DO QUALIFIED FOREIGN INSTITUTIONAL INVESTORS IMPROVE INFORMATION EFFICIENCY: A TEST OF STOCK PRICE SYNCHRONICITY IN CHINA?

1,2,3Massey University, Auckland, New Zealand, North Shore Mail Centre, Auckland, New Zealand

ABSTRACT

Stock price synchronicity at a country level has been the subject of many previous studies, but for most investors it is more relevant at a firm level. Working from the perspective of a foreign investor stock price synchronicity is analyzed at the firm-level in the hot Chinese stock market. The impact of foreign ownership, institutional ownership, the concentration of large shareholders, and audit quality are all considered as factors which impact on firm-specific information and thus moderate stock price. Using data of Chinese-listed firms in the Chinese A-shares capital market from 2004-2014 stock price synchronicity is measured. Empirical results suggest stocks invested by Qualified Foreign Institutional Investor (QFII) investors and institutional investors stocks have a significantly lower price synchronicity than stocks without institutional investment. This was found to increase as share concentration increased, until a relatively high concentration percentage was reached when synchronicity starts to fall again. Government ownership was shown to be a factor with high synchronicity but results for the use of a Big 4 Auditor was weaker.

© 2017 AESS Publications. All Rights Reserved.

Keywords:Stock price synchronicity, QFII Investors, China, Information efficiency, Institutional investors, Ownership.

JEL Classification:G14, G15, G18.

Received: 30September 2016/ Revised: 11January 2017/ Accepted: 20January 2017/ Published: 30January 2017

Contribution/Originality

This study contributes to the existing literature by analyzing the stock price synchronicity at firm level from the perspective of Qualified Foreign Institutional Investors in the Chinese stock markets. Empirical results suggest that stocks held by foreign Institutional Investors have a significant lower price synchronicity than socks without institutional investments.

1. INTRODUCTION

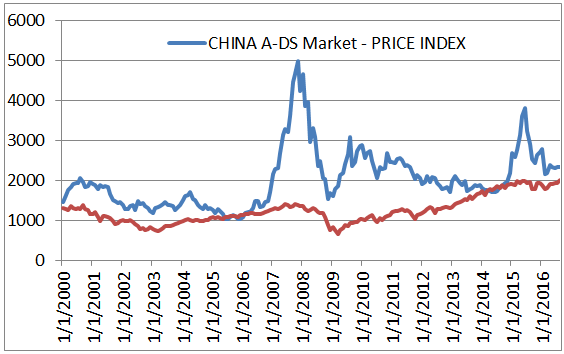

There can be little doubt that since China’s reform in the 1980s and 1990s, when many of the China’s State Owned Enterprises (SOEs) were privatized, China has again taken its place as a major world economy. One of its greatest successes has been its share markets, initially limited to foreign investors through its B-shares (traded in foreign currencies) and H-shares (Chinese stocks traded on the Hong Kong market). Then in November 2002 foreign investment was further relaxed when Chinese authorities introduced a special trading scheme, which allowed Qualified Foreign Institutional Investors (QFII’s) to trade directly in the A-shares (previously restricted to domestic investors). China’s share markets in Shanghai, Shenzhen and Hong Kong now have a market capitalization of $11trillion, second only to the USA’s market capitalization of $26trillion (Visual, 2016). However while its share market is large it can’t be described as a developed market, and while it has experienced rapid growth in the 1990s and 2000’s it has recently suffered from extreme reversals (Figure 1). Data in Figure 1 is for the entire market, and investors, particularly active investors don’t hold the entire market. Instead they buy individual stocks; they are therefore concerned about the performance and volatility of individual stocks. One way of looking at this is with stock price synchronicity, the relationship between the change in a single company’s stock price and the average market change.

Figure-1. China versus USA DataStream country equity indices

Source:The data used in Figure-1 is from DataStream database.

Roll (1988) was the first to find that the change in return for most stocks cannot be explained by the variation of market profitability and industry profitability. He thus suggested that the variation could not be explained because it reflected the firm-specific information in the prices.Morck et al. (2000) showed synchronicity is greater in poorer or emerging markets as stock prices in low GDP per capita markets tend to move together. Mature capital market shares on the other hand more adequately reflect a company’s data fundamentals, and companies have a lower stock price synchronicity.A number of researchers (Morck et al., 2000; Bushman et al., 2004; Jin and Myers, 2006) have suggested poor information flows, which are a characteristic of developing markets, could explain the high synchronicity. The original study of synchronicity in China wasGul et al. (2010) who used data from Chinese A-Shares, B-shares and H-shares over the period 1996-2003, showed synchronicity was a concave function of ownership by the largest shareholder and was related to government ownership. Additionally there was an inverse relationship with foreign ownership, auditor quality and earnings information. However this study is limited as foreign ownership was limited to B-shares and H-shares which were in foreign currencies on the Shanghai or Shenzhen Stock Exchanges or H-Shares which were registered in China, but listed and traded in Hong Kong. The QFIIs scheme provides foreign institutional investors direct access to China’s A-shares market, on a selective basis and using a quota system (Zou et al., 2016). Using QFIIs data and A-share data from 2003-2014 the limitations ofGul et al. (2010)are addressed, as not only is the data more current but by using QFIIs data for China’s A-shares large foreign institutional investors can be easily identified. These large institutions, can access firm-specific information more easily so that they can evaluate the value of stocks more accurately (Hirshleifer et al., 1994). Thus our results shed some new lights on the information transmission mechanism with the direct measurement for foreign ownerships involvements in Chinese listed firms.

The paper is conventionally structured; immediately following is a background to the Chinese share markets, the relevant literature is reviewed from which testable hypotheses are formulated. From these hypotheses empirical models are developed and tested in the methodology section. Results are then discussed and conclusions drawn. This study makes several contributions to the existing body of literature. First, it focuses on a significant developing market—China, where the country-level protection for investors is poor. The results help us to more clearly understand how firm-level protection for investors has an impact on disclosing firm-specific information to outside investors. Second, it is the first to consider the relationship between QFII and stock price synchronicity, with examination of how QFII ownership affects firm-specific information getting into the developing market. Third, the study is one of the few to analyze the influence of institutional ownership, largest shareholder ownership, and audit quality on firm-specific information contained in stock prices. Finally, the closest time period, from 2004 to 2014, is used to analyze stock price synchronicity. These contributions make the results are more convincing than prior studies.

1.1. Liberalization of the Chinese Share Markets

Since its liberalization in the early 1990s, there are three main categories of shares A-shares, B-shares and H-shares traded in the Chinese equity markets. A-shares and B-shares traded on the Shanghai and Shenzhen stock exchanges. B-shares were limited to foreign investors only prior to 2001 when a secondary market for domestic investors was allowed. A-shares were only available to domestic investors until 2003 when the market was further liberalized to fulfil the World Trade Organization (WTO) commitments, the Chinese Security Regulatory Commission (CSRC), the People’s Bank of China (PBC), and the State Administration of Foreign Exchange (SAFE) introduced a special trading scheme in November 2002, which allowed Qualified Foreign Institutional Investors to trade directly in the A-shares market. The QFIIs scheme is the first effort which allows foreign institutional investors to participate directly in Chinese capital markets, on a selective basis through a quota system. Other Chinese shares are H-shares incorporated in China that trade in Hong Kong. Shares in companies incorporated overseas are P-shares Hong Kong, S-shares Singapore, N-shares New York, L-shares London.

The CSRC and the SAFE are the regulatory bodies to overlook the investment activities conducted by the QFIIs. The CSRC is responsible for overseeing all transactions and conducting annual inspections on the QFIIs, it is also the authority body to grant the QFII status (the QFII license). The SAFE is responsible to supervise QFIIs activities associated to foreign exchange operations, i.e. the approval of QFIIs’ investment quotas, the issuance of foreign exchange certificates, supervision of account management and foreign exchange settlements. In addition to trade in Chinese A-shares, the QFIIs scheme also allows foreign institutional investors to participate in treasury securities, corporate bonds, mutual funds, warrants and other financial products listed by the CSRC.

The Qualified Foreign Institutional Investors are classified into the following main categories: Asset Management, Insurance, Securities, and Commercial Banks. There are also other institutions such as pension funds, charity foundations, endowment funds, and sovereign wealth funds. To qualify for a licensed QFII, the candidate must have stable financials, good credit history; meet the minimum asset scale set by the CSRC. For example, asset management and insurance institutions should have a minimum Asset under Management of USD 10 billion and a minimum of operating requirement of two years. They should also have no any sanction from the supervision system in the previous three years when lodge the application. For securities companies, the operating requirement is five years, and it increases to ten years for commercial banks. Over the years, the CSRC and the SAFE have gradually relaxed the QFII entry standard, for example, the Asset under Management from the asset management institutions was reduced from USD 10 billion to USD 5 billion. The shareholding ceiling was also revised which allows QFIIs to hold more than 10% of total A-shares outstanding for an individual firm. This rate was revised to 20% later, and again 30% in 2012.

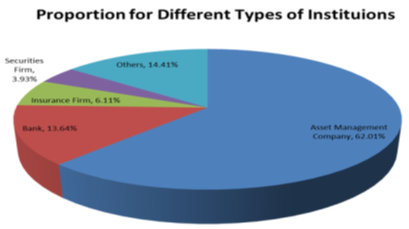

After receiving the license, a QFII can then apply the ‘quota’ (in USD). All QFIIs are required to apply its own custodian bank as the primary connection between the CSRC, the SAFE and the QFII. Both Chinese commercial banks and Chinese branch of foreign banks can serve as the custodian bank. The QFII scheme has been in operation for about 13 years, both the number of QFIIs and the ‘quota’ has expanded steadily. At the beginning of the scheme in 2003, the quota was USD 424 million, ten QFII licenses were granted to initiate the pilot programme. These include institutions such as UBS AG, Nomura Securities, Citigroup Global Market, Morgan Stanley, Goldman Sachs, The Hong Kong and Shanghai Banking Corporation, Deutsche Bank, ING Bank, JP Morgan, and Credit Suisse (HK). Many efforts have been implemented by the CSRC and the SAFE to accelerate the speed of QFII approval process. As of 28 September 2015, the quota increased to USD 79 billion and there were 277 licensed QFIIs. The CSRC exhibits a preference on asset management institutions when granting licenses, representing approximately 62 percent among all categories, and the second was puts towards the commercial banks at about 14 percent. Figure 2 illustrates the proportion of various types of institutions.

Figure-2. Proportion of Qualified Foreign Institutional Investors by category

Source:The data used in Figure-2 is from Zou et al. (2016).

2. LITERATURE REVIEW

Stock price synchronicity is the relationship between the change in a single company’s stock price and the average market change or moving together. The seminal work in this field is byRoll (1988) who was the first to find the change in return for most stocks cannot be explained by the variation of market profitability and industry profitability. He thus suggested that the variation could not be explained because it reflected the firm-specific information in the prices. The degree with which stocks move together depends on the relative amounts of firm-level and market-level information capitalized into stock prices (Roll, 1988).

Subsequent work byMorck et al. (2000) was able to show synchronicity or moving together was related to the per capita GDP. Using U.S. stock data from 1926 to 1995Morck et al. (2000) formed random monthly portfolios of 400 stocks and were able to show synchronicity fell as the U.S. economy developed. When they took an average week in 1995 for 37 countries, economies with high per capita GDP had lower synchronicity than economies lower per capita GDP had higher synchronicity. Using the R2 as a measure of synchronicity the countries with the highest R2’s were Poland 0.569, China 0.453 and Malaysia 0.429 compared to the U.S. 0.021, Ireland 0.058 and Canada0.062 (Morck et al., 2000). They conclude the result is not a result of structural characteristics like country or market size but suggest it may be related to private property rights and investor protections from insiders(Morck et al., 2000).

A company’s stock price can reflect market-level, industry-level, and firm-specific information (Piotroski and Barren, 2004). Accordingly, variation in the information at these three levels will cause changes in the stock price. Information from the market-level and industry-level will lead to a situation where all stock prices from the market, or specific industry, fluctuate in the same direction, causing them to all move up and down together. However, at the firm-level, specific information from a company will lead to an independent moderation of the stock price’s market or industry tendency and so stock price synchronicity will go down. Therefore, when the trading of a stock is based on a lot of firm-specific information, the stock price is supposed to contain more firm-specific information and lower its stock price synchronicity (Durnev et al., 2003).

Foreign investors are at a disadvantage to domestic investors and the benefit of risk reducing international diversification is irrefutable, leading most investors to having a bias towards domestic investment. Geographic and cultural distance along with, a lack of knowledge about foreign markets, legal and institutional constraints and currency risk impose additional transaction costs, and information costs on foreign investors.Shukla and Van Inwegen (1995) in a 1981 to 1993 study of U.K. and U.S. mutual funds found U.K. funds were at an information disadvantage. This resulted in poor performance, even after controlling for various characteristics like legal system, tax treatment, fund size, fund expenses and fund objectives. However a later study byKim and Yi (2015) of foreign and domestic institutional investors on the Korean Stock exchange, used stock price synchronicity to indicate the degree to which firm specific information is incorporated in prices, finding synchronicity decreases significantly with the intensity of trading by foreign investors and domestic institutional investors.

In response to the findings ofMorck et al. (2000) linking synchronicity to per capita GDP researchers have examined the synchronicity of individual stocks with the market. Most pertinent to this study is the earlier work on the Chinese market byGul et al. (2010) in which they show a concave function between synchronicity and ownership by the largest shareholders, maximized at around 50%. Of interest in China is the impact of government ownership which results in an increased synchronicity level. Factors which reduce synchronicity are foreign ownership and audit quality, proxy for this is engagement of one of the Big 4 auditors. Their final finding is the amount of earnings information in stock return is lower in stocks with high synchronicity. As the study byGul et al. (2010) was based on data from 1996 to 2003, their findings need to be re-validated given the changes which have occurred over the last 12 years. Firstly the introduction of QFII’s may have resulted in a significant change in market characteristics and secondly the stock market in China has increased in importance to global investors. Factors which have impacted on stock synchronicity and of interest in this study are foreign ownership, institutional investment, ownership concentration and audit quality.

3. METHODOLOGY

Gul et al. (2010) documented that in China, foreign ownership, institutional ownership, state ownership, ownership concentration, and auditing quality, in one way or another impact the stock price synchronicity. The introduction of the Qualified Foreign Institutional Investor provides us a natural experimental platform to examine the impact on the price synchronicity of foreign ownership. This proxy provides a direct measurement for foreign ownership and is considered to be better than the proxy employed inGul et al. (2010). Therefore we simply apply the market model to develop the measurement variables and model specifications. First, we estimated a market model (We only apply the market model for the following two reasons: 1. Results from other alternative models inGul et al. (2010) are qualitatively similar as the market model. 2. We use the holdings from QFIIs as a direct measurement for foreign ownership; therefore it is not necessary for us to use other alternative models for each fiscal year):

![]()

Lagged industry and market returns are also included in the model to alleviate concerns over potential non-synchronous trading biases that may arise from using daily returns as documented in Gul et al. (2010) (see also (Scholes and Williams, 1977; French et al., 1987)). Equation (1) effectively isolates total return variations attributed to domestic market wide and industry wide factors from those attributed to firm-specific factors. In estimating Equation 1, the daily return data should have at least 200 trading days in each fiscal year.

The stock price synchronicity is defined as the ratio of stock return variation to the total return variation, which is the adjusted R2 of the above market model. As in Gul et al. (2010) R2 is then transformed into the following format and SYNCHi is defined as the annual stock price synchronicity for firm i:

Based onGul et al. (2010) we propose the following hypotheses: H1 Stock price synchronicity is lower for firms with foreign ownership; H2 Stock price synchronicity is lower for firms with institutional ownership; H3 Stock price synchronicity increases with ownership concentration, and it is a concave function; H4 Stock price synchronicity is higher when the largest shareholder is government related, ceteris paribus; H5 Stock price synchronicity is lower for firms using Big 4 auditors. We therefore apply the following model specifications to test these hypotheses:

[Xi] is a vector of test variables representing foreign ownership, institutional ownership, ownership concentration, state ownership, and auditing quality, respectively. We also include a number of control variables, including firm leverage, MB, ROA, ROE, size, and volume1.

3.1. Data

All data are collected from RESSET database and cross checked with CSMAR for the period from 2004 to 2014. The following data are excluded; firms with less than 200 trading days in a year, financial firms, firms with any major asset restructuring during the sample period, and firms with incomplete dataset. After the selection process, our final sample comprises 16,826 firm-year observations.

Table- presents the industry distribution of our sample firms, based on RESSET industry classification. The sample comprises 63.81% firms from the manufacturing sector, followed by 5.89% from wholesale and retail trade, and 5.01% from real estate. Firms in the health and social work industries made up less than 0.1% of the total. Panel B reports the distribution of our sample firms by year. The number of firms increases over the eleven-year sample period, indicating the Chinese stock market grew steadily, except for the 2014 year.

Table-1.Sample industry distribution

Panel A: Industry distribution

A |

B |

C |

D |

E |

F |

G |

H |

I |

K |

L |

M |

N |

O |

Q |

R |

S |

Total |

|

No. |

365 |

358 |

10737 |

676 |

377 |

991 |

642 |

84 |

657 |

843 |

199 |

60 |

108 |

43 |

9 |

104 |

573 |

16826 |

% |

2.17 |

2.13 |

63.81 |

4.02 |

2.24 |

5.89 |

3.82 |

0.5 |

3.9 |

5.01 |

1.18 |

0.36 |

0.64 |

0.26 |

0.05 |

0.62 |

3.41 |

100 |

Panel B: Yearly distribution

2004 |

2005 |

2006 |

2007 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

Total |

|

No. |

1176 |

1231 |

951 |

1164 |

1316 |

1445 |

1540 |

1814 |

2120 |

2126 |

1943 |

16826 |

% |

6.99 |

7.32 |

5.65 |

6.92 |

7.82 |

8.59 |

9.15 |

10.78 |

12.6 |

12.64 |

11.55 |

100 |

Panel A presents the distribution of sample firms across industries based on RESSET industry classification, where A= Agriculture, B= Mining, C= Manufacturing, D= Electricity, gas, and water, E= Building and construction, F= Wholesale and retail trade, G= Transportation and logistics, H= Accommodation and catering industry, I= Information technology, K= Real estate, L = Leasing and Business Services, M= Scientific and technical services, N= Water, environment and public facilities management industry, O= Neighborhood services, repairs and other services, P= Education, Q= Health and social work, R= Culture, Sports and Entertainment, S= Complex. Panel B shows the distribution by year. See Table 2 for detailed description about the control variables.

For 49.2% of firms, the largest shareholder is government related. Although this number is considerably lower than the 66.5% reported inGul et al. (2010) the government still plays a significant role in controlling listed firms, despite the rapid growth of privatization in China over the last 15 years. There are about 4.8% firms issued both A and B-shares, 3.3% firms issued both A and H shares. On average, QFIIs hold about 0.2% of the total A-share capitalization. The overall institutional holdings (including QFIIs) account for 12.4% of total market capitalization. There are about 1.9% of firms using Big 4 firms as auditors, and 95.9% of firms were locally audited.

Table-2.Descriptive statistics

| Variables | Mean | Std. dev. | 5thPctl. | 25thPctl. | Median | 75thPctl. | 95thPctl. |

| R2 | 0.449 | 0.145 | 0.212 | 0.369 | 0.447 | 0.546 | 0.699 |

| SYNCH | -1.457 | 0.921 | -3.055 | -1.850 | -1.388 | -0.855 | -0.046 |

| BSHARE | 0.048 | 0.214 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| HSHARE | 0.033 | 0.179 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| QFIIHOLD | 0.002 | 0.007 | 0.000 | 0.000 | 0.000 | 0.000 | 0.011 |

| INSTHOLD | 0.124 | 0.135 | 0.000 | 0.022 | 0.081 | 0.181 | 0.395 |

| TOPHOLD | 0.380 | 0.160 | 0.150 | 0.274 | 0.362 | 0.500 | 0.661 |

| TOPGOV | 0.492 | 0.500 | 0.000 | 0.000 | 0.000 | 1.000 | 1.000 |

| BIG4 | 0.019 | 0.138 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| LOCAL | 0.959 | 0.199 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| VOL | 3.602 | 2.384 | 0.861 | 2.102 | 2.999 | 4.725 | 8.379 |

| SIZE | 22.005 | 1.010 | 20.551 | 21.445 | 21.886 | 22.554 | 23.877 |

| LEV | 0.470 | 0.207 | 0.114 | 0.351 | 0.483 | 0.627 | 0.793 |

| ROE | -0.637 | 205.954 | -14.443 | 3.459 | 6.741 | 11.530 | 21.690 |

| M/B | 4.510 | 34.229 | 1.080 | 1.957 | 2.719 | 4.432 | 9.589 |

| INDN | 6.105 | 1.486 | 3.638 | 4.913 | 6.917 | 7.365 | 7.449 |

| INDSIZE | 28.480 | 1.527 | 25.622 | 27.520 | 29.312 | 29.783 | 30.056 |

R2 andSYNCH are the R2 statistic and the stock price synchronicity estimated from Equations 1 and 2. BSHARE are firms that issued both A and B shares. HSHARE are firms that issued both A and H shares. QFIIHOLD are firms with Qualified Foreign Institutional Investors. INSTHOLD are firms with institutional holdings (both domestic and foreign). TOPHOLD is a measurement of ownership concentration, represented by the percentage of holdings from the largest shareholder. TOPGOV is a measurement for state ownership, represented by the percentage of government holdings from the largest shareholder. BIG4 is a measurement for auditing quality, represented by percentage of firms using Big4 as their auditors. LOCAL are firms that use local auditing firms. SIZE: Firm size is calculated as the log of total assets at the end of the fiscal year. INDNUM: Industry number is calculated as the nature log of the number of firms in the relevant industry. INDSIZE: Industry size measured as the log of year-end total assets of all sample firms in the industry to which a firm belongs. VOL: Trading volume computed as the total number of shares traded in a year, divided by the total number of shares outstanding at the end of the fiscal year. MB: Market-to-book ratio, computed as the total market value of equity, divided by the total net assets at the end of the fiscal year. LEV: Leverage computed as total liabilities divided by total assets. ROE: Return on equity is the profitability of the company calculated as operating profit divided by shareholders’ equity at the end of the fiscal year.

The correlations between the price synchronicity and the test variables in Equation 3 are presented in

Table-. There is a positive correlation between the price synchronicity and the ownership concentration, the state ownership, firms with H-shares on issue and having Big 4 as auditors. On the other hand, the price synchronicity is negatively correlated with firms with B-shares on issue, firms with both domestic and foreign institutional ownership. These results suggest that institutional ownerships, particularly foreign institutional ownership do actually contribute to the reduction of price synchronicity, thus, help to improve information efficiency. However, firms with higher ownership concentration, state ownership, using Big 4 as auditing firms, and firms issued H shares in Hong Kong, appear to have relative higher price synchronicity.

Table-3.Correlation matrix

| SYNCH | H SHARE | B SHARE |

QFII HOLD |

INST HOLD |

TOP HOLD |

TOP GOV |

BIG4 | |

| SYNCH | 1 | 0.013c | -0.026a | -0.029a | -0.088a | 0.001 | 0.093a | 0.008 |

| HSHARE | 1 | 0.021a | 0.075a | 0.023a | 0.064a | 0.090a | 0.545a | |

| BSHARE | 1 | -0.005 | 0.027a | -0.029a | 0.063a | 0.148a | ||

| QFIIHOLD | 1 | 0.131a | 0.045a | 0.024a | 0.067a | |||

| INSTHOLD | 1 | 0.002 | -0.032a | 0.012 | ||||

| TOPHOLD | 1 | 0.205a | 0.053a | |||||

| TOPGOV | 1 | 0.077a | ||||||

| BIG4 | 1 |

This table provides the correlation matrix between variables. BSHARE represents firms with both A and B shares on issue. HSHARE are firms that issued both A and H shares. QFIIHOLD are firms with Qualified Foreign Institutional Investors’ holdings. INSTHOLD are firms with institutional holdings (both domestic and foreign). TOPHOLD is a measurement of ownership concentration, represented by the percentage of holdings from the largest shareholder. TOPGOV is a measurement for state ownership, represented by the percentage of government holdings from the largest shareholder. BIG4 is a measurement for auditing quality, represented by percentage of firms using international Big4 accounting firms as their auditors. The superscripts a, b, and c represent the 1%, 5%, and 10% levels of significance, respectively.

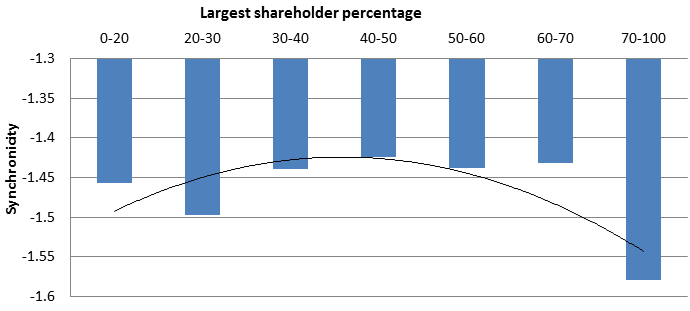

Gul et al. (2010) documented that due to the unique institutional environment in China where large controlling shareholders typically exercise nearly full control over major corporate decisions. Therefore, they predict that stock price synchronicity is a concave function of ownership concentration, measured by the percentage of shares held by the largest shareholder at the beginning of a fiscal year. We further investigate the relationship between ownership concentration and price synchronicity, following same approach as inGul et al. (2010) to compare the mean SYNCH on different levels of largest-shareholder concentration: 0-20%, 20-30%, 30-40%, 40-50%, 50-60%, and over 70%. Figure 3. depicts how price synchronicity varies with changes in ownership concentration level. We observe that the price synchronicity increases as the concentration level increases until the 40% concentration level. Then price synchronicity appears to decrease sharply and our result exhibits a stronger concave function compared toGul et al. (2010). On average, the largest shareholder holds more than 50% of total market capitalization for 25.03% (14.58%+7.45%+3.00%) of our sample firms, as opposed to 37.14% reported inGul et al. (2010). We believe this is mainly due to the rapid development and privatization of the Chinese equity market over the last 15 years.

Figure-3. Relationship between the percentage of shareholdings by the largest shareholder and stock price synchronicity

|

3.2. Multivariate Regression Analysis

Table 4 presents results from our multivariate regressions to examine the effects on stock price synchronicity of foreign ownership, institutional ownership, ownership concentration, state ownership, and audit quality. We employ eight models to test our hypotheses as proposed before, using various combinations of test variables. Numbers in parentheses are the t-values adjusted using standard errors corrected for clustering at the firm level. This will help to address potential serial correlation problem as documented inPetersen (2009).

Results from Model 1 in

Table- support our H1, suggesting that stock price synchronicity decreases for firms with foreign ownerships, as the coefficients on BSHARE and QFIIHOLD are both negative and statistically significant at the 1% level. The impact from the QFII holdings is much stronger than the BSHARE holdings, as the coefficient for QFII firms is -4.537 and the coefficient for BSHARE firms is -0.128. This indicates that the injection of foreign institutional ownerships to the Chinese A shares market contribute largely to the reduction of price synchronicity. It is also evident by the fact the coefficient of HSHARE becomes positive and statistically significant at the 1% level. This result suggests that firms with H shares on issue do actually experience relative higher price synchronicity for our sample period, 2004-2014.Gul et al. (2010) however, documented that both B and H share firms experience less price synchronicity for their sample period, 1996-2003. Our results have important policy implication and suggest that the introduction of Qualified Foreign Institutional Investors scheme indeed contribute to the information efficiency of the Chinese equity market. The CRSC and other regulatory bodies should consider further lifting those many barriers imposed on the Chinese financial market. This would help to enhance the liberalisation of Chinese financial market to the rest of the world.

Table-4.Multivariate regressions

| SYNCH | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 | Model 8 |

| Panel A: Test Variable | ||||||||

| HSHARE | 0.105 (2.96)a |

0.019 (0.40) |

||||||

| BSHARE | -0.128 (-4.57)a |

-0.148 (-4.95)a |

||||||

| Continue | ||||||||

| QFIIHOLD | -4.537 (-5.39)a |

-4.169 (-3.07)a |

||||||

| QFIICHANGE | -2.443 (-4.37)a |

-1.055 (-1.17) |

||||||

| INSTHOLD | -0.644 (-13.76)a |

-0.559 (-11.07)a |

||||||

| INSTCHANGE | -0.518 (-8.07)a |

-0.205 (-2.98)a |

||||||

| TOPHOLD2 | -0.522 (-2.62)a |

-0.522 (-4.4)a |

-0.574 (-2.89)a |

|||||

| TOPHOLD | 0.363 (2.15)b |

0.336 (4.7)a |

0.373 (2.22)b |

|||||

| TOPGOV | 0.083 (6.41)a |

0.076 (5.78)a |

0.077 (5.96)a |

|||||

| BIG4 | -0.080 (-1.36)c |

-0.092 (1.57)c |

||||||

| Panel B: Control variables | ||||||||

| LOCAL | -0.104 (-2.53)a |

-0.115 (-2.32)b |

||||||

| VOL | -0.027 (-9.09)a |

-0.027 (-8.95)a |

-0.033 (-11.00)a |

-0.028 (-9.41)a |

-0.028 (-9.00)a |

-0.028 (-9.21)a |

-0.026 (-8.74)a |

-0.036 (-11.57)a |

| SIZE | -0.110 (-14.35)a |

-0.106 (-14.44)a |

-0.096 (-13.14)a |

-0.110 (-15.13)a |

-0.112 (-14.99)a |

-0.116 (-15.59)a |

-0.113 (-14.99)a |

-0.101 (-12.35)a |

| LEV | -0.237 (-7.64)a |

-0.239 (-7.73)a |

-0.252 (-8.20)a |

-0.257 (-8.29)a |

-0.276 (-8.77)a |

-0.283 (-8.97)a |

-0.238 (-7.69)a |

-0.296 (9.43)a |

| ROE | -0.001 (-5.22)a |

-0.001 (-5.32)a |

-0.001 (-4.99)a |

-0.001 (-5.25)a |

-0.001 (-5.26)a |

-0.001 (-5.28)a |

-0.001 (-5.34)a |

-0.001 (-4.73)a |

| M/B | -0.002 (-9.07)a |

-0.002 (-9.17)a |

-0.002 (-8.76)a |

-0.002 (-8.94)a |

-0.002 (-9.08)a |

-0.002 (-9.10)a |

-0.002 (-9.19)a |

-0.002 (-8.44)a |

| INDNUM | 0.081 (1.15) |

0.082 (1.17) |

0.054 (0.76) |

0.084 (1.20) |

0.088 (1.25) |

0.096 (1.36) |

-0.081 (-1.15) |

-0.060 (0.85) |

| INDSIZE | 0.010 (0.25) |

0.010 (0.25) |

0.001 (0.02) |

0.010 (0.25) |

0.015 (0.35) |

0.012 (0.28) |

0.010 (0.24) |

0.008 (0.19) |

| Constant | 0.003 (0) |

-0.085 (0) |

0.201 (0.21) |

0.030 (0.03) |

-0.142 (0.15) |

0.006 (0.01) |

0.188 (0.19) |

0.154 (0.16) |

| Industry dummies | Included | Included | Included | Included | Included | Included | Included | Included |

| Year dummies | Included | Included | Included | Included | Included | Included | Included | Included |

| N | 16826 | 16826 | 16826 | 16826 | 16826 | 16826 | 16826 | 16826 |

| Adj. R2 | 0.309 | 0.308 | 0.315 | 0.310 | 0.309 | 0.309 | 0.307 | 0.319 |

This table presents multivariate regressions (Equation 3) to examine the effects on stock price synchronicity of foreign ownership, ownership concentration, institutional ownership, and audit quality. The dependent variable is SYNCH, is estimated using Equations 1 and 2. Panel A presents test statistics for all test variables: BSHARE is a dummy variable equals to 1 for firms with both A and B shares on issue. HSHARE is a dummy variable equals to 1 for firms with both A and H shares on issue. QFIIHOLD is the percentage of shareholdings by Qualified Foreign Institutional Investors. QFIICHANGE is the percentage change of shares held by QFIIs in a year. INSTHOLD is the percentage of shareholdings by institutional holdings (both domestic and foreign). TOPHOLD is a measurement of ownership concentration, represented by the percentage of holdings from the largest shareholder. INSTCHANGE is the percentage change of shareholdings by institutional investors in a year. TOPHOLD is a measurement of ownership concentration, represented by the percentage of holdings from the largest shareholder. TOPGOV is a dummy variable equals to 1 for firms with state ownership in their largest shareholder. BIG4 is a dummy variable equals to 1 for firms using international Big4 accounting firms as their auditors. We employ eight model specifications to test the five hypotheses as proposed before, using different combination of test variables. We also use a number of firm characteristic control variable for various model specifications Panel B contains results for all control variables as defined in . Numbers in parentheses are the t-values adjusted using standard errors corrected for clustering at the firm level. The superscripts a, b, and c represent the 1%, 5%, and 10% levels of significance, respectively.

We also introduce two new measures as alternatives for foreign ownership and institutional ownership, the percentage change of shares held by QFIIs in a year and the percentage change of shares held by institutional investors in a year. We then run Models 2, 3, and 4, to examine the impact of foreign ownership changes (denoted as QFIICHANGE), the impact of aggregate institutional holdings (denoted as INSTHOLD), and the impact of institutional ownership changes (denoted as INSTCHANGE). All three coefficients are negative and statistically significant at the 1% level, indicating that institutional ownerships (including foreign ownerships) significantly reduce the price synchronicity of their holding firms. This result supports our H2.

Models 5 and 6 examine the impact on price synchronicity of ownership concentration and state ownership. TOPHOLD is a measurement of ownership concentration, represented by the percentage of holdings from the largest shareholder. We also include the TOPHOLD2 as the price synchronicity is a concave function of ownership concentration, as observed in Figure 3..Gul et al. (2010) also argue that a better concentration measure would be the disparity between the largest shareholder’s position and those of other substantial investors, as the largest shareholder is more likely to become entrenched as the disparity increases. Therefore, we adopt a similar approach asGul et al. (2010) use the difference in percentage shareholding between the largest and the second- and third-largest shareholders, calculated as:

DIF and DIF2 are then applied to replace TOPHOLD and TOPHOLD2 in Model 6. We find similar results from Models 5 and 6. The coefficients for TOPHOLD in both models are positive and statistically significant at the 1% level, suggesting that firms with higher ownership concentrations have relative higher price synchronicity. This indicates that the ownership concentration is inefficient in providing information, which supports the H3. The coefficients for TOPHOLD2 in both models are negative and statistically significant at the 1% level, indicating that synchronicity is a concave function of ownership concentration, which is consistent withGul et al. (2010). The coefficients on TOPGOV are positive and statistically significant for both models, suggesting that the largest shareholder with state ownership provides less value-relevant information to the market than does the non-state related largest shareholder. Therefore, the state ownership is also inefficient in this regard, which in turn supports our H4.

Our H5 is support by results from Model 7, which examines the impact on price synchronicity of using BIG4 auditors. We find the coefficient for BIG4 is negative, and it is statistically significant at the 10% level. This suggests that BIG4 auditors are better to convey more reliable, relevant information to the market. But this phenomenal is weaker for our sample period as opposed to the sample period inGul et al. (2010). On the other hand, the coefficient on LOCAL is negative and statistically significant at the 1% level, indicating that local auditors are now more effective in providing high quality information to the market. This finding suggests the possible improvement of accounting quality for listed firms, as regulatory bodies have been gradually put strict policy towards reporting policy. The introduction of Qualified Foreign Institutional Investors may contribute to this phenomenal. We then perform a full regression analysis with all test variables in Model 8, results show that all coefficients remain with expected signs and significant levels.

We now focused on the control variables. The coefficients on VOL, SIZE, LEV, ROE, and M/B ratios are all negative and statistically significant at 1% level. The negative coefficient on VOL indicates that active trading activities do provide more information to the market. A negative SIZE coefficient suggests that small firms tend to mirror the market to a greater extent than large firms, and this result is inconsistent with Gul et al. (2010). A negative LEV coefficient indicates that firms with higher leverage tend to have lower price synchronicity. This may be due to the reason that higher levered firms are forced to disclose more information to the market. A negative M/B coefficient suggests that firms with greater growth potential tend to have more information embedded into their stock prices. We also find firms with greater ROE tend to have a lower price synchronicity. All other control variables are insignificant in all eight models.

According to Figure 3., synchronicity reaches its peak at around 40% ownership by the largest shareholder. We calculate the synchronicity-maximizing level of largest-shareholder ownership as inGul et al. (2010) using the coefficients for TOPHOLD and TOPHOLD2 to calculate the maximum level of largest shareholder ownership, and it is 32.50% (0.373/(2*0.574)). This result is in line with the result we observed in Figure 3., that the price synchronicity reaches its peak at around 30-40% ownership level and starts to drop sharply.

3.3. Robustness Checks

Gul et al. (2010) considered the potential self-selection bias that might arise from the fact that firms may select their own auditors. They addressed this issue using a two-stage regression and their result suggested that the inverse relation between synchronicity and Big 4 auditor choice is robust to potential endogeneity concerns. We found a relative weaker Big 4 effect in our study, therefore, the endogeneity concerns is not of great concern in this study. However, there was a major global financial crisis in 2008 which is during our sample period. We therefore perform the robustness check to investigate whether our results are sensitive to the 2008 global financial crisis. presents results for our robustness checks. We first perform the full regression model (Model 8 in

Table-) but excluding data from 2008, results are presented in column 2 in . The new regression results are similar to those reported in

Table-, except for the Big 4 coefficient is getting insignificant (at the 10% significant level in

Table-). This suggests that our results are unlikely to be driven by any exogenous shock caused by the 2008 financial crisis.

We also run another robustness check by excluding data for years 2006, 2007, and 2014, which are considered to be ‘GOOD’ periods in China. Results are presented in column 3 in . There are a few important observations needed to be addressed. The coefficients on QFIICHANGE and BIG4 become statistically significant; it is at the 1% level for the QFIICHANGE and at the 5% level for the BIG4. These results suggested that the impacts on price synchronicity of changes of foreign ownership and use of quality auditors are stronger during bear markets. This may suggest that investors are more sensitive to auditing quality during periods of economic turmoil.

4. CONCLUSION

Stock markets in China have come a long way since the first market liberalisation in the early 1990’s and the introduction of the Qualified Foreign Institutional Investors scheme has taken it further. Despite China being amongst the largest world equity markets it must still be approached with caution, particularly as country-level protections for investors is poor. Analysis of synchronicity provides a useful tool for understanding the workings of the Chinese stock market. Stock price synchronicity is shown to decline as the level of foreign investment increases in individual firms. Although this is not a new finding the use of QFII data provides a more reliable method for measuring the level foreign investment in individual firms. Testing of the use of a Big 4 auditor is still found to be significant (10% level) but this is weaker than in previous studies such asGul et al. (2010) which uses data predating the introduction of the QFII scheme. These results help us to more clearly understand how firm-level protection for investors has an impact on disclosing firm-specific information to outside investors. Despite over 20 years’ development there is still a long way to go for policy makers to ensure an informational efficiency equity market in China.

The main contribution of this study is it uses recent data from 2004 to 2014, and it is one of the few to analyse the influence of institutional ownership, largest shareholder ownership, and audit quality on firm-specific information contained in stock prices. These contributions make the results more convincing than prior studies, and they could be of interest to policy makers in other developing markets, with restrictions on foreign investors.

Table-5. Robustness checks

| Excluding 2008 Observations Excluding 2006,2007 and 2014 Observations | ||

| SYNCH | SYNCH | |

| Panel A: Test variables | ||

| HSHARE | 0.025 (0.51) |

-0.012 (0.22) |

| BSHARE | -0.145 (-4.51)a |

-0.165 (-4.96)a |

| QFIIHOLD | -4.426 (-3.00)a |

-3.288 (-1.86)c |

| QFIICHANGE | -1.224 (-1.27) |

-3.536 (-2.96)a |

| INSTHOLD | -0.524 (-9.93)a |

-0.571 (-9.93)a |

| INSTCHANGE | -0.227 (-3.12)a |

-0.223 (-2.93)a |

| TOPHOLD2 | -0.657 (-3.13)a |

-0.341 (-1.54) |

| TOPHOLD | 0.460 (2.58)a |

0.167 (0.89) |

| TOPGOV | 0.079 (5.79)a |

0.097 (6.66)a |

| BIG4 | -0.095 (-1.53) |

-0.125 (-1.89)b |

| LOCAL | -0.127 (-2.47)b |

-0.131 (-2.30)b |

| VOL | -0.037 (-11.27)a |

-0.046 (-13.13)a |

| SIZE | -0.113 (-12.96)a |

-0.081 (-8.89)a |

| LEV | -0.296 (-8.91)a |

-0.252 (-7.24)a |

| ROE | -0.001 (-4.82)a |

-0.001 (-3.65)a |

| MB | -0.002 (-8.28)a |

-0.002 (-6.19)a |

| INDNUM | -0.038 (-0.50) |

-0.013 (-0.16) |

| INDSIZE | 0.089 (1.92)c |

-0.039 (-0.8) |

| CONSTANT | -1.327 (-1.25) |

1.535 (1.38) |

| Industry dummies | Included | Included |

| Year dummies | Included | Included |

| N | 15510 | 12768 |

| Adj. R2 | 0.222 | 0.310 |

All variables are as defined earlier in . The dependent variable is SYNCH. Numbers in parentheses are the t-values that were adjusted using standard errors corrected for clustering at the firm level. The superscripts a, b, and c represent the 1%, 5%, and 10% levels of significance, respectively.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Bushman, R.M., J.D. Piotroski and A.J. Smith, 2004. What determines corporate transparency? Journal of Accounting Research, 42(2): 207-252.View at Google Scholar | View at Publisher

Durnev, A., R. Morck, B. Yeung and P. Zarowin, 2003. Does greater firm-specific return variation mean more or less informed stock pricing? Journal of Accounting Research, 41(5): 797-836.View at Google Scholar | View at Publisher

French, K.R., G.W. Schwert and R.F. Stambaugh, 1987. Expected stock returns and volatility. Journal of Financial Economics, 19(1): 3-29.View at Google Scholar | View at Publisher

Gul, F.A., J.-B. Kim and A.A. Qiu, 2010. Ownership concentration, foreign shareholding, audit quality, and stock price synchronicity: Evidence from China. Journal of Financial Economics, 95(3): 425-442.View at Google Scholar | View at Publisher

Hirshleifer, D., A. Subrahmanyam and S. Titman, 1994. Security analysis and trading patterns when some investors receive information before others. Journal of Finance, 49(5): 1665-1698.View at Google Scholar | View at Publisher

Jin, L. and S.C. Myers, 2006. R 2 around the world: New theory and new tests. Journal of Financial Economics, 79(2): 257-292.View at Google Scholar | View at Publisher

Kim, J.-B. and C.H. Yi, 2015. Foreign versus domestic institutional investors in emerging markets: Who contributes more to firm-specific information flow? China Journal of Accounting Research, 8(1): 1-23.View at Google Scholar | View at Publisher

Morck, R., B. Yeung and W. Yu, 2000. The information content of stock markets: Why do emerging markets have synchronous stock price movements? Journal of Financial Economics, 58(1–2): 215-260. View at Google Scholar | View at Publisher

Petersen, M.A., 2009. Estimating standard errors in finance panel data sets: Comparing approaches. Review of Financial Studies, 22(1): 435-480.View at Google Scholar | View at Publisher

Piotroski, J.D. and T.R. Barren, 2004. The influence of analysts, institutional investors, and insiders on the incorporation of market, industry, and firm-specific information into stock prices. Accounting Review, 79(4): 1119-1151.View at Google Scholar | View at Publisher

Roll, R., 1988. R². Journal of Finance, 43(3): 541-566.View at Publisher

Scholes, M. and J. Williams, 1977. Estimating betas from nonsynchronous data. Journal of Financial Economics, 5(3): 309-327.View at Google Scholar | View at Publisher

Shukla, R.K. and G.B. Van Inwegen, 1995. Do locals perform better than foreigners? An analysis of UK and US mutual fund managers. Journal of Economics and Business, 47(3): 241-254.View at Google Scholar | View at Publisher

Visual, C., 2016. All of the world’s stock exchanges by size. Retrieved from http://www.visualcapitalist.com/all-of-the-worlds-stock-exchanges-by-size/ [Accessed 30 August 2016].

Zou, L., T. Tang and X. Li, 2016. A tale of two styles: Do qualified foreign institutional investors have an edge over domestic funds managers in China? Paper Presented at the Asian Finance Association (AsianFA).

| Views and opinions expressed in this article are the views and opinions of the author(s), Asian Economic and Financial Reviewshall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |