AUDIT IN RUSSIAN FEDERATION AND THE RESEARCH TOWARD THE DETERMINATION OF THE FUNCTIONING OF AUDIT MECHANISM

1Assistant Professor, Faculty of Economics and Administrative Sciences, Iğdır University, Iğdır, Turkey, 2Associate Professor, Faculty of Economics and Administrative Sciences, Dokuz Eylül University, Izmir, Turkey

ABSTRACT

Although the development of audit laws in Russia corresponds to the end of the 80s, there has been experienced significant progress in this respect in the early 2000s. Since the early 2000s, many laws have been developed and many local auditing standards have been prepared in the country by benefiting from the international experience. Since 2010, the government control over the audit activity began to decline. In this study, information about the legal regulations implemented in Russia has been provided. Subsequently, basic indicators pertaining to the audit for the years 2013-2014 such, as the number of auditors and audit firms, distribution services volume by the auditing company, the number of audited companies, the revenue structure of the audit firms and regional distribution of audit firms, has been discussed and the impact of legislation on audit activity was investigated. Data related to the audit, are based on information published by the Russian Ministry of Finance.

© 2017 AESS Publications. All Rights Reserved.

Keywords: Auditing, Audit companies, Auditors, Regulations, Self-regulatory organizations of auditors in Russian federation, Ministry of Finance.

JEL Classification: M42, M48, C10.

Received: 26 July 2016/ Revised: 1 September 2016/ Accepted: 29 September 2016/ Published: 24 October 2016

Contribution/ Originality

In the scope of this study, using statistical data of the Russian Ministry of Finance, main indicators pertaining to the audit of the 2013-2014 year are included. As a result of examination of the information for every two years, both positive and negative developments in the audit field have been revealed. In this context, this study, including legal developments in Russia and comparative data, will add value to the relevant literature.

1. INTRODUCTION

Audit, is one of the elements of market economy that has substantial place in the development of country economy and entrepreneurship. The reliance of the interested parties to the financial statements, verified by the audit reports is ensured by the effectiveness of the legislation, regulating the audit activity and the code of professional ethics and the effectiveness of the organizations, controlling activity of auditors.

It is widely known that 1990s included the period of disintegration of USSR (Union of Soviet Socialist Republics). Right after the disintegration, getting into a new formation named “Commonwealth of Independent States”, by the interpretation of the disintegration of Soviets by West was a “beginning of instability on the East” tacking part of Russia and even in other names and ways was maintaining their efforts to revitalize the Soviet Union (Peker, 1996). At this point Russian Federation, that was at the central the political, cultural and economic status in the USSR, with the collapse of the Communist order, has passed to a new governing and economic order (Ayanoğlu, 2004). With this transition to a market economy, the works on reconstruction of Russian Federation accounting system in gained speed.

The development of the market relations in Russia, have brought about the evolvement in audit, the outlook on the auditor profession and in the series of new significant regulations in this scope. By repealing the Law No. 2263 of the 22.12.1993 that was including the interim arrangements, relating the audit activity, one of the most important regulations made in the audit area was coming to the effect of the Law No.119 of the 07.08.2001, after improved in 2008. The Law involves the audit company, auditor and auditor’s mission concepts, and the information regarding the companies to be subject to mandatory audit and reveals several amendments performed in the audit area like, education and certification of the auditors.

One of the other fundamental reforms realized in Russian audit market, was amendments in legal regulations that anticipated the passing to the self-audit process without getting a license. These amendments aim to considerably constraint the governmental intervention to the audit activity and establish the professional and social oversight mechanism of the audit activity. Nowadays, in consequence of the implemented amendments, there are five “Associations Self-regulatory Organizations of Auditors” existing in Russian Federation, maintaining their studies towards the reducing of public oversight in audit activity. Within this paper, at first, the Russian audit and the process of evolvement of the audit would be reviewed and after that, the legal arrangements would be included. Besides this, the place of audit mechanism in Russian Federation at application would be examined by the years specified for the study.

2. THE AUDIT IN RUSSIAN FEDERATION AND THE LEGAL AUDITING PROCESS

Even before the ‘October Revolution’ the cultural and application-oriented structure concerning the double-entry bookkeeping system prevailed in Russia. For example, K. I. Arnold (1775-1845) has written one of his major works, distinguishing the accounting theory from the application in the first half of the 19th century. Russian accounting philosopher Akhmatov in 1809 published his book named, “Italian Accounting Principle”. In the last quarter of 19th century the Russian authors of accounting F. V. Ezersky, A. M. Volf concentrating around the “Accounting Journal”, made significant contributions to the science of accounting. Consequently, when the socialist regime entered to the effect by the October Revolution of 1917, there had been a significant accounting system practice in Russia. It is observed, that the socialist regime naturally began the investigation of means on making use of this background (Güvemli, 2010).

The socialism is the unique order, showing progress versus capitalism 20th century. V. I. Lenin, the founder of the Soviet Union, while saying: “Socialism is accounting”, manifests that he is interested in accounting theory and its applications and definitely comments that he sees the accounting intentional for audit. Famous Russian historian Sokolov, conveyed this issue in work he has written in 1996, named “Accounting, From the Roots Until Today” (Güvemli, 2001). As the indication of the form, the conception of accounting-audit has taken in the period, revealed in the beginning of socialist system, the purpose of accounting was expressed in a chapter of the book prepared at the mastership of Pankov “General Accounting Theory” in this way:

‘The most important purpose of accounting is, to assist the government in issues relating the audit at time, the measurement and recording of procedures, the protection of socialist property, measurement of labor and consumption, sustaining of the economy policy committed for auditing of implementing the government plan. The one of the purposes of accounting is strengthening the economic regime. Economic and savings resource utilization is one of the most important characteristics of advanced socialist economy. Also the one of the most substantive factors, beyond the strengthening the economic regime is developing accounting regime’ (Güvemli, 2001).

The statements regarding the issue of accounting of socialist system, take place in the work of named, “Accounting and Accounting Reports” written by V. I. Ryabkin, T. I. Matveeve and V. E. Deshin in the beginning of the disintegration period. There is internal audit of accounting in socialist system. This type of audit ensures that the accounting records and financial statements give true and reliable information and compliance with the principles and rules. It performs the external audit present in capitalist countries. Because in socialist system, the assets and resources that are put under company’s order, are in possession of the Government and are the assets assigned to the company. In the capitalist system there is a form of relation as accounting-company owner-government and in socialist system the relation is in accounting- government form. Under these circumstances, accounting itself becomes the auditing instrument; the fundamental purpose of accounting comes out to be audit. This situation is main feature of the socialist system (Güvemli, 2001).

In the scope of audit in Russia the audit and the auditor concepts were first time used at the period of ruling of Tsar Petro I (1682-1725). During this period, there were generally developed new legal regulations relating the government accounting system. In addition, the abutment for these legal regulations was Western European countries. By means of aforesaid regulations the government aimed to increase the budget revenues and to conserve the assets (Pekdemir and Akgün, 1999).

As mentioned above, with The Bolshevik Revolution (October, 1917) the Czarism period has ended up and The Soviet Union period has begun. At the same time, all institutions controlling the economic activity of enterprises officially have passed into operation. Audit is implemented by the authorized government institutions and by various civil society organizations established by people and officially approved by the government. And especially, after World War II the excessive power of the government administration and the level of private enterprises at a scarcely low amount, made the formation and improvement of the auditor profession become unfeasible (Ayanoğlu, 2004). Briefly, the economic development of the countries leads to the establishment of laws and the significant social relations are arranged according legal rules taking part in legal regulations. In this context, with the historical development of audit in Russia the direct relationship is seen between the legal regulations. These stages can be broadly examined as herein below.

2.1. First Stage (Period between the Years 1987-1993)

At the first period while on one hand the establishment rule of auditing firms was dominating, on the other hand the formation of audit activities (for example; education of personnel, the issuance of the first certificate and licenses) of non-coercive character was envisaged. The resolution of Council of Ministers of the USSR No. 1033-245 from the 08.09.1987 of relating “The Establishment of Soviet Audit Company” enabled the setting up of joint-stock company “Inaudit”. The capital of the Company was assessed as 800.000 Roubles, while the shares of major shareholders as the Ministry of Finance (55 %), Ministry of Foreign Trade (10 %), USSR State Bank (5 %) and other government agencies (5 %) respectively. Joint-stock company “Inaudit” together with the qualified personnel despite both domestic and overseas services, in 1992 after the sale of shares by the shareholders the company was split into several independent companies. Following these events occurred a great need in establishment of audit standards and standardization of audit for the future its advancement (Losyeva and Prokhorov, 2013).

2.2. Second Stage (Period between the Years 1993-2001)

Framed by means of resolution No. 2263 from 22.12.1993 “The Interim Regulations on Audit Activity” has launched a new phase in development of audit (Nalyotova and Slobodchikova, 2005). By means of this regulations in Russia was established the legal basis for execution of audit as independent fiscal control (Sheshukova and Gorolilov, 2005). The regulations had taken in to their scope the control of audit activity, the penalties applied in case of violations of laws relating audit and the explanations concerning the obtaining the license. In order to perform the quality control of audit activity there was formed “The Audit Committee” at The Ministry of Finance. Right after has been begun the creation of associations combining the auditors and audit companies upon their own request. These associations have been obliged to perform the inspections regarding whether their members were operating in accordance with the legal regulations and occupational standards. Nevertheless, the high membership fee and lack of work in professional fields has left the whole efforts towards the creation of professional organizations inconclusive. By the year 2000 insufficiency of inspections implemented by both state and professional organizations led to the degradation of the audit quality. With the intent to eliminate the situation causing a great insecurity, in 2000 the department of control and audit at the Ministry of Finance has been commissioned to control the activity of all auditing companies and auditors operating in Russian Federation. Strengthening of the government control in the audit scope has necessitated the legal regulations regarding the audit (Yudina and Chernikh, 2005).

2.3. Third Stage (Period between the Years 2001-2008)

On 07.08.2001 “Law on Audit Activity” entered to force. According to this law, Ministry of Finance in order to realize the control of audit activities in country has been authorized to perform the duties listed below (Yudina and Chernikh, 2006):

- Make regulations within the limits of their powers,

- Carrying out activities towards the preparation of audit standards,

- Conduct systematic work concerning permits and licensing procedures and trainings,

- Perform the control over procedures relevant to the licensing conditions and demands of companies and auditors (Ivanova, 2009).

- Control the audit companies and auditors whether they comply to the audit standards while conducting their audit activity,

- Determine the conditions concerning the audit activities for the audit companies and auditors,

- Record the data relating the all audit companies and auditors into the state registration system and to provide it to the person interested.

- Make the accreditation of professional organizations (Suyts, 2007).

According to the “Decree on Government Regulation of Audit Activity in Russian Federation” No. 80, adopted on 06.02.2002, the authority to regulate and control the audit activities has been given to Ministry of Finance. Under the arrangements in the Principal Law, according to the resolution No. 47 from the 03.06.2002 the “Board of Supreme Control” to be operating in dependence of the Ministry of Finance was established and started actively to perform its duty. The Board has been assigned with abroad authority to participate actively in works of revising the auditing standards, to control the quality of audit, to monitor the innovations in audit area and to adopt them to the Russian conditions. Nevertheless, according to the resolution No. 38 the interim arrangements have been made for organization and coming into operation of “The Auditors Chamber”. Extensive powers were granted to the Auditors Chamber especially concerning the execution of the procedure relating to the receipt of auditing certificate and authorization documents for conducting of audit, organization of the examinations, retrieval of documents and control of the audit quality (Ayanoğlu, 2004).

In year 2001 with the enactment of mentioned Law, studies towards the preparation of audit standards in compliance with the international standards were initiated. On 23.09.2002 by the resolution of “Consent on Audit Standards” six “National Audit Standards” were prepared. As during the time while the Law has been in effect, thirty-four “National Audit Standards” were prepared and introduced into application. Russia launched studies over the harmonization of audit standards with “International Audit Standards”. If the Ministry of Finance makes the compliance to the audit standards compulsory, then Russia would one-step ahead in independent audit area.

Moreover, the other important progress concerning audit at mentioned period on 28.08.2003 was the preparation by the Ministry of Finance of “Codes of Conduct” in a way compatible with international standards.

Summarizing; while the auditing activity rules have been settled in Russia by Federal Interim Law No. 2263 (Interim Law) on the 22.12.1993, on 07.08.2001 by the entry into force of Main Federal Law No. 119 (Main Law) relevant to the Audit Activity has been regulated on 09.09.2001. Main Law, has replaced the Interim Law and launched the new era in auditing field in Russian Federation (Ayanoğlu, 2004).

2.4. Forth Stage (Period between the Years 2009-2014)

By the entry of the “Law on Audit Activityˮ No. 307 from 30.12.2008 into force on 01.01.2009 began a completely new period under the control of auditing activities. The Law aims the abatement of government role in control of auditing activity. For realization of this purpose several non-profit organizations as “Association Self-regulatory Organization of Auditorsˮ have been established. Since 01.01.2010, any auditing company and auditors not members of any of those associations cannot perform the auditing activity in Russian Federation (Golubeva, 2011).

During this period, nine new national standards were prepared in Russia in accordance with international standards; thereby former five standards have lost their validity. Nowadays, there are thirty-eight auditing standards guiding the auditors in the implementation of audit activities in Russian Federation. Furthermore, with the purpose of improvement of the parts related with responsibilities and competitive conditions for auditors taking part in, Codes of Conduct were prepared by the Ministry of Finance in 2003, standardization has been executed and on 22.03.2012 “The new Code of Ethics” was prepared.

Besides the studies towards the reduction of government control in audit field, the authorization given also to the Ministry of Finance causes controversies in today’s Russia. In other words, the feasibility to execute the control of auditors and audit companies by both the Self-regulatory Organizations of Auditors and the Ministry of Finance brings about the hesitations relating the issue whether the government trusts the self-regulatory organization of auditors. Nowadays, there are five Auditor’s Associations of Self-regulatory Organizations, operating in Russia. Studies on formation of unions are held towards improvement of self-control, increasing co-operation between companies and the solution of common problems (Sheremet, 2014). In consequence of the studies, performed in this aspect it is anticipated that later on self-control will be improved and number of members attending into association of self-regulatory organization of auditors in audit will increase. Subsequently periodic examination of audit and audit process, there could be given a place to the study towards the country’s auditing mechanism now.

3. RESEARCH ON AUDIT IN RUSSIAN FEDERATION

In this part of the study oriented towards the determination of the operability of the audit mechanism, a descriptive statistical research and its results will be mentioned.

The aim of the research is to determination of how and at what degree are audit mechanisms effective in the Russian Federation. In this context the research involves; number of auditors and audit companies in Russia, auditing companies according to the service capacity, number of audit companies members of association of self-regulatory organization of auditors, number of companies being audited, the regional distribution of audit companies, operational year, revenue structure.

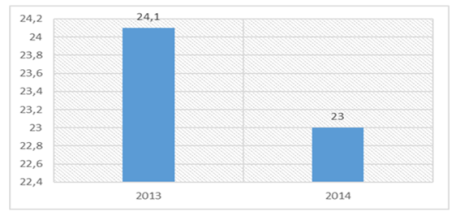

The two periods are taken as a basis in the research. These periods are years 2013 and 2014. The main reason of selecting those two periods is that they are fiscal years and the possibility of comparison between two periods. Despite the accessibility of certain data, inaccessibility of some other data mentioned as an issue of the research for previous few years takes place among the constraints of the research. Research involves a web-based application via the Internet. Research data, was obtained using the official web page of the Russian Federation and the Ministry of the Russian Federation Chamber of Auditors. According to the subject of the study, the findings and evaluations regarding to the data of years 2013 and 2014 can be examined in as follows. Quantitative findings related to the audit companies and auditors in Russian Federation can be presented as in the Table 1.

Table-1. Distribution of audit companies and auditors in Russian Federation according to years 2013 and 2014 (thousand)

| Audit Companies and Auditors Number | 01.01.2013 | 01.01.2014 |

| Audit Companies | 4,8 | 4,7 |

| Independent Auditors | 0,9 | 0,8 |

| Total Number of Authorized for Audit | 5,7 | 5,5 |

| Total Number of Auditors | 24,1 | 23,0 |

Source: http://www.sroapr.ru/official/3906/, 25.06.2016.

When observing Table 1 it seems to be even a little decline in the number of audit firms and auditors in 2014 year compared to 2013 year. While the number of audit companies in year 2013 was 4,8, it decreased to 4,7 in year 2014, the number of independent auditors in year 2013 has decreased from 0,9 to 0,8 in year 2014, totally from 5,7 in 2013 to 5,5 in 2014; and decreased by the number of auditors from 24,1 in 2013 to 23 in 2014. As a primary reason for this decline, the increase in expectations and demands related to the quality of audit service.

By the present year, while the number of companies authorized for auditing activity increased from 6,1 in 2011 to 6,2 in 2012, and for the both of this two years the 5,2 of the total number of this companies were audit companies. In the previous year 2011, while the total number of auditors was 26,3 thousand, in year 2012 it became 26,8 thousand. And by the essential years of the study those numbers have decreased. And the tendency of auditors towards the area with higher revenue, retirement and the decrease in success rate of auditors due to the complication of certificate examination can be shown as a reason for this decline (Cheremisina, 2014). And by the end of the year 2014 it is known that the number of auditors authorized for implementation of the auditing has decreased to 5,3 and the number of auditors has decreased to 22,2 thousand. Observed that the audit companies close before The Ministry of Finance and the Association of Self-regulatory Organization of Auditors begin to the audit. The high competition and dumping environment causes diminish in revenue of audit activity and as a result, the audit companies are closed.

New legal regulations in Russian Federation caused some amendments in the criteria of audit activity. After 01.01.2011 companies that will be subject to inspection have been reclassified and income limit for these companies (50-400 million roubles) and balance sheet assets amount has been increased to (20-60 million Russian Roubles) (Mamayeva, 2012). The implemented amendments have caused a decline in the number of companies and consequently caused a decrease in volume of services. In this context, the distribution of the auditing companies according to the volume of services can be demonstrated in the Table 2.

Table-2. Distribution of the auditing companies according to the volume of services in Russian Federation by years 2013 and 2014 (%)

Volume of Services of the Auditing Companies (Million Roubles) |

Share of Auditing Companies in Total Sum | Share of Auditing Companies in Total Auditing Report | Share of Auditing Companies Services in Total Amount of Services | Volume of Services of the Auditing Companies (Million Roubles) |

Share of Auditing Companies in Total Sum | Share of Auditing Companies in Total Auditing Report |

| 2013 | 2014 | 2013 | 2014 | 2013 | 2014 | |

| Under 1,5 | 41,0 | 40,1 | 12,3 | 12,0 | 2,4 | 2,2 |

| 1,5-3,0 | 21,2 | 20,5 | 15,2 | 14,2 | 4,1 | 3,8 |

| 3,0-9,0 | 25,4 | 26,4 | 30,4 | 29,7 | 11,7 | 11,5 |

| 9,0-70,0 | 11,3 | 12,0 | 27,5 | 29,4 | 19,5 | 20,1 |

| 70,0-150 | 1,0 | 1,0 | 11,9 | 11,2 | 23,1 | 21,7 |

| Over 1.500 | 0,1 | 0,1 | 2,6 | 3,5 | 9,1 | 40,7 |

Source: http://www.sroapr.ru/official/3906/, 25.06.2016.

As one can see in Table 2, in general the auditing companies, according to service volume have decreased in the year 2014 when compared with year 2013.

In contemporary conditions, the negative macroeconomic situation also negatively affects the auditing field. For example, according to the data of Central Bank the capital outflow in year 2013 was 59,7 billion $, and 63 billion $ in the first half of the year 2014, industrial production index in April 2014 would be detected as 2,4 %. And the average GNP growth rate between years 2015-2017 was 2,5 %. Complex macroeconomic situation, increasing the quantitative criteria, pertaining to the audit and the reduction in capital market transactions caused a decrease in the number of audited company (Anokhova and Paramonov, 2014). In addition, the tendency of companies not to implement audit service and irresponsibility shown in this direction was another factor affecting the decrease in the number of companies under audit. According to data released by the Ministry of Finance by the years 2013 and 2014 in Russian Federation numerical distribution of companies under audit is as in Table 3.

Table-3. Distribution of companies under audit in Russian Federation according to years 2013 and 2014

| Year | Moscow | St. Petersburg | Other Regions | Russia in Total |

| 2013 | 26.773 | 6.271 | 35.336 | 68.380 |

| 2014 | 27.810 | 5.963 | 34.084 | 67.857 |

Source: http://www.minfin.ru/ru/perfomance/audit/audit_stat/, 27.06.2016.

The number of companies in years 2013 and 2014, while demonstrating a decline in St. Petersburg and other Regions and in total has shown a rise in Moscow. It is known that also similar results had been in previous years.

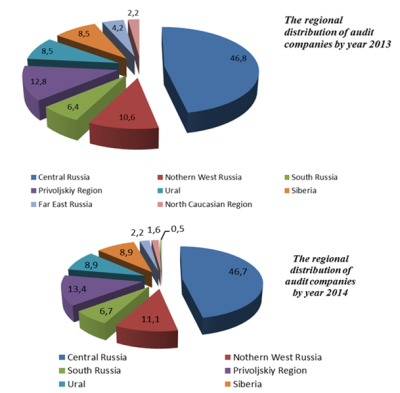

The information relating the regional distribution of audit companies and auditors take place in the Figure 1.

Figure-1. Regional distribution of audit companies in Russian Federation in years 2013-2014

Source: http://www.minfin.ru/ru/perfomance/audit/audit_stat/, 27.06.2016, (Figure was prepared by authors).

As it can be observed from the diagram; from the data relieved on the site of Ministry of Finance of Russian Federation the major part of audit companies in 46,8 % in year 2013 and 46,7 % in year 2014 are operating in Central Russia. The reason of auditing companies to prefer the central regions is the operation of all major financial centres in this region. While audit companies in year 2013 was 12,8 %, it increased to 13,4 % in year 2014 in Privoljskiy Region. Audit companies have increased from 10,6 % to 11,1 % in North West Russia, from 8,5 % to 8,9 % in Siberia and Ural, from 6,4 % to 6,7 % in South Russia in the year 2014 when compared with year 2013. Conversely, audit companies have decreased from 4,2 % to 2,2 % in Far East Russia, from 2,2 % to 1,6 % in North Caucasian Region. Add to this, has occurred rate of 0,5 % in Crimea. By this data, it also can be considered that other regions are not active enough in audit market.

“The Law on Audit Activityˮ also brought about significant changes in the requests concerning the auditors. Those changes involve demands like membership in “Auditor’s Association of Self-regulatory Organization” and the obligation of training in audit companies. In addition, in law were made amendments concerning the rules and examination requirements related to the receipt of the auditor's certificate, the conditions were complicated. Auditors, which are not certified according to the new rules from 01.01.2012, loose the right to perform audit activity (Mamayeva, 2012). Consequently, the number of members of Association Self-regulatory Organization of Auditors can be shown as in the Figure 2.

Figure-2. The number of members of Association Self-regulatory Organization of Auditors the in Russian Federation by years 2013 and 2014

Source: http://www.minfin.ru/ru/perfomance/audit/audit_stat/, 27.06.2016 (Figure was prepared by authors).

According to the data released at the site of Ministry of Finance of Russian Federation, the quantity of Association of Self-regulatory Organizations of Auditors decreased in 2014 when compared with 2013. Even if it is slight, the decline can be seen at the Figure 2.

When the data for previous years is examined this rate that was 26,3 % in 2011 has increased to 26,8 % in 2012. However, after year 2012 as it can be observed from the Figure 2 that in the number of companies, members of Associations that Self-regulatory Organizations of Auditors has been seen a decline. That is obvious that this decline has been affected by the decrease in the number of audit companies registered since 2012. Several not operating companies had been registered before the Law came into force. By the amendments that had been brought by the Law, when the activity of companies that were not able to receive the new certificate was ceased, in the number of this companies had been decreased.

It is known that in 2011 and 2012 the number of companies that are operating for 5 years and more is over 70 %. But in 2013 there had been observed a significant decrease in the number of one or two operating companies. The reason for this can be inferred the complication of market conditions and the close up of the companies established in years 2011 and 2012 by losing of the competitiveness. We can state that the number of companies with the period of activity over 5 years has risen from 2011 and this is based upon the market stability (Sheremet, 2014).

In this context, according to periods of company activity in years 2013 and 2014 companies are as in the Table 4.

Table-4. Distribution of the auditing companies according to activity period in Russian Federation by years 2013 and 2014 (%)

| Year of Audit Activity | The Share of Audit Companies in Total Number (%) | Year of Audit Activity |

| 2013 | 2014 | |

| Less than 1 year | 3,5 | 4,8 |

| 1-2 years | 7,2 | 6,8 |

| 3-4 years | 11,9 | 9,7 |

| Over 5 years | 77,4 | 78,7 |

Source: http://www.minfin.ru/ru/perfomance/audit/audit_stat/, 27.06.2016.

When the Table 4 is examined, it can be seen that the number of companies established during one year, compared with year 2013 has demonstrated an increase in 2014. This indicates that the new established companies do not avoid the ascending demands relating the quality of audit and the strict external audit. Similarly, the number of companies with the period of activity over 5 years increased.

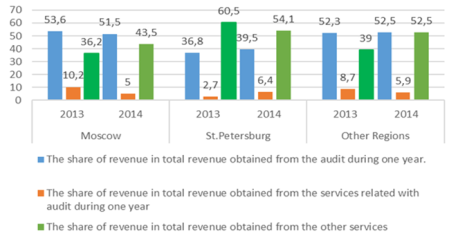

In the labor market of today’s Russia can be observed the disequilibrium between the high demands and the low qualification. The excess of the audit burden and low wages affects the motivation of employees negatively. Generally, due to the decline in the audit market the exhaustion of the resources of companies for increasing the wages causes the loss of employees. In addition, due to the complication of receiving the certificate, less number of auditors passes successfully the proficiency examination. Condition of working in an audit company at least for three years in order to obtain the right to take the examination, obstructs the entrance upon this area for those who will chose this career. In other words; low wages high demand and a heavy workload constrains the motivation of the ones, who is will choose the profession to enter the audit area and alienates the employees from the job (Paramonov, 2014). In this context, the regional revenue structure of audit companies that operate in Russian Federation can be demonstrated as in Figure 3.

Figure-3. The regional distribution of audit companies’ revenue in Russian Federation by years 2013 and 2014

Source: http://www.minfin.ru/ru/perfomance/audit/audit_stat/, 27.06.2016, (Figure was prepared by authors).

As it is seen from the Figure 3, according to the data released at the web site of the Ministry of Finance of Russian Federation, it is observed that the income obtained from the audit service in Moscow has decreased in 2014 in comparison with year 2013 and has increased in St. Petersburg and the other regions. The point of matter is that the income obtained from the services concerned with audit in Moscow has decreased in 2014 in comparison with the year 2013, and has increased in St. Petersburg. There is an increase observed in income acquired from other services in Moscow and the other regions in 2014 in comparison with year 2013 and a decrease in St. Petersburg.

As a reason for the decline in the revenue from the audit implemented in Moscow, the loss of customers of small companies in consequence of changes introduced by law and application of price reduction method for gaining new customers can be shown. It can be stated that the decline in the income related with the audit services both in Moscow and in other regions in contrast with the mandatory audit consultancy services is oriented on public interest and concerned with the governmental incentive (Mаkhonina, 2012).

4. CONCLUSION

In this paper, firstly, the development of audit in Russian Federation was examined periodically in stages and then there was given information about legal regulations in the country. Main Law replaced the Interim Law related to auditing. In this context, Main Law created the new era in auditing in Russian Federation. Nowadays, “Association Self-regulatory Organization of Auditors ˮ in Russian Federation are critically important matter for auditing. The decision oriented on reducing the government control in audit field, formed “Self-regulatory Organization Associationsˮ, the non-conformance between the assignments concerning with the control of the audit by the Ministry of Finance with the authorization issued to this association effects the audit activity in country in negative way. Therefore, for the improvement of audit in Russia is necessary to provide compliance between Ministry of Finance and “Self-regulatory Organization Associations ˮ. Also the enhancing the efficiency of Self-regulatory Organization Associations will be a factor accelerating the development of audit. Attaching importance to the issues like maximizing the internal control in associations, the obligatory rotation of the management, giving account to the members and more of the same will bring transparency and provide the efficiency.

Also in this study; it was determined the role and the importance of audit in nowadays Russian Federation and the main indicators of 2013 and 2014 years about functioning of audit mechanism were investigated. According to the research findings and evaluations, the number of audit companies and auditors, the volume of services of auditing companies, the number of member of Association Self-regulatory Organization of Auditors in 2014 year compared to 2013 year seems to be decreased. Conversely, it increased periods of company activity. The major part of audit companies is operating in Central Russia. However, the income obtained from audit service decreased.

In order to take precaution against the facts like low income and auditor’s price reduction policy that negatively affect the audit activity, the need of determination of attributed payment rate appropriate to the audit is obvious. Therewith detecting by the relevant institutions the facts that lead to unfair competition and the introduction of disincentive applications in this respect will provide the solution together with this.

There is a need to prepare the programs that would attract young personnel, provide the necessary conditions, not preventing their working order to dispose the shortage of personnel encountered in the audit field. Execution of studies towards the enhancing the reputation of auditor profession would facilitate the resolution of problems in the audit scope. In addition, it is considered that the introduction of titles like ‘Honorary Auditor’ and ‘Senior Auditor’ in Russian Federation would be impressive in increasing the value of the profession.

Consequently, this paper with research can add value for accounting literature.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Anokhova, E.V. and A.V. Paramonov, 2014. Features of development of the market for audit services in Russia. Journal of Аuditor, 8: 40-49.

Ayanoğlu, Y., 2004. Developments in audit area in Russia. Journal of Accounting and Auditing Perspectives, 4(12): 15-28.

Cheremisina, S.V., 2014. The development of audit in Russia. Journal of Problems of Accounting and Finance, 4(16): 48-51.

Golubeva, S.G., 2011. Basic tendencies of development of audit in Russia. Journal of Dairy Farming, 4(4): 51-54.

Güvemli, B., 2010. The development of accounting thought in Soviet Union Era (1917-1953). Journal of Accounting and Finance Academicians and Research Association, 10(48): 241-251.

Güvemli, O., 2001. Turkish state accounting date: XX Eepublican Era. Istanbul: Avcıol Publication, 4.

Ivanova, N.U., 2009. Elements of audit. St. Petersburg: Academy.

Losyeva, N.А. and I.V. Prokhorov, 2013. Formation and development of audit activities in Russia. Journal of Auditor, 9: 16-21.

Mamayeva, G.K., 2012. Impact of legislative innovations on the current state of audit services market in Russia. Bulletin of OrelGAU, 3(12): 131-135.

Mаkhonina, I.N., 2012. About the state and prospects of development of the financial audit in Russia. Journal of Socio-Economic Phenomena and Processes, 9(043): 92-99.

Nalyotova, I.А. and Т.Е. Slobodchikova, 2005. Аudit. Моscow: Publication of Forum Infra-М.

Paramonov, А.V., 2014. Audit market in 2013 and its problems. Rating of audit companies. Journal of Auditor, 4: 32-38.

Pekdemir, R.F. and V.K.L. Akgün, 1999. The development of accounting and auditing profession and accounting practices in the Russian federation. Journal of Accounting Academicians and Solidarity Foundation Accounting Science World 1(3): 61-79.

Peker, A., 1996. Accountant’s overview on the Asian Turkish Republics. Bulletin of Accounting Academicians and Solidarity Foundation, 2(4): 12-13.

Sheremet, А.D., 2014. A brief analysis of the current state of self-regulation institute in Russia. Journal of Auditor, 9: 24-27.

Sheshukova, Т.G. and М.А. Gorolilov, 2005. Audit: Theory and practice of application of international standards. Moscow: Finance and Statistics, 2.

Suyts, V.P., 2007. Audit. Moscow: Higher Education.

Yudina, G.А. and М.N. Chernikh, 2005. Theoretical, organizational, legal and methodological basis of the audit. Krasnoyarsk: KrasGASA.

Yudina, G.А. and М.N. Chernikh, 2006. Fundamentals of the audit. Moscow: KRONOS.

BIBILIOGRAPHY

http://www.minfin.ru/ru/perfomance/audit/audit_stat/. [Accessed 27.06.2016].

http://www.sroapr.ru/official/3906/. [Accessed 25.06.2016].

| Views and opinions expressed in this article are the views and opinions of the author(s), Asian Journal of Economic Modelling shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |