USAGE OF DERIVATIVES IN EMERGING MARKETS: THE CASE OF BOSNIA AND HERZEGOVINA

1International Burch University Francuske Revolucije bb, 71000 Sarajevo, Bosnia, 2International Burch University Sarajevo, B&H

ABSTRACT

During the last decade, financial derivatives have gained increased attention; they were one of the leading causes of the latest financial crisis. Their primary purpose is to provide instruments for hedging risks linked with stock market movements. Most of the financial economists agree that derivatives markets if abused, may cause disturbances in the financial markets, while some claim that derivatives markets provide valuable instruments for hedging financial risks. When we consider the importance of derivative markets, our primary goal is to investigate the degree of development of derivatives market in B&H. When we’re talking about derivatives market in B&H, it does not exist as organized markets yet. As many derivatives are being offered to the firms, only within the banking sector, we concluded that the financial system in B&H is bank centered. It follows the Continental model in which banks are playing a leading role. The participation of banks in the case of B&H is over 80%. The financial derivate market is organized as over the counter market as it offers currency swaps and forwards, and interest rate forwards. It’s important to notice that almost all business operations are done in "euro." Because of the currency board regime, agency regulations on banks' net open position and a relatively small exposure to foreign currencies, except the euro, currency risk in B&H is small. However, risk management is important for every firm, so the primary focus of this paper will be how B&H nonfinancial companies manage the risks that they have regarding the use of financial derivatives.

© 2017 AESS Publications. All Rights Reserved.

Keywords: Financial derivatives, Financial system, Risk management, Emerging markets, Volatility.

JEL Classification: G21, G32.

Received: 13 October 2016/ Revised: 3 November 2016/ Accepted: 22 November 2016/ Published: 3 December 2016

Contribution/ Originality

This study is one of very few studies which have investigated usage of derivative financial instruments in emerging markets. This research provides a unique insight of how derivatives can both stimulate and protect present and future investors, while also providing foundations for future in-depth studies on this topic.

1. INTRODUCTION

Financial instruments whose value is based or derived from some underlying asset such as stocks, bonds, loans, interest rates, foreign exchange rates, commodities, mortgages and even weather disasters such as earthquakes or hurricanes are called derivatives (Halilbegovic and Elvisa, 2016).

In last decade, trading with derivative financial instruments has become one of the most efficient means to raise the rate of return and reduce the risk in portfolio management. Financial derivatives are a tool for functioning and development of the financial markets. They provide the quality and quantity of the supply and demand of capital, improve the business climate, and create opportunities for new jobs, and the largest contributing to the decline in unemployment. Trading with derivatives was rising daily, because of the risk management in trading securities of financial as well as non-financial firms, the massive expansion of the stock market, the standardization of financial instruments, and the intensive development of information and communication technologies.

The primary goal of derivatives is to reduce the risk for one side while on the other hand offers the potential for a high return (at increased risk) to another. The vast spectrum of possible underlying assets and payoff alternatives leads to a diverse range of derivatives contracts available to be traded in the market. B&H don't have a market for derivatives. Some types are offered on the market by banks but according to the developed countries, it is insignificant. In this paper, I will try to show the use of this financial derivative in the advanced economies, how emerging economies are using this types of financial instruments, and what are the reasons that B&H and other transition countries from the area are not using and don’t have the development market of financial derivatives.

2. LITERATURE REVIEW

2.1. The Theoretical Framework

Derivative financial instruments include securities whose values are derived from one or more underlying assets such as stocks, bonds, currencies, interest rates, etc. It includes contracts in which the parties agree to transfer underlying assets on or before the determined date in the future, according to planned price. Financial derivatives are used as an instrument for risk management, more precisely to hedge business risks which include interest rate risk, commodity risk, security price risk, currency risk, interest rate risk and credit risk (Acharya et al., 2009).

Also, derivatives be used for speculative purposes. The risk in a derivative contract can be traded by buying the contract itself (e.g. with options) as well as by creating a new contract which represents risk characteristics that match, in a countervailing manner, those of the existing contract owned. According to the way they are traded in the markets, there are two groups of derivatives. Those are exchange-traded derivatives (that is financial instruments traded via specialized derivatives stock exchange or other exchanges), and over-the-counter markets or derivatives (privately negotiated between two parties: a bank and a non-financial firm) (Rovčanin and Aida, 2014).

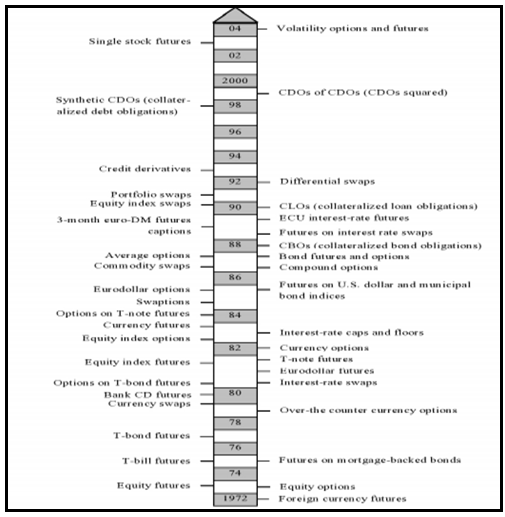

The figure 1 represents the timeline of the introduction of different types of financial derivatives to the capital markets.

Figure-1. The evolutionary path of derivative financial instruments

Source: Crouhy et al. (2006)

Each derivative provides a varied level of liquidity and entails certain costs and benefits. The first type of “modern” derivative currency futures was introduced to the US market in 1972. Later other derivatives came into the use, such as options and stock futures (1973), mortgage bond futures (1975), OTC currency options (1979), swaptions (1985), etc. All the way until credit derivatives (1993), single stock futures (2003), and volatility options and futures (2004), (Miloš, 2007).

2.2. Derivatives Market in Developed Economies

Derivatives are defined as contracts whose value is derived from another underlying instrument. In this case, the principal never changes owners. It means that the trade of essential tool is being arranged such as the revised of cash flows or compensation of credit risk, the price difference, etc. The organization of derivatives can be exchange-traded derivatives or over-the-counter derivatives (OTC). The notion amounts outstanding in the (OTC). The usage of derivatives rapidly increases in advanced economies as well as emerging markets. It means in both OTC contracts and exchange-traded contracts; through underlying classes, including interest-rate, currency, equity, and the most recent addition, credit (Sundaram, 2013). Financial markets are very volatile. That includes that people who are trading in foreign exchange, oil, and other commodities are exposed to significant risk because all these elements are linked to such fluctuating prices. Modern finance provides a method called hedging to reduce the risk. Derivatives are used for hedging.

There are several reasons to use derivatives:

1. Helping in transferring risks from risk adverse people to risk oriented people.

2. Assisting in the discovery of future and current prices.

3. Catalyzing entrepreneurial activity.

4. Because of participation of risk adverse people in greater numbers, they increase the volume traded in markets

5. Increasing savings and investment in the long run.

Derivatives are used for hedging; some people use it to speculate as well. In that term, there are some disadvantages of derivatives:

1. Derivatives raise volatility: Each market participants can be part of the derivative market with small initial capital because of leveraging derivatives provide. It leads to speculation and increases volatility in the markets.

2. A Higher number of bankruptcies: Due to leveraged nature of derivatives, participants look into positions which don't actually match their financial capabilities and eventually lead to bankruptcies.

3. Increased need of regulation: A large number of members take positions in derivatives and take speculative positions. It is required to stop activities like that and to prevent members from getting bankrupt and to halt the chain of defaults. In that case, it is a need to note that various economist considers derivatives are the main reason for the global financial crisis in 2008. Before the crisis, the benefits of financial derivatives were not only felt in industrialized countries, specially developed one. If governments which previously had problems issuing debt could borrow more cheaply. And it is called credit default swaps. Also, many economists consider that derivatives as financial instruments were and is not a problem but the way that investors used them to gain more profit taking more risky investments. Rousseau and Sylla (2003) however, how derivatives are important we can conclude from the report „The Financial Development Report 2015“ by World Economic Forum that as results of the report conclude that the top 10 economies in overall Index ranking:

“The derivatives market is, in a word, gigantic, often estimated at more than $1.2 quadrillion. Some market analysts estimate the derivatives market at more than 10 times the size of the total world gross domestic product, or GDP. The reason the derivatives market is so large is because there are numerous derivatives available on virtually every possible type of investment asset, including equities, commodities, bonds and foreign currency exchange. However, some analysts challenge estimates of the size of the derivatives market as vastly overstated.”

Table-1. Top 10 economies in overall Index ranking

| Country/Economy | Rank (2014-2015) |

| Switzerland | 1 |

| Singapore | 2 |

| United States | 3 |

| Finland | 4 |

| Germany | 5 |

| Japan | 6 |

| Hong Kong SAR | 7 |

| Netherlands | 8 |

| United Kingdom | 9 |

| Sweden | 10 |

Source: The Financial Development Report 2015

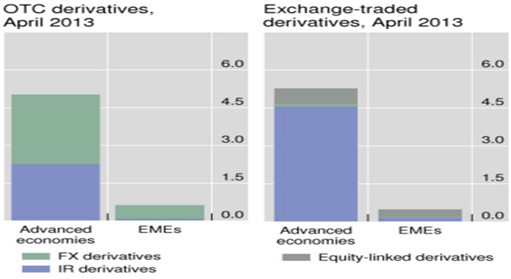

Figure-2. Derivatives turnover in advanced economies

Source: Bank for International Settlements

Table-2. OTC market FX turnover in advanced economies

| 2007 | 2010 | 2013 | Growth 2010-2013 | Global share | |

| Advanced economies | 5,984.4 | 7,173.4 | 9,599.2 | 33.8 | 179.6 |

| US dollar | 2,845.4 | 3,370.0 | 4,652.2 | 38.0 | 87.0 |

| Euro | 1,231.2 | 1,550.8 | 1,785.7 | 15.1 | 33.4 |

| Japanese yen | 573,4 | 754,2 | 1,231.2 | 63.3 | 23.0 |

Source: Bank for International Settlement

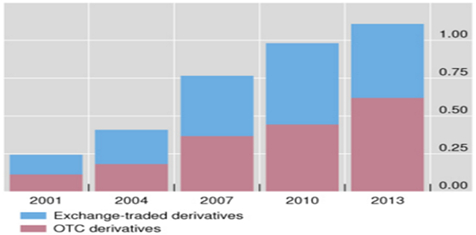

2.3. Derivatives Market in Emerging Economies

Generally, in emerging markets derivatives markets are small. This market is forming like an OTC market and globally compared to previous years its increasing.

In contrast, most represented derivatives in emerging countries in the field of FX contracts where the most significant activities in currencies such as Chinese renminbi, Mexican peso, Turkish lira and Russian rouble. This emphasizes the higher level of importance and the exposure to the foreign exchange rate in developing countries than developed countries. Although this market is growing quickly in emerging economies, the highlights of derivatives market in developing countries can be found in following:

Figure-3. Derivatives turnover in emerging markets

Source: Bank for International Settlements

1. Emerging market countries can benefit from derivative products because in many emerging market countries, the growth of institutional investors, including pension funds and insurance companies, has outstripped issuance of domestic assets creating a supply/demand imbalance. Derivatives can help fill this gap.

2. Emerging market countries face several challenges in developing derivative markets. These include relatively underdeveloped markets for the underlying assets; lack of adequate legal, regulatory, and market infrastructure; and restrictions on the use of derivatives by local and foreign entities.

3. In many emerging market countries, legal codes and accounting rules are silent on all or particular types of derivatives, fail to identify the regulatory jurisdiction over derivatives, or make derivative contracts unenforceable.

4. Regulators in emerging market countries should develop appropriate policies on the operational and credit risks of trading derivatives. Regulators often fear that derivatives will increase, rather than reduce, risk and, as a result, they adopt a conservative stance.

5. It is unclear whether exchange-traded or OTC derivatives are preferable for emerging market countries.

6. Exchange-traded derivatives reduce counterparty risk and make price and information transparency more accessible to a wider range of market participants, but they require cash market liquidity to develop. On the other hand, OTC derivatives are not so dependent on money market liquidity, but entail more counterparty risk and are less accessible.

7. In some emerging markets, capital account restrictions have shifted derivatives trading by foreign investors to offshore markets. This has several implications. It reduces the ability to monitor the transactions and limits many smaller investors, such as small- and medium-sized companies, from hedging their risks, due to higher transaction costs and limited market access.

Emerging economies have become important participants in international financial flows, leading to greater demand for their products as well as for their currencies, which affects the further development of derivatives markets in these countries where they generate a high daily turnover of trading, especially on the OTC market. However, although the market is steadily increasing about developed countries that percentage is still small, which means that further development is still required (Spasojević, 2011).

3. METHODOLOGY

Since there is a growing need among companies that operate in very turbulent business environments, it's important to consider the uses of derivative financial instruments when hedging different types of financial risks.

3.1. Research Objectives

In emerging markets, such as B&H, financial derivatives are entirely new financial tools and many companies don't have adequate knowledge on how to use them to manage their financial risk exposure. So, there is a need to determine the scope of the use of derivatives by companies in B&H for specific purposes of financial risk management. The aim of this paper is to explore if B&H companies properly hedge their financial risks. The primary objective is to provide recommendations for the improvements of the B&H risk management practices to ensure more efficient and effective hedging of the financial risks by using derivatives available on B&H capital markets through the financial institutions.

3.2. Research Hypothesis

Companies in B&H do not use advantages of derivatives usage in the financial risk management to the full extent.

3.3. Research Design

This research will be conducted on the data provided by the Foreign Trade Chamber of B&H, financial statements of the chosen companies, the Banking Agency of the Federation of B&H, the Banking Agency of Republika Srpska, B&H banks, and other government and non-government organizations.

4. ANALYSIS & DISCUSSION

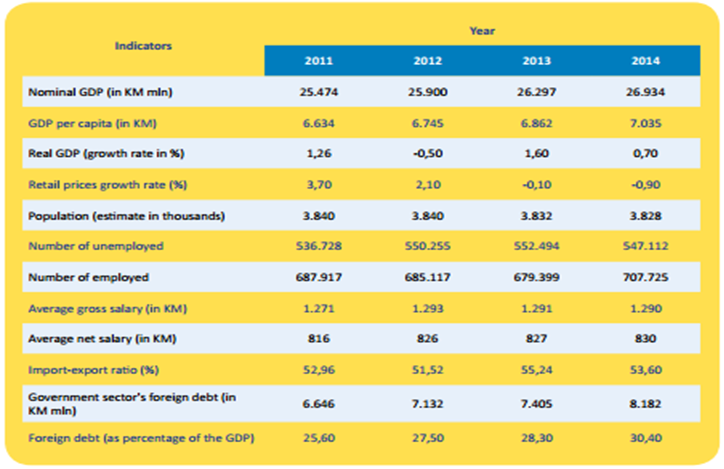

Monetary policy in Bosnia and Herzegovina is based on the principles of currency board where Convertible Mark (KM) is permanently tied to the euro at a ratio of 1 euro = 1.955830 KM. The currency board is applied in a rigid form, which means that the central bank uses only management functionality required reserves. From the table below we can see that GDP is increasing from year to year.

Figure-4. Macroeconomic indicators in B&H in 2011. – 2014

Source: Agency for insurance in B&H – annual report

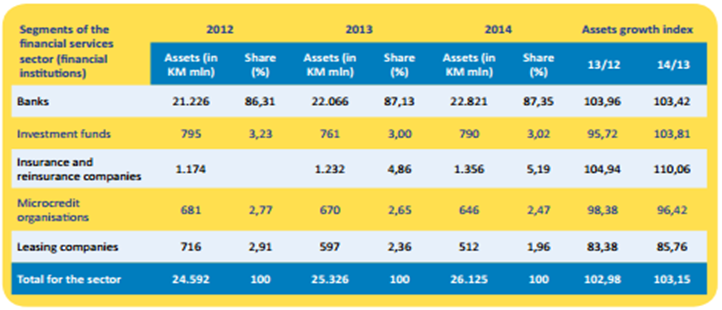

If we consider the structure of B&H financial system, it is important to notice that the country has a bank-centric financial system which follows the continental model and includes the participation of banks about 80%. Continental model assumes the model of universal banks - financial supermarkets that offer broadcasting services and sales of securities, financing, and financial management.

Figure-5. Structure of B&H financial services sector in 2012, 2013 and 2014

Source: Agency for insurance in B&H – annual report

Analyzing this structure, we can conclude that the financial system is not sufficiently developed nor sufficiently diversified. B&H has a capital market, with the two exchanges (Sarajevo Stock Exchange - SASE and Banja Luka - BLSE), but there is no developed money market.

When it comes to the impact of financial markets on the efficiency of investment in the economy of the country, it is necessary to point out that the dominant source of financing companies still represent commercial bank loans, and that alternative financing instruments, such as securities, have a negligible role. The law that regulates the derivative markets, in Federation, the Law on the Securities Market only defines derivatives and financial derivatives emphasizing that this market is controlled only as a mandatory trading on exchanges that in B&H still does not exist but only in the form of OTC market where banks offer their customers. For now, only three types of derivatives: currency forwards, currency swaps and interest rate swaps.

It is important to note that not all banks offer all three forms of derivatives, but the proposal is created about the volume and the size of the banks themselves. Also because of fixed exchange rate, companies are not interested in the use of financial derivatives, but when it comes to mitigating the price risks, especially in case of exporters, then the derivative must be taken into account.

To evaluate the demand for financial derivatives market of Bosnia and Herzegovina, Kozarevic and Jukan (2014) did research in the banking sector in B&H regarding the derivative that are offered and do the companies in B&H use this type of financial instrument. The sample included 29 commercial banks, of which 19 in FB&H and 10 in RS noting that ten banks in B&H (FB&H 6 and 4 in RS) offer derivative products to its customers.

The biggest interest amongst the bank clients is for currency forwards. The research shows a low supply of derivatives (34.48%), but also a weak demand because the results indicate that bank which is the largest provider of derivatives in the financial market of Bosnia and Herzegovina, concluded only ten contracts related to the derivative of the average value of around 750.000,00 KM or EUR 383,600.00. It is important to notice that the dominant users of derivatives are non-financial firms involved in production and distribution of oil and oil derivatives, furniture production companies, trading companies (especially trading businesses that import from China), gas trading and supplying companies, and IT companies. Interest rate swap (IRS) is the most used derivatives by the businesses in B&H. It means the exchange of one interest rate for the second stream without simultaneous exchange of principal.

Coupon Swap (plain vanilla) is a substitute payment under fixed interest rate for payments under variable interest rates and vice versa. It is characteristic that in these derivatives exchange only interest flows while equity is used to calculate payments based on interest rates, exchange investment flows done in predetermined periods during the swap, and average variable interest rates are EURIBOR and LIBOR with maturities of three, for six months and one year. Businesses that commonly used interest rate swaps are companies that are already in debt and have loans with variable interest rates. At the same time, companies are aware of the risk of the possibility of rising interest rates and that such a way of borrowing funds become too expensive. Businesses can protect themselves from rising interest rates, so as to replace its payments under floating rate payments at a fixed interest rate, and thus protect their businesses from adverse movements in interest rates.

For example, a company borrows 1 million for four years at a variable interest rate. Variable interest rate is three-month EURIBOR and fixed of 1.00%.

The Company believes that it will be a rise in interest rates and wants to protect itself from the risk and fixed costs - has a two-year interest rate swap. The Bank provides a quotation for a fixed interest rate for two years from 2:45%.

The company pays the loan - 3m EURIBOR + 1.00%

The company receives in interest swap - 3m EURIBOR

The company pays the interest rate swap - 2:45%

Net cost - 3:45%

This transaction is very simple and can help companies to protect themselves from risk exposure, but the companies in B&H are still not aware of all benefits that derivatives offer. Also, policymakers need to create the financial conditions for the development of derivatives and their especially regarding education, so participants in financial market don’t consider derivatives something that is complicated or the activity as useless speculation.

FX market is hazardous, and this segment of the market requires a high degree of caution, taking the company's experience, investment objectives, investment conditions, and considering that the B&H economy is small and mostly import-oriented, be. Companies are not important participants in international trade so that the volume of their transactions is significantly small compared to the large corporations that use derivatives for the reduction of risk. Bosnia and Herzegovina are not the only countries with the lack of derivatives market.

The same situation is in the neighborhood Serbia where there is no derivatives market. The law does not prohibit the development of this instruments and derivatives market, but the current structure does not have the infrastructure for the development of derivatives market. That means that transition countries still have a long path in including their financial systems in the world financial system.

5. CONCLUSIONS AND RECOMMENDATIONS FOR FUTURE STUDIES

Derivatives are an important financial tool of modern markets. To derivatives were able to exist in the financial market is necessary to secure financial infrastructure and a stable financial system. Derivatives are instruments that are widely used around the world. In addition to the essential functions of hedging, derivatives are used and for speculative purposes with the goal of quick profits.

It can be concluded that primary rationales for a small use of derivative instruments are due to lack of information about procedures of derivatives use and lack of knowledge about potential benefits of these devices in the domain of risk management. This applies not only to company employees but to bank employees too. Also, the major limiting factor of larger derivatives usage can be a relatively small number of business operations conducted by B&H companies in the global market as well as an absence of significant movements on B&H currency market due to currency board arrangement of the Central Bank of B&H (i.e. fixed course BAM against EUR and, consequently, a relatively low level of currency risk which the companies are exposed to, excluding BAM/USD).8 Amongst the risk factors hedged by the companies through their use of financial derivatives are cash flow volatility, revenue volatility, and protection of balance sheet positions.

B&H companies are more likely to decide not to use derivatives due to lack of knowledge and due to higher costs of maintaining derivatives portfolio, rather than the expenses related to financial risks. Nevertheless, the offer of derivative products in B&H is respectable with perspective to include additional products such as interest rate swaps, in contrast to the derivative offer in Croatia. Besides that, some the companies expect to use current and new financial derivatives instruments in their future business operations. But for now, if they want to improve their financial risk management practices, due to higher costs (resulted mainly from the banks’ provisions and their targeted profit rates) and despite their positive experience, B&H companies should, unfortunately, rather use exchange traded derivatives of more developed countries markets than derivatives on domestic OTC market.

As we summarized hypothesis can be confirmed. Further research suggests a need for more in-depth analysis of derivatives usage by nonfinancial firms in other countries of the region (e.g. Serbia, Montenegro, Macedonia, possibly Albania). Also, we recommend the research which would include a simulation of a local derivative exchange-traded market establishment. Such simulation would help demonstrate possible benefits and costs, probable regulation, connections and support from other similar markets (or their segments), etc.

In the future, the hope is that the banks do more especially in the field of education of its employees in this area and that the company will offer new types of derivative securities as banks in B&H are very liquid and have the ability to provide these types of investments and their development, but it is necessary is to create a financial architecture that will be the basis for further development.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Acharya, V., M. Brenner, R. Engle, A. Lynch and M. Richardson, 2009. Derivatives – the ultimate financial innovation. Restoring Financial Stability: How to Repair a Failed System, 233: 241.

Crouhy, M., D. Galai and R. Mark, 2006. The essentials of risk management. New York: McGraw-Hill.

Halilbegovic, S. and B. Elvisa, 2016. Limitations and inconsistencies of standalone usage of stochastics indicator in stock trading.

Kozarevic, E. and M.K. Jukan, 2014. Derivatives market development in Bosnia and Herzegovina: Present or future? International Journal of Management Cases, 13(3): 637-646.

Miloš, S.D., 2007. The derivatives as financial risk management instruments: The case of Croatian and Slovenian non-financial companies. Financial Theory and Practice, 31(4): 395-420.

Rousseau, P.L. and R. Sylla, 2003. Financial systems, economic growth, and globalization. Globalization in Historical Perspective. University of Chicago Press: 373-416.

Rovčanin, A. and H. Aida, 2014. The use of financial derivatives in risk management purposes of non-financial firms in Bosnia and Herzegovina1. Contemporary Trends and Prospects of Economic Recovery: 65.

Spasojević, J., 2011. Uloga kreditnih derivata u tekućoj finansijskoj krizi. Bankarstvo, 40(11-12): 92-111.

Sundaram, R.K., 2013. Derivatives in financial market development. International Growth.

Web

http://financenmoney.in/advantages-and-disadvantages-of-derivatives/ http://www.economist.com/blogs/freeexchange/2009/derivatives_and_development

http://www.cbbh.gov.ba

http://www.sase.ba

http://www.secrs.gov.ba

http://www.komvp.gov.ba

| Views and opinions expressed in this article are the views and opinions of the author(s), Asian Economic and Financial Review shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |