts is recorded by the State Bank of Vietnam as approximately 40% (State Bank of Vietnam, 2020

). The proportion of Vietnamese individuals with bank transaction accounts is recorded by the State Bank of Vietnam as approximately 40% (State Bank of Vietnam, 2020![]() ). It implies that in any 100 Vietnamese people, there are 57 Internet users, 34 smartphone users, and 40 bank account holders. The universalization of financial services through digitalization can increase the channels of assessing banking services, which later can attract more potential customers for the banks. The following sections provide a comprehensive picture of digital banking system in Vietnam, comprising of its infrastructure, legal framework, and current development. The brief analysis on each aspect may clarify the necessity of continuous expanding digital banking services to Vietnamese consumers.

). It implies that in any 100 Vietnamese people, there are 57 Internet users, 34 smartphone users, and 40 bank account holders. The universalization of financial services through digitalization can increase the channels of assessing banking services, which later can attract more potential customers for the banks. The following sections provide a comprehensive picture of digital banking system in Vietnam, comprising of its infrastructure, legal framework, and current development. The brief analysis on each aspect may clarify the necessity of continuous expanding digital banking services to Vietnamese consumers.

2.1. Vietnam’s Digital Banking Infrastructure

Vietnam’s banking system had 49 banks at June 2018, including 46 commercial banks, 2 policy banks, and 1 cooperative bank (State Bank of Vietnam, 2016![]() ). However, the number of transaction offices and branches on the scale of population in Vietnam was at moderate level compared to the region. Vietnam had 12.7 branches and transaction offices serving 100,000 adults in average, relatively high compared with other countries in the region (The World Bank Data, 2020

). However, the number of transaction offices and branches on the scale of population in Vietnam was at moderate level compared to the region. Vietnam had 12.7 branches and transaction offices serving 100,000 adults in average, relatively high compared with other countries in the region (The World Bank Data, 2020![]() ). This number in Indonesia is 16.2; Thailand is 11.7; Singapore is 8.4; Malaysia is 10.2 and Cambodia is 7.8.

). This number in Indonesia is 16.2; Thailand is 11.7; Singapore is 8.4; Malaysia is 10.2 and Cambodia is 7.8.

The network of transaction offices and branches in Vietnam shows an imbalanced distribution, while the top seven biggest banks account for 55% of the number of transaction points over the system. The system of Vietnamese transaction points has been still modest, while the demand for transactions and use of banking services in Vietnam has revealed various developing potentials.

2.2. Vietnam’s Digital Banking Legal Framework

Digital banks differ from traditional banks with product and service designs, policies, procedures provided to customers. The current legal system has certain progressive points on the construction of a legal corridor for electronic payment, card payment, licensing and monitoring non-banking institutions in providing payment services. However, some limitations of the current legal framework have been still found as follows:

- The lack of regulations, documents and procedures leads to difficulties in expanding digital payment, especially to young customers who prefer flexible procedures and regulations and to people who do not have bank accounts or live in rural areas.

- There is no e-KYC system in terms of user authentication. The Government and the SBV have not yet allowed banks to access the Citizens' Identity data system. They only base on the identification numbers provided by the customers.

- There is a lack of electronic signatures guidance. Currently the electronic transaction authentication can be managed electronically. However, the use of digital signatures has been still inadequate and inconvenient. For example, digital signatures are required to have specialized storage devices, and that may bring many inconveniences to customers.

- There is no official regulation for using digital documents (electronic documents) instead of paper documents. The inconsistent form of documents by different banks may lead to the lack of grounds for legal disputes and carry more potential risks.

- No standards for QR codes have been clarified. QR code, launched in 1994, has quickly been invested by financial institutions for worldwide applications. There are up to twelve organizations implementing QR code payment services, accepted by nearly 50,000 transaction points in Vietnam (VIRAC, 2019). Up to the middle of 2018, more than 8,000 stores and websites accept QR Pay, and it is expected to reach 50,000 at the end of the same year (Hai, 2018

).

). - Licensing procedures for current banking-related services are relatively complicated. Some banks might manage to develop their products in a short time but it takes up to three months to launch them to the market due to many procedural problems.

2.3. Vietnam’s Digital Banking Challenges and Opportunities

The process of digitizing the banking system in Vietnam was recognized by the Interbank electronic payment system, which has been funded by the World Bank since May 2002. It facilitates the process of innovation and modernization in the banking system, such as e-banking services, Internet banking and Mobile banking services. Mobile banking in Vietnam was first launched by ACB in 2003, based on the cooperation with VASC software and two mobile telecommunication corporations (MobiFone and Vinaphone). Meanwhile, Internet banking services were introduced in 2004 and quickly became popular with many Vietnamese customers.

In May 2016, the first digital bank of Vietnam was officially established by VPBank with the name “Timo” as Time and Money. Customers and Timo interact via the Internet and smart electronic devices (i.e. smartphones and tablets). At the same time, within the project of building smart branches towards the digital banking development strategy, Vietcombank – one of the largest banks in Vietnam – launched digital technology transaction spaces (Digital Lab) in Hanoi and Ho Chi Minh City. Recently, many other commercial banks (MBBank, Techcombank, etc.) have prepared for their own strategy to develop the digital banking services. In 2017, while TP Bank introduced Live Bank to the market, OCB launched Omni-channel – the first integrated bank in Vietnam.

Due to the fact of fast growth of digital banking in Vietnam, the operation and development of digital banking system must struggle with many challenges, including the insufficient legal framework relating to standard platforms for digital banks; the inadequate infrastructure of banks such as information technology system, security, marketing and operating activities; and the difficult conversion of customer behaviour in adapting to the new banking model since the psychology of Vietnamese people leans to being reserved and risk-averse, especially middle-aged people - those who are not familiar with and also not always willing to try non-traditional services like digital banking; etc.

Despite these reasons, Vietnam has a variety of potential to develop and exploit the advantages of digital banking. First, there is the increased usage of smart devices as well as the increasing time of surfing the Internet. According to the statistics of We are Social and Hootsuite (2019![]() ) Vietnam had 64 million Internet users in 2019, accounting for 66% of the population. There were 62 million social media users and 58 million mobile social media users. The report showed that 72% of grown-ups used smartphones, 43% of them had computers, 13% of them had tablets, and 94% of Internet users accessed the Internet daily. Secondly, the cash usage habit of Vietnamese has also changed significantly with the development of electronic banking services in recent years. With only three banks introducing electronic banking in 2004, this service was implemented by 100% of banks in the system by 2014. Thirdly, the dynamic Vietnam's banking system always strives to keep pace with the trend of the global banking system. Many banks have specific orientations for supporting digital banking, such as building new core banking, paying special attention to multi-channel management (Omni-Channel), and increasing customer experience.

) Vietnam had 64 million Internet users in 2019, accounting for 66% of the population. There were 62 million social media users and 58 million mobile social media users. The report showed that 72% of grown-ups used smartphones, 43% of them had computers, 13% of them had tablets, and 94% of Internet users accessed the Internet daily. Secondly, the cash usage habit of Vietnamese has also changed significantly with the development of electronic banking services in recent years. With only three banks introducing electronic banking in 2004, this service was implemented by 100% of banks in the system by 2014. Thirdly, the dynamic Vietnam's banking system always strives to keep pace with the trend of the global banking system. Many banks have specific orientations for supporting digital banking, such as building new core banking, paying special attention to multi-channel management (Omni-Channel), and increasing customer experience.

3. LITERATURE REVIEW ON THE BEHAVIOURAL AND USAGE INTENTION OF BANKING SERVICES

From one report on digital transformation in retail banking industry (Cisco, 2017![]() ), 53% of European banks – the market has 83% of people who are able to access the Internet at home - are looking for methods to invest in technology geared to customers. In developed Asian countries, 60% of transactions have transferred to digital channels.

), 53% of European banks – the market has 83% of people who are able to access the Internet at home - are looking for methods to invest in technology geared to customers. In developed Asian countries, 60% of transactions have transferred to digital channels.

Acknowledging the growing trend of digital banking in Asia since 2011, McKinsey (Barquin & Vinayak, 2015![]() ) conducted a survey of 16,000 financial customers in thirteen Asian markets for banking service’s usage behavior. During the period from 2011 to 2014, online banking became popular and the number of customers who made banking transactions via smartphones increased three times. The study highlighted the role of factors that accelerated the trend of digital banking development, including the rapid surge in Internet and smartphone usage as well as the growth of e-commerce. In addition, the survey results showed that up to 80% of customers were willing to switch to any bank that offered attractive digital services. However, the digitization process has not been fully implemented due to inconsistencies in investment and resources. Although researches on digital banking have been carried out, the studies about the determinants of customers' behaviour on digital banking services have been inconclusive and limited.

) conducted a survey of 16,000 financial customers in thirteen Asian markets for banking service’s usage behavior. During the period from 2011 to 2014, online banking became popular and the number of customers who made banking transactions via smartphones increased three times. The study highlighted the role of factors that accelerated the trend of digital banking development, including the rapid surge in Internet and smartphone usage as well as the growth of e-commerce. In addition, the survey results showed that up to 80% of customers were willing to switch to any bank that offered attractive digital services. However, the digitization process has not been fully implemented due to inconsistencies in investment and resources. Although researches on digital banking have been carried out, the studies about the determinants of customers' behaviour on digital banking services have been inconclusive and limited.

3.1. Prior Studies on the Acceptance of Using Online Banking Services

Among studies on digital banking services, research on customers’ acceptance of using online banking has been paid more attention. Casaló, Flavián, and Guinalíu (2007![]() ) examined the role of five factors (safety, security, usability, trust, and commitment) to the development of online banking in Spain. The study was based on data collected from 142 surveys conducted online for Spanish-speaking customers. Research showed that the lack of security is one of the leading causes of reduced trust in the Internet, thereby reducing the development of e-commerce. The results confirmed the positive and important effect of being aware of the safety of handling personal data on consumer confidence on an online banking site. In addition, trust and commitment of using online banking services were also exposed to be substantial in maintaining long-term relationships with customers.

) examined the role of five factors (safety, security, usability, trust, and commitment) to the development of online banking in Spain. The study was based on data collected from 142 surveys conducted online for Spanish-speaking customers. Research showed that the lack of security is one of the leading causes of reduced trust in the Internet, thereby reducing the development of e-commerce. The results confirmed the positive and important effect of being aware of the safety of handling personal data on consumer confidence on an online banking site. In addition, trust and commitment of using online banking services were also exposed to be substantial in maintaining long-term relationships with customers.

Yiu, Grant, and Edgar (2007![]() ) analysed the retail customers’ behaviour of adopting Internet banking in Hong Kong, employing the Technology Acceptance Model (TAM) adding two constructs (i.e. personal innovativeness and perceived risk). The study was based on three different views: the current Internet banking adoption rate; the impacts of perceived usefulness, perceived ease of use, perceived risk and personal innovativeness in information technology; and the potential impacts on the strategic activity of banking organisations operating in Hong Kong. The results from t-test and Pearson’s correlation confirmed the positive influences of chosen factors on the adoption intention.

) analysed the retail customers’ behaviour of adopting Internet banking in Hong Kong, employing the Technology Acceptance Model (TAM) adding two constructs (i.e. personal innovativeness and perceived risk). The study was based on three different views: the current Internet banking adoption rate; the impacts of perceived usefulness, perceived ease of use, perceived risk and personal innovativeness in information technology; and the potential impacts on the strategic activity of banking organisations operating in Hong Kong. The results from t-test and Pearson’s correlation confirmed the positive influences of chosen factors on the adoption intention.

Using the integrated model of technology acceptance model (TAM) and theory of planned behaviour (TPB), Lee (2009![]() ) conducted an online survey to investigate the customer acceptance behavior for online banking in Taiwan. Among 446 responses, 368 were valid and sufficient to analyse acceptance behavior of customers for online banking in Taiwan. The paper examined the impact of eleven factors on the dependent variable (i.e. customer's intention to use online banking), including seven independent variables (perceived ease of use, perceived benefit, perceived risks, security/privacy, performance, social and time risk, and a group of five control variables (perceived usefulness, attitude, subjective norm, perceived behavior control)). The research model was proved to be suitable for explaining and predicting the usage behavior of customers for online banking. The intention of using online banking was significantly influenced by perceived benefits and five risk faucets with the heavier impact from the latter. The study suggested that risk should be paid more attention than benefits provided by this service. Although perceived benefits and perceived usefulness were expected to have a causal link, the empirical results could not support this relationship.

) conducted an online survey to investigate the customer acceptance behavior for online banking in Taiwan. Among 446 responses, 368 were valid and sufficient to analyse acceptance behavior of customers for online banking in Taiwan. The paper examined the impact of eleven factors on the dependent variable (i.e. customer's intention to use online banking), including seven independent variables (perceived ease of use, perceived benefit, perceived risks, security/privacy, performance, social and time risk, and a group of five control variables (perceived usefulness, attitude, subjective norm, perceived behavior control)). The research model was proved to be suitable for explaining and predicting the usage behavior of customers for online banking. The intention of using online banking was significantly influenced by perceived benefits and five risk faucets with the heavier impact from the latter. The study suggested that risk should be paid more attention than benefits provided by this service. Although perceived benefits and perceived usefulness were expected to have a causal link, the empirical results could not support this relationship.

3.2. Prior Studies on the Acceptance of Using Internet Banking Services

Applying the same method as Lee (2009![]() ); Nasri and Charfeddine (2012

); Nasri and Charfeddine (2012![]() ) examined customer adoption of Internet banking under the Tunisian context, focusing on safety, confidentiality, effectiveness, government support, usefulness, ease of use customer behavior, social norms, and behavior control. Based on 284 respondents, the paper confirmed the validity of TAM and TPB models in analyzing customer acceptance for Internet banking, henceforward developed appropriate strategies to boost up the adoption of this service. The paper revealed significant factors influencing the usage intention of Internet banking in Tunisia, which were security and privacy to protect consumers' personal and financial information, government support, legal framework and infrastructure.

) examined customer adoption of Internet banking under the Tunisian context, focusing on safety, confidentiality, effectiveness, government support, usefulness, ease of use customer behavior, social norms, and behavior control. Based on 284 respondents, the paper confirmed the validity of TAM and TPB models in analyzing customer acceptance for Internet banking, henceforward developed appropriate strategies to boost up the adoption of this service. The paper revealed significant factors influencing the usage intention of Internet banking in Tunisia, which were security and privacy to protect consumers' personal and financial information, government support, legal framework and infrastructure.

Zandhessami and Geramayeh (2014![]() ) conducted empirical investigations to determine the factors that influence users' adoption of Internet banking. The paper employed DEMATEL technique (Decision - Making Trial and Evaluation Laboratory) to measure the determinants of Internet banking using data of Iranian firms. The findings revealed trust as the most important factor.

) conducted empirical investigations to determine the factors that influence users' adoption of Internet banking. The paper employed DEMATEL technique (Decision - Making Trial and Evaluation Laboratory) to measure the determinants of Internet banking using data of Iranian firms. The findings revealed trust as the most important factor.

Considering internet banking as an efficient service which is able to ease customers’ daily transactions, Foon and Fah (2011![]() ) investigated behavioral intention towards internet banking adoption by conducting surveys in Kuala Lumpur under the UTAUT framework. With 200 respondents, the paper illustrated that performance expectancy, effort expectancy, social influence, facilitating condition and trust significantly and positively influenced the intention to use internet banking in Malaysia and they were able to explain 56.6% variance of behavioral attention. Even though the sample size was insufficient to generalize the population in Kuala Lumpur, the findings was able to help banks to understand the behavior of using Internet banking and then to suggest different means to attract more customers to use this service.

) investigated behavioral intention towards internet banking adoption by conducting surveys in Kuala Lumpur under the UTAUT framework. With 200 respondents, the paper illustrated that performance expectancy, effort expectancy, social influence, facilitating condition and trust significantly and positively influenced the intention to use internet banking in Malaysia and they were able to explain 56.6% variance of behavioral attention. Even though the sample size was insufficient to generalize the population in Kuala Lumpur, the findings was able to help banks to understand the behavior of using Internet banking and then to suggest different means to attract more customers to use this service.

Under the circumstance of rapid growth of banking and finance industries, Hanafizadeh, Keating, and Khedmatgozar (2014a![]() ) conducted a systematic review of previous studies on the acceptance of adopting Internet banking during the period 1999-2012. The highlight of this paper was to summarize as well as categorize the system of 165 studies on Internet banking adoption according to three different purposes: to describe the phenomenon (descriptive); to understand the interplay between the factors that drive adoption (relational); or to draw higher level conclusions through a comparison across populations, channels or methods (comparative). The paper comprehensively systemized the sources, the national journals, and the countries being investigated, and the combination of these issues… in order to identify gaps in the rationale for accepting Internet banking and to discuss the main trends for the future research.

) conducted a systematic review of previous studies on the acceptance of adopting Internet banking during the period 1999-2012. The highlight of this paper was to summarize as well as categorize the system of 165 studies on Internet banking adoption according to three different purposes: to describe the phenomenon (descriptive); to understand the interplay between the factors that drive adoption (relational); or to draw higher level conclusions through a comparison across populations, channels or methods (comparative). The paper comprehensively systemized the sources, the national journals, and the countries being investigated, and the combination of these issues… in order to identify gaps in the rationale for accepting Internet banking and to discuss the main trends for the future research.

Sharif and Raza (2017![]() ) emphasized that hedonic motivation, trust, self-efficacy and habit were significant to predict behavioural intention whereas habit and behavioural intention could be used to explain adoption intention of internet banking in Pakistan. Based on the findings, the authors raised up the essential of enhancing customers’ skills of using internet banking as well as the necessity of changing internet banking screens and adding extra innovative interface to attract more customers.

) emphasized that hedonic motivation, trust, self-efficacy and habit were significant to predict behavioural intention whereas habit and behavioural intention could be used to explain adoption intention of internet banking in Pakistan. Based on the findings, the authors raised up the essential of enhancing customers’ skills of using internet banking as well as the necessity of changing internet banking screens and adding extra innovative interface to attract more customers.

3.3. Prior Studies on the Acceptance of Using Mobile Banking Services

Paying attention to the intention of adopting mobile banking, Afshan and Sharif (2016![]() ) conducted a research for the case of Pakistan, using the integration of three previous frameworks UTAUT, TTF and ITM. The CFA and SEM analyses were used to analyze the data gathered from university students. The paper contributed to the existing literature with the following findings: task contribution (TAC) and technology characteristics (TEC) significantly impact task technology fit (TTF); initial trust (IT) played an important role in structural assurance (SA) and familiarity with bank (FB); the combination of task technology fit (TTF), initial trust (IT), and facilitating condition (FC) could impact the adoption intention of mobile banking.

) conducted a research for the case of Pakistan, using the integration of three previous frameworks UTAUT, TTF and ITM. The CFA and SEM analyses were used to analyze the data gathered from university students. The paper contributed to the existing literature with the following findings: task contribution (TAC) and technology characteristics (TEC) significantly impact task technology fit (TTF); initial trust (IT) played an important role in structural assurance (SA) and familiarity with bank (FB); the combination of task technology fit (TTF), initial trust (IT), and facilitating condition (FC) could impact the adoption intention of mobile banking.

Examining mobile banking adoption in Pakistan, the study of Raza, Shah, and Ali (2019![]() ) was unique since it examined the Islamic banking factor using the modified UTAUT model. Except for social influence, this paper revealed that all selected independent variables (performance expectancy, facilitating conditions, effort expectancy, perceived value, habit, and hedonic motivation) had significant and positive impact on the intention to adopt m-banking services. These findings assisted the Islamic banks in Pakistan in implementing appropriate strategies to increase m-banking acceptance and usage.

) was unique since it examined the Islamic banking factor using the modified UTAUT model. Except for social influence, this paper revealed that all selected independent variables (performance expectancy, facilitating conditions, effort expectancy, perceived value, habit, and hedonic motivation) had significant and positive impact on the intention to adopt m-banking services. These findings assisted the Islamic banks in Pakistan in implementing appropriate strategies to increase m-banking acceptance and usage.

Regarding mobile banking’s security among customers, Munoz-Leiva, Climent-Climent, and Liébana-Cabanillas (2017![]() ) added innovation diffusion theory, perceived risk and trust to the classic technology acceptance model (TAM) in order to examine the determinants of acceptance behaviour of mobile banking in Spain. The paper used structural equation modelling (SEM) to analyse the data collected from an online survey. The empirical results revealed attitude as the most significant factor influencing mobile banking usage behaviour while rejected the hypotheses that usefulness and risk directly impact the acceptance of mobile banking applications.

) added innovation diffusion theory, perceived risk and trust to the classic technology acceptance model (TAM) in order to examine the determinants of acceptance behaviour of mobile banking in Spain. The paper used structural equation modelling (SEM) to analyse the data collected from an online survey. The empirical results revealed attitude as the most significant factor influencing mobile banking usage behaviour while rejected the hypotheses that usefulness and risk directly impact the acceptance of mobile banking applications.

Alalwan, Dwivedi, and Rana (2017![]() ) employed structural equation modelling (SEM) and confirmatory factor analysis (CFA) to analyse collected data from 343 valid questionnaires regarding adoption of mobile banking in Jordan. Selected constructs (performance expectancy, effort expectancy, social influence, facilitating conditions, hedonic motivation, price value, and behavioural intention) included in the conceptual framework were built up based on the UTAUT2 (Venkatesh et al., 2012

) employed structural equation modelling (SEM) and confirmatory factor analysis (CFA) to analyse collected data from 343 valid questionnaires regarding adoption of mobile banking in Jordan. Selected constructs (performance expectancy, effort expectancy, social influence, facilitating conditions, hedonic motivation, price value, and behavioural intention) included in the conceptual framework were built up based on the UTAUT2 (Venkatesh et al., 2012![]() ) adding trust as external factor. The empirical results exposed five factors (performance expectancy, effort expectancy, hedonic motivation, price value and trust) as significant factors to capture Jordanian customers’ behaviour intention. The actual adoption of mobile banking could be predicted via both behavioural intention and facilitating conditions.

) adding trust as external factor. The empirical results exposed five factors (performance expectancy, effort expectancy, hedonic motivation, price value and trust) as significant factors to capture Jordanian customers’ behaviour intention. The actual adoption of mobile banking could be predicted via both behavioural intention and facilitating conditions.

3.4. Prior Studies on the Acceptance of Using Banking Services in Vietnam

Following the trend in other Asian countries, digital banking services in Vietnam have great potential for development. The report prepared by McKinsey (Barquin & Vinayak, 2015![]() ) for Asian emerging markets showed a dramatic change in the usage of digital banking services compared to the year 2011. This survey included 700 respondents from Viet Nam. The results disclosed that 41% of Vietnamese customers were using computers or mobile phones for banking transactions. It revealed the strong growing potential in developing digital banking services for Vietnam. However, the current theoretical framework and recent studies in digital banking indicate that the topic of digital banking is still quite new. There is currently no in-depth study on the factors affecting the development of digital banking services for the case Vietnam. From the recent literature review in digital banking for the case of Vietnam, the current research has just been exploiting topics related to electronic banking and mobile banking.

) for Asian emerging markets showed a dramatic change in the usage of digital banking services compared to the year 2011. This survey included 700 respondents from Viet Nam. The results disclosed that 41% of Vietnamese customers were using computers or mobile phones for banking transactions. It revealed the strong growing potential in developing digital banking services for Vietnam. However, the current theoretical framework and recent studies in digital banking indicate that the topic of digital banking is still quite new. There is currently no in-depth study on the factors affecting the development of digital banking services for the case Vietnam. From the recent literature review in digital banking for the case of Vietnam, the current research has just been exploiting topics related to electronic banking and mobile banking.

Lin, Wu, and Tran (2015![]() ) examined the acceptance behavior of Vietnamese customers to use electronic banking services. Usefulness and social influences were found to have significant impact on the acceptance of using these services. The bank's reputation had no impact on the customers’ behaviour. These findings were consistent with the theoretical framework of Technology Acceptance Model (TAM) (Davis, 1986

) examined the acceptance behavior of Vietnamese customers to use electronic banking services. Usefulness and social influences were found to have significant impact on the acceptance of using these services. The bank's reputation had no impact on the customers’ behaviour. These findings were consistent with the theoretical framework of Technology Acceptance Model (TAM) (Davis, 1986![]() ; Davis., 1989

; Davis., 1989![]() ) and Theory of Planned Behavior (TPB) (Ajzen, 1991

) and Theory of Planned Behavior (TPB) (Ajzen, 1991![]() ; Ajzen, 2002

; Ajzen, 2002![]() ; Ajzen 1985

; Ajzen 1985![]() ).

).

With different perspectives on electronic banking, Dinh, Le, and Le (2015![]() ) measured the impact of the e-banking on the performance of Vietnamese commercial banks. The results showed that e-banking services had a positive impact on the profitability, but this impact had a relatively large delay of three years. Due to this large lag, the authors concluded that there was no significant impact of e-banking services on the growth of Vietnamese banks.

) measured the impact of the e-banking on the performance of Vietnamese commercial banks. The results showed that e-banking services had a positive impact on the profitability, but this impact had a relatively large delay of three years. Due to this large lag, the authors concluded that there was no significant impact of e-banking services on the growth of Vietnamese banks.

Using similar methodology to Lin et al. (2015![]() ); Liang (2016

); Liang (2016![]() ) investigated the use of mobile banking in Vietnam and Taiwan and further compared the factors influencing the decision to use this service in these two markets. With a sample of 440 Vietnamese responses and 337 Taiwanese responses, the results based on Confirmatory Factor Analysis (CFA) showed that the intention to use mobile banking services of Vietnamese customers depends on the trend of using banking services and suggestions of people around them. Additionally, ease of use played a key role in explaining the behavior for both Vietnamese and Taiwanese customers. Meanwhile, the facilitating conditions had no impact on the Vietnamese’s intention to use mobile banking services but significantly influenced customers’ behaviour in Taiwan.

) investigated the use of mobile banking in Vietnam and Taiwan and further compared the factors influencing the decision to use this service in these two markets. With a sample of 440 Vietnamese responses and 337 Taiwanese responses, the results based on Confirmatory Factor Analysis (CFA) showed that the intention to use mobile banking services of Vietnamese customers depends on the trend of using banking services and suggestions of people around them. Additionally, ease of use played a key role in explaining the behavior for both Vietnamese and Taiwanese customers. Meanwhile, the facilitating conditions had no impact on the Vietnamese’s intention to use mobile banking services but significantly influenced customers’ behaviour in Taiwan.

In another study on mobile banking services, Nguyen (2011![]() ) expressed that mobile banking services offered by Vietnamese commercial banks were basic, such as providing information and payment system. They had not paid attention to the development of value-added services based on existing mobile banking system, like financial advices or money transfer outside the system. According to the paper, the current mobile banking services was only developed to compete with other banks to retain customers, without focusing on quality, time and security of technology to serve customers better. In terms of utilities that support customers’ financial investment, the mobile banking system of securities companies should also be considered in Vietnam. Although investors' accounts were managed by commercial banks, all other transactions of investors were conducted by securities companies. Currently, Vietnamese securities companies have developed simple mobile banking such as IVR and SMS in comparison with the system to access information about order placement through automatic message reply and short SMS. Some other securities companies have developed mobile banking based on WAP status and Mobile Client Applications, but they are still in the early stages and low security is not high. These analyses confirmed a great potential development for mobile banking services in Vietnam.

) expressed that mobile banking services offered by Vietnamese commercial banks were basic, such as providing information and payment system. They had not paid attention to the development of value-added services based on existing mobile banking system, like financial advices or money transfer outside the system. According to the paper, the current mobile banking services was only developed to compete with other banks to retain customers, without focusing on quality, time and security of technology to serve customers better. In terms of utilities that support customers’ financial investment, the mobile banking system of securities companies should also be considered in Vietnam. Although investors' accounts were managed by commercial banks, all other transactions of investors were conducted by securities companies. Currently, Vietnamese securities companies have developed simple mobile banking such as IVR and SMS in comparison with the system to access information about order placement through automatic message reply and short SMS. Some other securities companies have developed mobile banking based on WAP status and Mobile Client Applications, but they are still in the early stages and low security is not high. These analyses confirmed a great potential development for mobile banking services in Vietnam.

Although a number of studies in the existing literature have examined the determinants of the behavioural intention of new technology, with a substantial attention paid on banking sector, the research conducted for digital banking services appear limited, especially under the context of Vietnam. This clarifies that there is a lack of empirical research understanding the impact of factors on consumers’ intentions to adopt and to use digital banking services in Vietnam. Hence, this paper can be considered as one of the first studies using the modified UTAUT model (UTAUT2) to find out the factors influencing Vietnamese customer’s intention as well as usage behaviour of digital banking services.

4. RESEARCH METHODOLOGY

4.1. Data Collection

Data was gathered from a survey conducted in Vietnam, mainly from two biggest cities Hanoi and Ho Chi Minh. A total of 400 questionnaires was distributed, of which 241 were returned giving a response rate of 58%. The questionnaire was designed with two parts: demographic and constructs questions. Demographic questions included gender, age, income, and education of the respondents. The eight constructs wereperformance expectancy (PE), effort expectancy (EE), social influences (SI), facilitating conditions (FC), hedonic motivation (HM), price value (PV), habit (HT), and trust (TR). Each factor was evaluated via indices as presented in Table 2. The questions were based on Likert seven-point scales ranging from 1 to 7 with a response continuum from “strongly disagree” to “strongly agree”. The reliability of the questionnaire was measured and assessed by Cronbach’s alpha α in IBM© SPSS© Statistics version 20 (IBM© Corp., Armonk, NY, USA).

4.2. Research Model

Technology acceptance has been analysed in the various studies based on different models in this field. The previous common models are comprising of Theory of Reasoned Action – TRA (Fishbein & Ajzen, 1975![]() ) Theory of Planned Behaviour – TPB (Ajzen, 1991

) Theory of Planned Behaviour – TPB (Ajzen, 1991![]() ) and Technology Acceptance Model – TAM (Davis, Bagozzi, & Warshaw, 1989

) and Technology Acceptance Model – TAM (Davis, Bagozzi, & Warshaw, 1989![]() ). In specific, the TRA model identified behaviour performed by an individual as the intention of this individual to perform the behaviour. Two determinants of behavioural intention were attitudes towards individual’s act or behaviour and subjective norm. TPB added Perceived Behavioral Control (PBC) ass one extra factor to the previous two determinants and was able to explain both the intention to use and the usage behavior. PBC was defined as “people’s perception of the ease or difficulty of performing the behavior of interest” (Ajzen, 1991

). In specific, the TRA model identified behaviour performed by an individual as the intention of this individual to perform the behaviour. Two determinants of behavioural intention were attitudes towards individual’s act or behaviour and subjective norm. TPB added Perceived Behavioral Control (PBC) ass one extra factor to the previous two determinants and was able to explain both the intention to use and the usage behavior. PBC was defined as “people’s perception of the ease or difficulty of performing the behavior of interest” (Ajzen, 1991![]() ). Within the TAM’s framework, behavioural intention to use a technology was the major determinant of actual acceptance of technology. Two factors significantly correlated with the behavioural intention were the factor Perceived Usefulness (PU) and Perceived Ease of Use (PEU). According to Davis et al. (1989

). Within the TAM’s framework, behavioural intention to use a technology was the major determinant of actual acceptance of technology. Two factors significantly correlated with the behavioural intention were the factor Perceived Usefulness (PU) and Perceived Ease of Use (PEU). According to Davis et al. (1989![]() ) PU was defined as “the prospective user’s subjective probability that using a specific application system will increase his or her jobs performance”; while PEOU was defined as “the degree to which the prospective user expects the target system to be free of effort”.

) PU was defined as “the prospective user’s subjective probability that using a specific application system will increase his or her jobs performance”; while PEOU was defined as “the degree to which the prospective user expects the target system to be free of effort”.

Unified Theory of Acceptance and Use of Technology – UTAUT was introduced later by Venkatesh, Morris, Davis, and Davis (2003![]() ) combining the ideas of the previous models and theories of user acceptance, four determinants of the intention to use technology are performance expectancy (PE), effort expectancy (EE), social influence (SI), and facilitating conditions (FC). The behavioral intention and facilitating conditions subsequently determine the technology usage. Additionally, the model also considers the impact of four moderator indicators (i.e. gender, age, experience, and voluntariness use). Nevertheless, the UTAUT model reveals its own limitations since its conception for an organisational context as opposed to a consumer one. Also, some important factors for the usage and success measurement for technology have not mentioned in this model, such as task-technology fit, technology performance, or user satisfaction (Merhi, Hone, & Tarhini, 2019

) combining the ideas of the previous models and theories of user acceptance, four determinants of the intention to use technology are performance expectancy (PE), effort expectancy (EE), social influence (SI), and facilitating conditions (FC). The behavioral intention and facilitating conditions subsequently determine the technology usage. Additionally, the model also considers the impact of four moderator indicators (i.e. gender, age, experience, and voluntariness use). Nevertheless, the UTAUT model reveals its own limitations since its conception for an organisational context as opposed to a consumer one. Also, some important factors for the usage and success measurement for technology have not mentioned in this model, such as task-technology fit, technology performance, or user satisfaction (Merhi, Hone, & Tarhini, 2019![]() ).

).

Venkatesh et al. (2012![]() ) modified the UTAUT model (known as Extended Unified Theory of Acceptance and Use of Technology or UTAUT2) by considering consumer technologies. Three constructs are added to the original UTAUT model, comprising of hedonic motivation (HM), price value (PV), and habit (HT). Therefore, under the theory of UTAUT 2, performance expectancy (PE), effort expectancy (EE), social influence (SI), facilitating conditions (FC), hedonic motivation (HM), price value (PV), habit (HT) determine the behavioral intention to use technology, whilst consumer behavioral intention and habit can be used to explain the actual usage of technology. Meanwhile, age, gender, and experience are also added as moderator variables to explain the dimensions from selected constructs to behavioral intention and use of technology. The UTAUT 2 model has been employed by recent studies and proved its equivalency in analyzing the adoption and usage of customers in terms of new technology (Arenas, Peral, & Ramón, 2015

) modified the UTAUT model (known as Extended Unified Theory of Acceptance and Use of Technology or UTAUT2) by considering consumer technologies. Three constructs are added to the original UTAUT model, comprising of hedonic motivation (HM), price value (PV), and habit (HT). Therefore, under the theory of UTAUT 2, performance expectancy (PE), effort expectancy (EE), social influence (SI), facilitating conditions (FC), hedonic motivation (HM), price value (PV), habit (HT) determine the behavioral intention to use technology, whilst consumer behavioral intention and habit can be used to explain the actual usage of technology. Meanwhile, age, gender, and experience are also added as moderator variables to explain the dimensions from selected constructs to behavioral intention and use of technology. The UTAUT 2 model has been employed by recent studies and proved its equivalency in analyzing the adoption and usage of customers in terms of new technology (Arenas, Peral, & Ramón, 2015![]() ; Megadewandanu, Suyoto, & Pranowo, 2016

; Megadewandanu, Suyoto, & Pranowo, 2016![]() ). Taking advantage of the modified UTAUT framework, this paper proposed the research model presented in Figure 1.

). Taking advantage of the modified UTAUT framework, this paper proposed the research model presented in Figure 1.

The measurements of selected variables are described in Table 1. The paper used Statistical Packages for Social Science (SPSS) to analyse the data conveyed from the questionnaires within the UTAUT2 framework. The results of regression models will be used to confirm the hypotheses among the variables in the model.

4.3. Research Hypotheses

Based on the prior studies in the literature and the context of Vietnamese banking system, this paper proposed the following hypotheses:

H1. Performance expectancy positively influences Vietnamese customers’ intention to adopt digital banking services.

H2. Effort expectancy positively influences Vietnamese customers’ intention to adopt digital banking services.

H3. Social influences positively influence Vietnamese customers’ intention to adopt digital banking services.

H4. Facilitating conditions positively influence Vietnamese customers’ adoption of digital banking services.

H5. Hedonic motivation positively influences Vietnamese customers’ intention to adopt digital banking services.

H6. Price value positively influences Vietnamese customers’ intention to adopt digital banking services.

H7. Habit positively influences Vietnamese customers’ intention to adopt digital banking services.

H8. Trust positively influences Vietnamese customers’ intention to adopt digital banking services.

Table-1. Measurement of research indices.

| Constructs | Index | Description |

| Performance Expectancy (PE) | PE1 | Digital banking services are diverse and useful for my job. |

| PE2 | Using digital banking services help me accomplish tasks more quickly. | |

| PE3 | Using digital banking services help me accomplish tasks more easily. | |

| PE4 | Using digital banking services would help me to increase my productivity. | |

| Effort Expectancy (EE) | EF1 | I would find digital banking services easy to use. |

| EF2 | I think I would learn to use digital banking services quickly. | |

| EF3 | My interaction with digital banking services is clear and understandable. | |

| EF4 | It would be easy for me to become skillful at using digital banking services. | |

| Social Influences (SI) | SI1 | People who are important to me think that I should use digital banking services. |

| SI2 | People in my environment think that I should use digital banking services. | |

| SI3 | Most people in my environment use digital banking services. | |

| SI4 | Via social media I think I should use digital banking services. | |

| Facilitating Conditions (FC) | FC1 | I have the resources necessary to use digital banking services. |

| FC2 | I have knowledge necessary to use digital banking services. | |

| FC3 | A digital banking service is compatible with other technologies I use. | |

| FC4 | I get help from others when I have difficulties using digital banking services. | |

| Hedonic Motivation (HM) | HM1 | Using digital banking services is convenient. |

| HM2 | Using digital banking services is enjoyable. | |

| HM3 | Using digital banking services is entertaining | |

| Price Value (PV) | PV1 | Using digital banking services save money compared to other banking services. |

| PV2 | I think using digital banking services is expensive. | |

| PV3 | Digital banking services offer better value for my money. | |

| Habit (HT) | HT1 | Using digital banking services has become natural to me. |

| HT2 | I am addicted to using digital banking services. | |

| HT3 | I think I must use digital banking services. | |

| HT4 | Using digital banking services has become natural to me. | |

| Security (SE) | SE1 | I feel assured when making digital banking transactions. |

| SE2 | I believe that my personal information will be protected when using digital banking services. | |

| SE3 | I believe that digital banking transactions can be done accurately. | |

| Trust (TR) | TR1 | I trust that my personal information will be secured when using digital banking services. |

| TR2 | I trust the procedure of settling transactions of digital banking services. | |

| TR3 | I trust that technical problems of digital banking services will be rarely happened | |

| TR4 | I feel assured that legal and technological structures adequately protect me from problems of digital banking services. | |

| Self-reliance (SR) | SR1 | I can proficiently use smart devices. |

| SR2 | I can access the Internet anywhere and anytime. | |

| SR3 | I do online banking services every day. | |

| Behavioral Intention of Digital Banking Services (BI) | BI1 | I will use digital banking services when I have sufficient conditions. |

| BI2 | I believe I will use/keep using digital banking services. | |

| BI3 | I will use more digital banking services in the future. | |

| BI4 | I will certainly introduce digital banking services to others. | |

| Usage Intention of Digital Banking Services (UI) | UI1 | Internal and external transfers, overseas transfers |

| UI2 | Bill payments | |

| UI3 | Online loans | |

| UI4 | Online savings | |

| UI5 | Insurance and investment | |

| UI6 | Financial management |

Ajzen (1991![]() ) and Venkatesh et al. (2003

) and Venkatesh et al. (2003![]() ); Venkatesh et al. (2012

); Venkatesh et al. (2012![]() ) revealed that behavioural intention has strong influence on the actual usage behaviour. In other words, the intention of digital banking services adoption can be predicted by the willingness of the customers to use them. Together with behaviour intention, habit and facilitating conditions can be also considered to examine the impact on usage intention. Consequently, this study hypothesized these relationships as follows:

) revealed that behavioural intention has strong influence on the actual usage behaviour. In other words, the intention of digital banking services adoption can be predicted by the willingness of the customers to use them. Together with behaviour intention, habit and facilitating conditions can be also considered to examine the impact on usage intention. Consequently, this study hypothesized these relationships as follows:

H9. Habit positively influences Vietnamese customers’ usage of digital banking services.

H10. Facilitating conditions positively influence Vietnamese customers’ usage of digital banking services.

H11. Behavioural intention positively influences Vietnamese customers’ usage of digital banking services.

5. EMPIRICAL RESULTS AND ANALYSIS

5.1. Demographic Analysis

Figure-2. Characteristics of respondents.

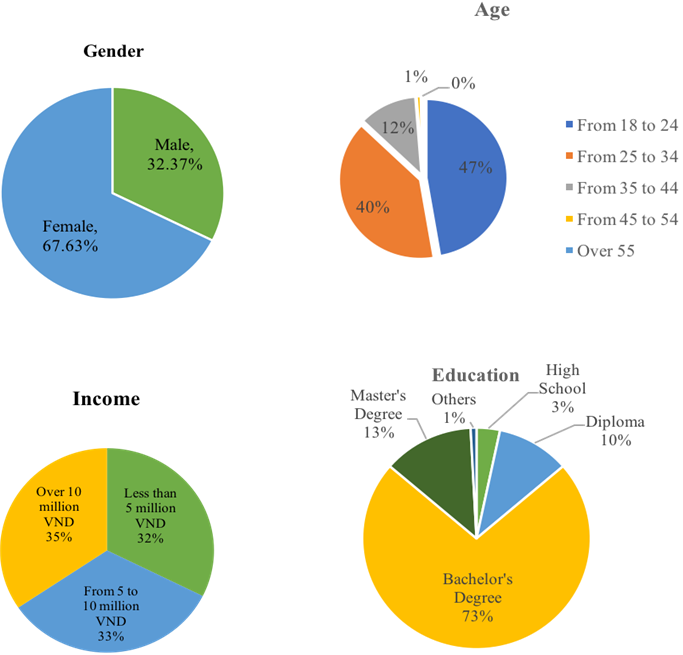

The characteristics of respondents are shown in Figure 2. The questionnaires were distributed to respondents from 18 to over 55 years old. The demographic profile shows that many respondents were found in the range of 18 to 24 years old (counted for 47%). The second largest group was in the range of 25 to 34 years old (counted for 40%). In terms of gender, two-third (67.6%) of the respondents were female. Only one-third (32.4%) were male. Among 241 respondents, 73% were equipped bachelor’s degree whereas only 4% were found to have educational foundation below diploma.

The demographic results indicated that the selected sample was mainly female, and skewed toward a young and highly educated generation. However, the income of the respondents was allocated equally for three ranges: less than 5 million VND (32%), from 5 to 10 million VND (33%), and over 10 million VND (35%).

Table-2. Descriptive statistics.

Indices |

Mean |

Std. Deviation |

Skewness |

Kurtosis |

Cronbach’s α |

PE |

5.475 |

1.661 |

-1.311 |

0.957 |

0.966 |

PE1 |

5.349 |

1.694 |

-1.067 |

0.418 |

|

PE2 |

5.660 |

1.742 |

-1.475 |

1.258 |

|

PE3 |

5.461 |

1.791 |

-1.258 |

0.639 |

|

PE4 |

5.432 |

1.745 |

-1.226 |

0.741 |

|

EF |

5.377 |

1.493 |

-1.140 |

0.900 |

0.962 |

EF1 |

5.506 |

1.568 |

-1.178 |

0.945 |

|

EF2 |

5.241 |

1.576 |

-0.835 |

0.012 |

|

EF3 |

5.228 |

1.517 |

-0.941 |

0.466 |

|

EF4 |

5.531 |

1.638 |

-1.329 |

1.227 |

|

SI |

4.611 |

1.501 |

-0.553 |

-0.381 |

0.879 |

SI1 |

4.614 |

1.714 |

-0.566 |

-0.487 |

|

SI2 |

4.452 |

1.805 |

-0.482 |

-0.757 |

|

SI3 |

4.527 |

1.787 |

-0.537 |

-0.700 |

|

SI4 |

4.851 |

1.701 |

-0.737 |

-0.225 |

|

FC |

4.923 |

1.332 |

-0.735 |

0.386 |

0.757 |

FC1 |

5.361 |

1.620 |

-1.068 |

0.454 |

|

FC2 |

5.369 |

1.605 |

-1.088 |

0.598 |

|

FC3 |

4.037 |

1.836 |

-0.096 |

-1.048 |

|

HM |

5.383 |

1.613 |

-1.185 |

0.560 |

0.939 |

HM1 |

5.568 |

1.699 |

-1.369 |

0.983 |

|

HM2 |

5.365 |

1.688 |

-1.185 |

0.630 |

|

HM3 |

5.216 |

1.738 |

-0.999 |

0.145 |

|

HT |

4.686 |

1.654 |

-0.486 |

-0.619 |

0.852 |

HT1 |

4.531 |

1.930 |

-0.481 |

-0.950 |

|

HT2 |

4.801 |

1.858 |

-0.669 |

-0.600 |

|

HT3 |

4.705 |

1.875 |

-0.518 |

-0.881 |

|

HT4 |

4.705 |

1.875 |

-0.518 |

-0.881 |

|

PV |

4.562 |

1.457 |

-0.391 |

-0.378 |

0.718 |

PV1 |

5.199 |

1.711 |

-0.933 |

0.135 |

|

PV2 |

4.141 |

1.888 |

-0.175 |

-1.098 |

|

PV3 |

4.344 |

1.862 |

-0.406 |

-0.921 |

|

TR |

4.822 |

1.471 |

-0.659 |

-0.114 |

0.962 |

TR1 |

4.730 |

1.599 |

-0.532 |

-0.491 |

|

TR2 |

4.801 |

1.634 |

-0.636 |

-0.333 |

|

TR3 |

4.826 |

1.579 |

-0.689 |

-0.131 |

|

TR4 |

4.747 |

1.658 |

-0.576 |

-0.469 |

|

TR5 |

4.776 |

1.592 |

-0.584 |

-0.261 |

|

TR6 |

5.050 |

1.578 |

-0.731 |

-0.130 |

|

BI |

5.371 |

1.601 |

-1.049 |

0.433 |

0.957 |

BI1 |

5.382 |

1.694 |

-1.101 |

0.533 |

|

BI2 |

5.432 |

1.741 |

-1.075 |

0.257 |

|

BI3 |

5.461 |

1.628 |

-1.081 |

0.425 |

|

BI4 |

5.212 |

1.737 |

-0.810 |

-0.300 |

|

UI |

4.840 |

1.514 |

-0.511 |

-0.495 |

0.891 |

UI1 |

5.357 |

1.757 |

-1.067 |

0.287 |

|

UI2 |

5.469 |

1.772 |

-1.182 |

0.500 |

|

UI3 |

4.141 |

1.961 |

-0.172 |

-1.130 |

|

UI4 |

4.946 |

1.906 |

-0.719 |

-0.620 |

|

UI5 |

4.207 |

1.972 |

-0.266 |

-1.086 |

|

UI6 |

4.917 |

1.904 |

-0.738 |

-0.523 |

5.2. Descriptive Statistics

The descriptive statistics results (in tables) indicate the values of mean and standard deviation for all factors of interest. The means ranged from the lowest at 4.56 (price value) to the highest at 5.48 (performance expectancy). They can be considered as relative high values, implying that the respondents mostly responded “agree” to “strongly agree” with the questions in the questionnaires. Additionally, the responses seemed to not fluctuate largely when the standard deviations were low (i.e. the values ranged within 1.33 and 1.66).

According to Tabachnick and Fidell (2007![]() ) skewness and kurtosis values can be evaluated as normal if they lie within the range [-2.58, +2.58]. The skewness and kurtosis of ten selected variables fluctuated from -1.311 to -0.391 and from -0.619 to +0.957, respectively. Therefore, all the items in the sample were considered as normally distributed.

) skewness and kurtosis values can be evaluated as normal if they lie within the range [-2.58, +2.58]. The skewness and kurtosis of ten selected variables fluctuated from -1.311 to -0.391 and from -0.619 to +0.957, respectively. Therefore, all the items in the sample were considered as normally distributed.

To evaluate the steadiness among the items of the specified constructs, Cronbach’s alpha was used. The previous studies ranked the Cronbach’s alpha into four categories based on its value: excellent reliability (above 0.90), high reliability (between 0.70 and 0.90), moderate reliability (between 0.50 and 0.70), and low reliability (below 0.50). Table 2 shows that the Cronbach’s alpha values of selected factors ranged from 0.718 to 0.966, with PE yielding the highest value while PV yielding the lowest value among all other variables. The results implied internal consistency or adequate convergence while all the constructs satisfactorily met the requirement for high reliability with no alpha values smaller than 0.70 (Pallant, 2016![]() ; Sekaran, 2003

; Sekaran, 2003![]() ).

).

Table-3. Correlation matrix.

| Variables | BI |

PE |

EF |

SI |

FC |

HM |

PV |

HT |

TR |

| BI | 1.000 |

||||||||

| PE | 0.811 |

1.000 |

|||||||

| EF | 0.798 |

0.843 |

1.000 |

||||||

| SI | 0.545 |

0.542 |

0.539 |

1.000 |

|||||

| FC | 0.711 |

0.677 |

0.733 |

0.522 |

1.000 |

||||

| HM | 0.860 |

0.845 |

0.834 |

0.624 |

0.761 |

1.000 |

|||

| PV | 0.615 |

0.591 |

0.596 |

0.615 |

0.646 |

0.670 |

1.000 |

||

| HT | 0.686 |

0.615 |

0.648 |

0.596 |

0.642 |

0.689 |

0.592 |

1.000 |

|

| TR | 0.675 |

0.641 |

0.643 |

0.624 |

0.569 |

0.702 |

0.601 |

0.657 |

1.000 |

The results of correlation matrices as shown in Table 3 and Table 4 explain how each of the selected items is associated with the remaining items. Relatively high correlations indicate that two items are associated and will probably be grouped together by the factor analysis. The selected variables in this paper were all positively correlated. According to Table 3, the correlation ranged between 0.522 and 0.860, and the highest correlation was recorded between behavioral intention and hedonic motivation. The correlation values among usage intention, behavioral intention, habit and facilitating conditions are represented in the Table 4. In particular, the correlation ranged from 0.611 to 0.728, implying a strong relationship among variables.

Table-4. Correlation matrix.

Variables |

UI |

BI |

HT |

FC |

UI |

1.000 |

|||

BI |

0.728 |

1.000 |

||

HT |

0.642 |

0.686 |

1.000 |

|

FC |

0.611 |

0.711 |

0.642 |

1.000 |

5.3. Hypotheses Testing Results

To confirm the stated hypotheses on behavioural intention and usage intention of Vietnamese customers, the regression tests were employed.

According to the findings from Table 5, performance expectancy, effort expectancy, hedonic motivation, habit, and trust were five factors which were found to have positive and significant influences on behavioural intention of digital banking services adoption. These findings, subsequently, supported the hypotheses H1, H2, H5, H7, and H8. The model can explain a variance of 77.9% (i.e. adjusted R-square) in the adoption of digital banking services.Table-5. Regression coefficients on behavioural intention.

| Factors | Unstandardized Coefficients |

Standardized Coefficients |

t |

Sig. |

Hypothesis |

Support |

|

B |

Std. Error |

Beta |

|||||

| Performance Expectancy (PE) | 0.204 |

0.062 |

0.212 |

3.285 |

0.001* |

H1 |

YES |

| Effort Expectancy (EE) | 0.118 |

0.070 |

0.110 |

1.686 |

0.093*** |

H2 |

YES |

| Social Influences (SI) | -0.065 |

0.047 |

-0.061 |

-1.402 |

0.162 |

H3 |

NO |

| Facilitating Conditions (FC) | 0.062 |

0.062 |

0.052 |

1.010 |

0.314 |

H4 |

NO |

| Hedonic Motivation (HM) | 0.430 |

0.072 |

0.434 |

5.962 |

0.000* |

H5 |

YES |

| Price Value (PV) | 0.016 |

0.050 |

0.015 |

0.322 |

0.748 |

H6 |

NO |

| Habit (HT) | 0.124 |

0.046 |

0.128 |

2.720 |

0.007* |

H7 |

YES |

| Trust (TR) | 0.087 |

0.052 |

0.080 |

1.671 |

0.096*** |

H8 |

YES |

| (Constant) | 0.227 |

0.208 |

1.092 |

0.276 |

Note: R = 0.887; R-Square = 0.786; Adjusted R-Square = 0.779

Dependent Variable: Behavioural Intention

*, **, and *** denote for significance levels at 1%, 5%, and 10%

Source: Outputs from SPSS 20.

Table-6. Regression coefficients on usage intention.

| Factors | Unstandardized Coefficients |

Standardized Coefficients |

t |

Sig. |

Hypothesis |

Support |

|

B |

Std. Error |

Beta |

|||||

| Behavioral Intention (BI) | 0.457 |

0.063 |

0.483 |

7.251 |

0.000* |

H9 |

YES |

| Habit (HT) | 0.216 |

0.056 |

0.236 |

3.857 |

0.000* |

H10 |

YES |

| Facilitating Conditions (FC) | 0.132 |

0.072 |

0.116 |

1.835 |

0.068** |

H11 |

YES |

| (Constant) | 0.725 |

0.255 |

2.845 |

0.005* |

Note: R = 0.758; R-Square = 0.574; Adjusted R-Square = 0.568

Dependent Variable: Usage Intention

*, **, and *** denote for significance levels at 1%, 5%, and 10%

Source: Output from SPSS 20.

The results of further analysis of usage intention are set out in Table 6. It revealed the significant influences of three selected constructs (behavioural intention, habit, and facilitating condition) on the intention of using digital banking services. Successively, the outputs strongly supported the hypotheses H9, H10, and H11.

The following Equation 1 and Equation 2 are derived from the empirical results:

Note: *, **, and *** denote for significance levels at 1%, 5%, and 10%

5.4. The Determinants of Behavioural Intention

The significant impacts of performance expectancy, effort expectancy, hedonic motivation, habit and trust on behavioural intention of Vietnamese customers were verified via the empirical findings in Equation 1. However, the results could not display the significant impact from social influence, facilitating conditions, and price value to behavioural intention.

The positive and significant influence from performance expectancy on behavioural intention implies that adopting digital banking services by customers relies on the probability of enhancing customers’ job performance and assisting customers to accomplish their jobs. This result supported the conclusions of Venkatesh et al. (2012![]() ). In line with the previous findings of Venkatesh et al. (2012

). In line with the previous findings of Venkatesh et al. (2012![]() ) the behaviour of Vietnamese digital banking services adoption was found to have a positive and significant relationship with effort expectancy. As most respondents were from a younger generation, it is likely stress-free for them to accept new and advanced technology in banking services. The significance of these two constructs (performance expectancy and effort expectancy) was consistent with previous studies (Alalwan et al., 2017

) the behaviour of Vietnamese digital banking services adoption was found to have a positive and significant relationship with effort expectancy. As most respondents were from a younger generation, it is likely stress-free for them to accept new and advanced technology in banking services. The significance of these two constructs (performance expectancy and effort expectancy) was consistent with previous studies (Alalwan et al., 2017![]() ; Hanafizadeh, Behboudi, Koshksaray, & Tabar, 2014b

; Hanafizadeh, Behboudi, Koshksaray, & Tabar, 2014b![]() ; Raza et al., 2019

; Raza et al., 2019![]() ).

).

Hedonic motivation was another constructing variable influencing the acceptance of modern banking services (Alalwan et al., 2017![]() ; Raza et al., 2019

; Raza et al., 2019![]() ; Sharif & Raza, 2017

; Sharif & Raza, 2017![]() ). Since digital banking services in Vietnam are considerably new and able to catch up with the current trend of global banking development, it may be evaluated as attractive and enjoyable factor for customers.

). Since digital banking services in Vietnam are considerably new and able to catch up with the current trend of global banking development, it may be evaluated as attractive and enjoyable factor for customers.

Trust works as one of the most important aspect in explaining the acceptance of new banking technology (Alalwan et al., 2017![]() ; Hanafizadeh et al., 2014b

; Hanafizadeh et al., 2014b![]() ; Munoz-Leiva et al., 2017

; Munoz-Leiva et al., 2017![]() ). The questionnaire in this paper covers questions relating to securities, procedure of settling transactions, and technical problem solving. The empirical findings support for the positive and significant impact of trust on adopting behaviour of digital banking services. It implied that the customers trust on the current securities system and ability to accomplish the procedure as well as to solve problems relating to digital banking services in Vietnam.

). The questionnaire in this paper covers questions relating to securities, procedure of settling transactions, and technical problem solving. The empirical findings support for the positive and significant impact of trust on adopting behaviour of digital banking services. It implied that the customers trust on the current securities system and ability to accomplish the procedure as well as to solve problems relating to digital banking services in Vietnam.

Along with the recent expansion of innovations in banking sector, especially the appliance of high technology to build up advanced banking services (such as internet banking, mobile banking…), a positive and significant relationship between the habit of Vietnamese customers and their adoption of using digital banking services is rational. This finding supported the studies of Sharif and Raza (2017![]() ) and Raza et al. (2019

) and Raza et al. (2019![]() ). Due to the variety of modern banking services (such as ATM, POS, SMS Banking, Mobile banking, Internet Banking) exercised by a large number of banks in Vietnam, the consumers take advantage of convenience whilst they are able to deal with many transactions (i.e. transferring money, savings, paying bills…) any time from home. These activities naturally become a habit of the customers.

). Due to the variety of modern banking services (such as ATM, POS, SMS Banking, Mobile banking, Internet Banking) exercised by a large number of banks in Vietnam, the consumers take advantage of convenience whilst they are able to deal with many transactions (i.e. transferring money, savings, paying bills…) any time from home. These activities naturally become a habit of the customers.

5.5. The determinants of Usage Intention