THE STUDY OF FACTORS AFFECTING THE TIMELINESS OF FINANCIAL REPORTS: THE EXPERIMENTS ON LISTED COMPANIES IN VIETNAM

1,2Hanoi University of Industry, Vietnam

3Thuongmai University, Vietnam

ABSTRACT

This paper studies the factors affecting the timeliness of financial reports (FR) of enterprises in Vietnam. This research uses panel data with 1070 observations, at 214 companies listed on Vietnam's stock market in the period 2012 - 2016. Retrieved results using the GLS method shows that there are 04 independent variables, including consolidated financial reports (CON), the audit firm (AUDIT), profitability (ROA) and the size of the business (SIZE) with relation to the timeliness of financial reports and statistical significance. There are two factors, including financial leverage (LV) and industry (INDUSTRY) which do not affect the timeliness of financial reports. In addition, the research results show that there are differences and statistical meanings in the publishing time of different types and starting times of financial reports. Based on those results, the authors have proposed a suggestion to boost the timeliness of FR.

Keywords:Timeliness Financial reports Vietnam. GLS method Profitability Financial leverage.

ARTICLE HISTORY: Received:11 January 2018. Revised:26 January 2018. Accepted:30 January 2018. Published:2 February 2018.

Contribution/ Originality:This study uses new estimation methodology, GLS method analysis to measure the factors affecting the timeliness of financial reports. Applying these exhaustive empirical methods result in: including consolidated financial reports, the audit firm, profitability and the size of the business with relation to the timeliness of financial reports.

1. INTRODUCTION

In the context of market economy, financial information plays a very important role in making business decisions. Misinformation, asymmetry leads to mistakes in decision-making, causing great damage to the individuals who used it. Therefore, to ensure transparency and truthfulness of financial information has always been a matter of primary concern of the managers, investors, credit institutions and other stakeholders. According to (IASB, 2010) the qualitative characteristics of information on the financial reports include: understandable, relevant, reliable and comparable. (IASB, 2010) gives the limitations of information quality are the balance between the benefits - costs; timeliness and the balance between the qualitative characteristics.

The overall purpose of financial reports is to provide helpful financial information of a certain unit for investors, present and future lenders, and for other creditors in making decisions for loan limits as one of the capital providers. It is the quality of financial reports that makes them useful. A financial report’s quality may be the fundamental or additional depending on their usefulness to the information of financial reports. Whatever characteristics, they all provide helpful information for FR (IASB, 2010). The converted idea of IASB and FASB on the quality of information SFH has two basic qualitative characteristics (Suitable, presented honestly) and four additional qualitative characteristics (comparable, verifiable, timeliness, understandable)

Timeliness: the characteristic of timeliness means that the information is available for the decision makers before it lost its value and the ability to influence those decisions. Having appropriate information sooner equals the fact that you can increase the level of its influence to the decisions and its delay may endanger its core and potential values. However, there is some information can still be viewed as timely even though its reporting time ended long ago because the user can still use and refer to it when making decisions. For example, information users need to identify the trend of volatility of many categories in FR to make decisions of investing or lending.

In the world, there have been a lot of studies on the timeliness of financial reports of listed companies in the stock market from a variety of different angles, in the developed and developing countries. Vietnam is a growing economy, in which there are regulatory, business environment and the uncompleted development of the stock market, so the research topic for the timeliness of financial reports will be much sense, although Vietnam had had a few previous studies on this topic. Based on the research review, the authors found some gaps of previous studies, such as narrow research scope, using data from the financial reports of listed companies only in a period of 1 year or 2 years, small study sample size, resulting in low reliability, limiting the generalization of research findings; some researches only testify the differences without regression estimations or strict observations to establish the most suitable module, and also has not clarified the differences in the timeliness of FR when deciding the end of annual auditory working schedule. Therefore, the authors extend this research by identifying more comprehensively the factors affecting the timeliness of financial reports so that there can be proposals to improve the timeliness of financial reports of businesses.

2. THEORETICAL BASIS

2.1. The Concept of Timeliness

According to Akle (2011) the timeliness of financial reports is understood that financial statements must be published to users when they need them to make decisions, because information loses its usefulness if it is not available when needed. Ahmed and Karim (2005) claimed that the timeliness of the preparation of the financial reports as a function of the variables related to the auditor and the units having financial reports audited, including: (i) the time needed to complete audited financial reports, (ii) the decision of the board of directors of the publication of the financial reports, (iii) legal requirements for minimum number of days between the date to hold the annual shareholders' and the date of notification of the time annual congress and (iv) other factors supporting as the availability of time or venue for the annual convention. According to the authors (Karim et al., 2006) the timeliness of the preparation of financial reports is influenced by two groups, including external factors (such as legal regulations, competitors) and internal factors (such as the characteristics of the company), and consists of three categories: the timeliness of audit activities, the timeliness of the publication of the report and overall timeliness. Meanwhile, Aktas and Kargin (2011) suggests that the timeliness is defined as the number of days between the end of the accounting year and the day that listed companies must publish financial reports in accordance with law. In this article, timeliness is interpreted as the timeliness of the activities of independent audit financial reports, as measured by the number of days from the date of the balance sheet in accordance with the law to the date of publication of the audited financial reports.

2.2. Theoretical Basis

Theory mandate: Mandate theory refers to the relationship between the owners of the business capital and another party is the operator - who represents the implementation of business decisions. According to Jensen and Meckling (1976) the demarcation between ownership and control of enterprises raises the risk of making the performance not at an optimal level, causing damage to investors. In the relationship between the owner and the operator, the operator can make decisions aimed at maximizing their personal interests instead of maximizing corporate value. Acts of personal interests of the executives also includes the use of many resources of the enterprise in the form of perks and avoid the risk, i.e. the executive risk aversion will reject investment opportunities unprofitable for the owners. Meanwhile, the owners want to maximize their benefits through the increased value of the business. When enterprises separation of ownership and management will appear delegate relationship managers (the assignee) - Owner (the mandate). This relationship leads to a problem is the information asymmetry between owners and managers. Managers control all activities of the enterprise, has the advantage in capturing information. Meanwhile, owners, investors need information for decision-making purposes to difficult access to information. To control the operation of the business, the owner must go through the control activities and reports increases monitoring costs. Disclosure of information is the management as a tool to reduce costs delegate because it reduces the information asymmetry between shareholders and management, reduce costs credentials. In mandate theory, as for the majority of enterprises operating in large scale, the conflict between the mandate and the assignee is very significant because the corporate executives often possess only a very small part stock part. Therefore, to limit mandating cost, operators need more disclosure to shareholders. Thus, the mandate theory has contributed to explain the influence of the scale factor to the disclosure. In addition, the theory mandate also helps to explain the influence of factors of profitability to the disclosure, as those companies with high profits, managers want to publish information more to demonstrate the capability of their management.

Theory information useful for decision making: Useful theory information came into existence in the 1960s, opening the first phase orientation on the use of accounting information useful to serve the appropriate decision. This theory is considered the theoretical foundation for the construction of the international accounting standards. In 1973, this theory was widely considered in the US with the objective of financial reporting is to provide useful information for decision making. On the other hand, this theory leans towards the usefulness of information for users than meets the requirements by law. Through orienting appropriate decisions, the focus has shifted from the accounting principles to the result of the accounting process in which information is provided. Useful theory information for decision making stems from the objective of accounting is to provide useful information for users to make economic decisions (Staubus, 2000) based on which, the qualitative characteristics of financial reports were identified. First Financial Reports should include the relevant information, which is the information that can help users to assess the past and predict the future of the business. Furthermore, this information should express actual business situation, which means true nature of economic phenomena. In addition, other minor requests such as comprehensible presentation, comparability, examining ability and timeliness must be met. The aforementioned qualitative characteristics are the foundation for construction or selection of accounting policies of the business (IASB, 2010). When being applied at the publication of financial reports, this theory requires financial reports to provide necessary information and timely decision making of users, which include two main investor and debt owner.

3. RESEARCH OVERVIEW

During the past time, in countries in the world and in Vietnam, there have been many studies affecting the timeliness of financial reports, case studies such as Ashton et al. (1989) were performed based on 465 companies listed on Canadian stock markets from 1977 - 1982. The results showed that the variables have a consistent relationship with the progress of the audit report completed in 6 years, categorizing by kind of the auditor, the field work action, the occurrence of special events and signs of net income. Owusu-Ansah and Leventis (2006) conducted a study on the factors affecting the timeliness of the publication of the financial reports of 95 non-financial companies listed on the stock market of Greece. Regression results of analysis showed that the large-scale enterprises, service firms and companies are audited by the auditing firm of the Big 5 take shorter time to publish financial reports. In addition, the study provides empirical evidence about the companies of the construction sector with an audit opinion not being the opinion accept full and enterprises with shares held directly and indirectly by people in business will not publish financial reports on time. Ezat and El-Masry (2008) focused on studying the factors that affect the timeliness of disclosure of financial reports over the 50 listed enterprises in Egypt in 2006. The research results show that relationship between the timeliness of disclosure of information through the network and the size of the company, field of activity, liquidity, shareholder structure, board composition and size of the administration. Specifically, firms operating in the service sector with large scale, high proportion of liquidity, high composition of independent directors and many members in the board will disclose information of financial reports timelier online.

Alkhatib and Marji (2012) focused on studying the factors that affect the timeliness of the audit reports of 137 companies listed in the Jordanian stock market in 2010. The study concluded that the rate of profits, the kind of audit company and company size in service companies are not related to the timeliness of audit while financial leverage has relationships with important implications for the timeliness of audit. In addition, the results also showed that in companies in the industrial sector, the ratio of profitability, types of audit firms, firm size and financial leverage will not affect the timeliness of audit reports. Khasharmeh and Aljifri (2010) could perform on a sample of 83 companies listed in 2004. The analysis results showed profitability, debt ratios, business type and ratio of dividend payments have a strong influence on the timeliness of the disclosure while the relationship between the type of audit firm, company size, ratio of price earning section and the disclosure of financial information is more promptly weak or has no relationship to each other. Model study AL-Shwiyat (2013) was performed on the sample included 120 companies listed on the stock market Jordan in 2012. The authors concluded that the time limit for financial reports publication is 111 days after the end of the financial year; the business activities in the industrial sector takes more time to publish financial reports while the enterprises activities in the banking sector are the fastest disclosure compared with other sectors. In addition, regression analysis results also show that company size, the longevity of enterprise debt rate and timeliness of financial reports disclosure statistically correlated with each other. Meanwhile, factors earnings per share (EPS) and timeliness of financial information has no relationship with each other.

In Vietnam (Tan, 2013) has carried out research in two consecutive years 2010 and 2011 with 175 observations; research results show that there is a relationship between the timeliness of financial reports of listed companies with the kind of auditors, in contrast to previous studies that the Big4 audit firms belonging tends to perform longer audit so that audit quality is higher. At the same time there are differences in the timeliness of financial reports by listed companies through two years 2010 and 2011. Vy and Khuong (2016) carried out research with data 100 listed companies have announced in the financial reports the period 2012 - 2014, using quantitative methods, the authors concluded that the number of subsidiaries, the complexity of the operation (representing the structural characteristics) profitability and annual audit opinion are the variables that affect the timeliness of the financial reports. Pham (2016) with sample includes 77 listed companies (on the HCMC Securities Exchanges) 2010-2014. The author uses quantitative research methods to assess the impact of these factors on the timeliness of financial reports. The study results showed that factors: Type of financial statements, business profits, type of audit firms, and financial leverage has a positive impact on the timeliness of financial reports. Meanwhile, factors of company size and business line negatively impact the timeliness of financial reports.

Through theoretical basis and a review of previous studies indicating that the studies in Vietnam research scope is narrow, using data from the financial statements of listed companies in recent period; the small sample study results in high reliability, yet not fully studied the factors affecting the timeliness of financial reports.

4. RESEARCH MODULES AND METHODS

4.1. Hypotheses

The consolidated financial reports: financial reports can be classified in several ways: summary reports and the completed ones, individual financial reports and consolidated ones, regular financial reports and ones with special purpose. Aktas and Kargin (2011) said that the complexity of financial reports also affects timeliness. Therefore, the consolidated financial reports of the parent company are usually announced later than other companies. This influence can be explained by a number of reasons as follows: First, the parent company must wait subsidiaries to submit the evaluated data for their end-of-year financial reports, then the handling and comparison of data and implementation of consolidation procedures; Second, the time to audit the consolidated financial statements is longer than that for the individual reports. Because apart from the need to implement procedures for individual financial statements, the auditor should perform additional procedures such as audit or review of the company members, comparing the internal transactions between the unit members and audit journal entries consolidation, meaning that businesses establish consolidated financial statements have time to publish the audit report will be longer than the now established SFH individual. Therefore, the assumption was made:

H1: Enterprises set up consolidated financial reports have affected positively and significantly to the timeliness of financial reports.

Accounting Company: audit firms often appear in many previous studies, and most of the studies concluded that: the factor of audit firms may affect the timeliness of financial reports, as firms often hold large auditing processes, supporting tools, such as sample selection tools, analysis tools and process information ... as well as support (tax department, IT department information and consultancy division, valuation). Therefore, the income of the audit evidence can be carried out more efficiently, saving time and resources according to Owusu-Ansah and Leventis (2006). According to Gilling (1977) delays of the audit for audit firms in Big 4 are expected to be less than the audit of other audit firms, because they are large enterprises, may perform audits more efficiently, and greater flexibility in scheduling to complete audits in a shorter time. However, there are mixed opinions about these aforementioned research results, because customers of audit firms most often are the companies that operate in large-scale, so that these customers need a long time to closeout accounting and financial reporting. In addition, the number of customers of the large accounting firms audit more than other firms. Therefore, the assumption was made:

H2: Big 4 audit companies have negatively influential relationships and are statistically significant to the timeliness of financial reports.

Profitability: Profit is a variable to be considered in many previous studies. Business operations profitability in the year is considered a good information, and vice versa trading company losses or low profits, it is considered bad news. According to Basu (1997) the companies which usually have good news publish earlier financial statements than the companies that do not have. Afify (2009) indicate that companies will not be willing to disclose bad information to the public, so they will delay the publication of the financial statements. Therefore, the assumption was made:

H3: Profitability of corporations influences negatively and is statistically significant to the timeliness of financial reports.

Enterprise scale: There are two opposite views on the relationship between firm size and the timeliness of financial reporting. The first point that large companies often delay the announcement of financial statements, because large companies have wide business network, the volume of products and services is larger, the structure is more complex than small firms. Thus, the volume of accounting information in big companies is a lot, so accountants need more time to process the data and make financial statements, Ahmed and Hossain (2010) have supported this view. The second point is that large companies often publish financial statements more quickly than small companies, because most large companies have accounting software support and the number of accountants are more than in small companies, thus the time set in the financial statements of large companies is shortened (Haw and Ro, 1990). Moreover, larger sized company equals that the number of shareholders will be more and more, so large companies need to rapidly release financial statements to the shareholders to serve their decision making. Therefore, the assumption was made:

H4: Enterprises Scale have negatively influential relationship and is statistically significant to the timeliness of financial reports.

Financial leverage: The company which has high rate of financial leverage is more likely bankrupt and auditors face a higher risk of litigation if done improperly. Therefore, auditors can be expected to carry out audit work which is relatively detailed, and therefore, the time to perform and complete the audit work will be longer. Research (Owusu-Ansah, 2000); (Ahmed and Hossain, 2010) suggests that there is a positive relationship between financial leverage and delaying the audited financial statements. Therefore, the assumption was made:

H5: Financial leverage has affected positively and statistical significance to the timeliness of financial reports.

Industry: The business has different characteristics in production processes, thus affecting the preparation of financial statements and audit work, so some researchers have previously used transformer industry as a variable explaining the timeliness of financial reporting. Results of Türel (2010) show that companies working in the industry of producing reports more timely, while according to Che-Ahmad and Abidin (2008) the time to publish financial statements of the financial companies are often shorter than the non-financial ones. By the non-financial companies often add other items such as inventory, accounts receivable, in addition to financial companies in the study were auditing the majority of audit firms big in the Big 4 and change audit firms should also less time will be faster audit non-financial companies. Apart from that, the results of Ahmad and Kamarudin (2003); Aktas and Kargin (2011) showed that companies working in the financial sector have the tendency to delay in reporting. Therefore, the assumption was made:

H6: Enterprises of industrial manufacturing industry are positively influential and statistically meaningful to the timeliness of financial reports.

4.2. Model Research

Based on the research overview, the hypothesis was built with the purpose of reviewing the empirical data of the Vietnamese businesses, identifying the factors that affect the timeliness of financial statement, the equations of regression model are as follows:

Uit : Random error

Financial statement disclosure time limit: is the goal of the factor model of research, the timeliness of the financial statement is meant to be the timeliness of financial statement audit activities are announced. Financial statement disclosure period will be calculated as follows:

Financial statement disclosure period audited year (TIME) = date of publication audited Financial Statement-fiscal year end date.

Table-1. The independent variables in the model

4.3. Research Data

To perform this study, the authors collected data of enterprises listed on the Ho Chi Minh Stock officials in the period 2012 - 2016. As of 2012 there are 306 businesses, after eliminating financial enterprises, there are 289 enterprises remaining. Among the businesses to collect data, only 214 enterprises have sufficient information to determine the variables in the research model in the period from 2012-2016, data collected from financial reports, consolidated financial reports have been audited.

4.4. Methods of Data Analysis

The research data are aggregated in the form of tables (panel data), data tables, cross-over units in aerial order, Cross section (enterprises in our samples) were surveyed in chronological order - time series. The procedure of study includes the following steps:

+ Fundamental analysis is performed firstly with aims to refine the research model, to eliminate the observations which are too large, too small, or too different from the sample size. This basic analysis step helps to check the relevance of the study before the implementation of regression analysis methods, including OLS FEM, REM and GLS, to ensure reliability for quantitative research results. Specific author groups will conduct analysis of statistical description, correlation analysis to eliminate the phenomenon of most online communities between the independent variables.

+ Research will proceed to determine if the independent variables have a statistically significant impact by evaluating index control for regression multivariate models. The data used to perform this test step are the full-size template, including all the financial reports of enterprises listed on the HOSE in 5 years from 2012-2016. The purpose of this work is to find out which independent variables have a statistically significant relationship to dependent variables, and from there will give the appropriate policy, thus the effectiveness in improving the timeliness of disclosure of information in the financial reports.

5. RESULT AND DISCUSSION

5.1. Research Outcome

The statistical data (Table 2) shows that the medium time of announcement of the audited financial statement is 83,298 days, in which the earliest is 9 days after the end of the accounting period and the latest is after 212 days. Among the surveyed businesses, the number of businesses made the consolidated financial statement accounted for 59.1%, and the rate of the financial statement audited by auditing enterprises Big 4 is 35.3%. The rate of profit after tax on average is 6.1% property, financial leverage ratio of average enterprises is 46.9%.

Table-2. Descriptive statistic among variables in the model

| Variables | Number of observations | Medium | Standard deviation | Minimum value | Maximum value |

| TIME | 1070 | 83.298 | 17.119 | 9 | 212 |

| CON | 1070 | 0.591 | 0.492 | 0 | 1 |

| AUDIT | 1070 | 0.353 | 0.478 | 0 | 1 |

| ROA | 1070 | 0.061 | 0.085 | -0.646 | 0.784 |

| SIZE | 1070 | 13.491 | 1.503 | 7.885 | 17.885 |

| LV | 1070 | 0.469 | 0.215 | 0.002 | 0.977 |

| INDUSTRY | 1070 | 4.150 | 2.709 | 1 | 9 |

Source: data in financial reports from the HSX, the author calculated from Stata 13.0

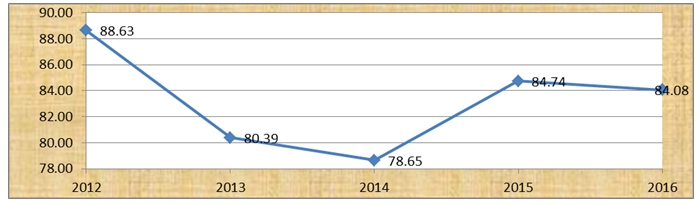

In the period 2012-2016, the time publishing audited financial statement is 83,298 days, in which the year 2012 is the latest with 88.63 days and the 2014 is the fastest year with the number of days average 78.65. However, the next year in 2015, the year 2016-time period audited financial statement disclosure increased, average time to publish audited financial statement is about 84 days.

Figure-1. Average number of days publishing audited financial statements 2012-2016 stage Source: Data in Financial Statements from the HSX, the author calculated from Stata 13.0

Table-3. Inspection result of the difference among the date of publication Audited Consolidated Financial Statements

| Content | Classification | Observation Number | Medium | Degrees of freedom | t | Pr |

| Types of Financial Statement | Individual Financial Statement | 438 | 80.1347 | 1068 | -5.0904 | 0.0000 |

| Consolidated Financial Statement | 632 | 85.49051 | ||||

| Accounting Periods | Accounting period ending calendar year | 1044 | 83.61782 | 1068 | 3.8964 | 0.0001 |

| Accounting period on the other end of the calendar year | 26 | 70.46154 |

Source:data in financial reports from the HSX, the author calculated from Stata 13.0

From table 3, we can see that the announcement time of the audited Financial statement for the businesses who set up individually is 80,13 days and for the ones who set up consolidately is 85.49 days, therefore, for the businesses with complex models or have a subsidiary, the announcement time of consolidated financial statement is later than that of individual audited financial statement, the results of checking the average differences shows significant difference with 99% reliability. Financial statement establishment periods of enterprises listed primarily on the calendar year (accounting 97.57%), there are very few businesses that created the financial statement in the end other end on December 31, statistical results indicates that the average time of enterprises who published audited financial statement having the other end of calendar year is 70.46, whereas the enterprises who set up the financial statement according to the calendar year have the average time of 83.61 days. Checking the difference shows the time announcing audited financial statement by accounting period is different and at the statistical significance level of 1%.

When considering the time announcing audited financial statement in the 2012-2016 stage, statistical results from table 4 shows that the industry has the earliest time, with the average publication time is 80,896 days, meanwhile the Real estate and Construction is the latest publishing the audited financial statement. Using the ANOVA test, with Bartlett's test results (table 5) shows that the variance of audited financial statement disclosure date with Prob > chi2 0.000 < = 0.05 is not uniform, so ANOVA test results cannot be used. Using non-parametric test Kruskal-Wallis, results showed that chi-squared = 22,486 with degrees of freedom (df = 8) and probability = 0.0041 < 0.05 can affirm the difference of time published audited financial statement between sectors.

Table-4. The average number of days publishing audited financial statements between sectors

| Sectors | Medium | Standard Deviation | Observation number |

| Real estate and Construction | 86.186 | 16.141 | 345 |

| Technology | 83.800 | 11.645 | 15 |

| Industry | 80.896 | 14.190 | 125 |

| Service | 81.945 | 20.399 | 110 |

| Consumer Goods | 84.611 | 15.014 | 95 |

| Energy | 83.400 | 11.755 | 85 |

| Agriculture | 81.436 | 19.922 | 140 |

| Materials | 80.327 | 20.343 | 110 |

| Health | 81.067 | 17.002 | 45 |

| Total | 83.298 | 17.119 | 1070 |

Source:data in financial reports from the HSX, the author calculated from Stata 13.0

Table-5. ANOVA test the average number of days announcing the audited Financial Statements between sectors

| Source | SS | df | MS | F | Prob > F |

| Difference between groups | 5647.619 | 8 | 705.952364 | 2.43 | 0.0131 |

| In group | 307632.3 | 1061 | 289.945596 | ||

| Total | 313279.9 | 1069 | 293.058837 | ||

| Bartlett's test | for | equal variances: chi2(8) = 56.5648 Prob>chi2 = 0.000 | |||

Source: data in financial reports from the HSX, the author calculated from Stata 13.0

On the basis of 9 branches in the form of dramatic survey, for the real estate industry and construction, technology, industry, energy, raw materials are the industrial production sector, is encoded by = 1; the rest is encrypted = 0

Table-6.Correlation matrix

| TIME | CON | AUDIT | ROA | SIZE | LV | INDUSTRY | |

| TIME | 1 | ||||||

| CON | 0.1539 | 1 | |||||

| AUDIT | -0.1184 | 0.0943 | 1 | ||||

| ROA | -0.2206 | -0.0694 | -0.0451 | 1 | |||

| SIZE | -0.0677 | 0.2547 | 0.0946 | 0.1853 | 1 | ||

| LV | 0.0451 | 0.0583 | 0.0402 | -0.4077 | 0.3481 | 1 | |

| INDUSTRY | 0.0437 | -0.0657 | -0.0823 | -0.1396 | -0.1598 | 0.1535 | 1 |

Source: data in financial reports from the HSX, the author calculated from Stata 13.0

From table 6, the results of the correlation coefficient between the variables, the purpose of checking the correlation tight between the independent variables and the dependent variable is to eliminate the factors that may lead to multicollinearity before running regression models. The correlation coefficient between the independent variables in the model is no greater than 0.8 pairs so it is less likely to occur multicollinearity between the independent variables, using regression models that authors VIF coefficients used for inspection.

The author will compare and choose which model would be the appropriate model: OLS, FEM or REM. To consider and choose between 3 models to fit regression method, the author uses inspection and testing F Hausman. By testing the F shows Prob> F = 0.000 <α = 5%, with statistical significance level of 5%, H0 would be rejected. That is, with collected data, we can see that method of running FEM models is suitable and OLS is inappropriate because of the existence of fixed effects in each business over time. After selecting the FEM model instead of running OLS method, the study authors estimated respectively enters table data based on the method has run model FEM and REM. Results from FEM and REM models running the authors will go testing to compare selected Hausman model FEM or REM. Inspection results are presented in Table Hausman 7. We see, Prob> chi2 = 0. 000 means P_VALUE = 0.000 <α = 5%, thus sufficient grounds to reject the hypothesis H0, the estimated fixed effects (FEM) is suitable than the estimate random effects (REM). Through the accreditation methods run FEM model is the best model selected. Use of accreditation: variance change, multicollinearity, autocorrelation and made the necessary adjustment to overcome the limitations of the model.

Inspection of the variance change phenomenon: To test if there is variance model change or not, the authors use the Modified Wald test verification. Assuming H0: no change phenomenon variance, H1: there is the phenomenon of variance change. Inspection results for P-value value is small (less than 0:05 implicit) assumption H0 is rejected and H1 accepted assumptions. Based on the results in Table 7 P_VALUE coefficients <α = 0.05 level. So H0 hypothesis is rejected. Results tested models show the value P-value received were of 0.000 <α (5%), this implies the hypothesis H0 is no phenomenon of variance change in the model is rejected for Statistical significance level of 5%. Therefore, the author conducted with disabilities overcome the regression model using regression methods GLS.

Table-7. Multivariate regression results

| VIF | OLS Models | FEM Models | REM Models | GLS Models | |

| CON | 1.16 | 5.138*** | 1.854 | 5.138*** | 5.032*** |

| [3.68] | [0.72] | [3.68] | [8.10] | ||

| AUDIT | 1.17 | -17.42*** | -20.20*** | -17.42*** | -16.35*** |

| [-4.63] | [-4.09] | [-4.63] | [-2.98] | ||

| ROA | 1.51 | -34.51*** | -23.98*** | -34.51*** | -36.22*** |

| [-4.64] | [-2.76] | [-4.64] | [-8.34] | ||

| SIZE | 1.72 | -0.425 | 0.433 | -0.425 | -0.467** |

| [-0.81] | [0.43] | [-0.81] | [-2.03] | ||

| LV | 1.16 | -1.34 | 0.187 | -1.34 | -0.753 |

| [-0.37] | [0.03] | [-0.37] | [-0.46] | ||

| INDUSTRY | 0.473 | 0 | 0.473 | 0.468 | |

| [0.30] | [.] | [0.30] | [0.64] | ||

| _cons | 88.83*** | 78.21*** | 88.83*** | 91.24*** | |

| [13.52] | [5.82] | [13.52] | [31.10] | ||

| N | 1070 | 1070 | 1070 | 1070 | |

| R-sq within | 0.0225 | 0.0266 | 0.0225 | ||

| R-sq between | 0.1731 | 0.1016 | 0.1731 | ||

| R-sq overall | 0.0898 | 0.061 | 0.0898 | ||

| Checking F | F (6, 1063) = 15.46 | F (5,851) = 1.28 | |||

| Prob > F = 0.0000 | Prob > F = 0.2685 | ||||

| Checking LM | Wald chi2(6) = 43.10 | Wald chi2(5) = 804.71 | |||

| Prob > chi2 = 0.0000 | Prob > chi2 = 0.0000 | ||||

| Checking Hausman | chi2(5) = 11.57 | ||||

| Prob>chi2 = 0.0412 | |||||

| Modified Wald test | chi2 (214) = 4.3e+05 | ||||

| Prob>chi2 = 0.0000 | |||||

| Wooldridge test | F( 1, 213) = 2.121 | ||||

| Prob > F = 0.1467 | |||||

| t statistics in brackets * p<0.1, ** p<0.05, *** p<0.01 | |||||

Source: data in financial reports from the HSX, the author calculated from Stata 13.0

Check the self-correlation phenomenon: Method Wooldridge test is used to test whether the self-correlation or the regression model. Put hypothesis: H0: no autocorrelation phenomena; H1: the phenomenon of autocorrelation. Inspection results for P_VALUE = 0.1467 value> α = 0.05 accept H0 hypothesis, i.e. no autocorrelation phenomena occur.

Check the phenomenon most plus online: to detect the phenomenon most plus online in the model, the author uses the magnification coefficient of variance (VIF-Variance Inflation Factor). There are many different suggestions for the value of VIF, but the most common is 2, which is the maximum level of VIF which exceeds that value can cause the phenomenon most online communities. Results the coefficient of the variable are smaller than VIF 2, proves not triggered the phenomenon most online communities.

The regression results by GLS: After performing regression and testing, we can choose a suitable model, the FEM, the author conducted remedy the defects were discovered the pattern by means of GLS (Generalized least squares). The results are presented in Table 7 as the results have been overcome the defects of the model.

5.2. Research Results Discussions

From the findings, the authors offer a number of discussions:

- Consolidated Financial Statements factor (CON), has positively related to the timeliness of financial reporting and statistical significance with a statistical significance 1 %, consistent with the hypothesis H1 initial construction, the research results are consistent with studies of Aktas and Kargin (2011); Pham (2016); Vy and Khuong (2016) studies are said that the complexity of SFH also affect timeliness. Therefore, the consolidated Financial Statements of the parent company are usually announced later than other companies. The study results showed that businesses must prepare consolidated Financial Statements which are usually longer than the individual Financial Statements, due to the complexities and processes up consolidated Financial Statements.

- Audit firm factor (AUDIT) is related inversely to the timeliness of financial reporting and statistical significance at 1%, so hypothesis H2 is accepted. This study is similar to results of the study Owusu-Ansah and Leventis (2006); Vy and Khuong (2016). However, contrary to the findings of Gilling (1977); Pham (2016). Thus, the results show that the Financial Statements audited by Big 4 firm implemented a shorter time.

- Profitability factor (ROA) for the regression results in the opposite direction and statistically significant at 1% affecting the timeliness of financial reporting, the research results are consistent with findings of Basu (1997) Trueman (1990); Carslaw and Kaplan (1991); Afify (2009). However, study results are contrast with research (Pham, 2016) the timeliness of financial reporting positively related to profitability, in addition, study results do not resemble study Vy and Khuong (2016) the timeliness of financial reporting has no relationship with profitability.

- Scale enterprises factor (SIZE), is related inversely to the timeliness of financial reporting and statistical significance level of 5%, the research results are consistent with the hypothesis H4 originally built while similar to the results of the study Ahmed and Hossain (2010); Haw and Ro (1990); Pham (2016).

- factor of financial leverage (LV) are not related to the timeliness of financial reporting, research results are inconsistent with the hypothesis H5 original construction, while not comparable with the results of research (Owusu-Ansah, 2000); (Ahmed and Hossain, 2010); (Pham, 2016).

- Industry factor is to reverse the regression results, but not significantly affect financial reporting timeliness, research results are not consistent with hypothesis H6 original building. The study results do not resemble study Che-Ahmad and Abidin (2008); Ahmad and Kamarudin (2003); Aktas and Kargin (2011); Türel (2010) and Pham (2016).

6. CONCLUSIONS AND RECOMMENDATIONS

6.1. Conclusions

With research and experimental results, the author uses data tables and 1070 which were studied in 214 enterprises to seal Vietnam stock exchange from 2012 to 2016, according to the regression analysis method is OLS stable, FEM, and the independent variable is Consolidated Financial Statement (CON), Unifi Inc audit (AUDIT), capacity (ROA profit), the scale of the enterprise (size), financial leverage (level) and industry (industry). In order to overcome the defects of changes such as variance, autocorrelation, the author uses GLS regression method. By means of regression results show that the GLS variable, audit, ROA, size of the relationship to calculate the time of financial reports, meaningful and suitable statistical theory is established. There are two factors that affect the industrial grade, but no statistically significant time to calculate financial reports, in addition, the results of the study show that there were statistically significant differences in time, financial reports have announced in the financial reports audit type in order to establish the duration of financial report years. The design of the study is to determine that the number of models is low (Table 7).

6.2. Recommendations

- For investors in the stock investment decision, they need to pay attention to the accounting information released in time and audited financial statement because this information will affect the decision-making ability of investors. The businesses which are good, large scale, accounting firms usually audit and announce financial statements sooner than other enterprises; it is a sign that people can be informed of high quality information from these enterprises.

- Enterprises need to publish full Financial Statements information, this will help investors, credit institutions, suppliers obtain useful information for decision making. Hence, companies themselves need to ensure the quality of Financial Statements published to create and maintain the confidence of investors for enterprises. This not only sets the stage for the confidence of investors for information in Financial Statements which are now published, but also helps businesses get position and improve corporate value to attract potential investors. The full disclosure and timely Financial Statements, audit reports, the report of the board of directors will create confidence for investors on transparency in information disclosure, and is a good signal to attract investors. Businesses may consider reviewing other options of accounting period within the calendar year; this will facilitate the enterprise to publish Audited Consolidated Financial Statements sooner, because if all enterprises accounting period ended in the last days of the calendar year, it will make it difficult for companies to arrange auditing staff to perform the audit, by which time the audit will last longer, affecting the timeliness of financial reports. Enterprises also need to increase the potty published Financial Statements in English, based on the survey of 1070 financial reports, only 09 Financial Statements are presented in English, so that businesses will have difficulty in attracting top private foreign investors, limitations with comparing business performance and the financial situation of enterprises in Vietnam with businesses in the region and the world.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Afify, H., 2009. Determinants of audit report lag: Does implementing corporate governance have any impact? Empirical evidence from Egypt. Journal of Applied Accounting Research, 10(1): 56-86. View at Google Scholar | View at Publisher

Ahmad, R.A.R. and K.A. Kamarudin, 2003. Audit delay and the timeliness of corporate reporting: Malaysian evidence. Paper Presented at the Communication Hawaii International Conference on Business. June, University of Hawaii-West Oahu.

Ahmed and M.S. Hossain, 2010. Audit report lag: A study of the Bangladeshi listed companies. ASA University Review, 4(2): 49-56. View at Google Scholar

Ahmed, J.U. and A. Karim, 2005. Does regulatory change improve financial reporting timeliness? Evidence from Bangladeshi listed companies: 1-37. Retrieved from https://www.victoria.ac.nz/sacl/centres-and-institutes/cagtr/working-papers/WP30.pdf .

Akle, Y.H., 2011. Financial reporting timeliness in Egypt: A study of the legal framework and accounting standards. Internal Auditing & Risk Management, 6(1): 81-91. View at Google Scholar

Aktas, R. and M. Kargin, 2011. Timeliness of reporting and the quality of financial information. International Research Journal of Finance and Economics, 63(1): 71-77. View at Google Scholar

AL-Shwiyat, Z.M.M., 2013. Affecting factors on the timing of the issuance of annual financial reports" empirical study on the Jordanian public shareholding companies". European Scientific Journal, 9(22): 407-423. View at Google Scholar

Alkhatib, K. and Q. Marji, 2012. Audit reports timeliness: Empirical evidence from Jordan. Procedia-Social and Behavioral Sciences, 62: 1342-1349. View at Google Scholar | View at Publisher

Ashton, R.H., P.R. Graul and J.D. Newton, 1989. Audit delay and the timeliness of corporate reporting. Contemporary Accounting Research, 5(2): 657-673.View at Google Scholar | View at Publisher

Basu, S., 1997. The conservatism principle and the asymmetric timeliness of earnings. Journal of Accounting and Economics, 24(1): 3-37.View at Google Scholar

Carslaw, C.A. and S.E. Kaplan, 1991. An examination of audit delay: Further evidence from New Zealand. Accounting and Business Research, 22(85): 21-32. View at Google Scholar | View at Publisher

Che-Ahmad, A. and S. Abidin, 2008. Audit delay of listed companies: A case of Malaysia. International Business Research, 1(4): 32-39. View at Google Scholar | View at Publisher

Ezat, A. and A. El-Masry, 2008. The impact of corporate governance on the timeliness of corporate internet reporting by Egyptian listed companies. Managerial Finance, 34(12): 848-867.View at Google Scholar | View at Publisher

Gilling, D.M., 1977. Timeliness in corporate reporting: Some further comment. Accounting and Business Research, 8(29): 34-50. View at Google Scholar | View at Publisher

Haw, I.M. and B.T. Ro, 1990. Firm size, reporting lags and market reactions to earnings releases. Journal of Business Finance & Accounting, 17(4): 557-574.View at Google Scholar | View at Publisher

IASB, 2010. International financial reporting standards. 1st Edn.: Wiley-VCH.

Jensen, M.C. and W.H. Meckling, 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4): 305-360. View at Google Scholar | View at Publisher

Karim, W., K. Ahmed and A. Islam, 2006. The effect of regulation on timeliness of corporate financial reporting: Evidence from Bangladesh. Journal of Administration & Governance, 1(1): 15-35.View at Google Scholar

Khasharmeh, H.A. and K. Aljifri, 2010. The timeliness of annual reports in Bahrain and the United Arab Emirates: An empirical comparative study. International Journal of Business and Finance Research, 4(1): 51-71. View at Google Scholar

Owusu-Ansah, S., 2000. Timeliness of corporate financial reporting in emerging capital markets: Empirical evidence from the Zimbabwe stock exchange. Accounting and Business Research, 30(3): 241-254. View at Google Scholar | View at Publisher

Owusu-Ansah, S. and S. Leventis, 2006. Timeliness of corporate annual financial reporting in Greece. European Accounting Review, 15(2): 273-287. View at Google Scholar | View at Publisher

Pham, N.T., 2016. Factors affecting the timeliness of financial statements of companies listed on the Ho Chi Minh City stock exchange. Economic Development Journal, 27(10): 76-93.

Staubus, G.J., 2000. The decision-usefulness theory of accounting: A limited history. New York: Routledge Publishing, Inc.

Tan, D.D., 2013. Several factors affect the timeliness of financial reporting by listed companies in Vietnam. Banking Technology Magazine, 84(1): 47-52.

Trueman, B., 1990. Theories of earnings-announcement timing. Journal of Accounting and Economics, 13(3): 285-301.View at Google Scholar

Türel, A., 2010. Timeliness of financial reporting in emerging capital markets: Evidence from Turkey. Istanbul University Journal of the School of Business, 39(2): 227-240.View at Google Scholar

Vy, N.T.X. and N.V. Khuong, 2016. The impact of enterprise characteristics to the timeliness of disclosure of financial statements: Experimental research on Vietnam's stock market. Journal of Science and Technology, 19(4Q): 143-157.