EXISTENCE AND EFFECTIVENESS OF ALTERNATIVE INSTITUTIONS OF DISPUTE RESOLUTION OF INDONESIAN BANKING (LAPSPI) IN THE IMPLEMENTATION OF MEDIATION

1Student of Law Faculty, Sebelas Maret University, Surakarta, Indonesia.

2Lecturer of Law Faculty, Sebelas Maret University, Surakarta, Indonesia.

ABSTRACT

Alternative Institution of Dispute Resolution of Indonesian Banking (LAPSPI) is an institution created to facilitate the resolution of banking disputes. LAPSPI is present and needed along with the increasing economic development in Indonesia. Therefore the writer wants to know the existence and effectiveness of the Alternative Institution of Dispute Resolution of Indonesian Banking (LAPSPI). In this study, it was used descriptive empirical research with qualitative data analysis methods. The location of this research is the Alternative Institution of Dispute Resolution of Indonesian Banking (LAPSPI) and the Financial Services Authority (OJK). The results of this study explained that out of 134 registered disputes handled by LAPSPI, there were 35 disputes resolved through Mediation (dispute resolution was carried out in Jakarta, Ketapang, Padang, Pekanbaru, and Malang), 1 dispute was resolved through the Arbitration service, 6 disputes were still pending, 24 disputes were rejected because they did not meet the requirements, and 68 disputes were returned to the applicant to be resolved through the IDR process. From the above data it can be concluded that the existence and effectiveness of LAPSPI have not met expectations. There are still many requests that are rejected, indicating that there are many people who do not understand what is LAPSPI. Therefore it is the duty of LAPSPI to be able to introduce themselves to the community. In addition, in this case LAPSPI also needs to provide intense education and socialization to the community so that this institution can be better known by them.

Keywords:LAPSPI, Banking, Mediation, Institution, Indonesian, Alternative dispute resolution.

ARTICLE HISTORY: Received:12 June 2019 Revised:25 July 2019 Accepted:29 August 2019 Published:17 October 2019.

Contribution/ Originality:The paper’s primary contribution is finding that LAPSPI is an alternative institution of dispute resolution in Indonesian that can be used by customers to resolve dispute with banks, by offering cheap, fast and efficient dispute resolution channels and handled by competent people in the banking sector.

1. INTRODUCTION

1.1. Background

Indonesia, as one of the developing countries, has a goal to improve national economic equality and national stability towards improving people's welfare, which requires large funds. One source of these funds is derived from community savings that can be fostered through banks and financial institutions (Tjokroamidjojo, 1984![]() ). The main function of banking is as an intermediary institution or an institution that connects people experiencing excess funds (surplus of funds) with people experiencing shortages of funds (Suprianto, 2002

). The main function of banking is as an intermediary institution or an institution that connects people experiencing excess funds (surplus of funds) with people experiencing shortages of funds (Suprianto, 2002![]() ) as mandated in Article 3 of Law Number 10 of 1998 concerning Amendment to Law Number 7 of 1992 concerning Banking. One of the Bank's other functions is as an agent of development, an institution to support the implementation of national development (Neni, 2010

) as mandated in Article 3 of Law Number 10 of 1998 concerning Amendment to Law Number 7 of 1992 concerning Banking. One of the Bank's other functions is as an agent of development, an institution to support the implementation of national development (Neni, 2010![]() ).

).

In the banking industry, the protection of disadvantaged customers is a huge influence because the customers themselves are the only banking consumers. The banking industry itself is a business that is very closely related to trust. Banks must play an active role in complaints or problems or disputes experienced by their customers, especially in terms of financial transactions. If the problem cannot be solved by the bank, then the customer and the Bank can choose or carry out dispute resolution outside the court or through the court.

Dispute resolution outside the court is a place to resolve problems or disputes without having to go through the proceedings. Besides dispute resolution outside the court or commonly also called alternative dispute resolution, offers convenience for the disputes to resolve disputes or problems by peaceful means. The means of peace referred to include mediation, adjudication, and arbitration. The regulation, supervision, as well as the function of implementing banking mediation, which was originally at BI as the central bank, will then be transferred to the Financial Services Authority, which is an independent institution and free from interference from other parties, which has the functions, duties or authority of regulating, supervising, examining and investigating at financial services sector. The regulation and supervision are regulated in Law Number 21 Year 2011 concerning the Financial Services Authority which was promulgated on November 22, 2011.

Based on Article 4 of Law Number 21 Year 2011 regarding the Financial Services Authority, it is stated that one of OJK's duties is to provide protection to consumers and / or the public. In order to provide consumer protection, OJK has issued OJK Regulation or Peraturan OJK (POJK) Number 1 / POJK.07 / 2013 dated July 26, 2013 concerning Consumer Protection in the Financial Services Sector. POJK in applying the principle of balance between developing and developing the financial services sector on an ongoing basis and jointly providing protection to consumers and / or the public as customers. POJK contains 3 (three) main aspects, namely increased transparency and disclosure of benefits, risks and costs for products and / or services of Financial Service Business Actors (PUJK), PUJK's responsibility to assess the suitability of products and / or services with the risks faced by financial consumers, simpler procedures and convenience of financial consumers to submit complaints and resolve disputes over PUJK products and / or services.

OJK has issued POJK Number 01 / POJK.07 / 2014 dated January 16, 2014 concerning Alternative Institution of Dispute Resolution (LAPS) in the Financial Services Sector in order to resolve disputes or PUJK products and / or services. With the enactment of POJK Number 1 / POJK.07 / 2013 concerning Consumer Protection in the Financial Services Sector and POJK Number 1 / POJK.07 / 2014 concerning Alternative Dispute Resolution Institutions (LAPS) in the Financial Services Sector, this is done in the context of efforts to protect and empower customers which is realized by the existence of infrastructure to handle and resolve various complaints and customer complaints. Therefore, on April 28, 2015, associations in the field of Banking, namely the National Bank Association (PERBANAS), the State Owned Banks Association (HIMBARA), the Regional Development Banks Association (ASBANDA), the Indonesian Sharia Bank Association (ASBISINDO), the Association of International Indonesian Banks (PERBARINDO) established the Alternative Institution of Resolution Dispute of Indonesian Banking (LAPSPI) which functions to resolve banking disputes which officially began operating in early 2016 (LAPSPI, 2017![]() ).

).

Settlement of consumer complaints through the Banking Institutions often does not meet agreement between the two parties so that to overcome this it requires an Alternative Institution of Dispute Resolution that is handled by people who understand and are able to resolve disputes in the banking world quickly, cheaply, fairly, and efficiently. From these problems then the LAPSPI was established. Based on its background, LAPSPI has 3 (three) services that can be used, namely Mediation, Adjudication, and Arbitration. The three types of services have different rules and procedures. Of the three services, mediation is more widely used.

OJK has accommodated around 14,980 questions from the public, 6,781 information, and 569 complaints from the public. Of these the most complaints were in the Banking sector in 2016. Based on data from the Report of Dispute Handling for one year, 2016 to 2017, only a few of the registered cases were successfully resolved by LAPSPI especially through mediation where it was not appropriate with the number of complaints that registered in LAPSPI. Of the 34 (thirty-four) cases that registered, only 13 (thirteen) cases were processed and of 13 (thirteen) cases, only 4 (four) cases met the settlement of dispute, 6 (six) cases did not meet the settlement and 3 (three) cases are still being processed by LAPSPI. From the explanation of the problem above, the writer is interested in discussing "The Existence and Effectiveness of Alternative Institutions of Dispute Resolution of Indonesian Banking (LAPSPI) in the Implementation of Mediation".

2. RESEARCH METHOD

The research type used in this study is empirical legal research. Soerjono Soekanto said that empirical legal research is research based on certain methods, systematic and thinking which aimed at studying one or several specific social phenomena by analyzing them (Soerjono, 2010![]() ). The nature of the research used is descriptive in accordance with the problems and objectives in this study.

). The nature of the research used is descriptive in accordance with the problems and objectives in this study.

The types and sources of data used in compiling this legal research are:

a. Primary data is data obtained and collected directly from the field or also called basic data (Soerjono, 2010![]() ) which is the object of research. As for what is included in the primary data in this study are the parties involved in dispute resolution through the mediation of the Alternative Institution of Dispute Resolution of Indonesian Banking (LAPSPI), as follows:

) which is the object of research. As for what is included in the primary data in this study are the parties involved in dispute resolution through the mediation of the Alternative Institution of Dispute Resolution of Indonesian Banking (LAPSPI), as follows:

- Chairperson and Executive Director of Alternative Institution of Dispute Resolution of Indonesian Banking (LAPSPI).

- Deputy Director of the Consumer Services of Financial Services Authority (EPK OJK) and staff.

b. Secondary data in this study is data obtained from information or knowledge obtained indirectly including official documents, books, research results in the form of reports (Soerjono, 2010![]() ).

).

In this study, it was used qualitative data analysis by using, classifying and selecting data obtained from field research, then related to theories, principles and legal norms obtained from library studies.

3. RESEARCH RESULTS AND DISCUSSION

Before discussing the Existence and Effectiveness of Alternative Institution of Dispute Resolution of Indonesian Banking (LAPSPI) in the Implementation of Mediation, the author will first discuss the process of dispute resolution regitstration through LAPSPI. According to Mr. Himawan Edhy Subiantoro, one of the informants in this study, there are 2 ways that can be taken to be able to request LAPSPI service facilities, namely:

- Disputes that occur before the agreement: The parties must include the dispute resolution clause through LAPSPI or known as Pacta de Compromittendo in the agreement to be signed.

- Disputes that occur after the agreement: The parties must agree together to resolve the dispute through LAPSPI. The requirement is to make a Mediation Agreement, Adjudication Agreement or Arbitration Agreement using LAPSPI Rules and Procedures. This method is also called Acta de Compromisse.

Facilities or methods of dispute resolution at LAPSPI that will be discussed in this study are mediation methods. The mediation method can be carried out if the consumer complaint to the Bank but does not meet a dispute resolution. According to Article 1 paragraph 1 of Regulation Number 01 of 2017 concerning Regulations and Procedures for Mediation, the definition of mediation is: "How to settle disputes outside the court through a negotiation process at LAPSPI to obtain a peace agreement with the assistance of a mediator".

Dispute resolution through mediation by LAPSPI is carried out by the parties based on good faith and dignity and without coercion from any party. Some of the reasons for choosing mediation through LAPSPI by the parties to settle the dispute are:

- LAPSPI Mediator is able to help resolve the parties' problems fairly, quickly, cheaply and efficiently.

- LAPSPI Mediator is professional in the Banking industry who understand the Banking world well and has mediation skills and has national mediators.

- Mediation through LAPSPI is conducted closed to the public so that confidentiality can be maintained (LAPSPI, 2017

).

).

In addition mediation can be used at each stage of dispute resolution, which is when:

- After deliberation which has failed.

- During the adjudication process, the decision has not been made.

- When the arbitrator is single, the Arbitral Tribunal offers peace efforts at the first trial.

- Before a court judge starts a case review (in accordance with Supreme Court Regulation No. 1 of 2016).

- During the arbitration process / trial has not been dropped (BAPMI, 2006).

Mediation in dispute resolution processed by LAPSPI has not met expectations. This is evident from existing data. OJK has accommodated around 14,980 questions from the public, 6,781 information, and 569 complaints from the public. Of that number, the most complaints were in the Banking sector in 2016. Based on data from the Report on the Results of Dispute Handling for one year, 2016 to 2017, from a number of cases that were submitted were only partially successfully resolved by LAPSPI, especially through mediation. This is not in accordance with the number of complaints that registered in LAPSPI. Of the 34 (thirty four) cases that came in, only 13 (thirteen) cases were processed and out of 13 (thirteen) cases, only 4 (four) cases encountered dispute resolution, 6 (six) cases did not encounter dispute resolution and 3 (three) LAPSPI is still being processed. The following authors describe the data regarding the Report on the Results of Dispute Handling during 2016, 2017 and 2018 as follows:

Table-1. Report on the results of dispute handling by LAPSPI period January 1 to December31, 2016.

| No | Number of cases | The case has been resolved by LAPSPI |

The process is postponed in LAPSPI |

The case is rejected |

Back to IDR process |

Total |

| A. | Credit | |||||

| 1. Auction / Collateral problems | 1 |

0 |

2 |

5 |

8 |

|

| 2. Determination of interest rates | 0 |

0 |

0 |

0 |

0 |

|

| 3. Restructuring | 2 |

0 |

0 |

6 |

8 |

|

| Sub total | 3 |

0 |

2 |

11 |

16 |

|

| B. | Credit card | |||||

| 1. Unrecognized use of a credit card | 1 |

0 |

0 |

1 |

2 |

|

| 2. Payment relief | 2 |

0 |

0 |

5 |

7 |

|

| Sub total | 3 |

0 |

0 |

6 |

9 |

|

| C. | Fund | |||||

| 1. Current / Savings / Deposit problems | 0 |

0 |

0 |

0 |

0 |

|

| 2. Transfer problem | 0 |

0 |

0 |

0 |

0 |

|

| Sub total | 0 |

0 |

0 |

0 |

0 |

|

| D. | e-Banking/ Internet banking/ Mobile banking | |||||

| 1. Fraud/Withdrawal of illegal funds | 2 |

0 |

0 |

0 |

2 |

|

| Sub total | 2 |

0 |

0 |

0 |

2 |

|

| Number of registered complaints | 8 |

0 |

2 |

17 |

27 |

|

Source: Annual report on alternative institution of dispute resolution of Indonesian banking (LAPSPI) Year 2018.

From the Table 1 it can be seen that LAPSPI has received complaints/ disputes from customers totaling 27 complaints/disputes starting from January 1, 2016 to December 31, 2016. For the credit sector is the first place ranks with 16 disputes, followed by 9 credit card disputes, and 2 disputes in the field of e-Banking.

Credit disputes are balanced between auction/collateral issues and restructuring issues, which are 8 disputes each. Credit card disputes are dominated by dispute over principal/interest arrears of 7 disputes, followed by disputes relating to the misuse / use of credit cards by other parties illegally (not recognized by the card holder) of 2 disputes. While disputes in the field of e-Banking are as many as 2 disputes in which both disputes are all related to fraud / illegal withdrawal of customer funds by other parties through internet Banking / mobile Banking (pishing).

Table-2. Report on the results of dispute handling by LAPSPI period January 1 to December 31, 2017.

| No | Number of cases | The case has been resolved by LAPSPI |

The process is postponed in LAPSPI |

The case is rejected |

Back to IDR process |

Total |

| A. | Credit | |||||

| 1. Auction / Collateral problems | 0 |

1 |

8 |

1 |

10 |

|

| 2. Determination of interest rates | 0 |

0 |

0 |

0 |

0 |

|

| 3. Restructuring | 3 |

0 |

4 |

5 |

12 |

|

| Sub total | 3 |

1 |

12 |

6 |

22 |

|

| B. | Credit card | |||||

| 1. Unrecognized use of a credit card | 2 |

0 |

0 |

0 |

2 |

|

| 2. Payment relief | 4 |

1 |

5 |

3 |

13 |

|

| Sub total | 6 |

1 |

5 |

3 |

15 |

|

| C. | Fund | |||||

| 1. Current / Savings /Deposit problems | 0 |

1 |

0 |

2 |

3 |

|

| 2. Transfer problem | 0 |

0 |

0 |

2 |

2 |

|

| Sub total | 0 |

1 |

0 |

4 |

5 |

|

| D. | e-Banking/ Internet banking/ Mobile banking | |||||

| 1. Fraud/Withdrawal of illegal funds | 1 |

1 |

0 |

2 |

4 |

|

| Sub total | 1 |

1 |

0 |

2 |

4 |

|

| Number of registered complaints | 10 |

4 |

17 |

15 |

46 |

|

Note: There is 1 customer with mediation services (paid), and 1 customer with arbitration services (paid).

From the Table 2, it can be seen that LAPSPI has received 46 complaints / disputes from the Customer as many as 46 disputes which registered from January 2017 to 31 December 2017. For the credit sector, it is in the first place ranks with 22 disputes, followed by 15 credit card disputes, 5 disputes in the field of third party funds and disputes in the field of e-Banking which are 4 disputes.

From the Table 3, it can be seen that LAPSPI has received 73 complaints / disputes from Customers starting from January 1, 2018 to June 30, 2018. For the credit sector it is in the first rank with 38 disputes, followed by 24 credit card disputes, 6 disputes in the field of e-banking, and 5 disputes in the field of third party funds.

Table-3. Report on the results of dispute handling by LAPSPI period January 1 to June 30, 2018.

| No | Number of cases | The case has been resolved by LAPSPI |

The process is postponed in LAPSPI |

The case is rejected |

Back to IDR process |

Total |

| A. | Credit | |||||

| 1. Auction / Collateral problems | 1 |

1 |

10 |

6 |

18 |

|

| 2. Determination of interest rates | 0 |

0 |

0 |

0 |

0 |

|

| 3. Restructuring | 5 |

0 |

4 |

11 |

20 |

|

| Sub total | 6 |

1 |

14 |

17 |

38 |

|

| B. | Credit card | |||||

| 1. Unrecognized use of a credit card | 3 |

0 |

0 |

1 |

4 |

|

| 2. Payment relief | 6 |

1 |

5 |

8 |

20 |

|

| Sub total | 9 |

1 |

5 |

9 |

24 |

|

| C. | Fund | |||||

| 1. Current / Savings /Deposit problems | 0 |

1 |

0 |

2 |

3 |

|

| 2. Transfer problem | 0 |

0 |

0 |

2 |

2 |

|

| Sub total | 0 |

1 |

0 |

4 |

5 |

|

| D. | e-Banking/ Internet banking/ Mobile banking | |||||

| 1. Fraud/Withdrawal of illegal funds | 4 |

0 |

0 |

2 |

6 |

|

| Sub total | 4 |

0 |

0 |

2 |

6 |

|

| Number of registered complaints | 19 |

3 |

19 |

32 |

73 |

|

Note: There are 1 customer with mediation services (paid), and 1 customer with arbitration services (paid).

Table-4. Report on the results of dispute handling by LAPSPI period January 1, 2016 to June 30, 2018.

| No. | Number of cases | The case has been resolved by LAPSPI |

The process is postponed in LAPSPI |

The case is rejected |

Back to IDR process |

Total |

| A. | Credit | |||||

| 1. Auction / Collateral problems | 2 |

1 |

12 |

8 |

23 |

|

| 2. Determination of interest rates | 0 |

1 |

0 |

0 |

1 |

|

| 3. Restructuring | 9 |

1 |

6 |

20 |

36 |

|

| Sub total | 11 |

3 |

18 |

28 |

60 |

|

| B. | Credit card | |||||

| 1. Unrecognized use of an credit card | 7 |

1 |

0 |

4 |

12 |

|

| 2. Payment relief | 8 |

0 |

5 |

26 |

39 |

|

| Sub total | 15 |

1 |

5 |

30 |

51 |

|

| C. | Fund | |||||

| 1. Current / Savings /Deposit problems | 4 |

2 |

1 |

3 |

10 |

|

| 2. Transfer problem | 0 |

0 |

0 |

2 |

2 |

|

| Sub total | 4 |

2 |

1 |

5 |

12 |

|

| D. | e-Banking/ Internet banking/ Mobile banking | |||||

| 1. Fraud/Withdrawal of illegal funds | 6 |

0 |

0 |

5 |

11 |

|

| Sub total | 6 |

0 |

0 |

5 |

11 |

|

| Number of registered complaints | 36 |

6 |

24 |

68 |

134 |

|

Note: There are 2 customers with mediation services (paid), and 1 customer with arbitration services (paid).

From the Table 4, it can be seen that LAPSPI has received complaints / disputes from customers totaling 134 complaints / disputes starting from January 1, 2016 to June 30, 2018. For the credit sector which is the first rank there are 60 disputes, followed by credit card disputes which is 51 disputes, 12 disputes of third party funds, and 11 disputes in the field of e-banking.

Of the 134 disputes resolved by LAPSPI, the following is the explanation:

- Resolved through mediation as many as 35 disputes (dispute resolution is carried out in Jakarta, Ketapang, Padang and Pekanbaru, Malang).

- Resolved through Arbitration service as many as 1 dispute.

- The case which is postponed (in the process at LAPSPI) as many as 6 disputes.

- Rejected because they did not meet the requirements which is 24 disputes.

- Returned to the applicant to be resolved through the process of IDR which is 68 disputes (LAPSPI, 2018).

In the recapitulation of disputes for the period January 2016 to August 2018, there were 134 Banking dispute requests spread across several regions in Indonesia. The recapitulation of complaints by region is:

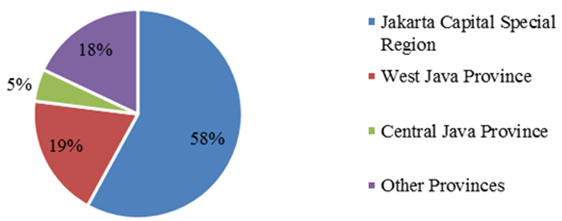

Figure-1. Recapitulation of disputes based on region in 2016-2018.

Source: Annual report on alternative institution of Indonesian banking (LAPSPI) year 2018.

From the results of the recapitulation assessment of disputes based on regions in the period of 2016 to 2018, it can be seen that the majority of banking dispute requests are in Java, especially in DKI Jakarta with 58% acquisition, then 19% in West Java Province, 5% in Central Java Province and 18% for other provinces.

In accordance with the mandate of OJK Circular Letter (SEOJK) Number 54 / SEOJK.07 / 2016, OJK has the obligation to monitor LAPS performance. OJK monitors reporting and complies with LAPS principles every 6 months. Furthermore, if necessary, OJK can request additional documents / information from LAPS. OJK will conduct an analysis and formulate the results of the analysis, as well as carry out a final assessment based on weighting and rating scale. Then OJK will submit the assessment results to LAPS. In the event that there are LAPS which, based on OJK's assessment, have not applied LAPS principles, OJK will provide guidance to the relevant LAPS. Coaching is done within a period of 6 months and can be extended for the next 6 months. OJK can remove LAPS from the LAPS List if guidance has been carried out but it still has not applied the LAPS principles. OJK will announce LAPS which is excluded from LAPS List on OJK website and national circulation newspaper.

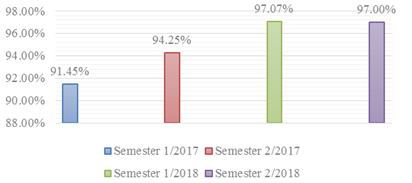

Based on the assessment given by the OJK for 4 (four) semesters starting from semester I & II in 2017 until semester I & II in 2018, LAPSPI received a good rating which is as follows:

Figure-2. Assessment of LAPSPI performance.

Source: Annual report on alternative institution of dispute resolution of Indonesian banking (LAPSPI) year 2018.

Based on the graphic evaluation of LAPSPI's performance conducted by OJK, it can be seen an increase in LAPSPI's performance. In semester 1 of the 2017 LAPSPI score 91.45%, then in semester 2 of the 2017 LAPSPI score 92.25%. Furthermore, in semester 1 of the 2018 period the value obtained by LAPSPI was 97.07%, and in semester 2 of 2018 the value was 97.00%. Based on this, LAPSPI is increasingly showing significant progress in terms of its performance based on regions.

According to Mr. Sardjito as Deputy Commissioner of the OJK EPK said that LAPSPI is one of the LAPS (Alternative Dispute Resolution Institutions) that resolves consumer disputes very well. This is based on the 90 percent report. This means that consumer disputes that are resolved 90 percent are very good in my opinion and also very good according to the OJK, according to LAPSPI's core values, so LAPSPI is credible. This opinion was conveyed at the LAPSPI seminar on 30 April 2018.

From the data stated above, it can be seen that the existence and effectiveness of LAPSPI in handling disputes, especially with mediation channels are good enough, it is proven from the number of 134 cases submitted, LAPSPI successfully resolved 34 cases through mediation. However, the existence of LAPSPI is still uneven because LAPSPI is only well known in the islands of Java. This is evidenced from the recapitulation data of disputes in 2016 to 2018 in which the dominance of cases is in Java, especially DKI Jakarta that reached 58%. This proves the lack of LAPSPI existence outside of Java. There are also other things that must be considered about the data that has been presented above where there are 24 cases that were rejected because they did not meet the requirements. It also proves the lack of understanding of the parties related to the conditions that must be completed. It is LAPSPI's duty to provide education to the public to be able to introduce LAPSPI as an institution that can be chosen in terms of banking dispute resolution.

4. CONCLUSION

Along with the increasing economic development in Indonesia, problems in the economic field, especially finance, are also experiencing an increasing impact. The problem is also inseparable from the dispute between the parties. The intended parties are financial institutions namely the Bank and also customers or other parties. Most of these problems are resolved through litigation or judicial channels. Even though banking dispute resolution can also be resolved through non-litigation channels. Settlement of banking disputes through non-litigation can be traveled through the Alternative Institution of Dispute Resolution of Indonesian Banking (LAPSPI). The presence of LAPSPI will make it easy for the parties to the dispute to resolve the problem peacefully. However, the existence and effectiveness of LAPSPI is still considered lacking. From the beginning of its establishment around April 2015 to 2018, from the data obtained by LAPSPI, there are 134 disputes have been received. Of the 134 requests, only 35 cases could be resolved through mediation. Alternative Institutions of Dispute Resolution or Indonesian Banking, or better known as LAPSPI, should provide more education to the public regarding the existence of a non-court dispute resolution agency. The form of education or understanding that can be given can be done through seminars, outreach or even utilizing the internet as a means of introducing LAPSPI.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: Both authors contributed equally to the conception and design of the study. |

REFERENCES

BAPMI, 2006. When using mediation (website). Available from http://www.bapmi.org/in/mediation_intro.php [Accessed August 1, 2019].

LAPSPI, 2017. Background of LAPSPI (Website). Available from http://lapspi.org/profile/#latarbelakang [Accessed May 21, 2018].

LAPSPI, 2017. Definitions, terms and registration of mediation (website). Available from https://lapspi.org/mediasi/#mediasi-definisi [Accessed May 21, 2018].

LAPSPI, 2018. Annual Report on Alternative Institutions of Dispute resolution of Indonesian Banking (LAPSPI) Year of 2018. pp: 47.

Neni, S.I., 2010. Introduction to Indonesian banking law. Bandung: Refika Aditama. pp: 14.

Soerjono, S., 2010. Introduction to legal research. Jakarta: University of Indonesia Publisher (UI-Press), 51: 5-6.

Suprianto, 2002. Prudential banking principles in the environment of rural banks (BPR) in the framework of disbursing and loans. Thesis, Surabaya, Airlangga University Postgraduate Program. pp: 3.

Tjokroamidjojo, B., 1984. Introduction to development administration. Jakarta: LP3JES. pp: 100.

Views and opinions expressed in this article are the views and opinions of the author(s), International Journal of Asian Social Science shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |