PREDICTING CONTINUANCE USAGE INTENTION OF MOBILE PAYMENT: AN EXPERIMENTAL STUDY OF BANGLADESHI CUSTOMERS

1Assistant Professor, Department of Management, Hajee Mohammad Danesh Science and Technology University, Bangladesh

2Assistant Professor, Department of Management Studies, Barisal University, Bangladesh

3Department of Business Administration, Chonbuk National University, South Korea

ABSTRACT

With the tremendous use of electronic devices, inhabitants create digital footsteps of their everyday lives, therefore, unlocked magnificent opportunities for the innovative companies to launch mobile payment system and offer value-added facilities. Mobile payment system has inaugurated a conspicuous phenomenon that can enable consumers to transform their mobile devices into a digital bank. Mobile payment has already proved its aids in the developed country market and projected to enjoy a cheerful prospect in the emerging market like Bangladesh. Moreover, a stream of research conducted in multiple countries regarding the domain of mobile payment, but a different scenario noticed in perspective of emerging country like Bangladesh as there hasn’t much yet. By giving importance on behavioral intention of consumer and specific characteristics of m-payments, this study aims to develop and test a research model by integrating usefulness and ease of use into the behavioral intentions. This study employed Confirmatory Factor Analysis and Structural Equation Modeling to analyze database, which was composed of 328 samples. Results show that continuous usage intention is significantly affected by customer satisfaction. Perceived usefulness and ease of use are positively influence the continuance usage intention and satisfaction. The current study may extensively contribute to knowledge extension of two research streams-strategic management and service marketing-by implementing appropriate business model and service marketing strategies for m-payment users in Bangladesh and potentially other emerging markets.

Keywords:Continuance usage intention Ease of use Usefulness Credibility Mobility and risk.

ARTICLE HISTORY: Received:26 February 2018, Revised:16 March 2018, Accepted: 19 March 2018,Published:21 March 2018.

Contribution/ Originality:This study documents the imaginative insights and realistic guidance on the antecedents of consumer behavioral intentions and how these can be achieved through the internal quality assurance and external factor considerations regarding m-payment. Practitioners may use these findings to design their effective service strategies and marketing plans.

1. INTRODUCTION

The growth of electronic communication has become the considerable innovation due to the change of human lifestyle. Higher degree of acceptance and distribution of technological improvement create a new shape of communication, which progressively used in business deeds and its effectiveness. Mobile payment (hereinafter m-payment) is considered as one of the fastest and convenient methods of transactions. In other words, m-payment can enable customers to turn their mobile phones into digital cash bank. The rapid change of digital technology tends to drastic change in payment systems. Nowadays, payment systems become the web-of-mobile payment with the development of mobile phone and communication networks.

Meanwhile, the use of mobile phone is more than personal computer; m-payment is becoming more popular than the e-banking. Additionally, it ensures the quality of service and facilitating the time and place constraints. Individual can build an interactive and independent relationship with others by using this alternative payment method, which is anticipated to progressively substitute for the predominant role of credit cards (Zea et al., 2012; Wilcox, 2014).

M-payment is recklessly growing payment method in Bangladesh. Within a very short time, mobile telecommunication reached the foremost service sector in this country by its growing network (Ahamed et al., 2015). Presently, five major telecommunication companies are operating businesses, holding a large number of subscribers along with price effective strategy. Furthermore, the government has paid highest attention to develop an ever greater dependency on information technology and its effective use, which resulting to do the work done sitting in the own premises of the citizen. This mobile communication strategy has become an indispensable part of human life, contemporarily service providers continuously strengthening competition by innovative customer service like m-payment.

Continuance usage intention or loyalty expresses an intended overt behavior toward product/service or its attributes. Consumer loyalty is the future state of customers whether they repurchase or renew the service contracts or converse, likely to switch to other product or service (Heesup and Sunghyup, 2017). Customers may have intention to retain the existing vendors as they find satisfaction toward their service or product. In this regard, most of the companies tend to approach satisfaction as a worthwhile long-run strategy. Intended consumer only be satisfied with promising and valid service through product performance model. In accordance with this satisfaction, consumers may recommend their surroundings by word-of-mouth communication, which resulting a higher degree of consumer loyalty.

Perceived usefulness and compatibility appeared to be the dominant factors affecting consumer attitude towards m-payment (Pham and Jonathan, 2015). From the six system characteristics model, reachability and convenience have significant impact on perceived usefulness and per ease of use which ultimately affect consumers’ intention to m-payment (Kim et al., 2010). A series of studies have accounted that perceived usefulness, perceived ease of use, trust, attractiveness of alternatives, compatibility, perceived cost, trial ability, mobility, social influence, credibility, and personal related factors have the dominant behavior on consumer intention to use for future time (Wessels and Drennan, 2010; Hanafizadeh et al., 2014; Yuan et al., 2014; Sharma et al., 2016). Venkatesh et al. (2003) proposed that consumer intention is basically pretentious by performance expectancy, effort expectancy, facilitating conditions and social influence. Moreover, consumer perception may be different due to the different factors level and different socio-economic circumstances. Thus, there is an urgency to understand the factor level effects on intention metrics.

The purpose of this study is to explore the antecedents of consumer behavioral intentions (consumer satisfaction and continuous usage intention) and to discover the major variables that logically and theoretically impact the antecedents of behavioral intentions of m-payment. It is suggested that consumer satisfaction is imperative antecedent of consumer loyalty. And consumer satisfaction has long dependency on different variables. The ambition of this study is to provide imaginary insight and realistic guidance as to how loyalty can be attained by providing internal quality assurance and external factor considerations.

The rest of the paper is organized as follows. The next section reviews the empirical literature of consumer behavioral intentions and describes the proposed research model. Then, the following section addressed the methodology of the study. And final section completes the paper with precise contributions and recommendations.

2. REVIEW OF THE EMPIRICAL STUDIES

M-payment is an alternative payment system for goods, services or any other means of transaction with the use of mobile device. Instead of cash, checks or even credit card payment, m-payment uses smart phone or mobile phone by the assistance of mobile telecommunication networks. This payment method can be useful in different payments, such as payments for shopping, ticketing, paying bills or charges. Mobile devices have strong access to digital content payments, such as apps, news, music, games, ring tones, and other virtual payments. M-payment allows the consumer to connect with a server, secure the authentication and authorization, and make m-payment with confirmation (Ding and Hampe, 2003). M-payment broadly covers two forms of payments such as, payments for shopping and payments of bills or transactions (Karnouskos and Fokus, 2004). In payments for shopping, m-payment competes with cash, checks, and credit or debit cards. Similarly for bills or transactions, it competes with online banking, money transfers or direct transactions.

2.1. Credibility

Credibility is the degree to which a person believes that there is no harm or privacy threat in the use of Mobile transactions (Wang et al.,2003). Credibility has an inverse relationship with risk or uncertainty. Individuals become worried about their personal information and financial transaction due to inappropriate credibility (Luran and Lin, 2005). Prior research has stated that a great degree of credibility resulting greater compatibility which ultimately affects the continuance intention to use (Kim et al., 2010; Hanafizadeh et al., 2014). Recent studies about m-payment has identified that credibility has a significant impact on intention to use (Wang et al., 2003; Luran and Lin, 2005). Additionally, Ahad et al. (2012) has concluded that credibility has positive relation with the adoption of mobile banking and intention to use. Therefore, we propose the following:

hypotheses:

Hypothesis 1a: Credibility has a positive effect on perceived usefulness of m-payment.

Hypothesis 1b: Credibility has a positive effect on perceived ease of use of m-payment.

2.2. Mobility

One of the most important features of mobile tool is mobility i.e., ability to access to the roaming time through wireless mobile networks. A significant number of researchers have identified the relationship between continuance intention to use the mobile technology and mobility (Mallat, 2007; Au and Kauffman, 2008; Kim et al., 2010). According to Kim et al. (2010) perceived usefulness is heavily influenced by the mobility of mobile technology. Mobile device has ‘anytime and anywhere’ advantage, which front runners the independency of time and place (Au and Kauffman, 2008). Mobile device provides freedom to the consumer convenience due to its wireless connection. Under this consideration, the following hypotheses are proposed:

Hypothesis 2a: Mobility has a positive effect on perceived usefulness of m-payment.

Hypothesis 2b: Mobility has a positive effect on perceived ease of use of m-payment.

2.3. Risk

Due to the association with threats and uncertainties, risk is considered as an important determinant of mobile service usage. Mobility of payment system increases risk factors. Wu and Wang (2005) have identified the significant relationship between perceived risk and intention to mobile use. Effects of risk being discovered by Wessels and Drennan (2010) and concluded a negative association among risk factors and m-payment intentions. Hanafizadeh et al. (2014) also posit the negative association. Furthermore, Yuan et al. (2014) and Kabir (2013) strengthen the assumption as risk has a negative influence on consumers’ behavioral intentions. It is reasonably difficult to excessive use of technological product, unless or until service provider minimizes the risk factors. Therefore, investigating this factor and its influence on consumer attitude and usage intention seems necessary. In this regard, the following hypotheses are proposed:

Hypothesis 3a: Risk has a negative effect on perceived usefulness of m-payment.

Hypothesis 3b: Risk has a negative effect on perceived ease of use of m-payment.

2.4. Usefulness

Usefulness is the imperative conjecture of behavioral intension in countless contexts including the internet, mobile commerce, and information systems. Usefulness refers the degree to which an individual believes that performance will be upward due to the use of a particular machine. Davis et al. (1989) pointed, usefulness is a subjective probability that the use of technology will enhance individual’s performance. In order to recommend the consumer to use of m-payment, this payment method should discover some extensive advantages than existing payment methods (cash, check or card payment). M-payment is a faster checkout because of technology use which does not require signature. VeriFone (2010) has stated that contactless payment can downsize the individual transaction time by 10-15 seconds. Thus, speed of this payment method is really attractive enough in busy life. Previous studies have concluded that consumers who perceive a significant usefulness and benefits from m-payment, more likely to use this in future time (Lu et al., 2011; Safeena et al., 2011; Kabir, 2013; Yuan et al., 2014). Hence, the following hypotheses are proposed:

Hypothesis 4a: Usefulness has a positive effect on consumer satisfaction toward m-payment.

Hypothesis 4b: Usefulness has a positive effect on continuance usage intention toward m-payment.

2.5. Ease of Use

Ease of use is characterized by multiple aspects as described in the existing literature. According to Casalo et al. (2008) usability is indirect credentials of consumer loyalty and word-of-mouth through satisfaction. Usability helps to fulfill consumers need in terms of manageability, leading the greater level of loyalty and positive attitude. It integrates ease of user’s capability of learning to manage the system. Ease of use is an important predictor to the adoption of mobile commerce (Kim et al., 2010; Yuan et al., 2014; Sharma et al., 2016). Ease of use is basically related with the innate features of technology that observed usefulness immensely affects the group of variables which have influence on perceived ease of use (Brown, 2002; Ramayah and Lo, 2007). Accordingly, perceived ease of use has positive influence on consumer attitude toward mobile banking (Kabir, 2013). Furthermore, Wessels and Drennan (2010) suggested that ease of use significantly affects consumer attitude and intention to use. Thus, the following hypotheses are formulated:

Hypothesis 5a: Ease of use has a positive effect on perceived usefulness of m-payment.

Hypothesis 5b: Ease of use has a positive effect on consumer satisfaction of m-payment.

Hypothesis 5c: Ease of use has a positive effect on continuance usage intention toward m-payment.

2.6. Satisfaction

Satisfaction is a general evaluation of a product whether that product meets the customer need and want or not. It works as a primary requisite to future purchase and directly affects consumer attitude. Customer satisfaction holds the concept that satisfying customers’ needs and wants generate customer loyalty. Scholars have long been recognized that loyal customers are very essential to every successful business (Bowen and McCain, 2015). To attain the organizational goal in a competitive market position, customer satisfaction and loyalty become the strategic objectives set by many organizations. Ram and Wu (2016) originate that customer satisfaction has a positive impact on customer loyalty. In addition, satisfaction creates loyal customer base, which is important building block of customer retention (Aghdaie et al., 2015; Ammari and Bilgihan, 2017). Thus, from the above arguments, following hypothesis is proposed:

Hypothesis 6: Satisfaction has a positive effect of continuance usage intention toward m-payment.

3. RESEARCH DESIGN

Our study considers a seven factors model comprising credibility, mobility, risk, perceived usefulness, ease of use, satisfaction, and continuance usage intention as major factors explaining inclination toward m-payment in Bangladesh. A structured questionnaire comprising 16 statements were used as a survey instrument that fitted into seven constructs. To measure the responses, 5-points Likert scale was used ranging from strongly agree (1) to strongly disagree (5). A convenient sampling technique was used to data collection and the survey had been conducted during the month starting from 15 June 2017.

Furthermore, a pilot study was conducted to test the questionnaire whether the instructions and meanings of questions were simple, clear and beneficial to the subjects. A total 25 number of respondents were taken in the pilot study, and changes were made accordingly. All of the questionnaires were scrutinized and incomplete or unlikely responses were removed. After succeeding data cleaning and removal of inappropriate responses, 328 valid responses are taken for final analysis. According to the sample demographic data, 66% respondents are male and 44% female, 60% of the respondents are over 25 years of age, 58% of the respondents have received a college education or above, and 49% are students.

The current study validates seven constructs of usefulness, ease of use, credibility, mobility, risk, satisfaction and customer intention toward m-payment to explain the study model. The measurements of usefulness and ease of use are taken from Kim et al. (2010) and Sharma et al. (2016). Measurement items credibility, mobility and risk are modified from Kim et al. (2010) and Yuan et al. (2014). Furthermore, behavioral items satisfaction and customer intention are adopted from Yuan et al. (2014) and Kim et al. (2010). Statistical Package for Social Science (SPSS) and Structural equation modeling (SEM) are used to data interpretation and analysis.

4. EMPIRICAL RESULTS

4.1. Data Reliability and Validity

To assess the internal consistency of data, Cronbach’s alpha reliability test was conducted. Reliability is the degree to which a measure is free from error and yield to consistent results (Hair et al., 2010). Cronbach’s alpha value is 0.734 representing data reliability of the study. KMO measure of sampling adequacy was carried out to examine the data validity, and Table 1 shows KMO of sampling adequacy value is 0.717 which additionally support the data validity of the study.

Table-1. Reliability and validity statistics

| Cronbach's Alpha | Cronbach's Alpha Based on Standardized Items | No. of Items |

| 0.734 | 0.760 | 16 |

| KMO and Bartlett's Test | ||

| Kaiser-Meyer-Olkin Measure of Sampling Adequacy. | 0.717 | |

| Bartlett's Test of Sphericity | Approx. Chi-Square | 816.384 |

| Df | 120 | |

| Sig. | 0.000 | |

Source: SPSS output

Discriminant validity is the degree to which the measurement of the variable is not a reflection of the other variables. Low correlations among the measure of interest and the measure of the other constructs represent discriminant validity (Fornell and Larcker, 1981). In addition, the issue of multicollinearity among the independent variables was also examined with a variance inflation factor (VIF) analysis, and the results show that the VIF values range from 1.071 to 1.33, below the threshold of 10 (Hair et al., 2010) , meaning all are at an acceptable level.

Table-2. Discriminant validity

| Mean | Std. Deviation | 1 | 2 | 3 | 4 | 5 | 6 | Tolerance | VIF | |

| 1. Usefulness | 3.34 | 0.76 | 0.93 | 1.07 | ||||||

| 2. Ease of use | 3.97 | 0.61 | 0.35 | 0.88 | 1.13 | |||||

| 3. Credibility | 3.73 | 0.73 | 0.18 | 0.29 | 0.78 | 1.27 | ||||

| 4. Mobility | 4.08 | 0.80 | 0.12 | 0.38 | 0.41 | 0.86 | 1.15 | |||

| 5. Risk | 3.02 | 0.90 | 0.002 | -.05 | -.41 | -0.08 | 0.92 | 1.08 | ||

| 6. Satisfaction | 3.90 | 0.66 | 0.26 | 0.28 | 0.80 | 0.45 | -0.34 | 0.75 | 1.33 | |

| 7.Continuance usage intention | 3.93 | 0.59 | 0.12 | 0.31 | 0.48 | 0.46 | 0.01 | 0.78 |

Source: SPSS output

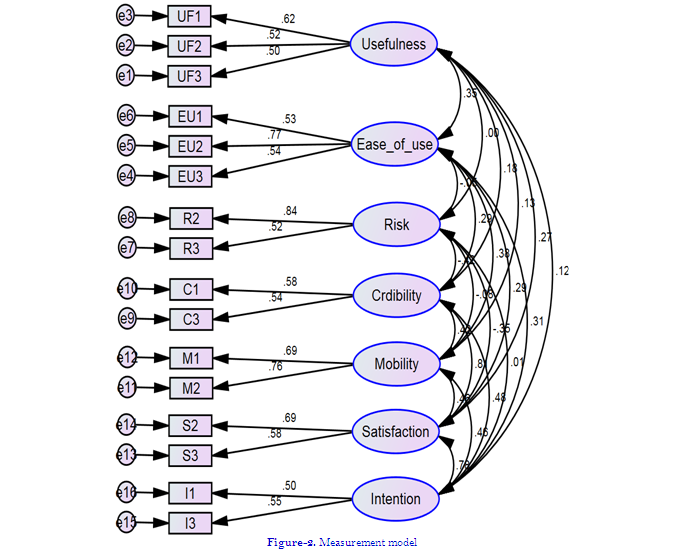

Unidimensionality measure was carried out through confirmatory factor analysis (CFA) to predict whether the operation correctly measure its variables or not. All the measurement items are to be significantly loadings on their respective constructs with moderate standardized weights (Table 3 and Figure 2). The validity constructs are established using Hair et al. (2010) recommendations that suggests factor loadings of higher than 0.50 (Hair et al., 2010). Comparative Fit Index (CFI), critical value 0.967 indicating a strong evidence of unidimensionality for the scale (Table 4). Basing on the satisfaction of unidimensionality, validity and reliability parameters, and multicollinearity, the study was subject to estimate the model analysis.

Table-3. Factor loadings and internal consistency reliability

| Items | Path | Variables | Unstd. Estimates | Std. Estimates | p |

| UF3 | <--- | Usefulness | 0.760 | 0.500 | *** |

| UF2 | <--- | Usefulness | 0.795 | 0.518 | *** |

| UF1 | <--- | Usefulness | 1.000 | 0.625 | |

| EU3 | <--- | Ease of use | 0.863 | 0.538 | *** |

| EU2 | <--- | Ease of use | 1.000 | 0.767 | |

| EU1 | <--- | Ease of use | 0.739 | 0.528 | *** |

| R3 | <--- | Risk | 0.638 | 0.521 | *** |

| R2 | <--- | Risk | 1.000 | 0.841 | |

| C3 | <--- | Credibility | 1.000 | 0.545 | |

| C1 | <--- | Credibility | 0.836 | 0.585 | *** |

| M2 | <--- | Mobility | 1.000 | 0.758 | |

| M1 | <--- | Mobility | 0.819 | 0.689 | *** |

| S3 | <--- | Satisfaction | 0.628 | 0.575 | *** |

| S2 | <--- | Satisfaction | 1.000 | 0.688 | |

| I3 | <--- | Intention | 1.000 | 0.546 | |

| I1 | <--- | Intention | 0.903 | 0.497 | *** |

(Note: *** p< 0.001)

4.2. Measurement Model Fitness

The associations among constructs were examined by structural equation modeling to evaluate the direct influence of the model constructs (Figure 2). The current study employed most commonly used fit indices to assess the overall goodness of fit of the measurement model: Goodness of Fit Index (GFI), Adjusted Goodness of Fit Index (AGFI), Comparative Fit Index (CFI), Normalized Fit Index (NFI), Tucker-Lewis Index (TLI), Root Mean Square Error of Approximation (RMSEA), p-value, p-close and the ratio of Chi-square to degrees of freedom (CMIN/df). Overall fit statistics of the measurement model are found to be meeting their respective critical value (Hu and Bentler, 1999. Hair et al.2010 that representing a good model fit (Table 4).

Table-4. Model fit indices

| Indices | Recommended value | Model fit indices |

| p-value | ≥0.05 | 0.370 |

| CFI | ≥ 0.95 | 0.995 |

| CMIN/d.f. | < 3 | 1.043 |

| GFI | >0.90 | 0.967 |

| AGFI | ≥ 0.80 | 0.946 |

| NFI | ≥ 0.90 | 0.896 |

| TLI | ≥ 0.90 | 0.993 |

| IFI | ≥ 0.90 | 0.99 |

| RMSEA | ≤ 0.05 | 0.012 |

| p-close | ≥ 0.05 | 1.000 |

Source: AMOS output

Source: AMOS output

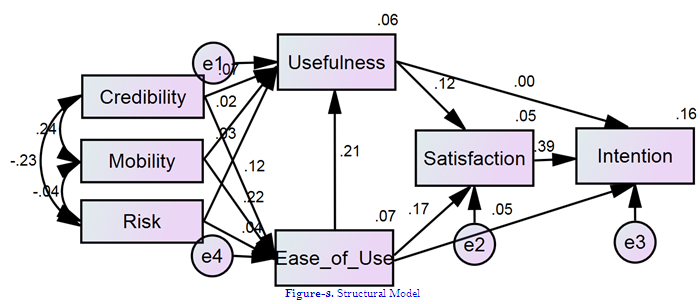

4.3. Structural Model-Hypotheses Testing

SEM was used to estimate the parameters of the structural model (Figure 3) and standardized solutions produced by AMOS maximum-likelihood method are shown in Table 5. The model is evaluated by inspecting the path coefficients (β weights) which outline the quality of association among the constructs.

4.4. Estimated SEM Equations

Continuance usage intention = {0.388(satisfaction) – 0.003(usefulness) + 0.051 (ease of use)}.

Satisfaction = {0.120(usefulness) + 0.167(ease of use)}.

Usefulness = {0.068(credibility) + 0.017(mobility) + 0.026(risk)}.

Ease of use = {0.123(credibility) + 0.219(mobility) + 0.044 (risk)}.

Continuance usage intention = [0.388{0.120(usefulness) + 0.167(ease of use)}-.003{0.068(credibility) + 0.017(mobility) + 0.026(risk)} + 0.051{0.123(credibility) + 0.219(mobility) + 0.044 (risk)}].

Source: AMOS output

Among the twelve paths proposed in the conceptual model, only six paths were significant; the path from credibility to ease of use (β=0.123, p<0.05), the path from mobility to ease of use (β=0.219, p<0.001), the path from usefulness to customer satisfaction (β=0.120, p<0.05), the path from ease of use to usefulness (β=0.209, p<0.05), the path from ease of use to customer satisfaction (β=0.167, p<0.001), and the path from satisfaction to continuance usage intention (β=0.388, p<0.001). These results statistically supported H1b, H2b, H4a, H5a, H5b, and H6. The summery of this causal model is illustrated in Table 5.

Table-5. Summary of hypotheses test

| Path proposed | Estimate | C.R. | P value | Supported | |||

| H1a | Credibility | ---> | Usefulness | 0.068 | 1.182 | 0.237 | No |

| H1b | Credibility | ---> | Ease of use | 0.123 | 2.195 | ** | Yes |

| H2a | Mobility | ---> | Usefulness | 0.017 | 0.301 | 0.764 | No |

| H2b | Mobility | ---> | Ease of use | 0.219 | 3.990 | *** | Yes |

| H3a | Risk | ---> | Usefulness | 0.026 | 0.471 | 0.637 | No |

| H3b | Risk | ---> | Ease of use | 0.044 | 0.797 | 0.425 | No |

| H4a | Usefulness | ---> | Satisfaction | 0.120 | 2.179 | ** | Yes |

| H4b | Usefulness | ---> | Intention | -0.003 | -0.066 | 0.948 | No |

| H5a | Ease of use | ---> | Usefulness | 0.209 | 3.736 | *** | Yes |

| H5b | Ease of use | ---> | Satisfaction | 0.167 | 3.014 | *** | Yes |

| H5c | Ease of use | ---> | Intention | 0.051 | 0.974 | 0.330 | No |

| H6 | Satisfaction | ---> | Intention | 0.388 | 4.458 | *** | Yes |

Note: *** p<0.001, **p<0.05

The structural model explains 16% of the variance in continuance usage intention of m-payment, 7% of the variance in ease of use, 6% of the variance in usefulness, and 5% in satisfaction. The path coefficient represented, satisfaction had a slightly higher direct influence on continuance usage intention with a total effect of 39%.

5. DISCUSSIONS AND MANAGERIAL IMPLICATIONS

The study empirically tests the antecedents of behavioral intentions and how they can be influenced by the effects of usefulness and ease of use of m-payment. Results suggest that ease of use increases the predictive power of continuance usage intention through explaining usefulness and customer satisfaction. Where, credibility and mobility are the main determinants of ease of use of m-payment service.

This study hypothesized and validated that ease of use of m-payment will have positive influence on customer satisfaction and usefulness, in addition it was assumed that credibility and mobility have significant positive influence on ease of use. The result supports these hypotheses H5a, H5b, H1b, and H2b. These findings are consistent with earlier studies of Riquelme and Rios (2010); Wessels and Drennan (2010); Yuan et al. (2014) and Kim et al. (2010). Therefore, it is expected that ease of use of m-payment system can play an important role in enhancing customer satisfaction and usefulness of m-payment service through the service credibility and mobility factors.

Additionally, current study proves the positive association between usefulness and customer satisfaction. Nonetheless, it has found a negative association between usefulness and continuance usage intention (Table 5), which is contradictory compared to the previous studies (Safeena et al., 2011; Yuan et al., 2014). The result portraits some confusing roles of risk factors on m-payment. Overall, customer satisfaction finds as the best determinant of continuous usage intention of m-payment service.

In the context of Bangladesh, the current study confirms the findings of Kabir (2013) and Ahad et al. (2012) that usefulness and ease of use have positive influence on consumer behavioral intentions toward m-payment. However, contradiction with them has aroused in some cases. Risk was significant and negatively related to m-payment, nonetheless, it was insignificantly positive in the current study. Additionally, in Ahad et al. (2012) study, ease of use was not found significant, however, the current study finds statistically significant association between ease of use and customer satisfaction, which is consistent with Kabir (2013).

This might happen because the customers in Bangladesh are not concerned about the usefulness or the risk involved in m-payment, or it may have been because of over dependency on ease of use or too much exposed to mobility. However, the findings of this paper confirm the existing body of literature and the importance of m-payment to customer service delivery. It shows that most of the service factors positively influence the consumer behavioral intentions.

The results of the current study significantly contribute to the theoretical and managerial understandings of customer behavioral intentions toward m-payment. This study has produced comprehensive understanding of the variables that appear to be most influential in this context. The comprehensive model suggests that credibility and mobility are the important determinants of m-payment. In other words, the model as a whole means that when a consumer forms behavioral intentions toward m-payment, consumers may retrieve the constructs directly or indirectly connected to it. From the practical point of view, as empirical result suggests, credibility, mobility, ease of use and satisfaction are the important factors that directly or indirectly affect the continuous usage intentions of m-payment. As a result, practitioners should take these factors into consideration when they design their marketing plans and service strategies. This study finds that satisfaction is significantly affected by ease of use and has significant impact on continuous usage intention of m-payment. Therefore, as well as designing useful and valuable service plans, managers should consider whether its actual performance meets or exceeds consumer expectations.

6. CONCLUSIONS

M-payment has now become an important banking service, and practitioners will be able to obtain grater benefits from it if they are able to make it more user-friendly. The results of the study increase the understanding of the continuous usage intention of m-payment, which is important for the sustainable growth of m-payment services. The ambition of this study was to provide imaginary insight and realistic guidance as to the antecedents of consumer behavioral intentions and how they can be attained by providing internal quality assurance and external factor considerations toward m-payment. The study results present the strong antecedents between customer satisfaction and continuous usage intention of m-payment. Furthermore, it produced positive association between usefulness and customer satisfaction, between credibility and ease of use, between mobility and ease of use, between usefulness and satisfaction, between ease of use and customer satisfaction. Results suggest to the practitioners that they may use these findings to design their effective service strategies and marketing plans.

Although, this study has produced some interesting results, limitations cannot be ignored. This study has attempted to discover major variables that logically and theatrically should impact the antecedents of behavioral intentions and their determinants of m-payment users. There might be other determinants of these relationships which were not considered in this study. Data were collected through convenient sampling method which may cause of sample bias. The instrument for examining the consumer behavioral intentions were adopted and modified from previous studies which might cause of linguistic bias. Therefore, future research in m-payment should integrate the limitations and more valuable attributes by using more comprehensive model which can generate more valuable findings.

| Funding: This study received no financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Aghdaie, S.F.A., R. Karimi and A. Abasaltian, 2015. The evaluation of effect electronic banking in customer satisfaction and loyalty. International Journal of Marketing Studies, 7(2): 90-98.View at Google Scholar | View at Publisher

Ahad, M.T., L.E. Dyson and V. Gay, 2012. An empirical study of factors influencing the SME’s intention to adopt m-banking in rural Bangladesh. Journal of Mobile Technologies, Knowledge & Society: 1-16.View at Google Scholar

Ahamed, B., S.M.M. Islam and K. Qaom, 2015. Customers’ attitude towards E-commerce in Bangladesh: An empirical study on some selected B2C E-commerce sites. Journal of Business and Technology, 10(1): 37-54. View at Google Scholar | View at Publisher

Ammari, N.B. and A. Bilgihan, 2017. The effects of distributive, procedural, and interactional justice on customer retention: An empirical investigation in the mobile telecom industry in Tunisia. Journal of Retailing and Customer Services, 37: 89-100.View at Google Scholar | View at Publisher

Au, Y.A. and R.J. Kauffman, 2008. The economics of mobile payments: Understanding stakeholder issues for an emerging financial technology application. Electronic Commerce Research and Applications, 7(2): 141–164. View at Google Scholar | View at Publisher

Bowen, J.T. and S.L.C. McCain, 2015. Transitioning loyalty programs: A commentary on the relationship between customer loyalty and customer satisfaction. International Journal of Conte Hospy Management, 27(3): 415–430.View at Google Scholar | View at Publisher

Brown, I.T.J., 2002. Individual and technological factor affecting perceived ease of use of web based learning technologies in a developing country. Journal of Intelligent Systems Developing country, 9(1): 1-15.View at Google Scholar | View at Publisher

Casalo, L.V., C. Flavián and M. Guinalíu, 2008. The role of satisfaction and website usability in developing customer loyalty and positive word-of-mouth in the e-banking services. International Journal of Bank Marketing, 26(6): 399-417. View at Google Scholar | View at Publisher

Davis, F.D., R.P. Bagozzi and P.R. Warshaw, 1989. User acceptance of computer technology: A comparison of two theoretical models. Management Science, 35(8): 982–1003.View at Google Scholar | View at Publisher

Ding, M.S. and J.F. Hampe, 2003. Reconsidering the challenges of M-payments: A roadmap to plotting the potential of the future M-commerce market. Paper Presented at the 16th Bled eCommerce Conference, Bled, Slovenia, June, 9–11.

Fornell, C. and D.F. Larcker, 1981. Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1): 39-50.View at Google Scholar | View at Publisher

Hair, J.F., W.C. Black, B.J. Babin, R.E. Anderson and R.L. Tatham, 2010. Multivariate data analysis. 7th Edn., New Jersey: Pearson Education Inc.

Hanafizadeh, P., M. Behboudi, A.A. Koshksaray and M.J.S. Tabar, 2014. Mobile-banking adoption by Iranian bank clients. Journal of Telematics and Informatics, 31(1): 62-78. View at Google Scholar | View at Publisher

Heesup, H. and S.H. Sunghyup, 2017. Impact of hotel-restaurant image and quality of physical-environment, service, and food on satisfaction and intention. International Journal of Hospitality Management, 63: 82-92.View at Google Scholar | View at Publisher

Hu, L.T. and P.M. Bentler, 1999. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternative. Structural Equation Modeling: A Multidisciplinary Journal, 6(1): 1-55. View at Google Scholar | View at Publisher

Kabir, M.R., 2013. Factors influencing the usage of mobile banking: Incident from a developing country. World Review of Business Research, 3(3): 96-114. View at Google Scholar

Karnouskos, S. and F. Fokus, 2004. Mobile payment: A journey through existing procedures and standardization initiatives. IEEE Communications Surveys and Tutorials, 6(4): 44–66.

Kim, C., M. Mirusmonov and I. Lee, 2010. An empirical examination of factors influencing the intention to use mobile payment. Journal of Computers in Human Behavior, 26(3): 310-322. View at Google Scholar | View at Publisher

Lu, Y., S. Yang, P.Y.K. Chau and Y. Cao, 2011. Dynamics between the trust transfer process and intention to use mobile payment services: A cross-environment perspective. Information and Management, 48(8): 393-403.View at Google Scholar | View at Publisher

Luran, P. and H.H. Lin, 2005. Toward an understanding of the behavioral intention to use mobile banking. Computers in Human Behavior, 21(6): 873–891. View at Google Scholar | View at Publisher

Mallat, N., 2007. Exploring consumer adoption of mobile payments-a qualitative study. Journal of Strategic Information Systems, 16(4): 413–432. View at Google Scholar | View at Publisher

Pham, T.T.T. and C.H. Jonathan, 2015. The effects of product related, personal related foctors and attractiveness of alternatives on consumer adoption on NFC-based mobile payments. Journal of Technology Society, 43: 159-172.View at Google Scholar | View at Publisher

Ram, J. and M.L. Wu, 2016. A fresh look at the role of switching cost in influencing customer loyalty: Empirical investigation using structural equation modelling analysis. Asia Pacific Journal of Marketing and Logistics, 28(4): 616-633.View at Google Scholar | View at Publisher

Ramayah, T. and M.C. Lo, 2007. Impact of shared beliefs on ‘‘perceived usefulness’’ and ‘‘ease of use’’ in the implementation of an enterprise resource planning system. Management Research News, 30(6): 420-431. View at Google Scholar | View at Publisher

Riquelme, H.E. and R.E. Rios, 2010. The moderating effect of gender in the adoption of mobile banking. International Journal of Bank Marketing, 28(5): 328–341. View at Google Scholar | View at Publisher

Safeena, R., N. Hundewale and A. Kamani, 2011. Customer's adoption of mobilecommerce: A study on emerging economy. International Journal of E-Education E-Business E-Management E-Learning 1(3): 228-233. View at Google Scholar

Sharma, S.K., S.M. Govindaluri, S.A. Muharrami and A. Tarhini, 2016. A multi-analytical model for mobile banking adoption: A developing country perspective. Review of International Business and Strategy, 27(1): 133-148. View at Google Scholar | View at Publisher

Venkatesh, V., M.G. Morris, G.B. Davis and F.D. Davis, 2003. User acceptance of information technology: Towards a unified view. MIS Quarterly, 27(3): 425-478.View at Google Scholar | View at Publisher

VeriFone, A., 2010. Cashless future on the horizon. Retrieved from http://www.verifone.co.uk/media/1420610/VeriFone_Cashless_Future_Contactless.pdf .

Wang, Y.S., Y.M. Wang, H.H. Lin and T.I. Tang, 2003. Determinants of user acceptance of internet banking: An empirical study. International Journal of Service Industry Management, 14(5): 501–519.View at Google Scholar | View at Publisher

Wessels, L. and J. Drennan, 2010. An investigation of consumer acceptance of M-banking. International Journal of Bank Marketing, 28(7): 547–568. View at Google Scholar | View at Publisher

Wilcox, H., 2014. NFC Mobile Payments to Drive Contactless Transactions to Reach Nearly $50 billion Worldwide by 2014: New Juniper Research Report.

Wu, J.H. and S.C. Wang, 2005. What drives mobile commerce? An empirical evaluation of the revised technology acceptance model. Information and Management, 42(5): 719-729.View at Google Scholar

Yuan, S., Y. Liu and R. Yao, 2014. An investigation of users’ continuance intention towards mobile banking in China. Journal of Information Development, 32(1): 20-34. View at Google Scholar | View at Publisher

Zea, O.M., D. Lekse, A. Smith and L. Holstein, 2012. Understanding the current state of the NFC payment ecosystem: A graph-based analysis of market players and their relations. Enfoque UTE, 3(2): 13-32.View at Google Scholar | View at Publisher