THE EFFECTS OF BUSINESS EFFICIENCY TO DISCLOSE INFORMATION OF SUSTAINABLE DEVELOPMENT: THE CASE OF VIETNAM

1,2Hanoi University of Industry, Vietnam

3 Vietnam institute of Indian and Southwest Asian Studies, Vietnam Cademy of Social, Vietnam

4,5 National Economics University, Vietnam.

ABSTRACT

This paper studies the impact of business efficiency on the level of sustainable development information disclosure of Vietnamese enterprises by using path structure model with the data of 294 enterprises listed on the stock market in 3 years from 2015 to 2017. Research results show that the level of sustainable development information disclosure of Vietnamese enterprises listed on the stock market is still quite low. This study has identified factors that positively influence the level of sustainable development information disclosure including business efficiency, firm size, Big4 and the number of members of the board of directors. The negative influencing factors with the level of sustainable development information disclosure are financial leverage and business sector. Based on the research results, the study propose some recommendations to improve the level of sustainable development information disclosure of enterprises in Vietnam: (i) promote disclosure of sustainable development for their benefit to businesses; (ii) supplement and improve the current legal system in Vietnam to create a solid legal basis for the implementation of sustainable development information disclosure.

Keywords:Information disclosure, Business efficiency, Sustainable development, Social responsibility, Financial leverage, Vietnam.

JEL Classification: G02; G03; G04.

ARTICLE HISTORY: Received:15 February 2019 Revised:18 March 2019 Accepted:23 April 2019Published:8 May 2019.

Contribution/ Originality:The contribution of this study is to apply path structure model with the data of 294 enterprises listed on the Vietnam stock market in 3 years from 2015 to 2017. This study has identified factors that positively influence the level of sustainable development information disclosure including business efficiency, firm size, Big4 and the number of members of the board of directors. The negative influencing factors with the level of sustainable development information disclosure are financial leverage and business sector.

1. INTRODUCTION

In the 1990s, enterprises studies began to care about the inclusion of social and environmental aspects and trends in enterprises' reports, while in the past the public only interested in information of financial statements. How to develop the economy but not harm the environment? That is the big question that must be answered and the solution is sustainable development. Sustainable development is currently an indispensable trend in the world that large organizations such as the United Nations, European Union, and developed countries such as the US, UK, Germany, and so on are interested in and implement. However, in developing countries and underdeveloped countries, small enterprises are concerned about economic growth instead of the implementation of social responsibility or towards sustainable development because of some limitations. Therefore, it is necessary to have empirical studies, surveys, and assessments on the relationship between business efficiencyand sustainable development.

Research on the relationship between business efficiencyand sustainable development are variety which attracts the attention of many leaders, managers, and researchers in many countries around the world. The impact of sustainable development information disclosure on business efficiency is different between the study of McWilliams and Siegel (2000![]() ) which investigated 524 enterprises in the US and the research of Nelling and Webb (2009

) which investigated 524 enterprises in the US and the research of Nelling and Webb (2009![]() ) which investigated more than 600 US enterprises. Burhan and Rahmanti (2012

) which investigated more than 600 US enterprises. Burhan and Rahmanti (2012![]() ) use data of 32 companies listed on the Indonesian stock market from 2006 - 2009 showed a positive relationship between business efficiency and sustainable development information. However, there are also studies that have not found the relationship between business efficiency and sustainable development information disclosure such us (Gnanaweera and Kunori, 2018

) use data of 32 companies listed on the Indonesian stock market from 2006 - 2009 showed a positive relationship between business efficiency and sustainable development information. However, there are also studies that have not found the relationship between business efficiency and sustainable development information disclosure such us (Gnanaweera and Kunori, 2018![]() ) with the investigation of 85 enterprises listed on the Tokyo and Japan stock exchanges from 2008 to 2014. In sum, there have been many studies on the relationship between sustainable development information and business efficiency. However, there is still many controversy about the outcome of this relationship.

) with the investigation of 85 enterprises listed on the Tokyo and Japan stock exchanges from 2008 to 2014. In sum, there have been many studies on the relationship between sustainable development information and business efficiency. However, there is still many controversy about the outcome of this relationship.

In Vietnam, the issue of sustainable development is a very new issue with little enterprises’ concern. In 2015, when Ministry of Finance issued Circular 155, on information disclosure on the stock market, reporting of sustainable development was really interested in many researchers. However, the studies in Vietnam on this issue is only explanatory studies which clarify the report on the sustainable development and lack of empirical studies. Previous studies mainly on social responsibility information, for example (Hoang et al., 2018![]() ) which investigate the impact of diversity in the board of directors on the announcement of social responsibility of enterprises listed in Vietnam stock market from 2008 to 2010. Research by Ha et al. (2019

) which investigate the impact of diversity in the board of directors on the announcement of social responsibility of enterprises listed in Vietnam stock market from 2008 to 2010. Research by Ha et al. (2019![]() ) which investigated listed companies on the Vietnamese stock exchange and indicated the factors affecting social information disclosure to business efficiency. Research on the relationship between social responsibility and financial efficiency by Trang and Yekini (2014

) which investigated listed companies on the Vietnamese stock exchange and indicated the factors affecting social information disclosure to business efficiency. Research on the relationship between social responsibility and financial efficiency by Trang and Yekini (2014![]() ) investigated the 20 largest enterprises listed on Hanoi and Ho Chi Minh Stock Exchange from 2010 to 2012 and the results show that there is a relationship between social responsibility and financial efficiency.

) investigated the 20 largest enterprises listed on Hanoi and Ho Chi Minh Stock Exchange from 2010 to 2012 and the results show that there is a relationship between social responsibility and financial efficiency.

Thus, base on the literature review of international and domestic studies, the authors found the gap of previous studies that are: (i) only focused on influencing factors as well as the level of social responsibility information disclosure instead of sustainable development information disclosure; (ii) the relationship between the social responsibility information disclosure and business efficiency are different. Therefore, it is necessary to expand the research on the effect of business efficiency on sustainable development information of companies listed on the Vietnamese stock market. (iii) new points in this study are that business efficiency was an intermediate variable, structural regression estimation will result in a more comprehensive and complete result, with firm size large enough in the period of 2015-2017.

2. THEORETICAL BASIC

2.1. Some Concepts

According to Brundtland's report presented at the World Environment Development Committee in 1987, sustainable development is the development that meets the needs of the existing businesses but not affect the development of future generations. This is considered as one of the most commonly used and acknowledged concepts.

Sustainable development report is the measurement, information disclosure and is responsible for explaining to internal and external stakeholders on the business performance that is towards the sustainable development goals of enterprises.

Sustainable development information disclosure of enterprises includes detailed information disclosure of environment, energy, human resources, products and community-related issues (Hackston and Milne, 1996![]() ). Vietnam also has many businesses which are aware of the importance of information disclosure and transparency of sustainable development information. Because of many different reasons, this information has been published in the Sustainable Development Report, annual report and on the website of the enterprise. Through sustainable development information disclosure, businesses can have great opportunities in attracting investment capital from socially and environmentally responsible investors, reinforcing the confidence of stakeholders in enterprises. The information disclosure of companies listed on the stock market must ensure "full, accurate and timely". Sustainable development information disclosure is acknowledged as a means to minimize information asymmetry and then, helps investors strengthen monitoring role for enterprises.

). Vietnam also has many businesses which are aware of the importance of information disclosure and transparency of sustainable development information. Because of many different reasons, this information has been published in the Sustainable Development Report, annual report and on the website of the enterprise. Through sustainable development information disclosure, businesses can have great opportunities in attracting investment capital from socially and environmentally responsible investors, reinforcing the confidence of stakeholders in enterprises. The information disclosure of companies listed on the stock market must ensure "full, accurate and timely". Sustainable development information disclosure is acknowledged as a means to minimize information asymmetry and then, helps investors strengthen monitoring role for enterprises.

2.2. Theoretical Framework

Sustainable development information disclosure is very useful for stock market members. However, in terms of theoretical basis, the research in this field has not yet agreed to use any general theory; many different theories were used to verify the level of sustainable development information disclosure. The theory that is frequently used are theory of agency, signalling theory, Proprietary Cost Theory, and stakeholder theory.

Theory of agency identifies a representative relationship as a contract whereby one or many people commit to others (representatives) to perform some services on their behalf (Jensen and Meckling, 1976![]() ). In the theory of agency, the owner is a shareholder and the managers are representatives of the shareholders. The relationship between shareholders and representatives will incur a loss due to the difference between the management representative of the enterprise and the shareholders. Disagreements between owners and representatives can be limited by providing detailed, transparent information about the company. Several factors related to theory of agency are firm size, financial leverage, profitability.

). In the theory of agency, the owner is a shareholder and the managers are representatives of the shareholders. The relationship between shareholders and representatives will incur a loss due to the difference between the management representative of the enterprise and the shareholders. Disagreements between owners and representatives can be limited by providing detailed, transparent information about the company. Several factors related to theory of agency are firm size, financial leverage, profitability.

Signaling theory indicates that asymmetric information between businesses and investors leads to an adverse choice for investors. To avoid this situation, enterprises voluntarily disclose sustainable development information and give positive signals to the market (Watts and Zimmerman, 1990![]() ). According to this theory, the larger the enterprise is, the more asymmetric information is. In addition, the enterprise with higher profitability tends to disclose more information to provide positive signals for investors about growth prospects, thereby positively impact on stock prices of enterprises.

). According to this theory, the larger the enterprise is, the more asymmetric information is. In addition, the enterprise with higher profitability tends to disclose more information to provide positive signals for investors about growth prospects, thereby positively impact on stock prices of enterprises.

Proprietary cost is seen as an important limitation of the sustainable development information disclosure and disclosure more information to investors can damage the company's competitive in the market. Darrough (1993![]() ) argued that firms that restrict information disclosure to avoid reducing their competitive although capital mobilization costs may be higher. Small enterprises are very sensitive, if the more sustainable development information is disclosed, the more detrimental the competitive advantage of the company in the market will be. Previous studies also consider costs derived from gathering and preparing information as an obstacle to voluntarily disclose more information. According to this theory, scale and profitability encourage companies to disclose more information to reduce these costs.

) argued that firms that restrict information disclosure to avoid reducing their competitive although capital mobilization costs may be higher. Small enterprises are very sensitive, if the more sustainable development information is disclosed, the more detrimental the competitive advantage of the company in the market will be. Previous studies also consider costs derived from gathering and preparing information as an obstacle to voluntarily disclose more information. According to this theory, scale and profitability encourage companies to disclose more information to reduce these costs.

The stakeholder theory has many applications including applications in the field of accounting (Freeman, 2010![]() ). According to this, the success of a company depends on the cooperation of stakeholders, because they provide tangible or invisible resources to ensure the existence of any company. These resources can be financial resources (shareholders), operating environment and public services (government agencies), labor (staff). Therefore, the company is responsible for providing information that explains the company's operations to related parties, instead of providing information to the owner only.

). According to this, the success of a company depends on the cooperation of stakeholders, because they provide tangible or invisible resources to ensure the existence of any company. These resources can be financial resources (shareholders), operating environment and public services (government agencies), labor (staff). Therefore, the company is responsible for providing information that explains the company's operations to related parties, instead of providing information to the owner only.

Thus, to what extent the enterprises disclose sustainable development information depend on the measurement of enterprises' managers on costs and benefits related to the transmission of this information to users’ information, importantly the capital investors. The application of agency theory in the framework of information economic theory is more appropriate, in order to assess more deeply the phenomenon and behavior of enterprises in sustainable development information disclosure. Because, in enterprises that have a separation between capital ownership and management that mean a problem of representative and asymmetric information will be exist, thus Sustainable development information disclosure must be implemented.

3. RESEARCH METHODOLOGY

3.1. Research Hypothesis

Based on an overview of the study, inheriting previous studies, the basic presented theories, in this study, the authors made the following research hypotheses as below:

- Business efficiency: The higher the business efficiency is, the more willing the enterprise is to devote financial resources to the development of a sustainable environment that they are operating in, Said et al. (2009

) believed that there is a close and positive relationship between profit and sustainable development information disclosure because it is believed that high-profit enterprises will actively publish information to show the role of enterprises in the welfare of the community and confirming the existence of the business. However, according to Burhan and Rahmanti (2012) it is said that there is a negative relationship between business efficiency and sustainable development information disclosure, while Gnanaweera and Kunori (2018) assumed that there is no relationship between business efficiency and sustainable development information disclosure. Since then, the authors hypothesize that:

) believed that there is a close and positive relationship between profit and sustainable development information disclosure because it is believed that high-profit enterprises will actively publish information to show the role of enterprises in the welfare of the community and confirming the existence of the business. However, according to Burhan and Rahmanti (2012) it is said that there is a negative relationship between business efficiency and sustainable development information disclosure, while Gnanaweera and Kunori (2018) assumed that there is no relationship between business efficiency and sustainable development information disclosure. Since then, the authors hypothesize that:

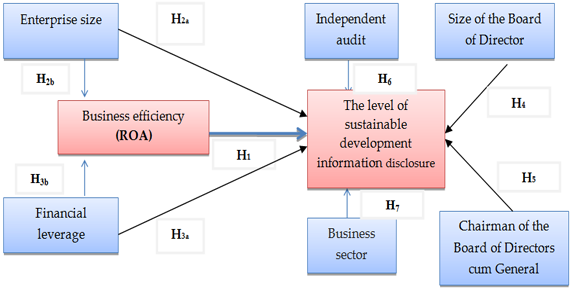

Hypothesis H1: There is a positive and statistically significant relationship between business efficiency (ROA) and the level of sustainable development information disclosure.

- Enterprise size: Large-scale enterprises are always confident about the development prospects of enterprises so they will often voluntarily publish more sustainable development information to create transparency in information, avoiding examinations and inspections of state agencies, as well as increasing the value of enterprises in the eyes of the community and investors. Jennifer Ho and Taylor (2007) found that large-scale companies publish more financial and non-financial information than small companies. On the other hand, there are many studies showing that the scale of enterprises also positively affects the business efficiency according to Kakani et al. (2001); Ha et al. (2019). Since then, the authors hypothesize that:

Hypothesis H2a: There is a positive and statistically significant relationship between business efficiency (ROA) and the level of sustainable development information disclosure.

Hypothesis H2b: There is a positive and statistically significant relationship between firm size and business efficiency (ROA).

- Financial leverage: According to Platonova et al. (2018); Hung et al. (2018) and Branco and Rodrigues (2008) companies with high financial leverage often tends to reveal more information to creditors, suppliers and investors in order to provide more assurance to the parties about their financial obligations. However, there is a study of Jensen and Meckling (1976); Nelling and Webb (2009) which found a negative correlation between financial leverage and the level of sustainable development information disclosure, they believed that the higher financial leverage firms have, the higher probability of default is, so they will reduce information disclosure. On the other hand, many studies have shown that financial leverage has a negative relationship with business efficiency according to Margaritis and Psillaki (2010). Since then the authors hypothesize that:

Hypothesis H3a: There is a negative and statistically significant relationship between financial leverage and the level of sustainable development information disclosure.

Hypothesis H3b: There is a negative and statistically significant relationship between financial leverage and business efficiency (ROA).

The size of the Board of Director: This factor affects sustainable development information disclosure. Barako (2007![]() ) found the relationship between the size of BOD and the level of sustainable development information disclosure. There are two perspectives related to this relationship. The first is that the small size of the BOD will make the information sharing among members and the processing of information easier and faster. However, the second point of view is that the Board of Directors with a larger number of members has a broader knowledge to carry out the advisory tasks, thus the implementation of supervision and advising will be better and sustainable development information will be disclosed more. Thus, the authors hypothesize that:

) found the relationship between the size of BOD and the level of sustainable development information disclosure. There are two perspectives related to this relationship. The first is that the small size of the BOD will make the information sharing among members and the processing of information easier and faster. However, the second point of view is that the Board of Directors with a larger number of members has a broader knowledge to carry out the advisory tasks, thus the implementation of supervision and advising will be better and sustainable development information will be disclosed more. Thus, the authors hypothesize that:

H4: The size of the Board of Director has a positive and statistically significant with the level of sustainable development information disclosure

- Chairman of the Board of Directors cum General Director: According to theory of agency, plurality will decrease the role of control and increase the ability to negotiate bonus for senior managers. In addition, the person has plurality easily dominate power and act opportunistically and harmfully to other shareholders. The study of Fathi (2013) argues that the chairman of the Board of Directors cum CEO has a negative impact on the level of sustainable development information disclosure, which means there is a tendency to hide adverse information. However, the results of the study of Ho and Wong (2001) do not show that the separation of these two positions affects the level of information disclosure. According to agency theory, there is always a conflict between owner and operator. Chairman of the Board represents the owner, executive director represents the executive. Therefore, the role separation is essential for business operations. The healthy environment and properly enforced control will promote information transparency. Although Vietnamese law does not force companies to separate roles between the chairman and the executive director, however, the separation shows a clearer mechanism. Today, some large companies also voluntarily separate the roles of these two positions and publicly announce to the shareholders. Since then the authors hypothesize:

H5: Chairman of the Board of Directors cum General Director has a positive and statistically significant with the level of sustainable development information disclosure.

- Independent audit: Although the preparation and presentation of financial statements are the responsibility of the manager, however, the reputation of audit company can significantly affect sustainable development information disclosure. Auditing company is an indispensable part of the financial statements of listed companies. Previous empirical studies have shown that the quality of auditing companies positively affects the level of sustainable development information disclosure of enterprises. The study of Vu (2012) indicated that the relationship between the size, reputation of the auditing company and the level of sustainable development information disclosure. Since then the authors hypothesize:

H6: Independent audit has a positive and statistically significant with the level of sustainable development information disclosure.

Business sector: Business sector is an important variable that explains the diversity of implementation level and sustainable development information in many studies (Jitaree, 2015![]() ); (Khlif et al., 2015

); (Khlif et al., 2015![]() ). According to Deegan and Gordon (1996

). According to Deegan and Gordon (1996![]() ) some industries may have a strong impact on the relationship between information. For example, the mining and oil and gas industries are more likely to publish social and environmental information than other industries. Moreover, Wallace and Naser (1995

) some industries may have a strong impact on the relationship between information. For example, the mining and oil and gas industries are more likely to publish social and environmental information than other industries. Moreover, Wallace and Naser (1995![]() ) explained that the reason for the difference in SR in some sectors is that each individual company must avoid being penalized for not publishing some of their industry-related issues. Their report may show some special issues that other companies are not required to publish. On the contrary, Owusu-Ansah (1998

) explained that the reason for the difference in SR in some sectors is that each individual company must avoid being penalized for not publishing some of their industry-related issues. Their report may show some special issues that other companies are not required to publish. On the contrary, Owusu-Ansah (1998![]() ) argues that the relationship between sustainable development and industry characteristics can be discovered, and shows some reasons why the practice of disclosing sustainable development of public The company is diversified that is not the same in the nature of the work involved, the type of product line or the variety of products and industry regulations. Since then the authors hypothesize:

) argues that the relationship between sustainable development and industry characteristics can be discovered, and shows some reasons why the practice of disclosing sustainable development of public The company is diversified that is not the same in the nature of the work involved, the type of product line or the variety of products and industry regulations. Since then the authors hypothesize:

H7: Enterprises in the manufacturing industry have a positive relationship with statistical significance with the level of sustainable development information disclosure.

3.2. Research Model

Based on the literature review and research hypotheses, the authors suggest the following research model Figure 1:

Figure-1. Model to study the effect of business efficiency on the level of sustainable development information disclosure.

Source: Calculation of authors based on software Stata.

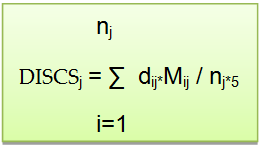

Based on the review studies, the authors performed measuring the level of information disclosure (DISCS) in the order as follows:

Step 1: Identify indexes, authors based on Circular 155/2015, consisting of 6 main categories, and 25 major indexes, will be assigned a value of 1 if declared, and 0 if not declared.

Step 2: Determine the weight of each index (qualitative and quantitative aspects, form), according to the following criteria Table 1:

Table-1. The weight of each index.

Structure |

Content |

Weight |

Content |

The adequacy |

0.45 |

Confidence level |

0.40 |

|

Presentation |

Report form |

0.05 |

Report structure |

0.05 |

|

Interactivity of the report |

0.05 |

Step 3: Based on the level of information provided in Step 2, assess the level of information disclosure at the following five levels Table 2:

Table-2. The level of information disclosure.

Degree evaluation (M) |

||||

1 (Poor) |

2 (Average) |

3 (Fair) |

4 (Good) |

5 (Excellent) |

Step 4: Calculate the average level of disclosure in the annual report, the disclosure index is calculated as follows:

In which:

DISCSj: level of information disclosure in the enterprise's annual report j;

Mij: Level of assessment from level 1-5 of index i in the enterprise's annual report j;

dij = 1 if the information factor i is published in the enterprise’s annual report j;

dij = 0 if the information element i was not published;

nj: number of informational factors that can be declared at enterprise j (n ≤ 25).

Variables in the research model and its measurement are shown in Table 3:

Table-3. Variables in the research model.

Variable |

ID |

Measurement |

Direction of impact |

Business Efficiency |

ROA |

Rate of profit after tax / Asset |

+ |

Size of firm |

SIZE |

Logarithm (total assets) |

+ |

Financial leverage |

LEV |

Debt / Total Assets |

- |

Number of Board members |

NUMBER |

Total number of board members |

+ |

Chairman & General Director |

DUAL |

1- Concurrently 0 - No concurrently |

+ |

Independent auditing |

BIG4 |

|

+ |

Business sector |

INDUSTRY |

1- if the registered field of business of the firm is belonging to the industry sector, 0 - if elsewhere. |

+ |

Source:Own editing.

3.3. Data

In this study, the authors collected data of 294 enterprises listed on Vietnam stock market in 3 years from 2015-2017, so the number of observations is 882. Collected data is calculated into variables in accordance with research requirements by Excel. Finally, calculated variable data is stored and processed for analysis and verification through STATA 13.

4. RESEARCH RESULTS AND DISCUSSION

4.1. Research Results

Statistical data Table 4 shows that among enterprises surveyed, enterprises have profitability ratio (after-tax profit on assets ROA) of 6.6% on average; The average financial leverage ratio of enterprises is 47.8%; Number of members of the Board lowest was 4 and at most 13 people, an average of 6.23 of each enterprise. In the survey sample, there were 28.57% of enterprises with the Chairman and General Director. The number of enterprises with financial statements of Big4 auditing company is 35.71% and the number of manufacturing enterprises accounts for 72.45% of the total research samples.

Table-4. Statistics describe independent variables.

Variables |

Number of observation |

Mean |

Standard deviation |

Minimum value |

Maximum value |

DISCS |

882 |

35.9005 |

28.6893 |

0 |

98.24 |

ROA |

882 |

0.0662 |

0.0902 |

-0.99 |

0.72 |

SIZE |

882 |

28.2002 |

1.5325 |

25.58 |

34.72 |

LEV |

882 |

0.4784 |

0.2216 |

0.01 |

0.97 |

NUMBER |

882 |

6.2381 |

1.6683 |

4 |

13 |

DUAL |

882 |

0.2857 |

0.4520 |

0 |

1 |

BIG4 |

882 |

0.3583 |

0.4798 |

0 |

1 |

INDUSTRY |

882 |

0.7245 |

0.4470 |

0 |

1 |

Source: Calculation of authors based on software Stata.

According to the results of Table 5, The level of sustainable development information disclosure of enterprises averaged 35.90%, in which 25.87% in 2015, 38.03% in 2016 and 42.80% in 2017. Thus, the level of sustainable development information disclosure of Vietnamese enterprises have been improved and increased year by year. This result also shows that enterprises have had an interest in the level of sustainable development information disclosure and especially after Circular 155 takes effect. However, this result indicates that the level of sustainable development information disclosure of listed companies in Vietnam stock market is still relatively low compared to requirements and regulations.

Table-5. Summary table of the level of sustainable development information disclosure by year.

Year |

Number of observation |

Mean |

Standard deviation |

Median |

2015 |

294 |

26.87 |

28.95 |

21.02 |

2016 |

294 |

38.03 |

27.75 |

37.06 |

2017 |

294 |

42.80 |

27.06 |

37.10 |

Trung bình |

35.90 |

28.69 |

37.04 |

Source: Authors calculated from Stata 13.0.

Table 6 shows the correlation coefficients between variables for the purpose of examining the close correlation between independent variables and dependent variables. At the same time, this result to eliminate factors that may lead to multicollinearity phenomenon before running the regression model. The correlation coefficient between the independent variables in the model has no pairs with absolute values greater than 0.8. In the correlation coefficient matrix between the independent variables and the dependent variable, the lowest coefficient is -0,3506 between ROA variable and financial leverage variable (LEV), the highest coefficient is 0.4659 between size of firm variables (SIZE) and Big4 control variable. Therefore, when using the regression model, it is less likely to encounter the multicollinearity phenomenon.

Table-6. Correlation matrix.

DISCS |

ROA |

SIZE |

LEV |

NUMBER |

DUAL |

BIG4 |

INDU STRY |

|

DISCS |

1 |

|||||||

ROA |

0.1475 |

1 |

||||||

SIZE |

0.4105 |

-0.0991 |

1 |

|||||

LEV |

0.0037 |

-0.3506 |

0.4294 |

1 |

||||

NUMBER |

0.1921 |

-0.003 |

0.2801 |

0.0811 |

1 |

|||

DUAL |

0.0251 |

-0.054 |

-0.0701 |

0.0496 |

-0.0858 |

1 |

||

BIG4 |

0.4207 |

0.0468 |

0.4659 |

0.1208 |

0.1627 |

-0.0015 |

1 |

|

INDUSTRY |

-0.1375 |

-0.0501 |

-0.0797 |

-0.026 |

-0.1539 |

0.0867 |

-0.1267 |

1 |

Source: Authors calculated from Stata 13.0.

Table-7. Multivariate regression results by the structure.

Hypothesis |

Structural |

Coef. |

Std. Err. |

z |

P-value |

|

H1 |

DISCS <- |

ROA |

38.224 |

9.703 |

3.94 |

0.000 |

H2a |

DISCS <- |

SIZE |

6.569498 |

0.6843739 |

9.6 |

0.000 |

H3a |

DISCS <- |

LEV |

-18.84806 |

4.354744 |

-4.33 |

0.000 |

H4 |

DISCS <- |

NUMBER |

1.040222 |

0.5145389 |

2.02 |

0.043 |

H5 |

DISCS <- |

DUAL |

4.781448 |

1.82472 |

2.62 |

0.009 |

H6 |

DISCS <- |

BIG4 |

14.96268 |

1.945305 |

7.69 |

0.000 |

H7 |

DISCS <- |

INDUSTRY |

-4.670942 |

1.860842 |

-2.51 |

0.012 |

_cons |

-152.708 |

17.945 |

-8.51 |

0.000 |

||

H2b |

ROA<- |

SIZE |

0.004 |

0.002 |

1.81 |

0.07 |

H3b |

ROA<- |

LEV |

-0.154 |

0.014 |

-10.84 |

0.000 |

_cons |

0.035 |

0.055 |

0.63 |

0.526 |

||

Source: Authors calculated from Stata 13.0.

Table 7 shows that business efficiency has an impact on the level of sustainable development information disclosure with a statistical significance of 5%. Size of firm variable affects positively both business efficiency and the level of sustainable development information disclosure. Besides, Big4 and the number of members of the board of directors have a positive influence on the level of sustainable development information disclosure. However, business sector affects negatively to the level of sustainable development information disclosure.

The results of testing the indicators of the models Table 8 show that the model of measuring the effect of business efficiency on the level of sustainable development information disclosure satisfies the control criteria of the estimated model, the level of explanation of factors is 36.6%.

Table-8. Results of tests.

Fit Indexes |

Standard |

Result |

X2 (df) (Prob > chi2) |

> 0.05 |

0.076 |

RMSEA |

< 0.05 |

0.036 |

CFI |

> 0.90 |

0.989 |

TLI |

> 0.90 |

0.965 |

SRMR |

< 0.05 |

0.014 |

CD |

0.366 |

Source: Authors calculated from Stata 13.0.

4.2. Discuss Research Results

Table-9. Summary of results of the research hypothesis.

Hypothesis |

Structural |

Expected sign |

P-value |

Compare |

Direction of impact |

Conclusion |

|

H1 |

DISCS <- |

ROA |

(+) |

0.000 |

< 0.01 |

(+) |

Accepted |

H2a |

DISCS <- |

SIZE |

(+) |

0.000 |

< 0.01 |

(+) |

Accepted |

H3a |

DISCS <- |

LEV |

(-) |

0.000 |

< 0.01 |

(-) |

Accepted |

H4 |

DISCS <- |

NUMBER |

(+) |

0.043 |

< 0.05 |

(+) |

Accepted |

H5 |

DISCS <- |

DUAL |

(+) |

0.009 |

< 0.01 |

(+) |

Accepted |

H6 |

DISCS <- |

BIG4 |

(+) |

0.000 |

< 0.01 |

(+) |

Accepted |

H7 |

DISCS <- |

INDUSTRY |

(+) |

0.012 |

< 0.01 |

(-) |

Rejected |

H3b |

ROA<- |

SIZE |

(+) |

0.07 |

< 0.1 |

(+) |

Accepted |

H3b |

ROA<- |

LEV |

(-) |

0.000 |

< 0.01 |

(-) |

Accepted |

Source: Authors calculated from Stata 13.0.

From the results of the research in Table 9 some discussions can be made:

- Business efficiency factor gives positive regression results and is statistically significant at 1% to the level of sustainable development information disclosure, in accordance with the original hypothesis. This result is also consistent with the study of Said et al. (2009) but in contrast to research Burhan and Rahmanti (2012) and did not consent to the study of Gnanaweera and Kunori (2018). Thus, business efficiency is a positive factor affecting the level of sustainable development information disclosure of enterprises.

- The size of firm factor is positively related to both business efficiency and level of sustainable development information disclosure and it is statistically significant at 5% level. This result is consistent with the research hypothesis. This study is similar to the results of research by Jennifer Ho and Taylor (2007) and Kakani et al. (2001). Thus, when businesses increase the reasonable scale, they will increase operational efficiency, and it leads enterprises to strengthen sustainable development information disclosure.

- Financial leverage factor is inversely related to both business performance and the level of sustainable development information disclosure and is significant at 5% level. This result is also consistent with the study by Platonova et al. (2018); Branco and Rodrigues (2008); Margaritis and Psillaki (2010); Dang et al. (2019).

- The number of members of the board of director has a positive impact on the level of sustainable development information disclosure, this research result is consistent with hypothesis H5. This result is similar to the research results of Barako (2007) when finding the relationship between the size of members of the Board of Directors and the level of sustainable development information disclosure. However, the results of this study contradict the study by Vu (2012) and Pham and Do (2015). In Vietnam, the operation regulations of listed companies on the stock market regulate the number of members of the board from 4 - 11 people. These members are usually major shareholders or represent major shareholders. From the regression results, the author found that the number of members of the board of directors of each company needs to be consistent with the scale of operation and specific businesses. Small-scale companies that operate simply need fewer members of the Board to quickly make decisions. In contrast, large-scale companies will need many members of the Board to take advantage of the diverse experience and capabilities of their members.

- The factor of Chairman and General Director has a positive influence on the level of sustainable development information disclosure but the results of this study are contrary to the research results by Fathi (2013) and Ho and Wong (2001). Therefore, hypothesis H5 is accepted.

- The regression result of the auditing firm variable in accordance with hypothesis H6. This result shows that enterprises are audited by Big 4, the level of sustainable development information disclosure is higher. Or the audit quality of Big 4 audit enterprises is higher and more stable than other enterprises in audit sector. This comes from the large classification existing in the audit industry in Vietnam and the audit quality of non-Big 4 audit firms (mainly domestic audits) is a remarkable thing to improve the overall quality of auditing and audited financial statements.

- Business has a negative relationship with the level of sustainable development information disclosure. This is not consistent with the hypothesis H7 which was developed. The results of this study contradict the study by Deegan and Gordon (1996) and Wallace and Naser (1995). The reason for this result is that in Vietnamese manufacturing enterprises require more sustainable information disclosure than non-manufacturing sectors (trade, services, finance). So enterprises have not yet sufficient resources to implement sustainable and comprehensive development information.

5. CONCLUSION AND RECOMMENDATIONS

Research results show that the level of sustainable development information disclosure of Vietnamese enterprises listed on the stock market is still quite low. This study has identified factors that positively influence the level of sustainable development information disclosure including business efficiency, firm size, Big4 and the number of members of the board of directors. The negative influencing factors with the level of sustainable development information disclosure are financial leverage and business sector. Based on the research results, the authors propose some recommendations to improve the level of sustainable development information disclosure of enterprises in Vietnam:

First, large-scale and efficient businesses need to be encouraged to promote disclosure of sustainable development for their benefit to businesses. When enterprises publish sustainable development information in separate annual reports and sustainable development reports to stakeholders, it will enhance the brand of the business. Besides, it will help businesses attract and retain talented people, build trust and loyalty of consumers and communities, the support of investors, the credibility of state management agencies, etc. Thereby, it contributes to making businesses more efficient and growing.

Secondly, the research shows that for enterprises in manufacturing industries, consumer goods, etc which published information related to environment and products less when comparing among other industries. This shows that the implementation of sustainable development in a full and true sense is not a simple matter and lies within the ability of instant resolution of most companies. It is hampered because of the limitations of awareness, resource factors, financial resources, technical, highly qualified manpower of Vietnamese enterprises. Therefore, the enterprises need to develop long-term strategies to apply and publish sustainable development information with appropriate steps in different stages. Moreover,the enterprises need to have a long-term strategy in developing and implementing standards.

Third, the Government should continue to supplement and improve the current legal system in Vietnam to create a solid legal basis for the implementation of sustainable development information disclosure. In addition, the government needs to strengthen propaganda to raise awareness about sustainable information disclosure and policies to encourage and support implementation for businesses and organizations.

| Funding: This study is funded by The Hanoi University of Industry, Vietnam. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Barako, D.G., 2007. Determinants of voluntary disclosures in Kenyan companies annual reports. African Journal of Business Management, 1(5): 113-128.

Branco, M.C. and L.L. Rodrigues, 2008. Factors influencing social responsibility disclosure by Portuguese companies. Journal of Business Ethics, 83(4): 685-701.Available at: https://doi.org/10.1007/s10551-007-9658-z.

Burhan, A.H.N. and W. Rahmanti, 2012. The impact of sustainability reporting on company performance. Journal of Economics, Business & Accountancy Ventura, 15(2): 257-272.

Dang, H.N., V.T.T. Vu, X.T. Ngo and H.T.V. Hoang, 2019. Study the impact of growth, firm size, capital structure, and profitability on enterprise value: Evidence of enterprises in Vietnam. Journal of Corporate Accounting & Finance, 30(1): 144-160.Available at: https://doi.org/10.1002/jcaf.22371.

Darrough, M.N., 1993. Disclosure policy and competition: Cournot vs. Bertrand. The Accounting Review, 68(3): 534-561.

Deegan, C. and B. Gordon, 1996. A study of the environmental disclosure practices of Australian corporations. Accounting and Business Research, 26(3): 187-199.Available at: https://doi.org/10.1080/00014788.1996.9729510.

Fathi, J., 2013. The determinants of the quality of financial information disclosed by French listed companies. Mediterranean Journal of Social Sciences, 4(2): 319-336.

Freeman, R.E., 2010. Strategic management: A stakeholder approach. England: Cambridge University Press. pp: 31-43.

Gnanaweera, K. and N. Kunori, 2018. Corporate sustainability reporting: Linkage of corporate disclosure information and performance indicators. Cogent Business & Management, 5(1): 1423872-1423872.Available at: https://doi.org/10.1080/23311975.2018.1423872.

Ha, H.T.V., V.T.T. Van and D.N. Hung, 2019. Impact of social reponsibility information disclosure on the financial performance of enterprises in Vietnam. Indian Journal of Finance, 13(1): 20-36.Available at: https://doi.org/10.17010/ijf/2019/v13i1/141017.

Ha, T.V., N.H. Dang, M.D. Tran, T.T. Van Vu and Q. Trung, 2019. Determinants influencing financial performance of listed firms: Quantile regression approach. Asian Economic and Financial Review, 9(1): 78-90.Available at: https://doi.org/10.18488/journal.aefr.2019.91.78.90.

Hackston, D. and M.J. Milne, 1996. Some determinants of social and environmental disclosures in New Zealand companies. Accounting, Auditing & Accountability Journal, 9(1): 77-108.Available at: https://doi.org/10.1108/09513579610109987.

Ho, S.S. and K.S. Wong, 2001. A study of the relationship between corporate governance structures and the extent of voluntary disclosure. Journal of International Accounting, Auditing and Taxation, 10(2): 139-156.Available at: https://doi.org/10.1016/s1061-9518(01)00041-6.

Hoang, T.C., I. Abeysekera and S. Ma, 2018. Board diversity and corporate social disclosure: Evidence from Vietnam. Journal of Business Ethics, 151(3): 833-852.Available at: https://doi.org/10.1007/s10551-016-3260-1.

Hung, D.N., C.D. Pham and V.T.B. Ha, 2018. Effects of financial statements information on firms’ value: Evidence from Vietnamese listed firms. Investment Management and Financial Innovations, 15(4): 210-218.Available at: https://doi.org/10.21511/imfi.15(4).2018.17.

Jennifer Ho, L.C. and M.E. Taylor, 2007. An empirical analysis of triple bottom-line reporting and its determinants: Evidence from the United States and Japan. Journal of International Financial Management & Accounting, 18(2): 123-150.Available at: https://doi.org/10.1111/j.1467-646x.2007.01010.x.

Jensen, M.C. and W.H. Meckling, 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of financial economics, 3(4): 305-360.Available at: https://doi.org/10.1016/0304-405x(76)90026-x.

Jitaree, W., 2015. Corporate social responsibility disclosure and financial performance: Evidence from Thailand. (Doctor of Philosophy Thesis), University of Wollongong.

Kakani, R.K., B. Saha and V. Reddy, 2001. Determinants of financial performance of Indian corporate sector in the post-liberalization era: An exploratory study (November 2001). National Stock Exchange of India Limited, NSE Research Initiative Paper No. 5.

Khlif, H., A. Guidara and M. Souissi, 2015. Corporate social and environmental disclosure and corporate performance: Evidence from South Africa and Morocco. Journal of Accounting in Emerging Economies, 5(1): 51-69.Available at: https://doi.org/10.1108/jaee-06-2012-0024.

Margaritis, D. and M. Psillaki, 2010. Capital structure, equity ownership and firm performance. Journal of Banking & Finance, 34(3): 621-632.Available at: https://doi.org/10.1016/j.jbankfin.2009.08.023.

McWilliams, A. and D. Siegel, 2000. Corporate social responsibility and financial performance: Correlation or misspecification? Strategic Management Journal, 21(5): 603-609.Available at: https://doi.org/10.1002/(sici)1097-0266(200005)21:5<603::aid-smj101>3.0.co;2-3.

Nelling, E. and E. Webb, 2009. Corporate social responsibility and financial performance: The “virtuous circle” revisited. Review of Quantitative Finance and Accounting, 32(2): 197-209.Available at: https://doi.org/10.1007/s11156-008-0090-y.

Owusu-Ansah, S., 1998. The impact of corporate attribites on the extent of mandatory disclosure and reporting by listed companies in Zimbabwe. The International Journal of Accounting, 33(5): 605-631.Available at: https://doi.org/10.1016/s0020-7063(98)90015-2.

Pham, D.H. and L.T.H. Do, 2015. Factors influencing the voluntary disclosure of Vietnamese listed companies. Journal of Modern Accounting and Auditing, 11(12): 656-676.Available at: https://doi.org/10.17265/1548-6583/2015.12.004.

Platonova, E., M. Asutay, R. Dixon and S. Mohammad, 2018. The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector. Journal of Business Ethics, 151(2): 451-471.Available at: https://doi.org/10.1007/s10551-016-3229-0.

Said, R., Y. Hj Zainuddin and H. Haron, 2009. The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Social Responsibility Journal, 5(2): 212-226.Available at: https://doi.org/10.1108/17471110910964496.

Trang, H.N.T. and L.S. Yekini, 2014. Investigating the link between CSR and financial performance: Evidence from Vietnamese listed companies. British Journal of Arts and Social Sciences, 17(1): 85-101.

Vu, K.B.A.H., 2012. Determinants of voluntary disclosure for Vietnamese listed firms. Doctoral Dissertation, Curtin University.

Wallace, R.O. and K. Naser, 1995. Firm-specific determinants of the comprehensiveness of mandatory disclosure in the corporate annual reports of firms listed on the stock exchange of Hong Kong. Journal of Accounting and Public Policy, 14(4): 311-368.Available at: https://doi.org/10.1016/0278-4254(95)00042-9.

Watts, R.L. and J.L. Zimmerman, 1990. Positive accounting theory: A ten year perspective. The Accounting Review, 65(1): 131-156.

Views and opinions expressed in this article are the views and opinions of the author(s), Asian Economic and Financial Review shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |