GROWING THE GROWTH OF THE GHANAIAN ECONOMY: IS THE FUNCTION OF THE COUNTRY’S FINANCIAL DEVELOPMENT OF ANY SIGNIFICANCE?

1,2Faculty of Management Sciences, Department of Accounting Usmanu Danfodiyo University, Sokoto, Nigeria

ABSTRACT

This study investigates the relationship between economic growth and financial development in Ghana, the study incorporates the variables of government expenditure, population and trade openness among others. The time span of the study is from 1970 to 2012. To ensure robust results, the ARDL bounds testing approach to cointegration was applied in analyzing the dynamic relationship between the variables. The findings of the study in the long-run, established that, financial development has a strong positive impact to the Ghanaian GDP and contrary was found to be the case in the short-run. In addition to that, population was discovered to have a negative impact on the long-run growth of the country’s GDP. The aim of this study is to assess the directions of how to grow the growth of the Ghanaian economy. Surprisingly, the study discovered that despite the negative contributions of the huge government expenditure which defied the Keynesian hypothesis and the Wagner’s law of stimulating economic growth due largely to other exogenous factors not included in this study, yet, the study suggested the need for the Ghanaian policy makers to place all effort in eliminating all forms of financial repression. In addition to that, there is the need for the establishment of all measures that will help in attracting foreign direct investment in to the country. This can be achieved through sound political stability, provision of basic infrastructural facilities, better supervision and prudential regulations of the country’s financial system and the encouragement of entrepreneurial growth, innovation and creativities within the local economy. Finally corruption and embezzlement should as much as possible be tamed if realistic results of growing the growth of the Ghanaian economy is to be attained.

© 2017 AESS Publications. All Rights Reserved.

Keywords:Rafindadi, Economic growth, Ghanaian economy, Africa, Entrepreneurship, Ghana.

ARTICLE HISTORY: Received:9 September 2016 Revised:1 November 2016Accepted:7 November 2016Published:14 November 2016

Contribution/ Originality:: This study contributes in the existing literature by investigating the positions of the long-run impacts of the dynamics of financial development on economic growth in Ghana. This study is one of very few studies which have investigated how to grow the growth of the Ghanaian economy considering the key economic shocks the country has suffered from in recent years. The paper's primary contribution is the discovery of how the huge government expenditure which defied the Keynesian hypothesis and the Wagner’s law of stimulating economic growth to have a negative impacts to the country’s GDP.

1. INTRODUCTION

Ghana and the rest of the Sub-Saharan African continents has for indiscernible decades been in contentious economic growth problem. To support the direction of this argument, Rafindadi and Yusof (2015) established that the concept of economic growth within the sub-Saharan continents of Africa has been quite epileptic, unsustainable and even where it exist, it is marred by incessant macroeconomic instability and financial crisis. Supporting this assertion was the findings of Fowowe (2008) in his leading studies, the author established that:

“The economic performances of Sub-Saharan African (SSA) countries have attracted considerable attention in recent years with superlative terms such as ‘tragedy’, ‘mediocre’, and ‘dismal’ used to describe the low rates of economic growth experienced in these countries from the 1980’s to date. SSA has been the only region in the developing world to ‘stagnate’, and growth rates have been by and large, poor. The average GDP per capita growth rate from 1961 to 2000 was 0.45% for SSA while it was 1.6% for Latin America and the Caribbean (LAC), 2.3% for South Asia (SA), and 4.9% for East Asia and the Pacific (EAP)”.

The menace of this situation has come to stay in most Sub-Saharan Africa making it an aid dumping avenue by satiated developed world. This menace continue to leave Africa and its continents in to beggar and defendant nations thereby, leading to a direct or indirect backwardness in productivity, technology, educational development, infrastructural facilities, poor private sector and entrepreneurial development. These bottlenecks continued to linger amidst a high rising population that inevitably breeds spiraling poverty levels among the continents. In addition to this development, high level of financial mismanagement and less developed financial system are among other factors that combine to impede on the road map of continental African growth. Similar in line with these arguments are the assertions established by Stiglitz (1998). The author pointed out that less developed financial system spills adverse effects to the entire of a nation’s economic system and makes the economy crisis prone. Stiglitz (1998) continue to point out that the financial development of any nation is the brain and master plan of its economy.

Waiting for aid to rejuvenate economic growth, directly or indirectly is the greatest economic mistake and indeed a procrastination of the growth prospects and an escalation of the economic growth deliria to infinity. To support this view, Ndambiri (2012) pointed out that government expenditure, nominal discount rate and foreign aid significantly cause negative economic growth. Similarly, Elbadawi (1999) establish in his empirical study of 62 countries that aid inflows can influence the real exchange rate to appreciate. In a more recent study, Rafindadi (2011) argued that the huge inflows of aid into Ghana which paved the way to the 1983 economic reform of the country was marred by some Dutch disease. Rafindadi (2011) continued to argue that, instead of aid to cause real appreciation of the Cedi in Ghana, however, it massively depreciated the currency thereby, leading to a high increase in the cost of doing business. In a more recent development and while counteracting the assertions made by Fowowe (2008) is the submission of the World Bank (2009) which hinted that, although African financial system is confronted with continuums of challenges, but yet in recent times it has been recording accelerating growth over the past years. This shows that, the indicators of financial development have steadily increased and the real private sector which has been growing at an accelerating rate in the past decades is now gaining momentum. This development also spells that Africa’s GDP can grow with, or without aids; similarly, this is a clearer indication that financial repression, financial mismanagement in Sub-Saharan Africa are sufficient candidates that could dwarf the competitive existence of entrepreneurial prospects in a country (Rafindadi and Yusof, 2014b).

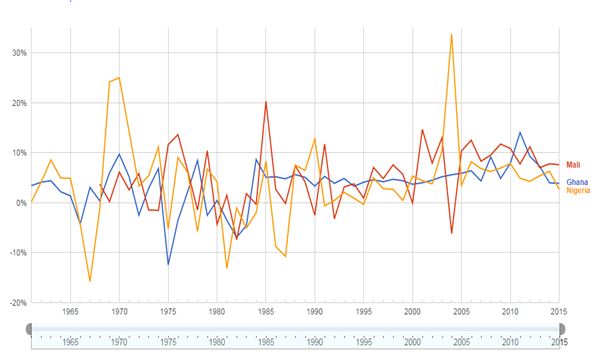

Considering the notorious and negative effects of aids in Ghana as reported by Rafindadi (2011) the question now is could the old theoretical supposition of King and Levine (1993a;1993b) work for the country? In their submission, King and Levine (1993a;1993b) discovered the existence of a statistically significant linkage between financial development and economic growth. The authors established that, the intermediationary role of financial institutions and markets in a country could provide the financial wherewithal to a profitable entrepreneurial pursuit, risk diversification, and the facilitation of efficient resource mobilization. These circumstances in turn will enhance the provision of a well-developed financial system which can help in improving not only the quality of capital formation and the efficiency of resource allocation but also facilitate in the promotion of a significant and sustainable long-run economic growth. How possible is this development in Ghana, is now the main focus of this study. Figure 1 shows the GDP growth rate in Ghana from 1965-2015

Source: World Bank 2013

From the introduction above, the rest of the paper is organized as follows: Section 2 provides a survey of both theoretical and empirical review, linking financial development and economic growth while the subsequent section provides the methodology which is in section 3 in that section, the study introduces the data, and the model specification and estimation procedures. Section 4 is the results and discussion. Finally, in Section 5 the study present the conclusion and policy guide towards growing the growth of the Ghanaian economy.

2. THEORETICAL AND EMPIRICAL REVIEW

Several pioneering studies exist decades ago on the burgeoning literature regarding the causal link between financial development and economic growth. Early researchers like Bagehot (1873); Schumpeter (1911) and emphatically agreed that the financial sector is the cardinal pillar for motivating economic growth on condition that it is free from vices that could be fraught to its effective functioning. These pioneering authors continued to argue that an effective and efficient financial system should have the voluntary wherewithal of mobilizing savings, allocating resource, pooling of risk, inducing liquidity, and reducing heavy transaction costs for them to function effectively and attain the required target. Similar to the assertions put forward by pioneering researchers, like Goldsmith (1969); Hicks (1969); Mckinnon (1973); King and Levine (1993b); Khan (2000); Pagano and Volpin (2001); Christopoulos and Tsionas (2004); Shan (2005); Khan et al. (2005); Jalil et al. (2008); Rafindadi and Yusof (2013a;2013b;2013c;2014a) conclusively pointed out that sufficient empirical evidence has supported that in the long run, an efficient banking and financial system will be an embodiment of capital accumulation, which will in turn promotes economic efficiency and support sustainable economic growth. Following to these arguments, four leading hypotheses that constitute the cardinal linking point between financial development and economic growth were developed, for instance the supply-leading hypothesis commonly known as the “finance-led growth hypothesis” and the demand-following hypothesis or the “growth-lead finance hypothesis” were among the early hypothesis development on the literature linking financial development and economic growth, then followed by the feedback or ‘bidirectional causality hypothesis”. The fourth and the final was the independent hypothesis (see, for example, Al-Yousif (2002) and Majid (2007)).

The seminal work of Schumpeter (1911) remained valid until in 1973 when Mckinnon (1973) transformed it into a strong hypothesis and used it as key policy analysis for developing countries and has yielded a strong acceptability for capital accumulation and diversified financial intermediation. The hypotheses of Mckinnon (1973) clearly identified that resources wastage, interest curtailing, unplanned and inefficient investment are strong elements that manifest as a result of financial repression which was common in the 1960s and 1970s in most less developed countries (LDCs). Following to this, McKinnon-Shaw proceed to assert that the most viable and enduring alternative is the adoption of financial liberalization where this will pique savings and investment which will in turn open the route to investment growth. Fry (1988); Greenwood and Jovanovic (1990) and Pagano (1993) became the key proponents that formalized the popularization of this hypothesis with little amendment using their endogenous growth model. In their own perspective, the authors emphasised more on “the lack of explicit modelling of the link between financial and real sector variables” (Andersen and Tarp, 2003).

In contrast to all the views pointed above, Robinson (1952) argued that finance does not have the potency to influence growth rather; financial development follows economic growth due largely from the consistent rise in the demand for financial services. The author continued to point out that typically, financial institutions are a mere reflection of the growth of the economic activity, as a result of this, market operators will have a demand for financial services to justify the significant rise in entrepreneurial activities they are undertaking and nothing more but that. These arguments were in line with the assertions of the fourth hypothesis. The “independent hypothesis” as it is commonly known. The Independent hypotheses in its version of arguments underscored the fact that financial development and economic growth are not causally related. According to its postulator Robert Lucas (a 1988 Nobel Laureate winner in economics) argued that “economists badly overstress the role of financial factors in economic growth”. In support of this argument was Nicholas Stern (1989) who did not consider the impacts of the financial system in the economic growth process in his investigation of the factors leading to economic growth. Similar instances also occurred in the case of Meier and Seers (1984) and more recently, Ram (1999) where the author argued “…the predominant correlation between financial development and economic growth is negligible or weakly negative”. He continued to point out that, perceiving it from the direction of how economists across the Atlantic are treating the topic, it is imperative at this juncture to point out unequivocally that both theoretical and empirical consensus are yet to settle the facts in contention.

On the empirical perspective, mixed results are often discovered by researchers, notwithstanding that development, the vast majority of evidence is found to be more favorable towards the positive relationship that subsist between financial development and economic growth. For instance, King and Levine (1993b) established a landmark in their cross-sectional study between 1960 to 1989. The findings of their study established how the level of financial development attained by a country can predict the future economic growth and future productive efficiencies most likely to be attained by that country. Complementing this line of study was the findings of Odedokun (1996) were the author used time-series regression analysis for 71 developing countries from 1960-1980. Surprisingly, the outcome of the research showed significant similarities with the findings of King and Levine (1993b). In that study, the authors discovered how the efficient impacts of financial intermediation piques economic growth in 80% of the continents surveyed. Neusser and Kugler (1998) in an attempt to confirm the above findings, the authors devised a model that helped them to analyze the effect of the influence of finance-growth relationship for 13 Organization for Economic Cooperation and Development (OECD) countries from 1970-1991. They applied time series analysis; the findings produced a positive correlation between financial development and growth. In contrast to the findings of Odedokun (1996) who discovered a digression on the causal structure underlying the relationship between financial development and economic growth. To confirm these findings and using the same methodology with Neusser and Kugler (1998); Rousseau and Wachtel (1998) found positive and significant relationship between financial depth and economic growth in five industrialized countries.

Levine et al. (2000) in their seminal investigation on the relationship which aims at finding the effects of financial development (FD) on GDP used the data of 71 countries from the period 1960 to 1995. The researchers employed significant combinations of key variables, such as the proportion of liquid liabilities to GDP, the proportion of deposit money of commercial banks domestic assets plus central bank domestic assets and the proportion of credit issued to private companies to nominal GDP. The result established significant correlation between the financial system and economic growth. In another similar direction, Khan and Senhadji (2003) using the data set of 159 countries from the period of 1960-1999 and using the two-stage least squares (2SLS). The authors pointed out that not only that financial development has a positive and statistically significant effect on economic growth in all the countries surveyed but they also constitute the key element responsible for the significant attainment of sectorial growth. Similar direction of research findings that used panel data also occurred in the studies of Christopoulos and Tsionas (2004); Ndebbio (2004); Apergis et al. (2007); Kiran et al. (2009). In contrast to the direction of the above research findings by various researchers, other prominent studies argued that it is economic growth that facilitate in the creation of the natural incentives for mobilizing financial development to attain an efficient peak. For instance, Demetriades and Hussein (1996) in trying to determine the relationship between financial development and economic growth used time series data to analyze the effects of this relationship on sixteen countries from 1960-1990. The authors in their own wisdom used the proportion of bank deposit liabilities to GDP and the proportion of bank lending on the private sector to GDP which they used as indicators of financial development. The result of the study showed how the causal effect between the defendant variable (FD) and the long run growth moves in a different direction for the respective countries surveyed.

Zang and Kim (2007) on their own part while examining the panel of 74 countries from 1961-1995. The researchers used the proportion of liquid liabilities to GDP, and the proportion of commercial bank deposit to domestic assets plus central bank domestic assets and credit liabilities issued to productive sectors of the economy. Surprisingly, the outcome of the result was same with Demetriades and Hussein (1996) that economic growth precedes financial development. Other supporters of this line of development using panel data research are Luintel and Khan (1999); Abu-Bader and Abu-Qarn (2006); Lucas (1988); and Mohamed (2008). However in the case of mixed findings, Esso (2009) used ARDL model to investigate the causal effects between FD and growth as a result of this, the author used data of respective ECOWAS countries from 1960-2005. In an attempt to make a valid and robust findings he co-opted in his research the proportion of M2 to GDP as the key and only indicator of financial development. The finding of the author established a statistically significant long-run association between financial development and economic growth in 4 respective countries among them are Cote d’Ivoire, Guinea, Niger and Togo while a negative long run association was discovered in Sierra Leone and Cape Verde. The results of the causality test showed how financial development causes economic growth only in Cote d’Ivoire and Guinea. The author concluded that the relationship between FD and economic growth is not generalizable considering key un generalizable elements inherent in individual country. In a more recent development Acaravci et al. (2009) used panel co-integration and panel GMM to determine the effect of the association between FD and economic growth for some selected SSA countries from 1975-2005. The outcome of the research showed a negative long-run association between financial development and economic growth. As a result of this, the authors investigated the bi-directional causal relationship between the growth of real GDP per capita and the domestic credit provided by the banking sector for the panel, the finding indicated that the selected SSA countries can enhance their growth prospects by devising a mechanism that can enable them to have an efficient and effective financial systems and vice versa. Abdullahi (2010) in his study of the linkages between financial liberalization, financial development and growth, the author used panel data of 15 SSA countries from 1976-2005. The finding of the study reveals the existence of long-run equilibrium relationship between financial development and economic growth. In order to confirm this finding he proceed with a country-by-country time series investigations and the evidence still showed that the direction of causality is running from financial development to growth. Supporting the work of Abdullahi (2010); Rachdi (2011) investigated the causal relationship between financial development and economic growth in MENA and the OECD continents. He used panel data cointegration and GMM system approach. His findings established that financial development is positively and strongly correlated with real GDP. This evidence suggests that the financial sector and real sector entities are having some degrees of association in OECD and MENA countries. However, after checking for robustness tests and the error correction approach, the finding of the author indicated a bidirectional causality for the OECD countries and unidirectional (economic growth- financial development) for the MENA countries. The later result was explained to be due to the weak financial systems of these countries.

Ndambiri (2012) while using a panel of 19 SSA countries from 1982-2000 investigated the determinants of economic growth in the selected continents. The authors applied the GMM methodology. The findings of their research established that physical capital formation and human capital formations are foremost the significant base line to the economic growth prospects of Sub-Saharan continents. However, and according to the author’s government expenditure, nominal discount rate and foreign aid significantly lead to negative economic growth.

3. METHODOLOGY

The traditional approach is to explore the cointegration relationship among the variable used in the study, in this respect, most researchers use the Engle and Granger and the Johansen cointegration mechanism. However these two approaches have some severe limitations. First of all, Engle and Granger is only application for bi-variate test so it doesn’t consider more than 2 variables at a time. Secondly, Johansen test is only applicable when the same order of integration of the variables are achieved. Moreover, Johansen is very sensitive with respect to optimal lag order selection (Gonzalo, 1994). See also Rafindadi and Ozturk (2015); Rafindadi (2016a;2016b). Taking in to considerations the myriad shortcomings of these models and following the series of criticism this study applied the autoregressive distributed lag (ARDL) Bounds test approach to cointegration by Pesaran et al. (2001). This mechanism has some key important advantages over all other existing methods and these are: (i) after selecting the optimum lag, co-integration relationship can be estimated under OLS technique (ii) this test furnishes the long and short-–run relationship among the variables and also provide the coefficient of the relationship simultaneously. (iii) In contrast to Engle-Granger and Johansen methods, this test provides consistent result even in existing mix order of I (0) or I (1) or mutually integrated relationships. However, this test procedure will not be applicable if an I (2) series exists in the model, (iv) Notwithstanding the incidence of endogeneity problem, ARDL model provides unbiased coefficients of explanatory variables along with valid t statistics. In addition, the ARDL model corrects sufficiently omitted lag variable bias (Inder, 1993). (v) Finally this test is very efficient and consistent in small and finite sample size.

3.1. Model Specification and Estimation Procedure

The prime objective of this paper is to examine the relationship between financial development and economic growth of the Ghanaian economy by incorporating government expenditure, population, and trade openness (measures by exports, imports and trade). The time span of the present study is 1970-2012. The functional form of the empirical model is given as following:

3.2. Model Estimation Procedure

In this study, the ARDL bounds test approach to cointegration was applied. This is because, the Pesaran et al. (2001) ARDL bound testing approach to cointegration was more effective and superior when compared with the Johansen cointegration model (Johansen and Julius, 1990)1 . In essence, the ARDL bound test has the key advantage of dichotomising between the dependent and the independent variables among others. In the estimation process using the ARDL bounds testing approach to cointegration, the study begin with the estimation of equation (1) under the OLS approach. Foremost, conducting the Wald Test or F- test for joint significance of the coefficients of lagged variables will be very essential for the purpose of examining the existence of long-run relationship among the variables. In this respect, the null hypothesis (H0):![]() i.e. that there is no cointegration among the variables, is compared against the alternative hypothesis (Ha):

i.e. that there is no cointegration among the variables, is compared against the alternative hypothesis (Ha):![]() Then the calculated F statistics is evaluated with the critical value (upper and lower bound) given by Pesaran et al. (2001). If the F-statistic is above the upper critical value given by Pesaran et al. (2001) the null hypothesis of no co-integration is rejected which indicates that long-run relationship exists among the variables and, conversely, if the F-statistic is smaller than the lower critical value the null hypothesis cannot be rejected implying no cointegration among the variables. However, if the F-statistic lies between lower and upper critical values, the test is inconclusive. In the second step, after establishing cointegration relationship among the variables, long-run coefficient of the ARDL model can be estimated following Rafindadi and Yusof (2013a;2013b;2013c). See also; Rafindadi and Ozturk (2015) and Rafindadi and Yusof (2015). See also Rafindadi (2014a;2014b) and Rafindadi (2016a;2016b;2016c):

Then the calculated F statistics is evaluated with the critical value (upper and lower bound) given by Pesaran et al. (2001). If the F-statistic is above the upper critical value given by Pesaran et al. (2001) the null hypothesis of no co-integration is rejected which indicates that long-run relationship exists among the variables and, conversely, if the F-statistic is smaller than the lower critical value the null hypothesis cannot be rejected implying no cointegration among the variables. However, if the F-statistic lies between lower and upper critical values, the test is inconclusive. In the second step, after establishing cointegration relationship among the variables, long-run coefficient of the ARDL model can be estimated following Rafindadi and Yusof (2013a;2013b;2013c). See also; Rafindadi and Ozturk (2015) and Rafindadi and Yusof (2015). See also Rafindadi (2014a;2014b) and Rafindadi (2016a;2016b;2016c):

4. PRESENTATION OF RESULTS

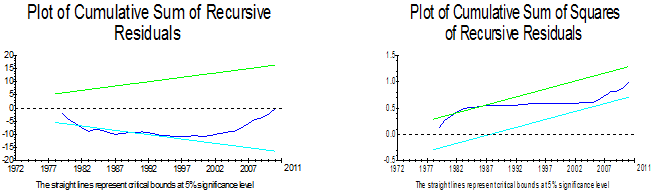

To ensure the stability of the model, the study performed two set of stability tests and these are the long-run coefficients and the short run dynamics. This was carried out following the suggestion by Pesaran and Pesaran (1997) to check the stability of short and long-run parameters of the selected ARDL model after estimating the error correction model by using the cumulative sum of recursive residuals (CUSUM) and the cumulative sum of squares of recursive residuals (CUSUMSQ) tests. This study applied these two test in order to ensure robust findings.

Table-1. Unit root test

Variables |

ADF Intercept & Trend I(0) |

ADF Intercept & Trend I(1) |

LGDP |

-0.84 |

-5.45*** |

TO |

-3.52** |

-5.33*** |

GOV |

-2.62 |

-6.07*** |

POP |

-6.43*** |

-1.85 |

FD |

0.29 |

-10.34*** |

** at 5%, ***at 1% * at 10%

Source: Estimated by the authors using E-views 8

Before proceeding to the ARDL estimation, this study conduct unit root test in order to observe the stationarity of each variables used in the study. In addition to that and in order to ensure that no variable is I(2) so as to avoid the spurious result as Ouattara (2007) argues that ARDL model is based on the assumption of I(0) and I(1). In this respect unit root test is carried out to ensure no variable exceed the integrated order of I (0) and I (1). The unit root applied in this study considers both constant and tread, and table 1 exhibit that all the variables are stationary at I (1) except TO and POP that were found to be stationary at I (0). At the presence of such mixed order of integration, the study proceed to apply ARDL bounds testing approach to cointegration approach test other than the Johansen and Jusilius cointegration approach.

Table-2. Optimum Lag Selection

Lag |

LogL |

LR |

FPE |

AIC |

SC |

HQ |

0 |

-286.619 |

NA |

3.186 |

15.348 |

15.563 |

15.425 |

1 |

-141.329 |

244.69 |

0.005 |

9.017 |

10.310 |

9.477 |

2 |

-57.659 |

118.90 |

0.0002 |

5.929 |

8.299 |

6.772 |

3 |

10.130 |

78.493 |

3.600 |

3.677 |

7.124 |

4.903 |

4 |

61.022 |

45.535* |

1.400* |

2.314* |

6.839* |

3.924* |

Source: Estimated by the authors using E-views 8

* indicates lag order selected by the criterion

Prior to estimating ARDL bounds test, this study conducts the optimum lag selection criteria. In order to ensure robustness, the study applied the Schwarz Bayesian Criterion (SC) where it reveals the optimum lag to be 4.

Table-3. Result from the bound test

Dep. Var. |

SC Lag |

F-statistic |

Prob |

Outcome |

FGDP(GDP| TO, POP, GOV, FD) |

4 |

4.169*** |

0 |

Cointegration |

FTO(TO|GDP, FCF, POP, GOV, FD) |

4 |

0.532 |

0.75 |

No cointegration |

FGOV(GOV|GDP,FCF, TO, POP, FD) |

4 |

1.915 |

0.135 |

Inconclusive |

FFD(FD|GDP,FCF, TO, POP, GOV) |

4 |

3.021* |

0.033 |

Cointegration |

FPOP(POP|GDP,FCF, TO,, GOV, FD) |

4 |

5.44*** |

0 |

Cointegration |

Source: Estimated by the authors using E-views 8 ** at 5%, ***at 1% * at 10%

Table 3 reports the results of the calculated F-statistics in that table, when each variable is considered as a dependent variable (normalized) in the ARDL-OLS regressions. The calculated F-statistics FGDP (GDP| TO, POP, GOV, FD) = 4.169 is higher than the upper bound critical value 3.991 at the 1% level also FFD (FD|GDP, TO, POP, GOV) =5.44 which is significant at 1% hence the null hypotheses of no cointegration is rejected when FD is considered as dependent variable. Since cointegration is established in the case of FGDP (GDP| TO, POP, GOV, FD), hence the study proceed to estimate the long run and short run dynamics.

Table-4. Estimated long-run coefficients using the ARDL bounds test

ARDL(1,0,0,0,0) selected based on Schwarz Bayesian Criterion, Dependent variable is LGDP |

||||

Regressor |

Coefficient |

Standard Error |

T-Ratio |

Probability |

GOV |

0.01 |

0.025 |

0.422 |

0.676 |

POP |

-0.019 |

0.135 |

-0.14 |

0.889 |

FD |

0.086 |

0.029 |

2.899 |

0.006 |

TO |

0.005 |

0.003 |

1.916 |

0.064 |

C |

5.188 |

0.533 |

9.726 |

0 |

Source: Estimated by the authors using E-views 8

Table 4 represents the long-run impact of each independent variable on the Ghanaian GDP growth. It shows that FD has a strong positive impact on GDP in the long-run. Likewise, TO helps in fostering the long-run economic growth of the country. The Table also shows that POP has a negative impact on long-run GDP growth. Indeed this result is very expected in the case of Ghana where population density is extremely high. The study shows that GOV expenditure has a positive but insignificant impact on the Ghanaian GDP.

Table-5. Error correction representation for the selected ARDL Model

ARDL(1,0,0,0,0) dependent variable is ΔlGDP |

||||

Regressor |

Coefficient |

Standard Error |

T-Ratio |

Probability |

ΔGOV |

0.001 |

0.004 |

0.39 |

0.698 |

ΔPOP |

-0.003 |

0.022 |

-0.142 |

0.888 |

ΔFD |

0.014 |

0.009 |

1.501 |

0.142 |

ΔTO |

0.001 |

0.298 |

3.352 |

0.002 |

ΔC |

0.892 |

0.557 |

1.602 |

0.118 |

ECM (-1) |

-0.172 |

0.106 |

-1.616 |

0.115 |

| ECM = GDP -.010927*GOV + .019034*POP -.086828*FD -.0058184*TO-5.1882*C | ||||

Source: Estimated by the authors using E-views 8

In Table 5 is the presentation of the short-run results. In that Table the findings of the estimated model established the existence of significant impact of the Ghanaian Trade openness to the country’s GDP. Similar discovery was made in the case of the long-run model estimation result. In addition to that, GOV was also found to be positive but providing an insignificant contributions to the country’s GDP. However, the immediate impact of population growth is surprisingly found to be negative and insignificant. Suggesting that, the vast population growth of Ghana provides no meaningful contributions to the country’s GDP. This may be attributable to the low entrepreneurial capacity and participation of the Ghanaian population. This may be necessitated by the rising level of poverty which is the case in most Sub-Saharan African countries, high costs of doing business, poor and epileptic energy supply, poor infrastructural facilities, and low level or poor government commitment towards the enhancement of the country’s entrepreneurial development. This situation could be attributed to the high level of political instability in the country which among other things created huge social and economic unrest in recent years of the country’s struggle to regain political and economic wherewithal. In a related development, the FD (financial development) of the Ghanaian economy was discovered to have no significant contribution to the country’s economic growth in the short-run. This is in contrast to the long-run findings were financial development was detected to have a positive and significant impact to the country’s GDP. The Error correction coefficient is negative and significant which means that after any economic shock it adjusts 17% per year towards the long-run equilibrium.

Table-6. Model diagnostic tests

Source: Estimated by the authors using E-views 8

5. CONCLUSION AND POLICY GUIDE

This study investigated the relationship between economic growth and financial development in Ghana by incorporating government expenditure, population and trade openness (exports, imports, trade) of the Ghanaian economy. The time span of the study is 1970-2012. The study applied the ARDL bounds testing approach to cointegration in analyzing the cointegration relationship between the variables. The long-run result established that FD has a strong positive impact on GDP. In addition to that TO was detected to have a positive value in fostering the long-run economic growth of the country. POP was among other variables that the study has discovered it to have a negative impact on the long-run growth of the country’s GDP. Indeed this result is very much expected in the case of Ghana where population density is extremely high and with no corresponding rise in job opportunities or strong government policy and commitment that could pique entrepreneurial opportunities.

In a related development, the study discovered GOV expenditure to be positive but having an insignificant impact on the Ghanaian GDP. This development suggest that growth on the side of the huge government expenditure does not deepen the financial development of the country for it to have positive stimulating force to the country’s GDP as rightly suggested by John Maynard Keynes and the Wagner’s law of public expenditure. This development may be due to systemic corruption and embezzlement that are a characteristic of most African economies. To support this claim, Table 4 and Table 5 of the empirical discoveries made in this study indicated that both in the long-run and in the short-run the excessive government expenditure of the country has not been of any significance to the country’s economic growth prospects. This development has strongly defied the assertions made by the Keynesian theory of public expenditure. In his wise assertion Keynes argued that public expenditure is an exogenous factor which can be utilized as a policy instrument to promote economic growth. According to the Keynesian economic thought, public expenditure should be seen as a cardinal pillar that contribute positively to economic growth. This is in the sense that, an increase in government consumption should as best as possible lead to an increase in employment, through profitable investment and other multiplier effects on aggregate demand. The author continue to point out that, government expenditure should augment the aggregate demand, which should in turn be capable of provoking an increased output depending on expenditure multiplier. In addition to that, Adolph Wagner contend with the fact that, the rise in public expenditure will be more than proportional to an increase in the national income (income elastic wants) and this development will in turn result in a relative expansion of the public sector institutions. Musgrave and Musgrave (1976) in support of Wagner’s law, opined that as progressive nations industrialize, the share of the public sector in the national economy should grow continually. However, in the case of Ghana this development was quite dismal. Under normal circumstances, government consumption on goods and services in Ghana should stimulate the economy which should in turn result in the demand for more financial services. However, due to systemic corruption and embezzlement this development has defied the expected positive contributions to the Ghanaian GDP.

In addition to the foregoing development, the study discovered, the immediate impact of population growth to be negative and insignificant in both the long-run and the short-run. This development suggests that, the vast population growth of Ghana provides no meaningful contributions to the country’s GDP. The finding on this part of the study is a clear indication that, entrepreneurial activities in the country is very low, and government policies yielded no positive impact on human capital development. With this finding, it became imperative to the Ghanaian policy makers to re-strategize in creating more opening to the country’s teeming population. The short-run empirical result further revealed that financial development in Ghana does not enhance the country’s economic growth. In order to ameliorate this worsening trend it is imperative to consolidate the gains of financial development in Ghana. To ensure this, there is the need to stabilize the performance of the financial system as recently done in Nigeria. This can be achieved through the restructuring of the Ghanaian banking system in particular and the appropriate use of fiscal and monetary measures. However, no matter the effort placed in this policy action, the result may still continue to be sordid. What is essential is for the Ghanaian government to place all effort in eliminating all forms of financial repression, and ensure the provisions of effective and efficient financial system that allow for the voluntary mobilization of savings, resource allocation, pooling of risk, inducing liquidity, and reducing heavy transaction costs. In addition to that, stringent measures should also be placed with respect to the costs, quality and volume of doing business in the country. This can be done by liberalizing the financial system which should in turn be capable of providing affordable but productive loans to quality entrepreneurial practices, and the establishment of all measures that will help in attracting foreign direct investment in to the country. This can be attained through sound political stability, provision of basic infrastructural facilities, better supervision and prudential regulations, encouragement of entrepreneurial rise, innovation and creativities within the local economies.

In conclusion, this study point it clearly to the Ghanaian policy makers that other internal factors could combine to inhibit the growth prospects of the country’s economy. These factors include the level of macroeconomic stability in the country and how cogent policy actions are instituted in counteracting negative changes. In addition to that, policy makers need to check how natural resource endowments are meaningfully exploited; how education in the country could pique high level of applicable innovation and creativity (which relate to educational systems quality and how education is exploited to create technology and science); institutional development and how sound they are in ensuring budgetary control and quality of implementation; the level of capital accumulation and how quick could this expand to provide more value; the ability of the financial system to convert capital into meaningful productivities; and the sophistication of the financial system and its agility to channel funds to ensure the thriving of entrepreneurial activities and exchange rate stabilisation among others. Rafindadi and Yusof (2013b) established that in the modern era, the most crucial factor affecting economic growth apart from those in the empirical and theoretical discoveries are a country’s ability to deal with international economic risks and how to cushion itself against these risks effectively. In addition to that, strategic but synergic measure which saves cost should be instituted to mitigate the effects of these internal risks on the country’s economic systems and subsystems. Failure to do so may translate in to additional reason that explain why countries such as Ghana may be experiencing poor economic growth. Consequently, it is pertinent at this juncture to note that the relationship between financial development and economic growth may not be consistently linear, but rather dependent on the ups and downs of an economic system and how carefully are these situations managed to avoid cannibalization. On the whole, the best quality route towards growing the growth of a country’s economic system apart infrastructural facilities rest mostly on infrastructural provisions which in turn piques productivities. In essence if the condition of a country’s productivities deteriorates, particularly if it is aggravated by less productive population that keep expanding every now and then obviously this situation will be more disastrous and with varying degrees of spillage where taming this spillage could be costly and ineffective in the long-run (Rafindadi and Yusof, 2014a).

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Abdullahi, A.D., 2010. Financial liberalization, financial development and growth linkages in Sub-Saharan African countries: An empirical investigation. Studies in Economics and Finance, 27(4): 314 – 339.

Abu-Bader, S. and A. Abu-Qarn, 2006. Financial development and economic growth nexus: Time series evidence from Middle Eastern and North African countries. Munich Personal RePEc Archive (MPRA) Paper No. 972. Germany: University Library of Munich.

Acaravci, S.K., I. Ozturk and A. Acaravci, 2009. Financial development and economic growth: Literature survey and empirical evidence from Sub-Saharan African countries. South African Journal of Economic and Management Sciences, 12(1): 11-27.

Al-Yousif, Y.K., 2002. Financial development and economic growth: Another look at the evidence from developing countries. Review of Financial Economics, 11(2): 131-150.

Andersen, T.B. and F. Tarp, 2003. Financial liberalization, financial development and economic growth in LDCs. Journal of International Development, 15(2): 189-209.

Apergis, N., I. Filippidis and C. Economidou, 2007. Financial deepening and economic growth linkages: A panel data analysis. Review of World Economics, 143(3): 179-198.

Bagehot, W., 1873. Lombard street. Homewood IL: Richard D. Irwin.

Bentzen, I. and T. Engsted, 2001. A revival of the autoregressive distributed lag model in estimating energy demand relationship. Energy, 26(3): 45-55.

Christopoulos, D.K. and E.G. Tsionas, 2004. Financial development and economic growth: Evidence from panel unit root and cointegration tests. Journal of Development Economics, 73(1): 55-74.

Demetriades, P.O. and A.K. Hussein, 1996. Does financial development cause economic growth? Time series evidence from 16 countries. Journal of Development Economics, 51(4): 387-411.

Elbadawi, I.A., 1999. External aid: Help or hindrance to export orientation in Africa. Journal of African Economics, 8(4): 578-616.

Esso, L.J., 2009. Cointegration and causality between financial development and economic growth: Evidence from ECOWAS countries. European Journal of Economics, Finance and Administrative Sciences, 16.

Fowowe, B., 2008. Financial liberalization policies and economic growth: Panel data evidence from Sub-Saharan Africa. African Development Review, 20(3): 549-574.

Fry, M.J., 1988. Money, interest, and banking in economic development. Baltimore and London: Johns Hopkins University Press, Johns Hopkins Studies in Development Series.

Ghatak, S. and J. Siddiki, 2001. The use of ARDL approach in estimating virtual exchange rate in India. Journal of Applied Statistics, 28(2): 573-583.

Goldsmith, R.W., 1969. Financial structure and development. New Haven, C.T.: Yale University Press.

Gonzalo, J., 1994. Five alternative methods of estimating long-run equilibrium relationships. Journal of Econometrics, 60(2): 203-233.

Greenwood, J. and B. Jovanovic, 1990. Financial development, growth, and the distribution of income. London, Ont., Canada: Dept. of Economics, Social Science Centre, University of Western Ontario.

Hicks, J., 1969. A theory of economic history. Oxford: Oxford University Press, 163.

Inder, B., 1993. Estimating long-run relationship in economics: A comparison of different approaches. Journal of Econometrics, 57(4): 53-68.

Jalil, A., Y. Ma and A. Naveed, 2008. The finance-fluctuation nexus: Further evidence from Pakistan and China. International Research Journal of Finance and Economics, 14(3): 220-237.

Johansen, S. and K. Julius, 1990. The full information maximum likelihood procedure for inference on cointegration with application to the demand of money. Oxford Bulletin of Economics and Statistics, 52(4): 169-210.

Khan, A., 2000. The finance and growth nexus. Business Review, 2.

Khan, M.A., A. Qayyum and A.S. Saeed, 2005. Financial development and economic growth: The case of Pakistan. Pakistan Development Review, 44, 4(2): 819-837.

Khan, M.S. and A.S. Senhadji, 2003. Financial development and economic growth: A review and new evidence. Journal of African Economies, 12(2): 89-110.

King, R. and R. Levine, 1993a;1993b. Finance and growth: Schumpeter might be right. Quarterly Journal of Economics, 153(2): 717–738.

King, R.G. and R. Levine, 1993b. Finance, entrepreneurship, and growth: Theory and evidence. Journal of Monetary Economics, 32(3): 513-542.

Kiran, B., N.C. Yavus and B. Guris, 2009. Financial development and economic growth: A panel data analysis of emerging countries. International Research Journal of Finance and Economics, 30(2): 87-94.

Levine, R., N. Loayza and T. Beck, 2000. Financial intermediation and growth: Causality and causes. Journal of Monetary Economics, 46(1): 31–77.

Lucas, R.E.J., 1988. On the mechanics of economic development. Journal of Monetary Economics, 22(2): 3–42.

Luintel, K.B. and M. Khan, 1999. A quantitative reassessment of the finance–growth nexus: Evidence from a multivariate VAR. Journal of Development Economics, 60(2): 381-405.

Majid, M.S., 2007. Does financial development and inflation Spur economic growth in Thailand? Chulalongkorn Journal of Economics, 19(2): 161–184.

Mckinnon, R.I., 1973. Money and capital in economic development. Washington: Brookings Institution.

Meier, G.M. and D. Seers, 1984. Pioneers in development. New York: Oxford University Press.

Mohamed, S.E., 2008. Financial-growth nexus in Sudan: Empirical assessment based on an autoregressive distributed lag (ARDL) model. Arab Planning Institute Working Paper Series No. 0803.

Musgrave, R. and P. Musgrave, 1976. Public finance in theory and practice. New York: McGraw-Hill.

Ndambiri, H.K., 2012. Determinants of economic growth in Sub-Saharan Africa: A panel data approach. International Journal of Economics and Management Sciences 2(2): 18-24.

Ndebbio, J.E.U., 2004. Financial deepening, economic growth and development: Evidence from selected Sub-Saharan African countries. African Economic Research Consortium (AERC) Research Paper No. 142.

Neusser, K. and M. Kugler, 1998. Manufacturing growth and financial development: Evidence from oecd countries. Review of Economics and Statistics, 80(4): 638-646.

Odedokun, M.O., 1996. Alternative econometric approaches for analyzing the role of the financial sector in economic growth: Time-series evidence from LDCs. Journal of Development Economics, 50(1): 119-146.

Ouattara, B., 2007. Foreign aid, public savings displacement and aid dependency in Cote d'Ivoire: An aid disaggregation approach. Oxford Development Studies, 35(1): 33-46.

Pagano, M., 1993. Financial markets and growth: An overview. European Economic Review, 37(2-3): 613-622.

Pagano, M. and P. Volpin, 2001. The political economy of finance. Oxford Review of Economic Policy, 17(4): 502-519.

Pesaran, M.H. and B. Pesaran, 1997. Working with microfit 4.0: Interactive econometric analysis. Oxford: Oxford University Press.

Pesaran, M.H., Y. Shin and R.J. Smith, 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(6): 289-326.

Rachdi, H., 2011. The causality between financial development and economic growth: A panel data cointegration. International Journal of Economics and Finance, 3(1): 143-158.

Rafindadi and Ozturk, 2015. Natural gas consumption and economic growth nexus: Is the 10th Malaysian plan attainable within the limits of its resource? Renewable and Sustainable Energy Reviews, 49(7): 1221–1232.

Rafindadi, A.A., 2014a. Econometric prediction on the effects of financial development and trade openness on the German energy consumption: A startling revelation from the data set. International Journal of Energy Economics and Policy, 5(1): 182-196.

Rafindadi, A.A., 2014b. Could the expanding economic growth and trade openness of the United Kingdom pose a threat to its existing energy predicaments? International Journal of Energy Economics and Policy, 5(1) 121-137.

Rafindadi, A.A., 2016a. Revisiting the concept of environmental Kuznets curve in period of energy disaster and deteriorating income: Empirical evidence from Japan. Energy Policy, 94(7): 274-284.

Rafindadi, A.A. and I. Ozturk, 2016b. Effects of financial development, economic growth and trade on electricity consumption: Evidence from Post-Fukushima Japan. Renewable and Sustainable Energy Reviews, 54(6): 1073–1084.

Rafindadi, A.A., 2016c. Does the need for economic growth influence energy consumption and CO 2 emissions in Nigeria? Evidence from the innovation accounting test. Renewable and Sustainable Energy Reviews, 62(6): 1209-1225.

Rafindadi, A.A. and Z. Yusof, 2013a. Is financial development a factor to the leading growth profile of the South African economy? Measuring and uncovering the hidden secret. International Journal of Economics and Empirical Research, 1(9): 99-112.

Rafindadi, A.A. and Z. Yusof, 2013c. Revisiting the contention of the FD/GDP nexus of the Northern Sudanese economy: A new startling empirical result. World Applied Sciences Journal, 28(9): 182-194.

Rafindadi, A.A. and Z. Yusof, 2013b. A startling new empirical finding on the nexus between financial development and economic growth in Kenya. World Applied. Sciences Journal, 28(9): 147-161.

Rafindadi, A.A. and Z. Yusof, 2014a. An econometric estimation and prediction of the effects of nominal devaluation on real devaluation: Does the Marshal-Lerner (M-L) assumptions Fits in Nigeria? International Journal of Economics and Financial Issues, 4(4): 819-835.

Rafindadi, A.A. and Z. Yusof, 2014b. Are the periods of currency collapse an impediment to entrepreneurship and entrepreneurial haven? Evidence from regional comparison. International Journal of Economics and Financial Issues, 4(4): 886-908.

Rafindadi, A.A. and Z. Yusof, 2015. Do the dynamics of financial development spur economic growth in Nigeria’s contemporal growth struggle? A fact beyond the figures. Quality & Quantity, 49(1): 365-384.

Rafindadi, A.A. and Z. Yusof, 2015b. Are linear and nonlinear exchange rate exposures aggravating agents to corporate bankruptcy in Nigeria? New evidence from the “U” test analysis. International Journal of Economics and Financial Issues, 5(1): 212-229.

Rafindadi, S.A., 2011. Foreign aid inflows and the real exchange rate: Are there Dutch disease effects in Ghana? IUP Journal of Financial Economics, 9(4): 180-210.

Ram, R., 1999. Financial development and economic growth: Aditional evidence. Journal of Development Studies, 35(2): 164-174.

Robinson, J., 1952. The rate of interests and other easys. London: Macmillan.

Rousseau, P.L. and P. Wachtel, 1998. Financial intermediation and economic performance: Historical evidence from five industrialized countries. Journal of Money, Credit and Banking, 30(1): 657-678.

Schumpeter, J.A., 1911. The theory of economic development. Cambridge: MA7 Harvard Univ. Press.

Shan, J., 2005. Does financial development 'lead' economic growth? A vector auto-regression appraisal. Applied Economics, 37(3): 1353-1361.

Stern, N., 1989. The economics of development: A survey. Economic Journal, 99(3): 597-685.

Stiglitz, J., 1998. More instruments and broader goals: Moving toward the post-Washington consensus (2)1,110-130. Helsinki: UNU/WIDER.

The World Bank, 2013. Washington, D.C: World Development Indicators. Retrieved from http://data.worldbank.org/data-catalog/world-development-indicators.

World Bank, 2009. Available from http://siteresources.worldbank.org/EXTAR2009/Resources/6223977-1252950831873/AR09_Complete.pdf [Accessed August, 2016].

Zang, H. and Y.C. Kim, 2007. Does financial development precede growth? Robinson and Lucas might be right. Applied Economic Letters, 14(3): 15-19.