- 1. INTRODUCTION

- 2. COMOROS ECONOMIC BACKGROUND

- 3. RESEARCH METHODOLOGY

- 4. EMPOWERING WOMEN THROUGH ISLAMIC FINANCIAL INCLUSION

- 5. PAYMENT FINANCIAL INCLUSION DIMENSION

- 6. BORROWING FINANCIAL INCLUSION DIMENSION

- 7. SAVING AND INVESTMENT FINANCIAL INCLUSION DIMENSION

- 8. INSURANCE FINANCIAL INCLUSION DIMENSION

- 9. USAGE OF FINANCIAL SERVICES

- 10. CONCLUSION AND RECOMMENDATIONS

- REFERENCES

EMPOWERING WOMEN THROUGH FINANCIAL INCLUSION: SOME EVIDENCE FROM COMOROS

Islamic Research and Training Institute (IRTI/IDB), Saudi Arabia

ABSTRACT

Financial inclusion incorporates a range of initiatives that make financial services available, accessible, and affordable to all segments of the population, including women, youth and rural communities and other disadvantaged groups. Islamic financial inclusion goes beyond improved access to finance to encompass enhanced access to savings and risk mitigation products, as well as social inclusion that allows individuals and companies to engage more actively in the real economy. This study’s main objective is to investigate how to empower Muslim women in Comoros via relevant Islamic financial products and services. The study used structured questionnaires to collect primary data from respondents who were randomly selected from among women living in the outskirts of Moroni, the capital of Comoros, and Tsidje, which is a large city not far from the capital. Three focus group discussions (FGDs) comprising 24 participants were held to facilitate a deeper understanding of Islamic financial inclusion among Comoros women. The results provide strong evidence of the importance of removing the barriers hindering access to Islamic financial services for the disadvantaged women in Comoros through providing Islamic social financial tools and building capacity. The results show that women either have no money to use the financial services or lack the relevant financial services knowledge that might make them capable of being financially included and hence lifted out of poverty.

Keywords:Islamic financial inclusion, Access to Islamic finance, Empowering women.

ARTICLE HISTORY: Received:15 November 2018 Revised:20 December 2018 Accepted:25 January 2019 Published:13 March 2019 .

Contribution/ Originality:This study investigated for the first time the financial inclusion of women in Comoros using structural questionnaires and focus group discussion. The results have significant implications for policy makers and financial institutions in Comoros to remove the financial inclusion barriers and innovate their relevant gender specific financial services.

1. INTRODUCTION

Financial inclusion is an important element in the formulation of Sustainable Development Goals (SDGs), the new development architecture that succeeds the Millennium Development Goals (MDGs). It was also given significant prominence at the United Nations Report (2015![]() ). At the Group of Twenty (G-20), financial inclusion has been given greater prominence in the reform and development agendas (Global Partnership for Financial Inclusion (GPFI), 2016

). At the Group of Twenty (G-20), financial inclusion has been given greater prominence in the reform and development agendas (Global Partnership for Financial Inclusion (GPFI), 2016![]() ). The G20 emphasized the key role of financial inclusion as an important element in the fight against the poverty and the pursuit of inclusive development1 . According to the Global F index Data (Demirgüç-Kunt et al., 2017

). The G20 emphasized the key role of financial inclusion as an important element in the fight against the poverty and the pursuit of inclusive development1 . According to the Global F index Data (Demirgüç-Kunt et al., 2017![]() ) 47 percent of women and 55 percent of men worldwide have an account at a formal financial institution, whether a bank, credit union, co-operative, post office, or microfinance institution. The gender gap varies widely across economies and regions. Among the regions, South Asia and the Middle East and North Africa have the largest gender gaps. It comprises of about 40 percent of women who are less likely to have a formal account than men (CGAP Women and Financial Inclusion, 2015

) 47 percent of women and 55 percent of men worldwide have an account at a formal financial institution, whether a bank, credit union, co-operative, post office, or microfinance institution. The gender gap varies widely across economies and regions. Among the regions, South Asia and the Middle East and North Africa have the largest gender gaps. It comprises of about 40 percent of women who are less likely to have a formal account than men (CGAP Women and Financial Inclusion, 2015![]() ).

).

Financial inclusion or inclusive finance is where effort is made to ensure that all households and businesses, regardless of levels of income, are able to effectively access and use appropriate financial services that they need to improve their lives. Financial inclusion incorporates a range of initiatives that make formal financial services available, accessible, and affordable to all segments of the population, including women, rural populations, the poor, persons with disabilities, and other disadvantaged groups. Financial inclusion goes beyond improved access to credit to encompass enhanced access to savings and risk mitigation products, and a well-functioning financial infrastructure that allows individuals and companies to engage more actively in the economy, while protecting user rights (Triki and Faye, 2013![]() ).

).

Financial inclusion is about the delivery of financial services at an affordable cost to the large sections of disadvantaged and low-income groups. Despite significant improvements in the financial sector’s viability, profitability and competitiveness, there are significant concerns that the banks have failed to provide basic banking services to a significant segment of the population, especially those who are underprivileged. Reasons vary from country to country as do the strategies, but coordinated efforts are needed as financial inclusion can lift the standard of living of the poor and the disadvantaged (Finnegan, 2015![]() ). For financial inclusion to be effective and successful, it is essential to find ways of harnessing the untapped potential of those individuals and businesses currently being excluded from the formal financial sector or not fully served by the available products and services.

). For financial inclusion to be effective and successful, it is essential to find ways of harnessing the untapped potential of those individuals and businesses currently being excluded from the formal financial sector or not fully served by the available products and services.

This study proposes to look at the following three concepts regarding Islamic financial inclusion:

- Access or the type of Islamic financial services available and the affordability of the same;

- Usage or the frequency and regularity of the use of Islamic Financial products and services; and,

- Quality or whether the available Islamic Financial services are tailored to the needs of the Comorians.

i. The rates of satisfaction with Islamic Finance products and services used by financially included individuals

An assessment of access considered the full range of Islamic Finance products and services available (savings, credit, insurance, mobile banking, etc.) as well as the physical (or virtual) location of Islamic bank branches, microcredit institutions (MFIs), credit unions, and so on. The costs of these services was also considered which included registration and administration fees, mark-up rates (on both loans and savings), and the cost of accessing the services (e.g. transport costs, costs of connectivity if relevant, and telephone or network charges).

The actual take-up and usage of financial services, regularity and frequency of use, and the period of time in which they were used was also assessed. This included the extent to which individuals make use of the products and services offered, the rate and frequency of use, and the length of time that they continued to use the service. Quality was measured by determining whether the Islamic products and services are tailored to the individuals’ needs. Are there appropriate segmentation strategies to make the products attractive for various income levels and types of users? Have the financial products and services been innovatively developed to meet the specific needs of the wide range of clients from entrepreneurs to farmers, salaried individuals, the poor, and individuals engaged in the informal economy?

The IDBG and CBS joint venture project for Islamic Financial inclusion enables disadvantaged people and low-income households to invest in human capital development through investing in education for their kids, and by paying for better health care. Islamic financial inclusion that was adopted, through Salam, Murabah, Mudarabah and other unconventional means of finance, might help the needy people and particularly rural inhabitants to invest in agricultural inputs and equipment. However, it also encourages them to start-up their business or even expand it further, thereby contributing positively to the overall physical capital and technology.

Through investing in real economics and real assets, Islamic financial inclusion can best help in promoting SDGs through its effective social and financial inclusion and hence alleviate poverty. Islamic financial inclusion has a wider scope that incorporates all the disadvantaged people with low income or without income at all and becoming the potential contributor to the economic growth and human wellbeing in the country.

Poor people need to be guided and empowered not only through access to financial services, but also by building their financial capacity. They need to be taught how to invest in high income generating activities within their given environment. Policy makers and multinational developmental intuitions and the donors need to be focused on four core financial inclusion dimensions through which disadvantaged and low-income people should be encouraged to be involved. These financial inclusion dimensions include the payment, borrowing, saving and investment, and takaful (Islamic insurance).

For years, studies have asserted that financial inclusion could create equality by empowering the disadvantaged and giving them greater control over their financial lives. Savings accounts could provide a safe and formal platform to save their earnings for future investments in business operations and build a credit history. Digital payments could help take control of finances and strengthen control over household budgets. Therefore, this would in turn result in higher spending on necessities such as health and education. While this may be right, questions need to be asked as to why, according to The World Bank, approximately 2 billion (Zottel and Khoury, 2016![]() ) remain outside the formal financial system.

) remain outside the formal financial system.

The answer revolves around financial capability. Why do individuals seem to be unwilling and lack the confidence even when they are given the opportunity to act? Do different living circumstances proffer different money management challenges that impact on financial capability and therefore financial inclusion? Why do they seem incapable of managing financial resources and using financial services in a way that best suits their individual needs and their prevailing social conditions?

This study aims to measure the financial inclusion of women living in Comoros. The study seeks to understand and determine the gap in a context of Comoro women’s weaknesses and strengths in terms of financial inclusion. Additionally, it seeks to provide policy makers with baseline information and benchmarks that will help identify and monitor the progress of policy interventions and specific programs in Comoro. It also seeks to allow for more focused research on topics related to financial access such as its linkage to individual, household, and community characteristics. This study could also be used in the identification of potential channels for financial literacy related to the women in Comoros.

2. COMOROS ECONOMIC BACKGROUND

Located in a strategic position at the northern end of the Mozambique Channel, the archipelago of the Union of Comoros consists of three islands: Ngazidja (Grande Comore), Mwali (Moheli), and Nzwani (Anjouan). The country has a claim on a fourth major island, southeastern-most Mayotte (Maore), though Mayotte voted against independence from France in 1974. Since then, an independent Comoros government has never administered it. Since 2011, Mayotte has been administered as an overseas department by France, which has vetoed United Nations Security Council resolutions that would affirm Comorian sovereignty over the island. The Comoros is a member state of the African Union, Francophonie, the Organization of Islamic Cooperation, the Arab League, and the Indian Ocean Commission.

The Union of the Comoros has three official languages – Comorian, Arabic, and French. The religion of the majority of the population is Islam. At 1,660 km2 (640 sq. mi), excluding the contested island of Mayotte, the Comoros is the third-smallest African nation by area. It has inadequate transportation links, a young and rapidly increasing population, and few natural resources. The population, excluding Mayotte, is estimated at 798,000. Since the declaration of independence, the country has experienced more than twenty coups d'état or attempted coups, with various heads of state assassinated. Along with constant political instability, the population of the Union of the Comoros lives with the worst income inequality of any nation. It has a Gini coefficient of over 60%, while also ranking in the worst quartile on the Human Development Index (HDI). Comoros’ HDI value for 2014 is 0.503— which puts the country in the low human development category—positioning it at 159 out of 188 countries and territories. The Comoros moved up to five places to 154 out of 189 countries in the 2016 edition of the World Bank’s annual Doing Business report. Subsequently, some 45% of the population lives below the poverty line. The Comoros, with an estimated gross domestic product (GDP) per capita income of about $700, is among the world's poorest and least developed nations.

Agriculture, fishing, hunting, and forestry are the leading sectors of the economy. Although the quality of the land differs from island to island, most of the widespread lava-encrusted soil formations are unsuited to agriculture. Despite this, most of the inhabitants make their living from subsistence agriculture and fishing. Average wages in 2007 hover around $3–$4 per day. Agriculture contributes 40% to GDP, employs 80% of the labor force, and provides most of the exports.

The Comoros is the world's principal producer of ylang-ylang essence derived from the flowers of a tree originally brought from Indonesia that is used in manufacturing perfumes and soaps. Ylang-ylang essence is a major component of Chanel No. 5, the popular scent for women. The country is also the world's second largest producer of vanilla, after Madagascar. Cloves are another important cash crop. The production of all these three commodities fluctuates wildly, mainly in response to changes in global demand and natural disasters such as cyclones. Profits—and therefore, government receipts—likewise skyrocket and plummet and this wreaks havoc with government efforts to predict revenues and plan expenditures.

The Comoros is also not self-sufficient in food production. Rice, the main staple, accounts for the bulk of imports. Other major obstacles include electricity shortages, vulnerability to external shocks, and low educational levels of its labor force which contribute to a subsistence level of economic activity, high unemployment leading to a heavy dependence on foreign grants, and technical assistance.

The Union of Comoros has a relatively small and underdeveloped financial sector. However, while financial intermediation and credit to the private sector is low, it has been expanding in recent years following the entry of two foreign commercial banks. Yet, at the same time, further development of credit markets remains constrained by poorly defined land ownership rights and weak enforcement of collateral guarantees. At present, the country's financial system comprises of eight financial institutions engaged in deposit taking and lending from the general public. These financial sector players include: The Banque des Comoros (The Central Bank), one commercial bank (Banque pour l’Industrie et le Commerce des Comoros), and one development bank (Banque de Development des Comoros). There also exists a National Savings Fund, a postal savings bank, two networks of microfinance institutions (MFIs), and a small finance program run by a USAID-supported organization, PlaNet Finance. The PlaNet Finance program offers training to poor and vulnerable groups to generate income, including creating and managing businesses, as well as granting them access to loans.

Since it reached its completion point under the Heavily Indebted Poor Countries (HIPC) Initiative in December 2012, the Comoros has returned to economic growth. The International Monetary Fund (IMF) initially projected growth of 2.2% in 2016. This was before the Comoros received huge budget support from Saudi Arabia and Chinese technical assistance for the energy sector amounting to 4 million EUR. Forecasters are now projecting 4.1% growth in 2016 and 2017 as a result of the gradual recovery of electricity generation, and, more importantly, the impact of Saudi Arabian budget support on household consumption2 . The government is working to upgrade education and technical training, to privatize commercial and industrial enterprises, to improve health services, to diversify exports, to promote tourism, and to reduce the high population growth rate. Continued foreign support is essential if the goal of 4% annual GDP growth is to be met.

3. RESEARCH METHODOLOGY

Financial capability is a complex concept that is not amenable to measurement by a small number of questions. That said, every effort will be made to ensure the utility of each question in the questionnaires and that all segments of the population will be able to answer them. This study used randomly selected individuals as the proposed unit of analysis. The study comprised of two main survey instruments: the main (individual) questionnaire, which includes the questions designed to measure financial capability and a location questionnaire.

The individual questionnaire was administered to one randomly selected adult in each sample household to collect data on the financial behaviors and attitudes identified by the qualitative work as key components of financial capability. The questionnaire was designed to capture some of the characteristics that make the individuals financially capable. Some data on the household where the individuals live was also gathered and 318 comprehensive responses were received.

The location questionnaire was designed to collect a limited set of community variables that used to characterize the environment in which the individuals make financial choices. It was administered only once via a focus group discussion in a given community or cluster of dwellings, and the data attributed to all the dwellings in the community. This was a time-saving approach. The questionnaires were translated into the most commonly spoken local languages of English, Arabic, and French.

A pre-test was undertaken to establish quality and comprehensiveness of the questionnaires with the lessons learnt incorporated into the revised final version of the questionnaires. Triangulation, reading, and re-reading of data to search for and identify emerging themes in the data were done consistently. Some of the objectives required in depth information (qualitative), while other objectives needed quantitative data for drawing analysis and conclusions.

After data collection, the questionnaires were checked for completeness. The data was cleaned and coded in Excel using a format that represents responses to specific questions/objectives. The qualitative data notes were edited and cleaned, and a repository of outstanding points was also created. These were then categorized into themes in line with the study objectives. The privacy of the respondents in this survey was protected. Data that contains identifying information will never be released, and respondents were made aware of the statistical confidentiality of the data they provide. At the start of the interview, the selected respondent was given a chance to understand what the survey is all about and how the data will be used. An agreement from the respondent to do the survey was obtained by their endorsement of the consent form. The data will remain confidential. While the unit record data will be available to analysts and researchers, it will never be disseminated to anyone with names, addresses, or any other information that would allow a respondent to be identified.

4. EMPOWERING WOMEN THROUGH ISLAMIC FINANCIAL INCLUSION

Table 1 shows the summarized statistics for the sample. Since the study is investigating women being empowered through Islamic financial inclusion, 100% of the sample is women. This table shows that more than 40% of the sample was married, around 7% were either widowed or divorced, and the rest were single. Most sampled households (42.1%) resided in the outskirts of the investigated cities, 31.4% live in rural areas, while 13.8% resided in the urban areas. 34.5% of those surveyed were the heads of their households. Most of the respondents were employed (56.4%), while 43.6% either refused to answer, had informal work or were unemployed. 52.3% of the respondents had more than high secondary school, more than a third had finished high school, and only 12.9% had stopped education before high school. The average age of the respondents shows that almost more than 80% were below 40 years old, while only 19.5% was above 40 years old. On average, 67.3% of the participants who were women reported their monthly income as being less than 5000 KMF, while 23.9% refuse to declare their monthly income.

Table-1. Sample descriptions.

Variables |

Mean% |

Female (%) |

100 |

Education (%) |

|

Less than high school |

12.9 |

High school |

34.8 |

University |

52.3 |

Marital status (%) |

|

Married |

40.3 |

Divorced/ widowed/ separated |

6.9 |

Single |

52.8 |

Employment (%) |

|

Employed |

56.4 |

Others |

43.6 |

Respondents' place of residence (%) |

|

City |

13.8 |

Outskirts of the city |

42.1 |

Rural areas |

31.4 |

Refuse to answer |

12.7 |

Household heads |

34.5 |

Age (%) |

|

(16-25 Years |

39.6 |

(26-40 Years |

40.9 |

(More than 40) |

19.5 |

Monthly income (%) |

|

Less than 5,000 |

67.3 |

More than 5,000 |

8.8 |

Refused to answer |

23.9 |

Source: Author computation from the Financial Inclusion Structured Questionnaires.

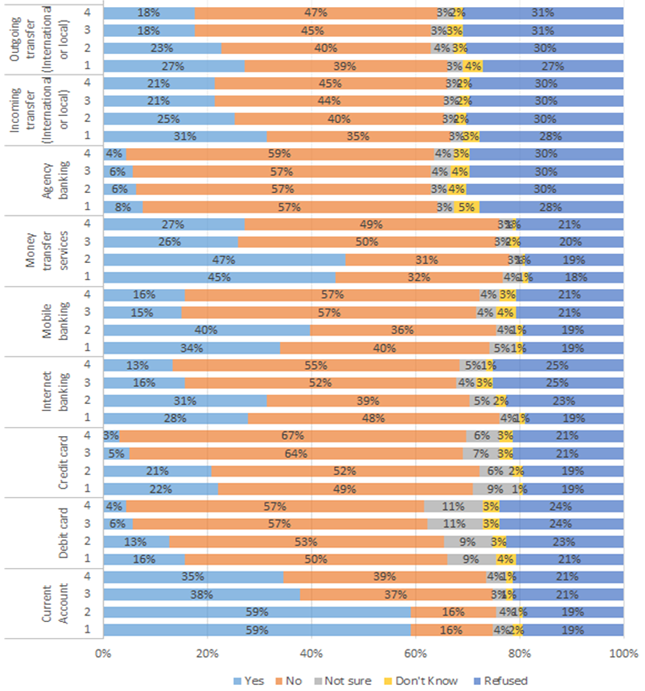

5. PAYMENT FINANCIAL INCLUSION DIMENSION

Figure 1 shows that with 59% of those surveyed, either the women or their immediate family had previously owned bank accounts in either conventional or Islamic banks, while 25% either did not know if they did so or refused to answer. Holding a bank account is essential as a tool in financial inclusion. Unfortunately, more than 70% of those surveyed women claimed that they were either not willing or could not bear the costs of holding a bank account. The cost is one of the challenges that might affect disadvantaged Comoro women’s access to finance. Figure 1 also showed that only 16% of the surveyed sample owned a debit card. This implied that the majority of the women under investigation were not able to use the ATM which reduces the cost of using physical bank accounts and has expanded the financial services significantly. Only 22% of the sample or their immediate family owned a credit card and most of them (78%) indicated that it was costly and that they could not afford it.

Recently, wireless and internet banking has proved to be an effective solution for expanding the financial services, particularly in reaching the poor and rural areas in order to overcome the cost of infrastructure and the high cost of using financial services. While the above argument showed that the high cost of holding or using debit accounts is one of the challenges facing Comoro women, only 28% of them or their immediate family use internet banking services. Most of the surveyed women did not know about internet banking which reflects the level of financial illiteracy among the respondents. Additionally, the high costs might prevent the respondents acquiring devices and access to internet.

Figure-1. Payment Financial Inclusion Dimension.

Source: Author computation from the Financial Inclusion Structured Questionnaires.

The above wireless payment argument was reflected clearly when the respondents were asked about whether they owned mobile devices or if they were able to bear the cost of related products and services. Only 34% of the sample declared that they owned mobile devices, while 57% agreed that they either were not able or were unwilling to bear the cost of mobile services. Hence, the government of Comoros needs to provide reasonable wireless internet infrastructure to encourage adoption by disadvantaged users in order to overcome the high cost of providing the financial services.

Finally, the transfer of money inside and outside the country is essential for financial inclusion and it helps the country to achieve economic growth. Unfortunately, the results of the survey showed that there were weak ingoing (31%) and outgoing (27%) money transfers among respondents and their family. However, this might imply that more disadvantaged women in Comoro do not usually benefit from financial inclusion through money transfers. Comoros women might not be holding enough means of payment that would help them become financially empowered.

6. BORROWING FINANCIAL INCLUSION DIMENSION

The demographic breakdown in Table 1 shows that the surveyed women borrow and save for a range of activities despite their disadvantaged situation or their employment. Also, more than 31% rural women in the sample are expected to borrow and save for agriculture and livestock investment, while the other 13% of respondents might borrow and save to invest in the joint venture or start up business since they are living in the city. Those who live in the outskirts of the city fall in between the rural area and the city. Also, they might borrow and invest to meet the demands of the urban people or those in small shops and individual business. The majority of the women surveyed are educated and they are expected to borrow, save, and invest.

Figure-2. Borrowing Financial Inclusion Dimension.

Source: Author computation from the Financial Inclusion Structured Questionnaires.

Figure 2 shows the questions that were asked of the respondents in order to examine their ability to borrow using one or some of the above financial services. Using one or more of the financial products is essential to help disadvantaged and low-income people to fulfil their financial needs. The respondent was also asked four questions in each of the payment components. The questions asked whether they or any one from their immediate family currently owned , or in the past 12 months had owned, any of the above means of payments. If it was available, could they get it if they wanted it? Would they be willing to pay the cost of this product or service? Would they be able to bear the cost of this product or service?

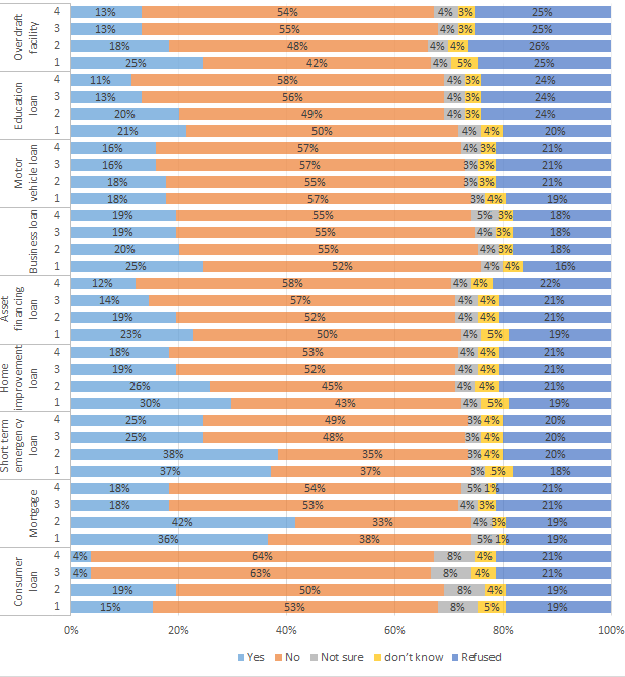

Figure 2 shows that there are very low levels of borrowing from all type of the respondents whether they are living in the city, around the city, or rural areas. Only 15% of the respondents were able to take out consumer loans, and the majority of them could not take out consumer loans. Their answers implied that they could not bear the high cost (more than 65% claimed the cost was high) of borrowing the consumer loan. Alternatively, being Muslim, they might refrain from borrowing for consumption. The respondents’ borrowing levels relatively improved when asked about mortgage loans (36%), short-loans (37%), and home-improvement loans (30%). Despite these improvements, the cost of borrowing still represented the main challenge for low-income women and the disadvantaged. As with consumption loans, the other loans such as business loans (25%), asset financing loans (19%), and motor vehicle loans (18%) also showed a very low level of uptake.

On an average, the above results reflected a higher percentage of non-borrower women in the case of Comoros such as in consumer loans (85%), mortgage loans (64%), short-term loans (63%), home-improvement loans (70%), asset financing loans (81%), business loans (75%), and motor vehicle loans (82%). The non-borrowers’ responses indicated that they were unable to borrow; they did not know where to borrow from or were just not sure. This, represents an additional constraint to financial access in Comoros. The policy makers need to be very specific in studying these challenges for financial inclusion. These non-borrowers might not know where to get the loan or are less aware of the institutions providing the loans, reflecting greater supply side constraint in Comoros. Moreover, the not sure answer implies a lower level of financial literacy since the surveyed women showed a lower understanding of how and where to get the loan. Finally, the results also show that women in urban and rural Comoros faced almost similar barriers to financial access as reflected by the lower rates of borrowing from the financial institutions.

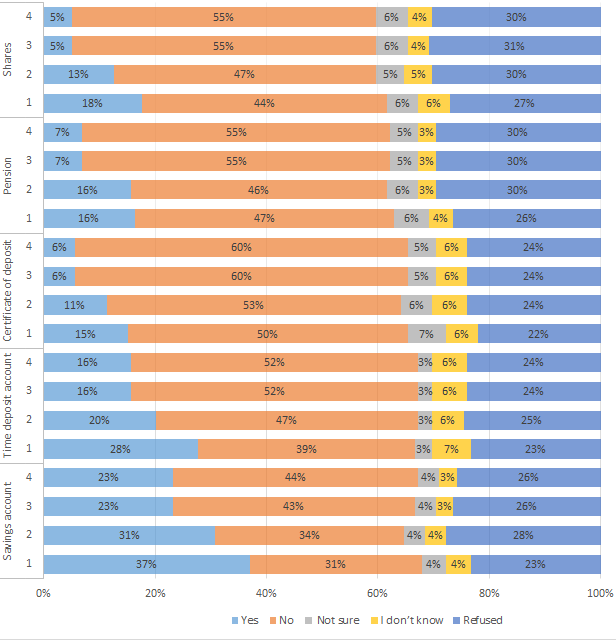

7. SAVING AND INVESTMENT FINANCIAL INCLUSION DIMENSION

Figure 3 represents the questions that were asked of the respondents in order to examine their ability to save using one or some of the above-mentioned financial services. Using one or more of the financial products is essential to help disadvantaged and low-income people save and invest and gain more financial empowerment. Each respondent was asked four questions about each financial product: whether they or any one in their immediate family currently save or invest or have done so in the past 12 months; if it was an available product could they use it if they wanted to; were they willing to do so; and would they be able to afford doing so? Saving and investment is essential for financial empowerment for disadvantaged and low-income groups, helping them become financially secure and face emergencies. Investment can help people grow their wealth. Investment options such as certificates of deposit and stocks can also offer returns which lead to wealth creation. Figure 3 above shows that the surveyed sample has low savings and investments. 37% have a savings account but only 23% are able and willing to save.

Figure-3. Saving and Investment Financial Inclusion Dimension.

Source: Author computation from the Financial Inclusion Structured Questionnaires.

This might be due to the high cost of saving and investment. The surveyed women also have low incomes or have no surplus income at all to save and invest. The level of savings is even lower for time deposit accounts (28%), certificate deposits (15%), and pensions (16%). The low level of savings implies that the surveyed women live without any expected returns that help them accumulate some wealth to face periods of emergency need. The amount of non-saving women is also very high with respondents not using saving accounts (63%), time deposits (72%), certificate deposits (85%), and pensions (84%). Investment options also don’t fare well. The above results show that only 18% of the respondents have some investment in shares. The level of non-investment (82%) respondents is even higher than the non-savers. More respondents have declared that they have no money, or that their income is too low to save, invest or to borrow. If the respondents have no money, this would even make it difficult for them to be financially included. As all the surveyed women are Muslims, they should be socially included by given them Sadagah, Zakat, and Waqf before they are granted financial access.

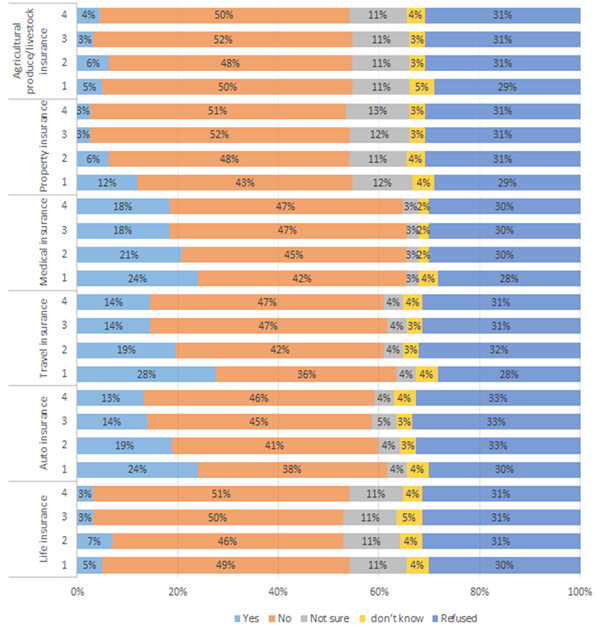

8. INSURANCE FINANCIAL INCLUSION DIMENSION

Figure-4. Insurance Financial Inclusion Dimension.

Source: Author computation from the Financial Inclusion Structured Questionnaires.

The recent discussions between academics and practitioners revealed that insurance is a very essential and effective tool for alleviating poverty through risk mitigation. Insurance also helps those who recently got out of poverty and starting up businesses to manage their risk and avoid living in poverty again. The recent innovations in technology help the insurance sectors to develop effective products to target disadvantaged and low-income groups, particularly with education and health care services in addition to business risk services. It is critically important to assist the poor and the disadvantaged by helping them to startup businesses and grant them more access to insurance and an improvement of their financial inclusion. Providing insurance to the poor and rural areas is an easy task but leaving them without insurance might lead to vital risk for their sustainable development.

In light of this discussion, the surveyed sample was asked about their view on the insurance services provided and the opportunities they might have in Comoros. Figure 4 represents the view of the surveyed women in Comoros regarding their opportunity to use insurance services. The discussion highlighted the importance of the insurance services as a tool for financial inclusion for them being disadvantaged and having a low income. Similar to the previous questions, the respondents were asked four questions for each insurance service: if they or any one in their immediate family has subscribed now, or in the past 12 months, to any means of insurance services; if it was possible to get it if it was available; if they were willing to pay for it; if they could pay for it. The results in Figure 4 above show that only 5% of the surveyed sample or their immediate family subscribed to life insurance services. More than 90% of the respondents were not able to subscribe. The results revealed that the surveyed women could not afford to pay for life insurance services and some lacked the knowledge of why, how, and where to get the life insurance services. The demand was higher for other types of insurance such as auto insurance (24%), travel insurance (28%), and medical insurance (24%) compared to the demand for life insurance.

However, it is still considered far too low to achieve the sustainable development standard. Medical insurance is a basic need and the survey shows that 76% of the sampled women were not medically insured. Usage of property insurance services was also very low with only 12% of women taking out property insurance and only 3% willing to take it if it was available. The majority of the sample could not bear the cost of insurance services or were unaware of its advantages even if they could afford to pay for it. Since more than 31% of the respondents were living in rural areas, agriculture insurance could be very important for their risk mitigation and hence financial inclusion. The results showed that the demand for this type of insurance services was very low (5%). More than 90% of the respondents were either not insured or did not know what this type of service provided. Agriculture insurance has become an essential tool for alleviating poverty in the rural areas. On average, the above results show that the respondents either lack the financial capacity to subscribe to the insurance services or lack enough literacy to demand it. There is also an implication that there is a large supply barrier in terms of insurance services so women may not have relevant products to use.

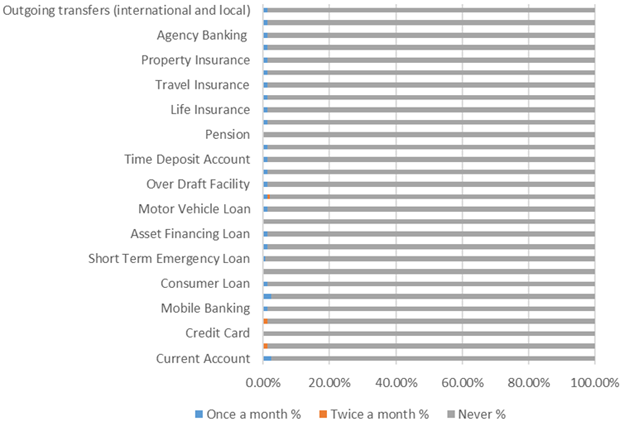

9. USAGE OF FINANCIAL SERVICES

Figure 5 shows the respondents’ self-reported frequency of using different financial products and services. Only the debit account and internet banking was used by 1.3% of the respondents twice a month, while other financial services such as a current account, mobile banking, and money transfer services were reportedly being used once a month. Mortgages, credit cards, business loans, and pensions were reported to not be used at all by the surveyed women. The low rate of usage of financial services as reflected in Figure 6 shows that the respondents have little or no enough money to circulate through the financial system.

Figure-5. Usage of Financial services.

Source: Author computation from the Financial Inclusion Structured Questionnaires.

The respondents were asked about what types of new products and services they would like to receive. The majority of the sample requested services that built capacity and awareness. 76.9% of the respondents indicated that they typically own a mobile phone and that they are ready to perform electronic financial transactions if they were available. 13.8% of those surveyed who held bank accounts used financial institution teller for their transactions, 6.2% used online banking, and only 3.1% used the ATM. This might indicate that either the usage of financial services in Comoros were associated with severe supply side barriers or that the women‘s lack of financial literacy has led them to follow the easiest and least costly options while using financial services.

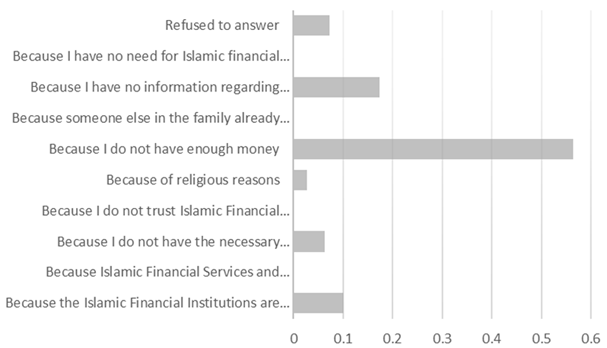

The results show that the surveyed women in Comoros have more difficulties in getting financial loans. More than 56% Figure 6 of them indicated that they do not have enough money. Hence, 81.4% of the respondents indicated that they had never taken out a loan, while 3.1% of the respondents indicated that they had taken out a loan of more than KMF 100,000 (USD 200). The average monthly loan repayment amount made by 9.3% of the respondents was reported to be less than KMF 1000 (USD 2); however, 2.1% of the respondents did report paying more than KMF 100,000 (USD200). When the respondents asked how they paid their loans, 50% used cash, 44.4% used mobile, and only 5.6% used direct debit from their accounts.

For disadvantaged and low-income women, the highest ranked reasons for taking out a loan were to cater for emergencies, to pay school fees, construction, and medical expenses. In terms of loan maturity, 22.2% of the respondents indicated that the maturity period for the loan was 3 months, while 11.1% indicated 48 months. 16.7% of the respondents indicated that the duration for loan approval was 3 days. 9.4% of the respondents required security when borrowing, with 23.1% stating that this security was often in the form of a title deed. 6.3% of the respondents had borrowed from family and friends within the past 12 months, 1.4% had borrowed from a private lender, and none had borrowed from their employer.

Figure-6. Reasons for not having Islamic Financial Institutions Account.

Source: Author computation from the Financial Inclusion Structured Questionnaires.

In term of whether the respondents were able to save part of their income, 62.7% of the sample reported saving nothing in a month, 24% saved less than KMF 1000 (USD 2), 12% saved between KMF 1000-5000 (USD 2 -10), and 1.3% saved between KMF 10,000-20,000 (USD 20 – 40). 68% of the respondents reported that there was no return on their savings, while 25.3% indicated that they earned less than KMF 1,000 (USD 2). Interestingly, 10.4% of the respondents reported that they had saved with an informal savings group in the past 12 months rather than with financial institutions. Informal saving is always a common safe haven for the disadvantaged people everywhere.

The respondents took lower loans and saved less than what is expected. The sample was asked whether the distance between their work and residence affected their weak usage of the financial institutions. 51.5% were living less than one kilometer away from a financial institution, while 91.1% of them reported that the distance did not affect whether they were a client or not or have a significant impact on what transactions they carried out. Again, this implies that the main reasons for not using the financial services by the surveyed women of Comoros were low income, poverty, lack of the right Islamic financial products, which are gender specific, and the lack of financial literacy.

10. CONCLUSION AND RECOMMENDATIONS

Access to financial services enables disadvantaged and low-income individuals and households such as the Comoros’ women to invest in activities that might earn them relatively good future income. This would allow them to pay for their family’s and kids’ medical care, education, and spending for welfare. This study investigated empowering women in Comoros through Islamic financial inclusion. To achieve the objectives, the study used structured questionnaires to collect primary data. The sample covered respondents randomly selected from women living in the outskirts of Moroni, the capital of Comoros, and Tsidje. Subsequently, more than four financial inclusion dimensions have been surveyed including: payment financial inclusion dimensions; borrowing financial inclusion dimensions; saving and investment financial inclusion dimensions; and insurance financial inclusion dimensions.

The study examined nine payment indicators which are related to ownership. Overall, the study found the level of means of payment ownership related to the surveyed women in Comoros and their immediate family to be very low with the exception of the current bank account (59%). Holding less means of payments might prevent Comoros women being granted effective access to the financial services.

The study also investigated the ability of the sample to borrow using nine borrowing financial services. Overall, the results also showed weak ability to borrow for all the categories in the sample for both women living in the city or its outskirts or rural areas (84% non-borrowers). This implies that both urban and rural women in Comoros face similar barriers whether a lack of financial services or shortage of income.

The third set of financial inclusion dimensions examined were saving and investment. These dimensions were important for empowering women to help them to grow and face any emergency need. Five saving and investment indicators were tested. As in the other financial inclusion dimensions, saving and investment also exhibit relatively low patterns. The average non-savers’ women on the sample were more than 75% relatively less than the average non-investors (82%). Insurance services are another important financial inclusion dimension that helps the disadvantaged women to mitigate risk. Agricultural and livestock insurance is vital for rural inhabitants. The low level of insurance demand among the respondents implies that either they lack the financial capacity to subscribe to insurance services or they lack financial literacy. It also implies potential supply side barriers from insurance companies plus the lack of gender specific insurance services products.

The study also examined the frequency usage of all the outgoing financial services across the dimensions. The study found that only the debit card and internet banking were used twice a month on an average and all the other financial services including the current account, mobile banking, and money transfer were used only once a month. When the respondents were asked about what new services they might need they identified services that would build capacity and awareness and wireless banking. Currently, the study shows that the respondents prefer to use the institution’s teller to online banking and the ATMs.

Finally, the results show that the respondents have more difficulties in getting financial loans. 81.4% of the respondents indicated that they never took out formal financial loans at all. Only 9.3% and 2.1% of the respondents indicated having an average monthly loan repayment of more than KMF 1000 (USD 2) and KMF 100,000 (USD200) respectively.

Those who stated their monthly loan repayments were considered more active compared to the rest of the sample. In this case the results imply that university graduate students could potentially be more active in increasing their low income and be financially included if they were well trained. The results also show that Comoro’s women have limited bank account ownership and the lowest usage of financial services. The limited ownership and lack of financial services can be attributed to the shortages of financial resources and financial literacy. More than 56% of the respondents when asked why they would not use financial services stated that they had no money while the study showed that Comoros women have a low financial literacy preventing them owning and using financial services Hence, based on the results of this study, one can conclude that empowering Comoros women via financial inclusion requires removing barriers so that they can access Islamic financial services. Our findings suggest that the goal of improving Comoros’ women financial inclusion should be pursued through top government policies. As the majority is Muslim women, the focus might be on improving gender access to Islamic financial services, particularly through social inclusion tools such as Zakat, Wagf, and Sadagah together with a multilateral financial inclusion program such as that adopted by the Islamic Development Bank Group (IDBG) and the Central Bank of Sudan. Additionally, the research recommends the intervention of IRTI and the relevant department within the IDBG to design effective capacity building programs to improve Comoros’ women’s financial awareness and literacy.

| Funding: This study received no specific financial support. |

| Competing Interests: The author declares that there are no conflicts of interests regarding the publication of this paper. |

REFERENCES

CGAP Women and Financial Inclusion, 2015. Available from http://www.cgap.org/topics/women-and-financial-inclusion .

Demirgüç-Kunt, A., D. Singer, S. Ansar and J. Hess, 2017. The global findex database, measuring financial inclusion and the fintech revolution. Available from http://globalfindex.worldbank.org/ .

Finnegan, G., 2015. Discussion paper in strategies for women’s financial inclusion in the commonwealth. Printed and Published by the Commonwealth Secretariat.

Global Partnership for Financial Inclusion (GPFI), 2016. Report on G20 Financial Inclusion Indicators. Available from https://www.gpfi.org/sites/default/files/Indicators%20note_formatted.pdf .

Triki, T. and I. Faye, 2013. Financial inclussion in Africa. African Development Bank. Available from https://www.afdb.org/fileadmin/uploads/afdb/Documents/Project-and-perations/Financial_Inclusion_in_Africa.pdf .

United Nations Report, 2015. Addis Ababa Action Agenda of the Third International Conference on Financing for Development. Available from https://www.un.org/esa/ffd/wp-content/uploads/2015/08/AAAA_Outcome.pdf .

Zottel, S. and F. Khoury, 2016. Enhancing financial capability and inclusion in Senegal: A demand-side survey (English). Finance and markets global practice. Washington, D.C.: World Bank Group.

Websit link

- https://en.wikipedia.org/wiki/Economy_of_the_Comoros

- https://en.wikipedia.org/wiki/Comoros

- http://www.heritage.org/index/country/comoros

- http://www.uncdf.org/en/Comoros-Islands

- http://fic.wharton.upenn.edu/fic/africa/Comoros%20Final.pdf

- https://www.afdb.org/en/countries/east-africa/comoros/comoros-economic-outlook/

Views and opinions expressed in this article are the views and opinions of the author(s), International Journal of Asian Social Science shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |