STRATEGIC ENTERPRISE MANAGEMENT FOR INNOVATIVE COMPANIES: THE LAST DECADE OF THE BALANCED SCORECARD

1Department of Engineering Management, Marmara University, Istanbul, Turkey, 2Faculty of Engineering, Department of Electrical and Electronics Engineering, Marmara University, Istanbul, Turkey, 3Faculty of Engineering, Department of Industrial Engineering, Marmara University, Istanbul, Turkey

ABSTRACT

Setting corporate vision, strategy, and associated unit-based strategic goals are crucial for any company to create and to sustain the competitive advantage. This concept has been frequently discussed in theory and practice. The case is no different from the innovation perspective of enterprises. Therefore, this article is aimed at exploring the integration of balanced scorecard into innovative strategic management, providing a framework of interrelated issues based on the existing literature and application areas in this research field. Along with the brief review of innovation based strategic management, which includes 13 peer reviewed journal articles; 8 book chapters, 41 peer-reviewed scientific journal articles, including a content analysis, was conducted to show the last ten years of the balanced scorecard approach from the innovation perspective. The literature review revealed that: (1) the number of related publications on the topic is showing similarity over the last few years; (2) the explored research field has been mainly grounded on balanced scorecard research, but has also been enriched by innovation perspective; and (3) there are wide range of industry applications based on innovation conducted for the balanced scorecard approach. The literature review provides a summary of the most important issues that emerged in this field which can shed lights on the new opportunities and challenges for further research.

© 2017 AESS Publications. All Rights Reserved.

Keywords: Literature review, Balanced scorecard, Strategic management, Innovation, Strategy, Performance.

Received: 1 June 2016/ Revised: 15 June 2016/ Accepted: 22 July 2016/ Published: 15 August 2016

Contribution/ Originality

This study documents a review of different approaches of the balanced scorecard for strategic decision making in the last decade.

1. INTRODUCTION

Flexibility to be one step ahead of changes in customer requirements is crucial for any company to sustain competitiveness. Having high innovation capability and being innovative is a precondition for industrial organization to be flexible in order to meet the expectations of customers. However, innovation initiatives bring some substantial risk and challenges. Tough and rapidly increasing global competition, decrement in product life cycle, higher expectations on personalized product demand, and quickly changing business environment can be listed as some complex challenges that companies face with. The capability to acquire and install innovative processes, procedures, and formations are vital requirements in order to overtake the global competition (Kohl, 2016).

In this difficult competitive business of today, many companies handle the idea of innovation as an essential tool for gathering the advantage in competition. Given the reason, many organizations give large amounts of importance to the concept of innovation management. Companies consider their customers, stakeholders, complementarians, suppliers and other partners as source of innovation. They prefer to build their innovation strategy based on the information gathered from recommendations, thoughts, offers and suggestions from their internal and external stakeholders. Prior to the decision on the needs to initiate innovation, companies discover opportunities in market and deliver required materials and information that leads knowledge creation. To be successful in creating the innovation, organizations aims to organize and manage these processes effectively and maximize their innovation potential (Lendel et al., 2015). Strategic management of innovation, is the beginning of new system, procedures, structure and applications within a company that directly effects the performance and competitiveness of organization (Walker et al., 2015). Therefore, an effective strategic enterprise management that focus on innovation, is crucial for innovative companies in order to sustain the growth in tough conditions of competitive business environment.

The rest of the study is organized as follows, section 2 is a brief review on strategic enterprise management and business innovation. The balanced scorecard, and its implementation areas are discussed in section 3. It is then followed by the conclusion and the bibliography.

2. BRIEF REVIEW ON STRATEGIC ENTERPRISE MANAGEMENT AND BUSINESS INNOVATION

Many researchers studied on strategic enterprise management and its effect on innovation creation. Besides, there are many studies encountered on the importance of innovation and its influences on companies’ performance and outcome. Carmeli et al. (2010) analyses the importance of innovation leadership for a firm and how it supports the firm to change and adapt its external environment as well as to improve its performance. They also examine the positive effects of strategic fit between the firm and its external stakeholders to enhance business performance. They utilize the collected data from 117 different companies and the results points that, innovation leadership combined with strategic fit have positive effects on competitiveness and performance of the company.

In his study, Prajogo (2016) research the effects of different business environment on various types of innovations that leads the business performance. Two role business environment; dynamic business environment, and competitive business environment are taken under consideration. The data collected from 207 Australian manufacturing companies is utilized in this survey and both theoretical and practical inferences are discussed in detail. Kohl (2016) propose a new evaluation system for innovation initiatives companies in manufacturing business. In the study, the introduced system is named as integrated evaluation system and evaluation of innovation integrated evaluation system that deal with the gaps known in existing approaches.

In the research conducted by Planko (2016) in order to commercialize sustainability innovation, a strategy framework for collective system building that include four key areas are proposed. These areas are; development and optimization of technology, creation of market, coordination, and socio-cultural changes. The theoretical analyses are supported with an empirical case study in the Dutch smart grid area.

Lendel et al. (2015) propose a handy tool for managers which include a series of instructions in order to support them to managing innovation processes. They built this handy guide according to theoretical scientific research as well as empirical research results. This recommendation set guide to managers about how they can effectively plan innovation processes, how to manage innovation tasks and activities, and how evaluate and monitor the results and objectives of innovation.

In the research paper of Bouhali (2015) authors focus on the leadership roles for effective innovation management. The differences and matches of strategic planning and strategic thinking in organizational management and their effects on innovation are introduced. The study presents leadership roles integration for innovation based on strategic thinking and strategic planning by pointing out substantial distinctions and connections between them.

Lopez-Nicolas and Merono-Cerdan (2011) emphasis on the knowledge management strategies and its influence on innovation capacity as well as the overall performance. The empirical study based on the data collected from 310 organizations in Spain shows that, companies are not informed about the results and implications of knowledge management. Another important inferences of this study are both codification and personalization of knowledge management strategies and its direct and indirect impacts on either organization’s innovation creation or business performance. Moreover, the research of Sołoducho-Pelc (2015) signifies the importance of strategic management in order to use the opportunities come with changes are examined. The study emphasis on strategic management processes that leads preparation before occurring changes and search for new growth opportunities. In this research, the strategic management processes which should be applied in order to be prepared before changes occur and use the opportunities of changes by finding new development fields and starting new creative innovation. A formulation of the strategy is proposed which include long-run development plan including wishful growth priorities and search of opportunities that initiates innovation by using the advantage of the contribution of business partner.

Yıldız et al. (2014) focus on the innovation creativity and leadership roles to investigate its effect on the performance of the organization. They claim that the innovativeness and leadership have substantial impact on success of business. Their results yield an alteration with respect to size, location, sector and other factors. The study is supported with a case study that consists of a questionnaire completed with 576 employee working in different companies, industry sectors, and service sectors in Istanbul. The transformational and transactional leadership roles are considered in this survey. Results obtained from this survey shows that, even there are many other factors that influence business success of a company, a strategic leadership management and innovativeness have crucial positive effects on company performance.

In their research about strategic thinking and business innovation, Calabrese and Costa (2015) directs the focus to another innovation intellectual foundation that is strategic thinking of leaders. They underline the difficulties of creation of business innovation and the path started from leader’s strategic thinking ended with business innovation is complex and not easy. A theoretical model labelling strategic thinking rely on Peirce’s theory of abduction is proposed. What’s more, the contribution of enterprise systems and digital platforms to organizational innovation processes are discussed in the article of Sedera (2016). They examine the positive effects of effective usage of digital platforms and successful enterprise systems to attain business innovation by utilizing technological advances. The data collected from 189 organizations that are used in order to clarify the relationships between effective usage of information systems and success of innovation creation on business performance. Finally, the study of Apak and Atay (2014) is worth to mention due to a conducted survey on global innovation and knowledge management in small and medium size firms of Turkey and Balkan countries. They point that; in today’s rapidly changing business environment; in order to be flexible and adaptable to changes; and to take advantage of competitiveness, innovation management is becoming one of the most crucial factors. Enterprises are required to set their strategies wisely and measure their performance effectively to reach the mentioned success in innovation management. Balanced Scorecard is generally considered as the most powerful tool to measure the performance of innovation management.

3. THE BALANCED SCORECARD APPROACH

The main goal is to reach competitive advantage. In their earlier works in gaining the competitive advantage Prahalad and Hamel (1990) discussed the roots of it with comparisons of Canon and Honda with Xerox and Chrysler within the time periods from 1980 to 1988. Their work stated that the difference and cooperation of Western and Japanese systems to consolidate competencies to generate products that could enhance the business towards the generation of multiple end products. Their work later introduced in the book of Schilling (2013) with questions to test the firm’s core competencies such as significance, range, simple imitation.

Although identification of core competencies and dynamic capabilities of a company are generally considered as a key in terms of agility and responsiveness for a solid kick, a success towards the innovation cannot be reached without the top level commitment. With the commitment given by the top-level management, firm’s strategic direction can be set. Afterwards, the real question turns out to be the correct way of setting relative targets in relation to the measuring such targets.

The most efficient performance measurement system is developed by Kaplan and Norton (1996) named balanced scorecard -mostly referred as BSC. Although the balanced scorecard was first used to make noteworthy changes in the performance improvements, it was later expanded from the business environment to government and non-profit sectors.

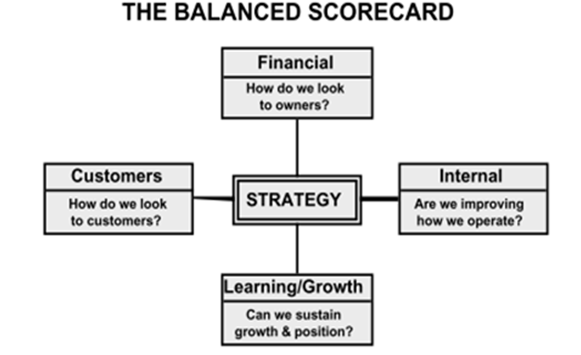

In the last decade, several book chapters are included in the literature. Frost (2007) briefly explained the popularity of this measurement tool by mentioning its influence on Forbes 500 companies. The chapter also discussed four traditional performance measurement categories -Financial, Internal Processes, Customers, and Learning & Growth- to address the metrics that are covering the strategy as shown in Figure 1.

Figure-1. The Balanced Scorecard - (Frost, 2007)

Source: Frost (2007)

Although the BSC developed by Kaplan and Norton (1996) for a strategic planning associated with the vision and vision-paralleled strategy of the organization, Jacobsen (2011) introduced a non-conventional methodology named “The Real Balanced Scorecard”. The work is aimed to fit the concept into environmental and social performances along with the financial improvement aspects. Hence, it is aimed to extend the traditional framework to nonfinancial performance measurement systems.

Gulati (2013) is another author to address the balanced scorecard as a performance measurement tool. Apart from the earlier discussed four perspectives, he pointed that the developed metrics, collected data, and analyze phase of such perspectives should not include any bias. The chapter includes detailed discussions in terms of maintenance and reliability for each perspective of the balanced scorecard.

The balanced scorecard is also introduced in the handbooks of American Society for Quality (ASQ). In the Certified Manager of Quality/ Organizational Excellence Handbook, it is indicated that the key measurements of the BSC should be selected cautiously in each segment as the organization can only benefit from intelligent and confident decisions to receive the desired output (Westcott, 2014). The latter handbook – Certified Six Sigma Green Belt- that is published in 2015, introduced the Balanced Scorecard as one of the 9 key quality approaches over the years by mentioning its benefit for monitoring outcomes in the key management areas of an organization (Munro et al., 2015). Their study also refers the BSC as a key translator of the organization’s vision and strategy into actions if it is deployed in full manner. Munro et al. (2015) also states that the commonly used brainstorming activities to set sound metrics for the balanced scorecard may not always yield successful outcomes.

The work completed by Pasman (2015) referred the balanced scorecard as one of the risk management tool in risk-based economic decision making in gas, oil and chemical industrial processes. The study discusses that the organization’s best direction could be determined with theoretical methods and practical tools for decision making since systems include plenty of inputs.

What’s more, AMACOM, Book Division of American Management Association introduced the balanced scorecard concept in financial decision making and analysis techniques. According to the study, implementation of the strategy through the BSC is helping it to its evolution in terms of technological changes and competitiveness. (Sherman, 2015).

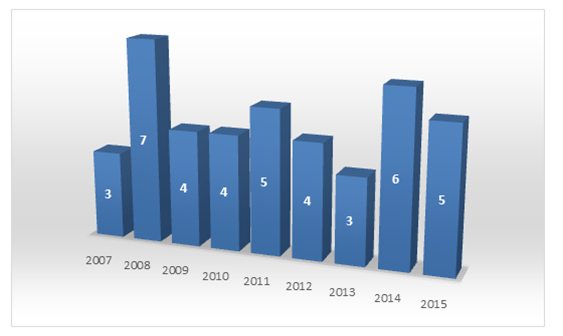

Although the use of balanced scorecard was gathering increasing importance, Voelpel et al. (2006) approached critically towards the key problematic effects over the 1996 - 2006 time horizon to suggest future directions. Their study offered an alternative to the balanced scorecard with the inclusion of a systemic scorecard for the innovation economy. The idea of the systemic scorecard is often associated with a dynamic shift towards different industries and business units. On the other hand, the balanced scorecard is applied in wide range of industries and business sectors. The last decade of the innovative approaches on the balanced scorecard are introduced in the later stages of this study as summarized in Table 1. As it is indicated in the table, the last ten years of the balanced scorecard is divided into eleven categories as information systems and knowledge management, Finance and management accounting, R&D and new product development, tourism, construction, medical & health care, method specific (Artificial Neural Network, Analytic Hierarchy Process), corporate social responsibility & sustainability, real estate, social services, and manufacturing. In figure 2, yearly distribution of those articles are shown.

Table-1. Application Area of the Balanced Scorecard in the Last Decade

Figure-2. Yearly Distribution of the articles

3.1. R&D and New Product Development (NPD)

Since the implementation of the company strategy and its objectives may cause problems in R&D activities and new product development -this is commonly happening due to its high cost structure and volume- setting different goals for R&D activities are necessary. Garcia-Valderrama et al. (2008) introduced a general BSC model within this context. The proposed BSC model for R&D is tested with management experts of the related field. It was found that the proposed model is valid with the best indicators for organizational effectiveness. Garcia-Valderrama et al. (2009) later took it to the next level with the case analysis of 90 different companies for the application of data envelopment analysis to investigate the interrelations of BSC perspectives for research and development purposes. In Bigliardi and Dormio (2010) used literature analysis, Delphi technique and case study in their study for developing a balanced scorecard for R&D performance measurement. Authors found that the BSC model is suitable for research and development and could be used for testing large number of companies that are operating in R&D field.

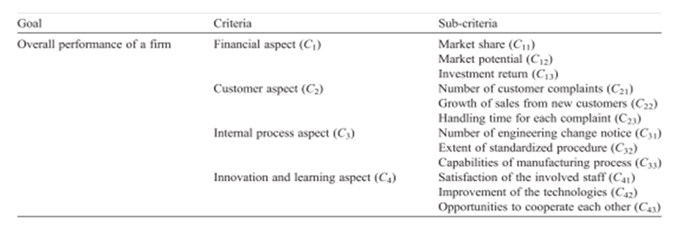

Apart from the conventional perspectives, there are also several non-traditional perspectives of the BSC exist in the literature. The study of Chen (2008) worth to mention. It has associated the BSC with fuzzy analytic hierarchy process (FAHP) in order to measure the usefulness of a new product development. In order to increase the overall performance of a firm, they have chosen sub-criteria to each perspective of the BSC as shown in figure 3.

Figure-3. The Hierarchical Structure of Balanced Scorecard (BSC) – (Chen, 2008)

Source: Chen (2008).

Risk management for product innovation comes along with major uncertainties because of the dynamic technologies and markets. Wang et al. (2010) suggested a risk management framework to rise success proportions of R&D projects. Authors used the BSC to identify key performance indicators of the project that are in line with the firm’s vision and strategy.

The BSC is also used in technology strategy planning by Ghazinoory and Soofi (2012). As the systematic national planning was first emerged on development of nanotechnology in Iran, strategy map and balanced scorecard are used by Ghazinoory and Soofi (2012) for measuring the efficiency of National Iranian Nanotechnology Initiative.

Khota and Pretorius (2012) discussed R&D strategy map with balanced scorecard perspective that focus a strategy on intellectual property and product innovation and introduced knowledge-centered metrics for product development with BSC perspective.

Moreover, Jarrar and Smith (2014) discussed the significance of innovation to organizations with the relationships between entrepreneurial strategy and each of the participative budgeting, BSC, total quality management, just in time, and organizational performance. The study conducted by Rylková and Bernatík (2014) evaluates the performance measurement in Czech Republic and similarly mentions the importance of modern measurement tools as BSC, total quality management etc. as the fourth and the last phase of measuring business performance. Another Czech study is implemented by Zizlavsky (2014) for the discussion of innovative performance management and management control system in small and medium-sized enterprises that are located in Czech Republic.

3.2. Information Systems and Knowledge Management

In web-based decision systems, Bhargava et al. (2007) discussed the first introduction of innovative enterprise performance management systems that has happened in 1998. Alongside with it, the study highlights the milestones of performance management in web-based decision systems especially from the decision support systems perspective.

What’s more, the BSC innovation and learning framework is fitted to the tacit knowledge by Harlow (2008). The study proposes a usage of the tacit knowledge index to evaluate the level of tacit knowledge within firms and its consequence on firm performance. It is believed that the tacit knowledge index is suitable to the BSC innovation and learning framework. It is also pointed that the BSC innovation and learning has a measurability problem. On the other hand, however, it is suggested that the tacit knowledge index can solve this problem by allowing the managers of the firm to lift the company’s innovation and learning parameters through various programs that are using the tacit knowledge index.

Another IT-based innovation was obtained from the work of Amberg and Lang (2009). The authors examined five different scorecards and used IT balanced scorecard for their research to point the alignment of IT-based innovation and IT-innovation. In addition to this, Asosheh et al. (2010) focus on IT as one of the keys for organizational innovation and competitive advantage. Hence, offer data envelopment and balanced scorecard approach for project selection in information technology. In this new methodology, BSC is used as a defining tool for project evaluation criteria.

Han (2011) also took the balanced scorecard into next level with self-innovation. The author took the case company into consideration as Kaplan and Norton’s balanced scorecard does not meet demands of the case company’s requirements in personalizing the balanced scorecard.

Another approach on knowledge management is included into the literature by Lopez-Nicolas and Merono-Cerdan (2011). Authors wanted to enlighten the consequences of strategies towards the knowledge management that influence corporate performance and innovation of the company. The study used a similar model to proposed financial perspective in the BSC. They state that the conclusion of their study can aid knowledge management designs for higher innovation, profitability, efficiency, and effectiveness in strategic management.

Electronic supply chain management is generally considered as a strategy in gaining the competitive advantage. Wu and Chang (2012) think that the diffusion of electronic supply chain management is crucial for success. Therefore, they focused on the BSC with the extension to supply chain management for four performance perspectives for adequate measuring. By standing the base to the innovative diffusion theory and the balanced scorecard, the study offers a framework for investigating the stage-based structure with the BSC. In 2014, Wu and Chen further discussed the stage-based diffusion of information technologies and the balanced scorecard with the innovation diffusion theory.

Furthermore, Loukis and Charalabidis (2013) empirically investigated the role of information systems to generate a business value with its suppliers, business partners and customers etc. They aimed to contribute to the literature by investigating the data of 14,065 European firms from 25 countries that operate in 10 business sectors that is collected through e-Business Watch Survey of the European Commission.

3.3. Finance & Management Accounting

Moreover, the use of balanced scorecard is also discussed parallel to the innovation perspectives in management accounting literature. Rom and Rohde (2007) focused on the innovation within the context of enterprise resource planning (ERP) and integrated information systems (IIS). To some extent, the study suggests that the balanced scorecard is a sophisticated approach for measuring the performance of the management accounting. The research investigated within the study of Rom and Rohde (2007) suggests that a research on management accounting techniques and ERP systems suggests that companies prefer using the balanced scorecard with lower degrees of integration. This integration is often described as the use of specialized software.

In the International Conference on Management Science and Engineering, Zhao (2007) introduced another innovative aspect of the BSC. Despite the fact that their study was based on the state-owned enterprise group, they based their study on the balanced scorecard to investigate the strategic financial risk management. The study suggest that the BSC has a direct impact on the decision-making efficiency in strategic financial management.

Accounting information systems are later taken into consideration by Granlund (2011). The discussion was based on the relationship among information technology, management accounting and management control. Similar to Rom and Rohde (2007); Granlund (2011) introduced the BSC as a key technical tool in strategic management.

Moreover, the study of Belfo and Trigo (2013) discuss the today and tomorrow of accounting information systems and indicated that the balanced scorecard systems will continue to grow in terms of importance in years.

Chenhall and Moers (2015) focused on the scope of innovation in management accounting and its influence on the management control. They pointed the development of BSC to observe the organizational behavior concerning the management control.

Another finance related approach is introduced by Yiannaki (2015). The author is developed a study on small and medium-sized enterprises to compare their handling of both risk and crisis management. The study aimed to improve SME’s management performance for crisis.

3.4. Tourism

Another innovative application area of the BSC for strategic management is tourism. Huang (2008) examined the travel agencies in Taiwan from the strategic point of view in terms of the performance management model. The study offers a wide range of theoretical application background for BSC applications. It is concluded that the correct identification of the BSC performance indicators can help to realize and improve -in terms of efficiency- the e-commerce strategic goals of the company. This is also to yield a better tourism performance. While investigating the strategic orientations of the tourism enterprises in Turkey, Avci et al. (2011) added the related literature of the increasing interest on the BSC for firms performance.

3.5. Construction

Luu (2008) applied the BSC and strengths-weaknesses-opportunities-threats (SWOT) analysis to a large contractor in Vietnam (AnGiang Construction Company) in order to define company strategies not only short-term but also long. The case company of the study was selected due to its best practices in strategic management compared to its competitors and the proposed method is offered for a general use.

3.6. Medical & Healthcare

Healthcare studies also benefited the strength of BSC. McGillis (2008) studied nurse staffing, system integration of organization through the examination of financial indicators with evidence of BSC. As a result of the prediction of nursing care hours (system, type of hospital, and geographic location), it is found that patient and nursing care hours are significantly related to the clinical data.

Luo et al. (2012) however, proposed a model for BSC implementation for service innovation. The study is designed for a medical service department and the implementation is based on an operation-level strategic planning tool while they studied internal medicine ward, surgery ward, gynecology ward, and pediatrics ward in a district hospital.

3.7. Real Estate

Zhou and Zhang (2009) investigated the financial and non-financial pointers of the real estate industry broadly and introduced the gray correlation analysis theory -named as the correlation of uncertainty between system factors or things- into the BSC as well as its drawbacks for strategic investment in the market. In order to implement the BSC indicator system, authors focus on overall and sector-specific strategies.

Hence, a strategic direction should be set by companies with the involvement of top level management. It is seen extremely important -especially SMEs in developing countries- as the owners of such companies have tendency to set the entire strategic direction and plan -including the unit level- bypassing the company hierarchy.

3.8. Social Services

Within this context, Gorun (2014) shows that the balanced scorecard is beneficial to develop wide range of industries including social services. It is believed the balanced scorecard is beneficial due to its modernity in strategic management which allows the improvement of services in efficiency and quality terms.

3.9. Manufacturing

Huang et al. (2011) focus on the organizational innovation with respect to the resource-based view of firm in Taiwanese biopharmaceutical industry. Resource-based and balanced scorecard point of views are taken into account for the analysis of the empirical model that focuses on the information capital, human capital and organization capital for innovative capability. Noori (2015) introduced a research for a steel manufacturing company for innovation performance. The author ranked strategic business units of the company based on their performance on innovation. Within the study, fuzzy analytic hierarchy process and balanced scorecard are applied to explore the algorithms and procedures in detail whilst seeing the BSC as a useful framework for evaluating the innovation performance of the organization. Karabulut (2015) on the other hand, conducted a study of manufacturing firms in Turkey to observe the company performance from the innovation strategy point of view. The author indicates that designing attractive strategies for innovation yields high company performance. The BSC method is considered as a link between the organizational strategy and the performance of the company.

3.10. Corporate Social Responsibility (CSR) & Sustainability

In addition to this, social responsibility steps that the company take are crucial for stakeholder management. Zhang et al. (2009) focused on the stakeholder satisfaction via strategic management. Authors have focused on the improvement of the organizational capability and the optimization of the internal procedure for the strategy implementation with the use of budget plan, balanced scorecard and strategy map within the concept of strategic planning. It is shown that achieving the goal of strategy implementation for stakeholder satisfaction and contribution cannot be considered without the strategy map and the balanced scorecard. Leon-Soriano et al. (2010) further investigated the literature on corporate social responsibility for implementing sustainability BSC in order to direct its strategic planning and management phases. The discussion of sustainable balanced scorecard was considered as a key to take human factor into account via economic and ecological sustainability. Another environmental sustainability issue is undoubtedly the air pollution. Given the reason, scholars pay increasing attention to the environmental aspects of sustainability. One of the most used model for assessing the environmental impact was pressure-state-response. Wang (2013) studied the pressure-state-response with the combination of BSC for assessing the development on sustainability in Shandong Province of China. They yield environmental management and economic mentions for future use. In addition to this, Álvarez (2015) introduced a case study of a Spanish company that deals with the financial sector software. The study aimed to guide in improving the sustainability by suggesting a strategic management approach with the balanced scorecard. It is believed that the BSC framework is the way of improving the sustainability.

3.11. Method Specific Applications (Artificial Neural Network & Analytic Hierarchy Process)

Apart from the sectoral case discussions of the balanced scorecard, some of the articles are more associated with the method it proposes. To this extent, Savetpanuvong and Tanlamai (2008) focused on the strategic neuron modelling with artificial neural network base. The study introduced the balanced scorecard and strategy map in customer value proposition and value-creation as a hidden process. Authors chosen an enterprise performance data from Thailand to train the samples. Furthermore, Quezada and Lopez-Ospina (2014) proposed a method to identify the cause-effect relationships between strategic objectives of a strategy map of a balanced scorecard. In their study, the Analytic Hierarchy Process and Analytic Network Process are used to model a BSC. It is considered as a useful approach since the blend of those two enables the investigate tangible and intangible factors of BSC.

4. CONCLUSION

This article addresses the topics of strategic management and balanced scorecard approach by pointing the innovative issues about these matters must be reflected. These subjects were acknowledged as a main result of a content analysis of analyzed scientific journal articles that deal with the incorporation of innovation perspective of the strategic management and the balanced scorecard. Earlier works in this field have filed a wide range of issues as being important. These studies have either been usually practical, or have solely motivated on very specific theoretical issues of strategic management and balanced scorecard combination. Most notably, this is a literature review combining innovation, strategic management, and the balanced scorecard. Based on the results of the content analysis conducted, the relevant issues and grouping of the application areas are presented in a context providing a summary by organizing and deliberating the identified issues (see Table 1, and Figure 2). Finally, wide range of application areas of the balanced scorecard prove that regardless of the operating area of the enterprise, innovation is crucial for competitive advantage and success. Hence, the strategic objectives of the company should be set with the innovation point of view to sustain their strengths in the environment that they operate in.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Álvarez, C., 2015. A scorecard framework proposal for improving software factories sustainability: A case study of a Spanish firm in the financial sector. Sustainability Switzerland, 7(12): 15999-16021.

Amberg, M. and M. Lang, 2009. IT balanced scorecard as tool for managing IT innovations and IT-based innovations. Proceedings of the European Conference on Information Management & Evaluation, (Kütz 2005). pp: 471–478.

Apak, S. and E. Atay, 2014. Global innovation and knowledge management practice in small and medium enterprises (SMEs) in Turkey and the Balkans. Procedia Social and Behavioral Sciences, 150: 1260–1266.

Asosheh, A., S. Nalchigar and M. Jamporazmey, 2010. Information technology project evaluation: An integrated data envelopment analysis and balanced scorecard approach. Expert Systems with Applications, 37(8): 5931–5938. DOI http://dx.doi.org/10.1016/j.eswa.2010.02.012.

Avci, U., M. Madanoglu and F. Okumus, 2011. Strategic orientation and performance of tourism firms: Evidence from a developing country. Tourism Management, 32(1): 147–157. DOI http://dx.doi.org/10.1016/j.tourman.2010.01.017.

Belfo, F. and A. Trigo, 2013. Accounting information systems: Tradition and future directions. Procedia Technology, 9: 536–546.

Bhargava, H.K., D.J. Power and D. Sun, 2007. Progress in web-based decision support technologies. Decision Support Systems, 43(4): 1083–1095.

Bigliardi, B. and A.I. Dormio, 2010. A balanced scorecard approach for R&D: Evidence from a case study. Facilities, 28(5): 278-289.

Bouhali, R., 2015. Leader roles for innovation: Strategic thinking and planning. Procedia Social and Behavioral Sciences, 181: 72–78.

Calabrese, A. and R. Costa, 2015. Strategic thinking and business innovation: Abduction as cognitive element of leaders strategizing. Journal of Engineering and Technology Management, 38: 24–36. DOI http://dx.doi.org/10.1016/j.jengtecman.2015.06.001.

Carmeli, A., R. Gelbard and D. Gefen, 2010. The importance of innovation leadership in cultivating strategic fit and enhancing firm performance. Leadership Quarterly, 21(3): 339–349. DOI http://dx.doi.org/10.1016/j.leaqua.2010.03.001.

Chen, H.H., 2008. Operating NPD innovatively with different technologies under a variant social environment. Technological Forecasting and Social Change, 75(3): 385–404.

Chenhall, R.H. and F. Moers, 2015. The role of innovation in the evolution of management accounting and its integration into management control. Accounting, Organizations and Society, 47: 1–13. DOI http://dx.doi.org/10.1016/j.aos.2015.10.002.

Frost, B., 2007. Balanced scorecard. In designing metrics - crafting balanced measures for managing performance. Dallas, Texas: Measurement International. pp: 24–26.

Garcia-Valderrama, T., E. Mulero-Mendigorri and D. Revuelta-Bordoy, 2008. European journal of innovation management article title page. European Journal of Innovation Management, 11(2): 241–281.

Garcia-Valderrama, T., E. Mulero-Mendigorri and D. Revuelta-Bordoy, 2009. Relating the perspectives of the balanced scorecard for R&D by means of DEA. European Journal of Operational Research, 196(3): 1177–1189. DOI http://dx.doi.org/10.1016/j.ejor.2008.05.015.

Ghazinoory, S. and A. Soofi, 2012. Modifying BSC for national nanotechnology development: An implication for ‘social capital role in NIS theory. Technological and Economic Development of Economy, 18(3): 487–503.

Gorun, A., 2014. New models and modern instruments in the development of social services. Revista De Cercetare Si Interventie Sociala, 45: 240–252.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A research note. International Journal of Accounting Information Systems, 12(1): 3–19. DOI http://dx.doi.org/10.1016/j.accinf.2010.11.001.

Gulati, R., 2013. Managing Performance. In maintenance and reliability best practices. 2nd Edn., Industrial Press. pp: 283–307.

Han, L.H., 2011. Innovation of balanced scorecard on the theory and practice. Proceedings - International Conference on Machine Learning and Cybernetics, 3: 1006–1009.

Harlow, H., 2008. The effect of tacit knowledge on firm performance. Journal of Knowledge Management, 12(1): 148–163.

Huang, H.C., M.C. Lai and T.H. Lin, 2011. Aligning intangible assets to innovation in biopharmaceutical industry. Expert Systems with Applications, 38(4): 3827–3834. DOI http://dx.doi.org/10.1016/j.eswa.2010.09.043.

Huang, L., 2008. Strategic orientation and performance measurement model in Taiwan’s travel agencies. Service Industries Journal, 28(10): 1357–1383.

Jacobsen, J.J., 2011. Conveying and reporting on a mission and vision of environmental and social responsibility. In sustainable business and industry - designing and operating for social and environmental responsibility. Milwaukee, Wisconsin: American Society for Quality (ASQ). pp: 15–24.

Jarrar, N.S. and M. Smith, 2014. Innovation in entrepreneurial organisations: A platform for contemporary management change and a value creator. British Accounting Review, 46(1): 60–76. DOI http://dx.doi.org/10.1016/j.bar.2013.07.001.

Kaplan, R.S. and D.P. Norton, 1996. Measuring business strategy in the balanced scorecard: Translating strategy into action. Boston, MA: Harvard Business Press. pp: 43-190.

Karabulut, A.T., 2015. Effects of innovation types on performance of manufacturing firms in Turkey. Procedia - Social and Behavioral Sciences, 195: 1355–1364.

Khota, I. and L. Pretorius, 2012. Harvesting ip-based value potential: The intellectual property scorecard as a mechanism to capitalize on technological innovation, knowledge, and ip. International Journal of Innovation and Technology Management, 9(2). Available from http://www.worldscientific.com/doi/abs/10.1142/S0219877012500095.

Kohl, H., 2016. Integrated evaluation system for the strategic management of innovation initiatives in manufacturing industries. Procedia CIRP, 40: 335–340.

Lendel, V., Š. Hittmár and M. Latka D, 2015. Application of management of innovation processes in enterprises: Management approach, problems and recommendations. Procedia Economics and Finance, 34(15): 410–416.

Leon-Soriano, R., M.J. Munoz-Torres and R. Chalmeta-Rosalen, 2010. Methodology for sustainability strategic planning and management. Industrial Management & Data Systems, 110(2): 249–268.

Lopez-Nicolas, C. and A.L. Merono-Cerdan, 2011. Strategic knowledge management, innovation and performance. International Journal of Information Management, 31(6): 502–509.

Loukis, E.N. and Y.K. Charalabidis, 2013. An empirical investigation of information systems interoperability business value in European firms. Computers in Industry, 64(4): 412–420. DOI http://dx.doi.org/10.1016/j.compind.2013.01.005.

Luo, C.M.A., H.F. Chang and C.H. Su, 2012. Balanced scorecard as an operation-level strategic planning tool for service innovation. Service Industries Journal, 32(12): 1937–1956.

Luu, T.V., 2008. Performance measurement of construction firms in developing countries. Construction Management and Economics, 26(4): 373–386.

McGillis, H.L., 2008. Nurse staffing and system integration and change indicators in acute care hospitals: Evidence from a balanced scorecard. Journal of Nursing Care Quality, 23(3): 242–252.

Munro, R.A., G. Ramu and D.J. Zrymiak, 2015. A six sigma and organizational goals. In certified six sigma green belt handbook. Milwaukee, Wisconsin: American Society for Quality (ASQ). pp: 1–30.

Noori, B., 2015. Strategic business unit ranking based on innovation performance: A case study of a steel manufacturing company. International Journal of Systems Assurance Engineering and Management, 6(4): 434–446.

Pasman, H., 2015. Costs of accidents, costs of safety, risk-based economic decision making: risk management. In risk analysis and control for industrial processes - gas, oil and chemicals - a system perspective for assessing and avoiding low-probability, high-consequence event. Elsevier. pp: 383–406.

Planko, J., 2016. Strategic collective system building to commercialize sustainability innovations. Journal of Cleaner Production, 112: 2328–2341. DOI http://dx.doi.org/10.1016/j.jclepro.2015.09.108.

Prahalad, C.K. and G. Hamel, 1990. The core competence of the corporation. Harvard Business Review, 68(3): 79–91.

Prajogo, D.I., 2016. The strategic fit between innovation strategies and business environment in delivering business performance. International Journal of Production Economics, 171: 241–249. DOI http://dx.doi.org/10.1016/j.ijpe.2015.07.037.

Quezada, L.E. and H.A. Lopez-Ospina, 2014. A method for designing a strategy map using AHP and linear programming. International Journal of Production Economics, 158: 244–255. DOI http://dx.doi.org/10.1016/j.ijpe.2014.08.008.

Rom, A. and C. Rohde, 2007. Management accounting and integrated information systems: A literature review. International Journal of Accounting Information Systems, 8(1): 40–68.

Rylková, Ž. and W. Bernatík, 2014. Performance measurement and management in Czech enterprises. Procedia - Social and Behavioral Sciences, 110: 961–968.

Savetpanuvong, P. and U. Tanlamai, 2008. Modeling strategy with strategic Neuron ®. In 4th IEEE International Conference on Management of Innovation and Technology. Bangkok: IEEE. pp: 559-564.

Schilling, M.A., 2013. Designing the organization’s strategic direction. In strategic management of technological innovation. New York: McGraw-Hill. pp: 105–126.

Sedera, D., 2016. Innovating with enterprise systems and digital platforms: A contingent resource-based theory view. Information and Management, 53(3): 366–379.

Sherman, E.H., 2015. Financial decision making and the techniques used in financial analysis. In manager’s guide to financial analysis - powerful tools for analyzing the numbers and making the best decisions for your busines. AMACOM - Book Division of American Management Association. pp: 1–16.

Sołoducho-Pelc, L., 2015. Searching for opportunities for development and innovations in the strategic management process. Procedia - Social and Behavioral Sciences, 210: 77–86.

Voelpel, S.C., M. Leibold and R.A. Eckhoff, 2006. The tyranny of the balanced scorecard in the innovation economy. Journal of Intellectual Capital, 7(1): 43–60.

Walker, R.M., J. Chen and D. Aravind, 2015. Management innovation and firm performance: An integration of research findings. European Management Journal, 33(5): 407–422. DOI http://dx.doi.org/10.1016/j.emj.2015.07.001.

Wang, J., W. Lin and Y.H. Huang, 2010. A performance-oriented risk management framework for innovative R&D projects. Technovation, 30(11-12): 601–611. DOI http://dx.doi.org/10.1016/j.technovation.2010.07.003.

Wang, Q., 2013. Key evaluation framework for the impacts of urbanization on air environment - a case study. Ecological Indicators, 24: 266-272. DOI http://dx.doi.org/10.1016/j.ecolind.2012.07.004.

Westcott, R.T., 2014. A management skills and abilities. In Certified Manager of Quality/Organizational Excellence Handbook. American Society for Quality (ASQ), Milwaukee, Wisconsin. pp: 132–199.

Wu, I.L. and C.H. Chang, 2012. Using the balanced scorecard in assessing the performance of e-SCM diffusion: A multi-stage perspective. Decision Support Systems, 52(2): 474–485. DOI http://dx.doi.org/10.1016/j.dss.2011.10.008.

Wu, I.L. and J.L. Chen, 2014. A stage-based diffusion of IT innovation and the BSC performance impact: A moderator of technology-organization-environment. Technological Forecasting and Social Change, 88: 76–90. DOI http://dx.doi.org/10.1016/j.techfore.2014.06.015.

Yiannaki, S.M., 2015. A systemic risk management model for SMEs under financial crisis. International Journal of Organizational Analysis, 20(4): 406–422.

Yıldız, S., F. Baştürk and İ.T. Boz, 2014. The effect of leadership and innovativeness on business performance. Procedia - Social and Behavioral Sciences, 150: 785–793.

Zhang, S., Y. Zhang and Y. Liu, 2009. Enterprise strategic management framework based on stakeholder satisfaction and contribution. In 2009 International Conference on Information Management, Innovation Management and Industrial Engineering. pp: 87–91.

Zhao, H., 2007. An innovative research on the mechanism of integrated strategic financial risk management in the state-owned enterprise group - based on the balanced scorecard. In 2006 International Conference on Management Science and Engineering. Lille: IEEE. pp: 1696–1702.

Zhou, X. and X. Zhang, 2009. Evaluation of strategic investment value of the real estate industry. In 2009 International Conference on Information Management, Innovation Management and Industrial Engineering. IEEE. pp: 42-45.

Zizlavsky, O., 2014. The balanced scorecard: Innovative performance measurement and management control system. Journal of Technology Management & Innovation, 9(3): 210–222.

| Views and opinions expressed in this article are the views and opinions of the authors, International Journal of Asian Social Science shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |