CAUSAL RELATIONSHIP BETWEEN FOREIGN DIRECT INVESTMENT AND EXPORT: THE CASE OF DEVELOPING ECONOMIES OF ASIA

1,2,3Economics Departmant, Mustafa Kemal University Tayfur Sökmen Kampüsü; Serinyol/Turkey

ABSTRACT

Utilizing annual data from 1980-2015 for 19 developing economies of Asia, this study examines the causality relation between foreign direct investment and exports. According to the first part of Granger Causality results, China, Republic of Korea, Indonesia, Singapore and Turkey has causality from export to FDI at 1% significance level. Nepal, Sri Lanka, Philippines, Thailand and Oman has a causality from export to FDI at 5% significance level. Finally, it is possible to say that Bangladesh and India has a causality from export to FDI at 10% significance level, while the likelihood value is very close to the 5% significance value. According to the second part of the Granger causality relationship tests Sri Lanka, Indonesia and Turkey has a causality from FDI to export at 1% significance level, India, Nepal and Thailand has a causality from FDI to export at 5% significance level. Finally, the existence of a causality relationship from FDI to Export was found at 10% significance level in Hong Kong, Bangladesh, Singapore, Bahrain, Oman and Saudi Arabia. Briefly export led growth hypothesis is valid for developing economies of Asian countries.

Keywords:Foreign direct investment Export Long-run causality Cross-section dependence Slope heterogeneity.

ARTICLE HISTORY: Received:14 March 2018, Revised:9 April 2018 Accepted:11 April 2018 Published:13 April 2018.

Contribution/ Originality:This study uses new estimation methodology to analyze causal relationship between foreign direct investments and export which considering cross-section dependence and slope heterogeneity in addition to current literature.

1. INTRODUCTION

In the aftermath of the oil crisis of the 1970s, countries all around the world engaged in trade liberalization. Further strengthened by the wave of globalization starting in the early 1980s, this process of liberalization encompassed the free movement of goods as well as the free movement of capital. Investments in terms of capital take the shape of either foreign direct investment (FDI), as in the case of multi-national corporations (MNCs) investing in developing countries, or in the form of portfolio investments, also called as "hot money"

Countries of East, South, and South-East Asia have been a primary focus for multinational companies in recent decades. This is also reflected in the significant share of these countries in exported commodities in world markets; and this was the major factor that encouraged us to examine the relationship between FDI and exports in these regions.

The first part of the study provides an overview of the theoretical approaches to the relationship between FDI and exports. The second part discusses empirical studies examining different aspects of the relationship between the two variables. The third part presents the empirical application. In this section, the analysis of stationarity of variables based on panel data unit root tests is followed by residual cointegration tests, and panel cointegration tests are performed. Panel data used in the study allows the inclusion of a large number of countries, and a large number of time-series observations. In the final section, the empirical results of our analysis are presented.

1.1. Theoretical Approaches

According to the definition provided by the International Monetary Fund (IMF), the concept of foreign direct investment relates to the investment stock in which more than 10% is owned by foreign investors. This usually refers to investments that are made by multinational companies, and affiliates or subsidiaries of these investments are foreign-controlled. Foreign direct investment flow-entry consists of two categories. The first category includes the direct net transfers from parent company to the foreign affiliate through equity or debt; and the second category refers to the earnings that are reinvested by foreign affiliates (De Mooij and Ederveen, 2001).

The foremost consideration for countries to engage in exports is to earn the foreign currency required for financing imports of goods and services from abroad. Exporting is also preferred for achieving economies of scale, specialization, and scope in production, as well as gaining experience in export markets (Prasanna, 2010). Foreign direct investments are widely believed to increase the exports of host countries in several ways: a) by increasing the domestic capital that is required for export, b) by providing the transfer of technologies and new products that play an important role in exports, c) by facilitating access to new, large foreign markets, and finally d) by providing training for the local workforce as well as improved technical and management skills. This is not to say that foreign direct investment is believed to be completely free from any adverse effects on the economy of a country. FDI is usually considered to have the potentially adverse effects, such as: a) reducing domestic savings and investments, b) leading to the transfer of technologies which are at a lower level, or inappropriate for the factor ratios in the host country, c) not necessarily increasing exports, as it targets only the domestic market of the host country, and d) hindering the expansion of the domestic firms in exports (Zhang, 2005).

With regard to the effects of foreign direct investment on the export performance of host countries, debates among economists have not been resolved. The conflict and ambiguity existing within the economic theory and empirical evidence sustain these differences of opinion. Many authors assert that FDI has insignificant or even a negative effect on exports, while others consider FDI to have a strong and positive effect on exports (Gu et al., 2008). Contrary to those authors Jayachandran and Seilan (2010) and Alıcı and Ucal (2003) who have argued that there is no relationship between foreign direct investment and exports, others Prasanna (2010); Gunawardana and Sharma (2009); Liu and Chang (2003); Zhang (2005); Vukšić (2005) and Vural and Zortuk (2011) insist on the existence of a strong positive effect of FDI on export performance. Given the importance accorded to foreign direct investment and exports in economic growth, the relationship between both variables emerges as a significant topic of research (Samsu et al., 2008). The relationship between both variables has been subject to various classifications within the literature, and the following is a detailed account of these classifications.

An important theoretical question regarding the relationship between foreign direct investment and export performance is whether the variables are substitutes or complements. There are two classical studies in the literature considering this discussion: Mundell (1957) and Markusen (1983). In his classical study, Mundell (1957) claimed that international trade and factor mobility are substitutes (Schiff, 2006). Mundell (1957) set out by eliminating the classical assumption which stipulated that factors of production are internationally immobile, and assumed the commodity movements to permit some degree of factor mobility. Thereby, an increase in trade barriers encourages the mobility of factors (factor movements), and an increase in restrictions of factor mobility encourages an increase in trade (Mundell, 1957). This indicates that an increase in factor mobility leads to an increase in the volume of factor flows, and an increase in factor flows causes a decrease in the volume of trade, and vice versa. Consequently, factor mobility will serve as a substitute for trade flows (Goldberg and Klein, 1999). According to Sun (2001) this substitution is caused by the fact that “international flows of factors tend to bring factor prices closer and reduce differences in factor endowments between countries”. Including additional assumptions to the standard model, on the other hand, Markusen (1983) concluded a different relationship between commodity trade and factor trade. In all cases it is indicated that the initial trading equilibrium is not characterized by factor-price equalization. Factor mobility leads to an inflow of the factor used intensively in the production of the export good, and an outflow of factor used intensively in the production of the import good, since each equilibrium includes a country which has relatively higher price for the factor used intensively in the production of its export good. This adds a factor-proportions basis for trade, which complements the other basis for trade. As a result, factor movements between two economies lead to an increase in the volume of commodity trade and leaves countries relatively well-endowed with the factor used intensively in the production of the export good.

In analyzing the effects of FDI on the exports of any country, the first step is to determine whether multinational firms are horizontally or vertically integrated (Kutan and Vukšić, 2007). Horizontal multinational firms set up factories in many countries in order to produce the same goods or services, while vertical multinational firms separate the production process into parts geographically as a final production activity and a center for the production (Zhang and Markusen, 1999). In other words, horizontally integrated multinational firms produce the same product in more than one country, and vertically integrated multinational firms produce different parts of production process in different countries (Kutan and Vukšić, 2007). Horizontal multinationals are modeled by Markusen (1983) and vertical multinationals are modeled by Helpman (1984); Zhang and Markusen (1999). Helpman (1984) asserted that in the development of the general equilibrium theories of international trade multinational firms were not emphasized, while studies dealing with multinational firms remained within the framework of partial equilibrium analysis. For this reason, he analyzed the emergence of multinational firms within a simple general equilibrium model of international trade. In his model, the relative factor rewards-differences in relative factor endowments are emphasized. That is, since firms are trying to maximize their profits and minimize their costs, they make location choices of product lines by taking advantage of the differences in relative factor endowments; and this process eventually leads to the emergence of multinational corporations.

Markusen (1984) developed a general equilibrium model of multinational firm based on economies of multi-plant operation. What the term “economies of multi-plant operation” refers to in this context can be summarized as follows: In an industry of independent owners of the same production facilities, technical or financial advantages are owned by a single owner of two or more production facilities. Sources of multi-plant economies are often found in firm-specific activities, including R&D, advertising, marketing, distribution, and management services. Multinational firms have a tendency to centralize the firm-specific activities. While production facilities are geographically dispersed, therefore, firm-specific activities are centralized in a particular location. The behaviour of multinational firms is summarized as follows Namini and Pennings (2009): in investing abroad, horizontal multinational firms aim to provide services to new markets, while vertical multinational firms aim to reduce production costs.

The enterprises of multinational firms are classified as horizontal foreign direct investment, and vertical foreign direct investment (Braconier et al., 2002). The principal intention of horizontal FDI is to penetrate the domestic market; hence coined as “market-seeking investment” (Demekas et al., 2007). The incentives of this investment are trade costs, market size, and access to local markets (Demekas et al., 2007) and Braconier et al. (2002). In determining places of production, therefore, horizontal FDI prefers locations proximate to the final market. This allows for decrease in trading costs, through the duplication of the production process, and the serving of demand in foreign markets with local production (Johnson, 2006). Vertical FDI, on the other hand, emphasizes the differences in relative factor costs, and decomposes the production stages among different countries (Braconier et al., 2002). The decomposition of production depends on factor intensity. In order to take advantage of differences in factor costs, every stage of production is located where production factor is cheaper (Johnson, 2006). The skilled-labor-intensive stages of production are located in the country with abundant skilled-labor, and the unskilled-labor intensive or resource-intensive stages in appropriate placements that would facilitate taking advantage of differences in relative factor prices (Zhang and Markusen, 1999). Often taking advantage of the relative wealth, vertical FDI attempts to minimize production costs by using cheap labor force. However, though attractive due to differences in factor costs, this type of investment is repelled by trade costs (Demekas et al., 2007).

According to Amiti et al. (2000) forecasts regarding the relationship between FDI and foreign trade depends, first of all, on whether FDI is vertical or horizontal. Whether FDI is horizontal or vertical, in turn, depends on various characteristics of the country. Vertical FDI dominates, for instance, when countries differ significantly in relative factor endowments, while horizontal FDI dominates when countries are similar in size and in relative endowments. Accordingly, theories related to horizontal FDI predict a negative relationship between FDI and foreign trade, while theories related to vertical FDI predict a positive relationship.

In supporting and advocating foreign investors, politicians emphasize two particular effects of foreign direct investment: The first is the direct impact on the productivity of firms that receive foreign investment; and the second is the indirect or spillover effect that is created by foreign owned firms, and that has a positive effect on local firms (Hanousek et al., 2011). In other words, the export performance of subsidiaries of multinational companies in the host country refers to the direct effects of foreign direct investment, while the effects on the exports of the host country through technology transfer and knowledge spillovers refer to the indirect effects of foreign direct investment (Vukšić, 2006). The direct effects are observed through productivity, usually measured by a change in total factor productivity, or by labor productivity of a firm founded by foreign investors. Indirect effects of foreign direct investment in a host country, on the other hand, are the externalities or spillovers to domestic companies, and industries (Hanousek et al., 2011).

Aitken et al. (1997) examined two hypotheses related to export-spillovers: The first hypothesis is about the spillovers arising from all export activities, and the second is about the spillovers that arise only from the export activities of multinational firms. If the spillovers arise from all export activities, a firm will export more as the local concentration of export activity increases, but if the spillovers arise only from the export activities of multinational firms, on the other hand, a firm will export more as the local concentration of export activity by the MNC increases. In the study by Blomström and Kokko (1998) the spillovers arising from the export activities of multinational firms are divided into the categories of “productivity spillovers” and “market access spillovers”, and they define three ways in which productivity spillovers take place: 1) Host country’s local firms imitate or copy the technology used by MNC affiliates operating in the local market; 2) local firms are forced to use the existing technology and resources more efficiently; or 3) local firms are forced to search for new and more efficient technologies since the entry of an affiliate leads to more severe competition. Market access spillovers, on the other hand, occur because the MNC causes local firms to enter the same export markets, either by creating transport infrastructure or by disseminating information about foreign markets that can be used also by local firms.

Hanousek et al. (2011) furthermore, defined the two categories of spillovers of FDI as horizontal and vertical spillovers. Horizontal spillovers take place when there are externalities to domestic companies at intra-industry level. The entry of the multinational firms to the host country causes the productivity of the local firm to increase, as they copy new technologies or hire trained labor force or managers. In contrast, the vertical spillover takes place at the inter-industry level, as in the case of technology transfer to domestic producer or consumer in the production process. Companies that operate in sectors where the foreign enterprise is not operating are affected by the presence of FDI, if they have direct contacts with FDI through the supply and provision of services. The efficiency of domestic companies increases since foreign companies require higher standarts from them.

Finally, Kutan and Vukšić (2007) divided the effects of FDI into two further categories: 1) “supply capacity-increasing effects”, and 2) “FDI-specific effects”. The “supply capacity-increasing effects” occur when the entry of FDI causes the host country’s production capacity to increase, and this production capacity causes the export supply potential to increase. The “FDI-specific effects”, on the other hand, occur since the MNCs possess superior knowledge and technology in production processes and better information about export markets compared with the local firms.

1.2. Empirical Studies

In this section we will first review the debates in the literature regarding the causality between FDI and exports. Liu et al. (2001) to start with, claimed that there is a two-way causal relation between FDI and exports: first, foreign trade –or export- leads to FDI, and naturally FDI leads to trade or export. According to their account, since trade is much easier and less risky than FDI, most firms will initially trade in foreign markets. Over time, as they learn more about the economic, political and social conditions of the foreign country, and gain experience, the home country firms will set up new subsidiaries in foreign markets.

According to the argument by Zhang and Felmingham (2001) the interaction between FDI and export plays a role in determining the foreign trade policy. In the case of one-way and absolute relationship between FDI and exports, that is from export to FDI (EXP → FDI), their claim is that an export-led growth strategy should be followed, together with a liberal foreign trade policy that reduces the costs for the exporters, and encourages exports. If the causality is from FDI to export (FDI → EXP), they claim that FDI in-flow is a prerequisite for the expansion of any country’s exports; and in this case, they recommend that FDI leading to growth in exports over time should be promoted. If there is a two-way (mutual) causal relationship between export and FDI (EXP ↔ FDI) FDI and exports tend to interact throughout the development process; but in the case of no causal relationship between the two variables, they recommend alternative strategies other than the encouragement of FDI, which aim at structural transformation and the growth of economy. According to De Mello (1997) the direction of causality between growth and foreign direct investment is fully dependent on the determinants of foreign direct investment. If there is a strong relationship between FDI determinants and growth, the growth will cause FDI. If the determinants of FDI are in the recipient country, on the other hand, production will increase through the externalities and productivity spillovers that follow FDI. Causality, therefore, may be bi-directional.

Studies investigating the causal relationship between exports and foreign direct investment could be categorized according to their findings. Although they differ with regard to the periods covered as well as the economies analysed, the studies by Dritsaki et al. (2004); Samsu et al. (2008); Liu et al. (2001); Johnson (2006) and Ahmed et al. (2007) have strongly suggested that there is a unidirectional causal relationship from FDI to export, while Temiz and Gökmen (2009) found that the unidirectional causal relationship is from export to FDI. Thestudy by Liu et al. (2002) revealed a bidirectional causal relationship between FDI and exports. Ahmed et al. (2007) examined the causality between FDI and export in the countries of Sub-Saharan Africa, and they concluded that there is bi-directional Granger causality between FDI and exports in Ghana, Kenya, and Nigeria, while there is unidirectional causality that runs from export to FDI in Zambia, and from FDI to export for South Africa. Zhang and Felmingham (2001) on the other hand, examined the relationship between FDI flows and exports for People's Republic of China (PRC) as a whole, and for its provinces. Bi-directional causality was found between PRC’s exports and FDI as a whole. For the provinces, however, the research presented mixed results. Bi-directional causality is found for high FDI concentrated along the Chinese coast, and for low FDI concentrated in Western China, while in the case of the medium FDI in central China causality flows from export to FDI. The studies by Jayachandran and Seilan (2010) and Alıcı and Ucal (2003) on India and Turkey respectively, could not find any causality between FDI and export.

Amiti et al. (2000) is one of the studies that investigate the relationship between FDI and export in terms of whether they are substitutes or complements. They analyzed the relationship of US export (US is the world’s largest exporter of goods and services), and FDI (US is also the largest source of FDI) with 25 partner countries. The results of their study indicate that i) since the horizontal FDI is dominant when countries are similar in terms of size and relative skill endowments, and trading costs are high, FDI and trade are substitutes, ii) since the vertical FDI is dominant when countries are different in terms of size and relative skill endowments, and trading costs are low, FDI and trade are complements. Namini and Pennings (2009) examined the relationship between US multinationals and FDI by using the analytical general equilibrium models; and they concluded that horizontal multinational activities lead to complementary relationship between domestic and foreign capital expenditures, while vertical multinational activities lead to substitute relationship between domestic and foreign capital expenditures. Addressing the relationship between foreign trade costs and FDI in order to assess whether FDI and foreign trade are substitutes or complements, Pontes (2005) concluded that the relationship between FDI and foreign trade costs is not monotonic. When the trade costs are high the relationship between FDI and foreign trade is positive and two variables are complements. When the trade costs are low, however, the relationship between FDI and foreign trade is negative and two variables are substitutes.

The study by Barrios et al. (2003) examined the effects of a firm's own R&D activities and intra-sectoral spillovers on the decision of the firm about export and export intensity. They divided spillovers into two groups, the export activities of other firms and the R&D activities of other firms; and allowed for different spillovers arising from domestic firms and multinationals firms located in the same industry. They concluded that a firm’s own R&D activity is an important determinant in deciding to become an exporter or not, and, if it becomes an exporter, in deciding how much to export; yet the R&D spillovers arising from domestic or multinational firms have no impact on the decision of a domestic firm on becoming an exporter or not. The foreign firms, however, benefit from R&D spillovers of other multinational firms located in the same sector. As a result, the R&D spillovers have positive effects on a firm’s export ratios for both domestic and foreign firms. In another study conducted by Barrios et al. (2005) the effect of FDI on the development of local firms is examined by emphasizing two effects of FDI: the first one is the competition effect that prevents the entry of domestic firms, and the second one is positive externalities that encourage the development of local industry. Utilizing a simple theoretical model, they concluded that the evaluation of domestic firms by the continuous flow of FDI produces a U-shaped curve. This is due to the fact that at the beginning the competition effect that dominates causes some local firms to exit the market, but the competition effect decreases over time, and positive externalities that encourage local firms to enter the market become prevalent.

In the case of single-country studies investigating the impact of FDI on exports,the studies by Zhang (2005); Sun (2001); Liu and Chang (2003); and Wang et al. (2007) indicate that FDI has a statistically significant positive effects on China's exports; while Pesaran (2007) and Vural and Zortuk (2011) reached similar conclusions for India and Turkey, respectively.

With regard to the findings of sector-based studies, Zhang and Song (2001) have found that an increase in the level of FDI has a positive and statistically significant impact on export performance of China's manufacturing sector; while Vukšić (2005) concluded that FDI inflows have a positive and statistically significant impact on the export performance of Croatian manufacturing industry. Gunawardana and Sharma (2009) on the other hand, have found that FDI has a positive and statistically significant impact on the short-term and long-term export performance of Australian manufacturing industry.

1.3. Data and Methodology

In order to examine the relationship between foreign direct investment and export, we use the panel data models developed for datasets that include large number of time series observations (T), and large number of groups or individuals (N) . The foreign direct investment data used in the study were taken from UNCTAD statistics database on an annual basis, for 19 developing economies of Asian countries including Eastern Asia Countries1 , Southern Asia Countries2 , South-Eastern Asia Countries3 and Western Asia Countries4 . GDP deflator which is used to derive the real FDI data and real export data is taken from the Worldbank data bases. The significance of the size of exports of a country in attracting foreign direct investment was taken as a criterion in order to determine the relationship between foreign direct investment and exports. The sample period used to examine the relationship between export (exp) and foreign direct investment (fdi) in 19 countries is 1980-2015. Since the nonstationarity of variables causes wrong results, stationarity checked before regression analysis.

Before examining the causality relation between the series, whether there is dependency between cross sections (countries) constituting the panel or not is examined by Lagrange Multiplier-LM test that is developed by Breusch and Pagan (1980) for the first time and the Adjusted Crossectionally Dependence Lagrange Multiplier (LMadj) test that bias is adjusted by Pesaran et al. (2008). As a unit root test for the series; Cross-Sectionally Augmented Dickey Fuller (CADF) test was used. This test is one of the second generation unit root tests and developed by Pesaran (2007) taking into consideration cross sectional dependency (CD) and structural breaks in the series. The homogeneity of the cointegration coefficients, ie whether the coefficients of the explanatory variable, have changed from cross section to cross section; is examined by the slope homogeneity test developed by Pesaran and Takashi (2008) we have proposed a simple procedure for Granger causality test with LA-VAR approach of Toda and Yamamoto (1995) in heterogonous mixed panels by using Meta analysis.

1.3.1. Cross Section Dependence

The existence of cross section dependency is controlled: by Breusch and Pagan (1980) CD LM1 test when the time series dimension is larger than the cross section dimension (T> N); by Pesaran (2004) CD LM2 test, when the time series dimension is equal to the cross section dimension (T = N); by Pesaran (2004) CD LM test when the time series dimension is smaller than the cross section dimension (T<N). These tests are deviating when the group mean is zero but the individual mean is different from zero. Pesaran and Takashi (2008) corrected this deviation by adding the variance and the mean to the test statistic. For this reason, the nominal deviation is expressed as corrected LM test (LMadj). The LM test statistic is as follows.

The test statistic developed by Pesaran (2004) is as follows:

the null hypothesis of this statistic is no cross-sectional dependence CD → N (0, 1) for N → ∞ and T sufficiently large. Contrary to the LM statistics; the CD statistic has mean at exactly zero for fixed values of T and N, under a wide range of panel data models, including homogeneous/heterogeneous models, non-stationary models and dynamic panels (De Hoyos and Vasilis, 2006).

Where: ![]() represents the mean, VTij represents the variance.

represents the mean, VTij represents the variance.

The test statistic from here shows asymptotically standard normal distribution

Test Hypotheses;

H0:No Cross Section Dependency

H1:Cross Section Dependency

When the probability value obtained from the test result is less than 0.05, at the 5% significance level, the H0 hypothesis is rejected and it is decided that there is cross section dependency between panel units.

Table-1.The Test Results of Cross-Sectional Dependency and Homogeneity

| CD Tests | Stat | P value |

| LM (Breusch and Pagan, 1980) | 169.879 | 0.000 |

| CDlm (Pesaran, 2004) CDlm) | 13.163 | 0.000 |

| CD (Pesaran, 2004) CD) | 6.164 | 0.000 |

| LMadj (Pesaran et al., 2008) | 25.519 | 0.000 |

| 88.379 | 0.000 | |

| 93.582 | 0.000 |

As can be seen from the Table 1. H0 hypotheses have been strongly rejected, since the probability values for the variables are less than 0.05 and it is decided that there is Cross Section Dependency in the series. In this case, there is cross section among the countries constituting the panel. No cross section dependency hypothesis is rejected according to cross section dependency tests. On the other hand, according to the results of the homogeneity test, the H0 hypothesis of homogeneous coefficients is rejected. So it can be said that the panel data includes cross section dependency and heterogeneity

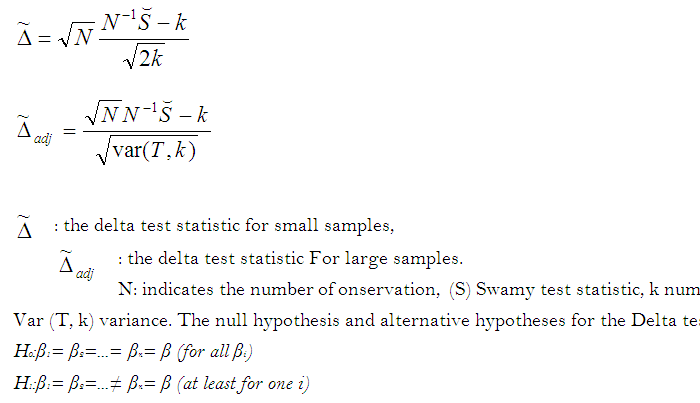

In panel data analysis; since data sets have both cross section and time series dimensions, ıt does not make sense to assume that there is no influence on each other within a given time period or assume that a shock to time series would affect the cross-sectional units at the same time (assumption of homogeneity). Therefore, Δ)1 test which is developed by Pesaran and Takashi (2008) for the first time, is applied to the variables. Delta test statistics are calculated as follows.

1.3.2. Unit Root Test

The first problem encountered in the panel unit root test is whether the cross sections forming the panel are independent of each other or not. Panel unit root tests at this point are divided as first and second generation tests. The first generation tests are also divided into homogeneous and heterogeneous models. While Levin et al. (2002); Breitung (2005) and Hadri (2000) are based on the homogeneous model hypothesis; Im et al. (2003); Maddala and Wu (1999); Choi (2001) are based on the heterogeneous model assumption.

The first generation of panel unit root tests is based on assumption of the cross-sectional independency and all cross-sectional units will be be affected at the same level from the shock that arise from any one of the units forming the panel. However, it is a more realistic approach that a shock coming from one of the cross-sectional units affects the other units at different levels. To overcome this shortcoming, second-generation unit root tests have been developed in order to analyze stability by considering the dependency between cross-sectional units. Among the main second-generation unit root tests, MADF (multivariate Augmented Dickey Fuller) that is developed by Taylor and Sarno (1998) SURADF (Seemingly Unrelated Regression Augmented Dickey Fuller) developed by Breuer et al. (2002) and CADF (Cross-sectional Augmented Dickey-Fuller) developed (Peseran, 2006) can be considered.

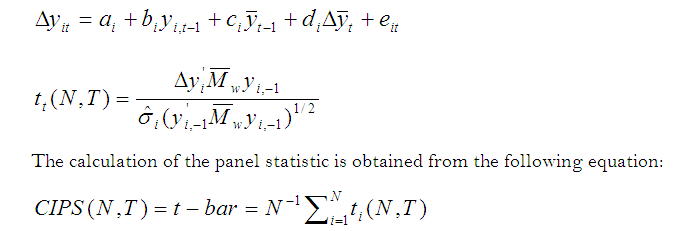

The stability of the series that are used in this study is examined by CADF second generation unit root tests developed by Pesaran (2007) since cross sectional dependency is detected among the countries that constitute the panel. With CDAF test, a unit root test can be performed in each cross sectional unit (in each country) that constitute the panel. Thus, the stability of the series can be calculated for the general and for each cross section unit separately. The CADF test, which assumes spatial autocorrelation and assuming that each country is differently affected by time effects, is used in the T>N ve N>T cases. Stability is tested for each country by comparing these test statistical values to the Pesaran (2007) "in CADF critical table values". If the CADF critical table value is greater than the CADF statistical value, the null hypothesis is rejected and only the result is that the series of that country is stationary. The CADF test developed by Pesaran (2007) is based on the following regression model. The t statistic ti (N, T) is given below

.

.

The calculated CIPS statistics are calculated by averaging the t statistics of each cross sectional unit

Table-2.The Results of CADF Unit Root Test

| Country | FDI | Export | ||

| China | -4.71* | - | -2.338 | -3.468*** |

| HongKong | -3.187*** | - | -3.997** | - |

| KoreanRepublic | -1.501 | -4.92* | -2.430** | - |

| Banghladesh | -4.583* | - | -3.082*** | - |

| India | -5.152* | - | -3.232*** | - |

| Iran | -3.224*** | - | -3.197*** | - |

| Nepal | -5.073* | - | -5.095* | - |

| Pakistan | -2.807 | - | -2.858 | -4.055** |

| Sri Lanka | -4.874* | - | -1.690 | -3.246*** |

| Indonesia | -5.921* | - | -3.019*** | - |

| Malaysia | -4.056** | - | -3.927** | - |

| Philippines | -3.226*** | - | -4.086* | - |

| Singapore | -2.490 | -4.55* | -3.861** | - |

| Thailand | -4.840* | - | -3.008*** | - |

| Bahrain | -5.196* | - | -3.141*** | - |

| Jordan | -4.499* | - | -3.037*** | - |

| Oman | -4.970* | - | -3.559** | - |

| SaudiArabia | -2.938 | -5.22* | -2.985*** | - |

| Turkey | -4.999* | - | -3.787** | - |

| CIPS stat | -4.118* | -5.46* | -3.281** | -4.340* |

| Individual Critical Valueu | %1: -4.11 | CIPS critical values | %1: -2.38 | |

| %5: -3.34 | %5: -2.20 | |||

| %10: -2.96 | %10: -2.11 |

* indicates rejection of null hypothesis at %1 significance level

** indicates rejection of null hypothesis at %5 significance level

*** indicates rejection of null hypothesis at %10 significance level

The test we used is Pesaran (2007) Cross-sectionally Augmented Dickey Fuller (CADF) test. This test can be used in situations where N <T or T <N as well as considering cross-sectional dependency. The panel's general seems static but it is important for us that it is not stable at the second level. When writing the result, we can say that the panel I(0) and I(1) are mixed. Constant considered in the model. The causality test we use is not a problem as it allows the panel contain unit root. The CIPS statistic is the average of the test statistics calculated for each country. Since we use heterogeneous testing, we are interested in the results on an individual country basis.

1.3.3. Panel Granger Causality Analysis

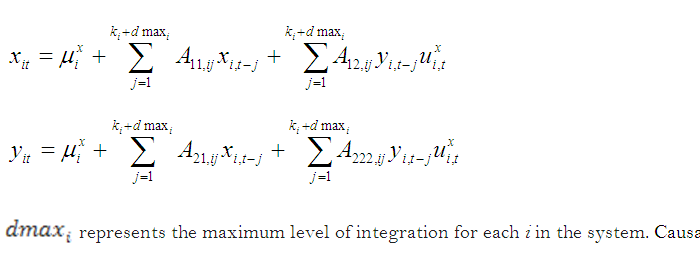

Emirmahmutoglu and Nezir (2011)'s causality test is also a test that can be used when the series are not stable at the same level, ie when some of the series are I (0) and some are I (1) and no cointegration relation is found between the variables.

The VAR models for two variables are set up as follows:

Table-3. Results of Granger Causality Test.

| Country | Export → FDI | FDI→ Export | ||||

| Lag | Wald | P value | Lag | Wald | P value | |

| China | 2 | 9.840 | 0.007* | 2 | 1.409 | 0.494 |

| HongKong | 3 | 5.890 | 0.117 | 3 | 6.497 | 0.090** |

| Korean Republic | 2 | 13.879 | 0.001* | 2 | 3.354 | 0.187 |

| Banghladesh | 1 | 3.310 | 0.069*** | 1 | 3.483 | 0.062*** |

| India | 1 | 3.153 | 0.076*** | 1 | 4.025 | 0.045** |

| Iran | 1 | 0.184 | 0.668 | 1 | 0.033 | 0.856 |

| Nepal | 3 | 8.874 | 0.031** | 3 | 10.575 | 0.014** |

| Pakistan | 3 | 4.602 | 0.203 | 3 | 5.864 | 0.118 |

| Sri Lanka | 2 | 7.342 | 0.025** | 2 | 44.923 | 0.000* |

| Indonesia | 2 | 10.377 | 0.006* | 2 | 67.702 | 0.000* |

| Malaysia | 2 | 3.674 | 0.159 | 2 | 0.769 | 0.681 |

| Philippines | 2 | 7.971 | 0.019** | 2 | 2.705 | 0.259 |

| Singapore | 2 | 13.247 | 0.001* | 2 | 4.789 | 0.091*** |

| Thailand | 1 | 4.610 | 0.032** | 1 | 5.060 | 0.024** |

| Bahrain | 1 | 1.527 | 0.217 | 1 | 2.947 | 0.086*** |

| Jordan | 1 | 1.332 | 0.248 | 1 | 0.461 | 0.497 |

| Oman | 3 | 8.153 | 0.043** | 3 | 7.387 | 0.061*** |

| Saudi Arabia | 3 | 5.116 | 0.163 | 3 | 7.757 | 0.051*** |

| Turkey | 3 | 13.516 | 0.004* | 3 | 85.251 | 0.000* |

*Indicate significance at the 1% level.

**Indicate significance at the 5% level.

***Indicate significance at the 10% level.

Bootstrap replication: 10.000 Lag: Akaike Information Criterion Max lag: 3.

The results obtained based on the Granger causality test, which considers the horizontal section dependency and heterogeneity, are presented in Table.3.

When we examine the causality relationship from export to FDI, we can observe that China, Republic of Korea, Indonesia, Singapore and Turkey has causality from export to FDI at 1% significance level. On the other hand, we can say that Nepal, Sri Lanka, Philippines, Thailand and Oman has a causality from export to FDI at 5% significance level. Finally, it is possible to say that Bangladesh and India has a causality from export to FDI at 10% significance level, while the likelihood value is very close to the 5% significance value.

When we examine the countries where the causality relation is identified, it is observed that these countries are trying to grow by adopting the export-led growth strategy. The fact that the causality from export to FDI in the countries mentioned above suggests that the export figures in the country are an important incentive for the foreign investor.

The second part of the Granger causality relationship tests is the existing causality from foreign direct investments (FDI) to export. According to the results, while Sri Lanka, Indonesia and Turkey has a causality from FDI to export at 1% significance level, India, Nepal and Thailand has a causality from FDI to export at 5% significance level. Finally, the existence of a causality relationship from FDI to Export was found at 10% significance level in Hong Kong, Banghladesh, Singapore, Bahrain, Oman and Saudi Arabia.

As explained in the theoretical part of the study, foreign direct investment can lead to an increase in exports, by the ways of technology transfer, domestic capital increase. This is also confirmed in the context of the fact that countries are high-tech exporting countries. On the other hand, it is thought that the outflow created by foreign direct investments in countries where FDI has no causal relationship to export is directed towards the domestic market.

According to these results; It can be said that the foreign direct investments are an important factor in increasing the export performance. On the other hand, exports are also an important indicator for countries seeking foreign direct investment.

2. CONCLUSION

In this study, we aimed to investigate the relationship between FDI and exports based in 19 developing Asian countries (China, Hong Kong, KoreaRep., Bangladesh, India, Iran, Nepal, Pakistan, Sri Lanka, Indonesia, Malaysia, Philippines, Singapore, Thailand Bahrain, Jordan, Oman, SaudiArabia and Turkey). First, heterogeneity of the variables were investigate with the Delta test Pesaran and Takashi (2008) and then the existence of dependency between cross-sectional units that make series were examined by the CADF. This test is one of the second generation unit root tests and developed by Pesaran (2007) taking into consideration cross sectional dependency (CD) and structural breaks in the series. On the other hand, Emirmahmutoglu and Nezir (2011) panel causality tests were applied.

The causality test includes two parts. 1- causality relationship from export to FDI and 2- causality from foreign direct investments (FDI) to export. As a first step the causality relationship from export to FDI was examined, and it was observed that China, Republic of Korea, Indonesia, Singapore and Turkey has causality from export to FDI at 1% significance level. On the other hand, we can say that Nepal, Sri Lanka, Philippines, Thailand and Oman has a causality from export to FDI at 5% significance level. Finally, it is possible to say that Bangladesh and India has a causality from export to FDI at 10% significance level, while the likelihood value is very close to the 5% significance value. This result supports the claim of Zhang and Felmingham (2001). Their claim is that some credence is given to an export led growth strategy. Export attracts FDI as it stimulates economic development and structural change and that's why an export-led growth strategy should be followed, together with a liberal foreign trade policy that reduces the costs for the exporters, and encourages exports.

The second part of the Granger causality relationship tests is the existing causality from foreign direct investments (FDI) to export. According to the results, while Sri Lanka, Indonesia and Turkey has a causality from FDI to export at 1% significance level, India, Nepal and Thailand has a causality from FDI to export at 5% significance level. Finally, the existence of a causality relationship from FDI to Export was found at 10% significance level in Hong Kong, Banghladesh, Singapore, Bahrain, Oman and Saudi Arabia.

As explained in the theoretical part of the study, foreign direct investment can lead to an increase in exports, by the ways of technology transfer, domestic capital increase. This is also confirmed in the context of the fact that countries are high-tech exporting countries. On the other hand, it is thought that the outflow created by foreign direct investments in countries where FDI has no causal relationship to export is directed towards the domestic market.

According to these results; It can be said that the foreign direct investments are an important factor in increasing the export performance. On the other hand, exports are also an important indicator for countries seeking foreign direct investment.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Ahmed, A., E. Cheng and G. Messinis, 2007. Causal links between export, FDI and output: Evidence from Sub-Saharan African Countries. CSES Working Paper No.35, Centre for Strategic Economic Studies, Victoria University: 1-24.

Aitken, B., G.H. Hanson and A.E. Harrison, 1997. Spillovers, foreign investment and export behavior. Journal of International Economics, 43(1-2): 103-132. View at Google Scholar | View at Publisher

Alıcı, A.A. and M.Ş. Ucal, 2003. Foreign direct investment, exports and output growth of Turkey: Causality analysis. Paper to be Presented at the European Trade Study Group (ETSG) Fifth Annual Conference.

Amiti, M., D. Greenaway and K. Wakelin, 2000. Foreign direct investment and trade: Substitutes or complements. University of Melbourne, Working Paper, 1-24. [Accessed 13.07.2012].

Barrios, S., H. Görg and E. Strobl, 2003. Explaining firms’ export behaviour: R&D, spillovers and destination market. Oxford Bulletin of Economics and Statistics, 65(4): 475-496.View at Google Scholar | View at Publisher

Barrios, S., H. Görg and E. Strobl, 2005. Foreign direct investment, competition and industrial development in the host country. European Economic Review, 49(7): 1761-1784.View at Google Scholar | View at Publisher

Blomström, M. and A. Kokko, 1998. Multinational corporations and spillovers. Journal of Economic Survey, 12(2): 1-31. View at Google Scholar | View at Publisher

Braconier, H., P.J. Norbäck and D. Urban, 2002. Vertical FDI revisited. The Research Institute of Industrial Economics, Working Paper, No.579: 1-46.

Breitung, J., 2005. A parametric approach to the estimation of cointegrating vectors in panel data. Econometric Reviews, 24(2): 151-173. View at Google Scholar | View at Publisher

Breuer, B., R. Mcnown and M. Wallace, 2002. Series-specific unit root testwith panel data. Oxford Bulletin of Economics and Statistics, 65(5): 527-546.View at Google Scholar | View at Publisher

Breusch, T.S. and A.R. Pagan, 1980. The lagrange multiplier test and its applications to model specification in econometrics. Review of Economic Studies, 47(1): 239-253. View at Google Scholar | View at Publisher

Chang, T., G. Rangan, I.-L. Roula, S.-K. Beatrice, S. Devon and T. Amy, 2015. Renewable energy and growth: Evidence from heterogeneous panel of G7 countries using Granger causality. Renewable and Sustainable Energy Reviews, 52: 1405–1412. View at Google Scholar | View at Publisher

Choi, I., 2001. Unit roots tests for panel data. Journal of International Money and Finance, 20(2): 229-272. View at Google Scholar

De Hoyos, R.E. and S. Vasilis, 2006. Testing for cross-sectional dependence in panel-data models. Stata Journal, 6(4): 482-496. View at Google Scholar

De Mello, L.R., 1997. Foreign direct investment in developing countries and growth: A selective survey. Journal of Development Studies, 34(1): 1-34.View at Google Scholar | View at Publisher

De Mooij, R.A. and S. Ederveen, 2001. Taxation and foreign direct investment, a synthesis of empirical research. CPB Discussion Paper, No. 003: 1-52.

Demekas, D.G., B. Horváth, E. Ribakova and Y. Wu, 2007. Foreign direct investment in European transition economies -therole of policies. Journal of Comparative Economics, 35(2): 369-386.View at Google Scholar | View at Publisher

Dritsaki, M., C. Dritsaki and A. Adamopoulos, 2004. A causal relationship between trade, foreign direct investment and economic growth for Greece. American Journal of Applied Sciences, 1(3): 230-235.View at Google Scholar | View at Publisher

Emirmahmutoglu, F. and K. Nezir, 2011. Testing for Granger causality in heterogeneous mixed panels. Economic Modelling, 28(3): 870–876.View at Google Scholar | View at Publisher

Goldberg, L.S. and M.W. Klein, 1999. International trade and factor mobility: An empirical investigation. National Bureau of Economic Research (NBER) Working Paper Series, Working Paper No. 7196 1-28.

Gu, W., T.O. Awokuse and Y. Yuan, 2008. The contribution of foreign direct investment to China’s export performance: Evidence from dissaggregated sectors. Selected Paper Prepared for Presentation at the American Agricultural Economics Association Annual Meeting, Orlando.

Gunawardana, P.J. and K. Sharma, 2009. The impact of inward FDI, labour productivity and industry assistance on manufacturing exports of Australia. Working Paper Series School of Economics and Finance: 1-15.

Hadri, K., 2000. Testing for unit roots in heterogeneous panel data. Econometrics Journal, 3(2): 148-161.View at Google Scholar

Hanousek, J., E. Kočenda and M. Maurel, 2011. Direct and indirect effects of FDI in emerging European markets: A survey and meta-analysis. Economic Systems, 35(3): 301-302. View at Google Scholar | View at Publisher

Helpman, E., 1984. A simple theory of international trade with multinational corporations. Journal of Political Economy, 92(3): 451-472. View at Google Scholar | View at Publisher

Im, K.S., M.H. Pesaran and Y. Shin, 2003. Testing for unit roots in heterogeneouspanels. Journal of Econometrics, 115(1): 53-74.View at Google Scholar

Jayachandran, G. and A. Seilan, 2010. A causal relationship between trade, foreign direct investment and economic growth for India. International Research Journal of Finance and Economics, 42: 74-88.

Johnson, A., 2006. FDI and exports: The case of high performing East Asian economies. Centre of Excellence for Studies in Science and Innovation (CESIS) Paper No. 57, Electronic Working Paper Series, The royal Institute of Technology, Sweeden.

Kutan, A.M. and G. Vukšić, 2007. Foreign direct investment and export performance: Empirical evidence. Comparative Economic Studies, 49(3): 430-445. View at Google Scholar

Levin, A., C.F. Lin and C.S.J. Chu, 2002. Unit root tests in panel data: Asymptoticand finite-sample properties. Journal of Econometrics, 108(1): 1-24.View at Google Scholar | View at Publisher

Liu, X., P. Burridge and P.J.N. Sinclair, 2002. Relationships between economic growth, foreign direct investment and trade: Evidence from China. Applied Economics, 34(11): 1433-1440View at Google Scholar | View at Publisher

Liu, X. and S. Chang, 2003. Determinants of export performance: Evidence from Chinese industries. Economics of Planning, 36(1): 45-67. View at Google Scholar | View at Publisher 190-202.View at Google Scholar | View at Publisher

Maddala, G.S. and S. Wu, 1999. A comparative study of unit root tests with panel data and a new simple test. Oxford Bulletin of Economics and Statistics, 61(1): 631-652.View at Google Scholar | View at Publisher

Markusen, J.R., 1983. Factor movements and commodity trade as complements. Journal of International Economics, 14(3-4): 341-356.View at Google Scholar | View at Publisher

Markusen, J.R., 1984. Multinationals, multi-plant economies, and the gains from trade. Journal of International Economics, 16(3-4): 205-226. View at Google Scholar | View at Publisher

Mundell, R.A., 1957. International trade and factor mobility. American Economic Review, 47(3): 321-335.View at Google Scholar

Namini, J.E. and E. Pennings, 2009. Horizontal multinational firms, vertical multinational firms and domestic investmment. Tinbergen Institute Discussion Paper: 1-29. Retrieved from http://repub.eur.nl/res/pub/14741/2009-0042.pdf [Accessed 19.08.2012].

Pesaran, H.M., 2004. General diognastic tests for cross section dependence in panels. Discussion Paper No. 1240.

Pesaran, H.M., 2004. General diognastic tests for cross sectiondependence in panels. CESifo Working Paper No. 1229.

Pesaran, H.M., 2007. A simple panel unit root test in the presence of cross section dependence. Journal of Applied Econometrics, 22(2): 265-312.View at Google Scholar | View at Publisher

Pesaran, H.M., U. Aman and Y. Takashi, 2008. A bias-adjusted LM test of error cross-section independence. Econometrics Journal, 11(1): 105–127. View at Google Scholar | View at Publisher

Pesaran, H.M. and Y. Takashi, 2008. Testing slope homogeneity in large panels. Journal of Econometrics, 142(1): 50-93 View at Google Scholar | View at Publisher

Peseran, M.H., 2006. A simple panel unit root test in the presence of crosssection dependecy. Cambridge Working Papers in Economics, 0346.

Pontes, J.P., 2005. Fdi and trade: Complements and substitutes. 1-8. Retrieved from http://www.iseg.utl.pt/departamentos/economia/wp/wp032006deuece.pdf [Accessed 30.10.2012].

Prasanna, N., 2010. Impact of foreign direct investment on export performance in India. Journal of Social Sciences, 24(1): 65-71.View at Google Scholar | View at Publisher

Samsu, S.H., A.M. Derus, A.Y. Ooi and M.F. Ghazali, 2008. Causal links between foreign direct investment and exports: Evidence from Malaysia. International Journal of Business and Management, 3(12): 177-183.

Schiff, M., 2006. Substitution in Markusen’s classic trade and factor movement complementarity models. World Bank Policy Research Working Paper No. 3974: 1-11.

Sun, H., 2001. Foreign direct investment and regional export performance in China. Journal of Regional Science, 41(2): 317-336.View at Google Scholar | View at Publisher

Taylor, M. and L. Sarno, 1998. The behaviour of real exchange rates during the post-bretton woods period. Journal of International Economics, 46(2): 281-312.View at Google Scholar | View at Publisher

Temiz, D. and A. Gökmen, 2009. Foreign direct investment and export in Turkey: The period of 1991-2008. Paper Presented at Econ Anadolu 2009: Anadolu International Conference in Economics, June 17-19.

Toda, H. and T. Yamamoto, 1995. Statistical inference in vector autoregressions with possible İntegrated processes. Journal of Econometrics, 66(1-2): 225-250. View at Google Scholar | View at Publisher

Vukšić, G., 2005. Impact of foreign direct investment on croatian manufacturing exports. Financial Theory and Practice, 29(2): 131-158. View at Google Scholar

Vukšić, G., 2006. Foreign direct investment and export performance of the transition countries in central and Eastern Europe. Paper for presentation at the 12th Dubrovnik Economic Conference, organized by the Croatian National Bank. pp: 1-28.

Vural, İ.Y. and M. Zortuk, 2011. Foreign direct investment as a determining factor in Turkey’s export performance. Eurasian Journal of Business and Economics, 4(7): 13-23. View at Google Scholar

Wang, C., P.J. Buckley, J. Clegg and M. Kafouros, 2007. The impact of inward foreign direct investment on the nature and intensity of Chinese manufacturing exports. Transnational Corporations, 16(2): 123-140.

Zhang, K.H., 2005. How does FDI affect host country’s export performance? The case of China. Paper Presented to International Conference of WTO, China and the Asian Economics, III.Xi’an, China, 25-26 June. pp: 1-17.

Zhang, K.H. and J.R. Markusen, 1999. Vertical multinationals and host-country characteristics. Journal of Development Economics, 59(2): 233-252.View at Google Scholar | View at Publisher

Zhang, K.H. and S. Song, 2001. Promoting exports the role of inward FDI in China. China Economic Review, 11(4): 385-396.View at Google Scholar | View at Publisher

Zhang, Q. and B. Felmingham, 2001. The relationship between inward direct foreign investment and China’s provincial export trade. China Economic Review, 12(1): 82-99.View at Google Scholar | View at Publisher