CREDIT RISK AND FINANCIAL STABILITY UNDER CONTROLLING EFFECT OF FINANCIAL SECTOR DEVELOPMENT: A STUDY FROM BANKING SECTOR OF GCC MEMBERS

The Public Authority for Applied Education & Training, The College of Business Studies, State of Kuwait

ABSTRACT

The purpose of this study is to analyze the effect of five indicators of credit risk on four financial stability measures under the title of return on assets, return on equity, Z-Score of ROA, and ROE. While economic growth, inflation and financial sector development are added as control variables. Based on the sample of top 20 banks in GCC, regression models are developed for the financial stability, credit risk indicators and control variables. It is observed that NPLs (credit risk indicator) to gross advances is significantly impacting on all stability measures. While, the impact of non-performing loans to equity ratio on stability is also significant for the whole sample. Under first sub sample of top 10 banks, both non-performing loans to gross advances and provision against NPLs are significant determinants to create instability in the banks. Besides, effect of NPLs to equity ratio is found to be negatively significant for both ROA and ROE under 2nd sub sample of the study. The effect of financial sector development is positively significant for the banking sector stability in both full and sub samples. Contribution of the study can be viewed from both theoretical and practical context as it is a very first attempt to consider credit risk indicators, stability measures, financial sector development and economic growth for Gulf states. Core limitations covers the limited sample size and focus on the present decade which can be reconsidered with better sampling and adding the time duration of last decade as well.

Keywords:Financial stability, Credit risk, Non-performing loans, Financial sector development, GCC.

ARTICLE HISTORY: Received:12 October 2018 Revised:16 November 2018 Accepted:24 December 2018 Published:10 January 2019 .

Contribution/ Originality:This study contributes in the existing literature from the context of credit risk and its integration with financial stability. Earlier studies have done their focus on emerged economies while GCC member states are not reasonable addressed.

1. INTRODUCTION

The idea of financial stability covers the concept of systematic risk to the business organizations. It refers to the current financial situation, based on the various economic and financial gauges, both in the relevant industry and overall economy. During the time of 2007, world economy has suffered the issue of financial crisis, known as the biggest in its severity after the great depression of 1930s. Business firms like banks and financial organizations are putting their significant attention towards their stability which can secure them form uneven financial situations. Both industry specific and regional economic indicators can put their significant influence for the banking firms to disturb their stability, hence creating financial anomalies. In overall financial system, significance of banking sector is very much crucial as it is known as the back bone to the economy. Therefore, attention is required towards the financial stability and its key indicators which can define the growth and sustainability of the banking firms. As per the review of present and past literature, financial stability is of deep concern to the reserachers and financial analysts, related to the banking sector. Various measures have been observed to explain the idea of banking firm’s stability. For instance, it can be measured through performance proxies like return on assets, return on equity, liquidity position and capital adequacy ratio. However, Z-score is found to be among the top priorities for the reserachers while dealing with the stability of the banks in financial terms.

Significant literature work is provided to explain the idea of financial stability and its determination through bank-based risk factors. Among the significant determinants, role of liquidity risk (shortage of cash to full fill day to day expenditure), credit risk in the form of low asset quality, operational risk like higher operating cost with weak internal controls, and market risk like higher cost of borrowing the funds are in continuous observation. Due to interdepdency of financial sector both in the world and regional economies, it is observed that higher systematic risk pressure is causing a lower stability for the banks. Meanwhile, credit risk is known as the key indicators to analyze the assets quality of the banks as it deals with the provision of loans to both public and private sectors in the economy. Among the significant proxies, non-performing loans (NPLs) are of great importance in the financial literature. In this regard, the association between credit risk indicators like NPLs and financial stability have been observed as key contribution in the present study due to missing consideration in the literature. NPLs considers the value of those amount of loans which are provided by the banks, but due to some financial crisis or other reasons, borrowers are unable to repay the loan amount over more than 90 days as per banking schedule. Higher value of the NPLs in the balance sheet of the banks reflects their poor risk management practices specifically from the context of advances to the borrowers, hence leads to the lower stability.

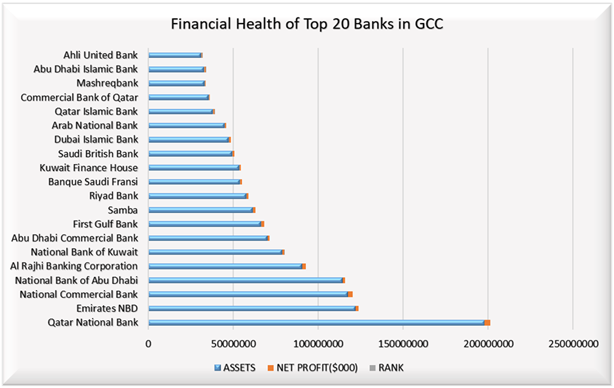

In addition, impact of economic indicators like financial sector development, growth in the economy and level of inflation indicates both positive and negative impression on banks. Sophisticated economic activities and financial growth in the economy lead to the better banking results and more stability for to face uneven financial hurdles. However, from the context of empirical association between credit risk and financial stability measures, controlling the effect of financial and economic growth provides some actual empirical facts. Based on this assumption, this study attempts to explore the relationship between credit risk factors and financial stability for Gulf corporation council (GCC). After reviewing the literature, it is observed that association between financial stability, credit risk indicators based on the controlling effect of financial sector and economic development is not under attention in the Gulf region. Therefore, this study is going to cover this gap through empirical exploration between the targeted variables. In recent time, numerous public and private sector banks are providing their operational services in GCC. Figure 1 explains the financial health of top 20 banking firms. It is observed that Qatar national bank is found to be 1st in ranking regarding Net Profit and Assets Valuation. While Emirates NBD is at 2nd ranking as measured through the growth factors of assets and earnings. Financial position for the rest of the banking firms in presented in figure below.

The rest of the pattern for this study is as follows. Present section is providing an overview of the topic. Section two describes the critical review of literature and contribution from the earlier findings. Section three deals with the operationalization of the variables. Section four provides research methods. Section five deals with empirical findings and discussion. Last section pacts with the conclusion and future implication of the study.

This study contributes in the existing literature from three perspectives. At first, this paper examines the role of credit risk indicators through NPLs and their impact on the stability of banking firms in financial terms. At second, controlling effect of economic growth, financial sector development and inflation is observed for both credit risk and financial stability from GCC members, which considers as the first effort in the literature. At third, GCC top banking firms have not very under appropriate attention of the reserachers and little contribution is available in present literature.

Figure-1. Financial Health of top 20 banks in GCC

Source: Gulf Business (2018![]() )

)

2. REVIEW OF LITERATURE

From the context of financial sector, like banks, plenty of literature work is provided regarding financial stability and its key determinants. However, much attention is paid towards the developed economies and significant space is yet to be covered from the context of developing and emerging economies. For instance, study of Bouheni and Hasnaoui (2017![]() ) has focused on 722 commercial banking firms, working in the region of Eurozone during the time of 1999 to 2013. To analyze the empirical relationship, generalized method of moments or GMM technique is applied for the stability and its link with the cyclical behavior of the banks. Findings of their study explains that there is a strong negative association between the risk-taking approach of the banks and business cycle, which assumes that financial stability is procyclical in the selected banks. Besides, their study explains that lending activities of the banks have been increased after the risk-taking behavior of the banks which indicate their positive and co-movements in the selected regions. However, they have noticed that both cyclical behavior and risk-taking actions significantly depend on the size of the lending activities. In addition, they have assumed that there is a significant impact of bailout programs on financial stability of selected banks. Another study conducted by Goodhart (2006

) has focused on 722 commercial banking firms, working in the region of Eurozone during the time of 1999 to 2013. To analyze the empirical relationship, generalized method of moments or GMM technique is applied for the stability and its link with the cyclical behavior of the banks. Findings of their study explains that there is a strong negative association between the risk-taking approach of the banks and business cycle, which assumes that financial stability is procyclical in the selected banks. Besides, their study explains that lending activities of the banks have been increased after the risk-taking behavior of the banks which indicate their positive and co-movements in the selected regions. However, they have noticed that both cyclical behavior and risk-taking actions significantly depend on the size of the lending activities. In addition, they have assumed that there is a significant impact of bailout programs on financial stability of selected banks. Another study conducted by Goodhart (2006![]() ) has focused on the context of financial stability development for the banking firms, working in the region of England during the time of 2002 to 2004. Based on the modelling of stress testing, it is observed that banking sector stability is purely link to the overall system in the economy, not just to the individual banking firm activities. He has explained that there is strong need towards the development of some appropriate models, addressing the issue of financial stability based on the various risk measures like liquidity and capital adequacy.

) has focused on the context of financial stability development for the banking firms, working in the region of England during the time of 2002 to 2004. Based on the modelling of stress testing, it is observed that banking sector stability is purely link to the overall system in the economy, not just to the individual banking firm activities. He has explained that there is strong need towards the development of some appropriate models, addressing the issue of financial stability based on the various risk measures like liquidity and capital adequacy.

Diallo and Al-Mansour (2017![]() ) explain the concept of shadow banking, financial sector stability and insurance giant in the region of America (American International Group or AIG). They have empirically examined the collapse of insurance sector, based on factors of financial stability across various countries and shadow banking system. To measure the stability, Z-score is considered during the time of 1998 to 2011 with economic growth. They have found that insurance sector in the selected region is negatively associated with the financial stability and it is determinantal for the countries which higher level of shadow banking assets. Another work conducted by Fu et al. (2014

) explain the concept of shadow banking, financial sector stability and insurance giant in the region of America (American International Group or AIG). They have empirically examined the collapse of insurance sector, based on factors of financial stability across various countries and shadow banking system. To measure the stability, Z-score is considered during the time of 1998 to 2011 with economic growth. They have found that insurance sector in the selected region is negatively associated with the financial stability and it is determinantal for the countries which higher level of shadow banking assets. Another work conducted by Fu et al. (2014![]() ) indicates the fact that financial stability is of core interest for the policy makers and academic writers since 2007; time of financial crisis in the world economy. To analyze the factor of financial stability in 14 economies of Asia Pacific during the time of 2003 to 2010, they have considered concentration, banking regulations and competition for the banks. Findings of their study indicate that banking sector stability through Z-score measure have been influenced by the concentration, regulatory and banking sector institutional framework. Meanwhile the impact of some macro factors is controlled while taking the association between financial stability and its determinants.

) indicates the fact that financial stability is of core interest for the policy makers and academic writers since 2007; time of financial crisis in the world economy. To analyze the factor of financial stability in 14 economies of Asia Pacific during the time of 2003 to 2010, they have considered concentration, banking regulations and competition for the banks. Findings of their study indicate that banking sector stability through Z-score measure have been influenced by the concentration, regulatory and banking sector institutional framework. Meanwhile the impact of some macro factors is controlled while taking the association between financial stability and its determinants.

Guy and Lowe (2011![]() ) have considered the value of credit risk and assets quality through NPls as a key measure. They have explained the fact that higher level of NPls ratio in the banking firms reflects greater credit risk exposure. To analyze the association between the NPLs and financial stability measure, regional economic variables are also under observation. Using the panel data approach, it is found that both aggregate and at individual level relationship between credit risk indicators and financial stability exists. Besides, value of loan delinquency remains to be in for future time for the selected banks, hence banking sector will be resilient for the financial and real shocks in the economy.

) have considered the value of credit risk and assets quality through NPls as a key measure. They have explained the fact that higher level of NPls ratio in the banking firms reflects greater credit risk exposure. To analyze the association between the NPLs and financial stability measure, regional economic variables are also under observation. Using the panel data approach, it is found that both aggregate and at individual level relationship between credit risk indicators and financial stability exists. Besides, value of loan delinquency remains to be in for future time for the selected banks, hence banking sector will be resilient for the financial and real shocks in the economy.

From the context of credit risk management, various studies have provided both theoretical and empirical contribution. For instance, Fatemi and Fooladi (2006![]() ) have examined the idea of credit risk management in large banking firms of US. They have argued that for the banking sector in recent year, credit risk management is observed as a significant obligation in overall financial matters. Based on the questionnaire survey, primary data is collected for top 100 banking firms, currently working in the region of USA. Findings of their study indicates the fact that default risk is the most significant factor, which needs significant attention from the management of selected banks. Besides, to analyze the credit risk exposure, some banking firms are focusing on the concept of vendor-marketed model as compare to own in-house model. Their findings help to understand the perceived importance of credit risk in US banking. Another study conducted by Ghosh (2017

) have examined the idea of credit risk management in large banking firms of US. They have argued that for the banking sector in recent year, credit risk management is observed as a significant obligation in overall financial matters. Based on the questionnaire survey, primary data is collected for top 100 banking firms, currently working in the region of USA. Findings of their study indicates the fact that default risk is the most significant factor, which needs significant attention from the management of selected banks. Besides, to analyze the credit risk exposure, some banking firms are focusing on the concept of vendor-marketed model as compare to own in-house model. Their findings help to understand the perceived importance of credit risk in US banking. Another study conducted by Ghosh (2017![]() ) also focused on the key factors and their association with the credit risk in the form of NPLs. The time duration of the study is based on fourth quarter of 1992 to first quarter of 2016 while adding the sector specific and regional economic indicators. Findings of their study indicates that most pronounced effect on NPLs is recorded through housing price in US. Besides, the effect of economic growth through GDP cannot neglectable for the strategic planning. Duffie (2008

) also focused on the key factors and their association with the credit risk in the form of NPLs. The time duration of the study is based on fourth quarter of 1992 to first quarter of 2016 while adding the sector specific and regional economic indicators. Findings of their study indicates that most pronounced effect on NPLs is recorded through housing price in US. Besides, the effect of economic growth through GDP cannot neglectable for the strategic planning. Duffie (2008![]() ) explains the concept of credit risk through its innovation and implication for the definition of financial stability. While Goodhart (2005

) explains the concept of credit risk through its innovation and implication for the definition of financial stability. While Goodhart (2005![]() ) has empirically investigated the relationship between financial regulations, credit risk and financial stability. They have explained that although a recent development for the monetary policy along modelling of systematic risk management for better financial stability. But the problem of sustaining the financial stability is still an ongoing phenomenon. In the risk management framework of banking sector, the role of Basel regulations is very important which deals with the credit risk mechanism while taking the contemporary trends in banks. Some other studies examine the relationship between credit risk indicators, financial stability and growth in various economies (Crockett, 2000

) has empirically investigated the relationship between financial regulations, credit risk and financial stability. They have explained that although a recent development for the monetary policy along modelling of systematic risk management for better financial stability. But the problem of sustaining the financial stability is still an ongoing phenomenon. In the risk management framework of banking sector, the role of Basel regulations is very important which deals with the credit risk mechanism while taking the contemporary trends in banks. Some other studies examine the relationship between credit risk indicators, financial stability and growth in various economies (Crockett, 2000![]() ; Wagner and Marsh, 2006

; Wagner and Marsh, 2006![]() ; Duffie, 2008

; Duffie, 2008![]() ; Acharya et al., 2014

; Acharya et al., 2014![]() ; Acemoglu et al., 2015

; Acemoglu et al., 2015![]() ; Ghosh, 2015

; Ghosh, 2015![]() ; Dell'Ariccia, 2016

; Dell'Ariccia, 2016![]() ; Morgan and Pontines, 2018

; Morgan and Pontines, 2018![]() ).

).

2.1. Variables Descriptions and Hypotheses development

2.1.1. Credit Risk/ Non-Performing Loans (NPLs)

In financial statements of banking sector, quality of assets is reflected through value of non-performing loans. Similar measure is observed to replicate the concept of credit risk for both domestic and foreign banks in any region. The value of NPls is explained as loan on which the debtor of the money has not made the schedule payment over 90 days for the commercial loans and for 180 in case of consumer loans (Ghosh, 2015;2017![]() ). Non-performing means that a specific amount of loan has stopped its interest, principal or both payments during a stated time (Armstrong et al., 2015

). Non-performing means that a specific amount of loan has stopped its interest, principal or both payments during a stated time (Armstrong et al., 2015![]() ). Various measures have been presented in existing literature to reflect the concept of credit risk/asset quality through NPLs. For instance, the ratio of NPLs to gross advances can be a key indicator as explained by Ihsan and Jadoon (2016

). Various measures have been presented in existing literature to reflect the concept of credit risk/asset quality through NPLs. For instance, the ratio of NPLs to gross advances can be a key indicator as explained by Ihsan and Jadoon (2016![]() ). It uses to explain the amount of NPLs with the ratio of gross advances by the banking firms. Higher this ratio reflects more problem of credit risk and vice versa. Another measure of NPLs in banking sector is the provision against NPLs to gross advances (Saba et al., 2015

). It uses to explain the amount of NPLs with the ratio of gross advances by the banking firms. Higher this ratio reflects more problem of credit risk and vice versa. Another measure of NPLs in banking sector is the provision against NPLs to gross advances (Saba et al., 2015![]() ; Umoren et al., 2016

; Umoren et al., 2016![]() ). It represents the portion of total provision set aside by the bank to settle the NPLs in their books of accounts. Meanwhile, ratio of NPLs to shareholder equity indicates the comparison of credit risk and total stockholder’s equity portion in the balance sheet (Wahid et al., 2015

). It represents the portion of total provision set aside by the bank to settle the NPLs in their books of accounts. Meanwhile, ratio of NPLs to shareholder equity indicates the comparison of credit risk and total stockholder’s equity portion in the balance sheet (Wahid et al., 2015![]() ). Besides, two other measures like NPLs write off to NPLs provisions, and provision against NPLs to NPLs ratios are under researchers attention to define the overall value of credit risk in the banking sector (Jassaud and Kang, 2015

). Besides, two other measures like NPLs write off to NPLs provisions, and provision against NPLs to NPLs ratios are under researchers attention to define the overall value of credit risk in the banking sector (Jassaud and Kang, 2015![]() ; Saba et al., 2015

; Saba et al., 2015![]() ). All these measures are under observation in the present study to explain the credit risk in selected banks.

). All these measures are under observation in the present study to explain the credit risk in selected banks.

2.2. Financial Stability (FS)

Financial stability assumes a condition where all the key role players in overall financial market work in a smooth structure and can absorb uneven financial shocks. Higher financial stability reflects better risk management by the business firms like banks and more efficiency of the risk managers. Besides, measure of financial stability is used for both overall economy and for the banking industry. However, focus of literature is significantly towards the banking stability. Various dimensions are presented in the present literature for FS. For instance, return on assets, return on equity, Z-Score of return on assets, and Z-Score through return on equity are mostly cited in empirical research (Hidayat et al., 2016![]() ; Board, 2017

; Board, 2017![]() ; Pisedtasalasai and Rujiratpichathorn, 2017

; Pisedtasalasai and Rujiratpichathorn, 2017![]() ). However, measurement through Z-Score reflects the standard deviation in the return on both equity and assets with the capital ratio of the banking firms over time.

). However, measurement through Z-Score reflects the standard deviation in the return on both equity and assets with the capital ratio of the banking firms over time.

2.3. Control Variables

2.3.1. Financial Sector Development (FSD)

A large body of literature has suggested that financial sector development plays a huge role for the economic health and stability. It defines the capital accumulation through increasing in saving rates, production of investment related information in the economy, and encouraging the flow of foreign capital. Those countries having better financial development tends to have significant growth and faster financial stability in small and medium enterprise as it provides them the access to finance. Various measures have been presented in the literature to reflect the concept of FSD. For instance, ratio of assets of financial institutions to the GDP indicates FSD (Le et al., 2016![]() ; Otchere et al., 2017

; Otchere et al., 2017![]() ). Present study has considered this ratio as a key measure to reflect financial sector development with its controlling effect for credit risk and financial stability.

). Present study has considered this ratio as a key measure to reflect financial sector development with its controlling effect for credit risk and financial stability.

2.4. Gross Domestic Product (GDP)

The value of gross domestic product (GDP) considers the total production of goods and services in the economy over a specific time. It indicates the economic growth in the country while taking the personal consumption expenditure with the investment of business, Government spending and net exports over same time duration (Murry and Nan, 1994![]() ; Sutton et al., 2007

; Sutton et al., 2007![]() ). Better economic growth in the country will lead to the better stability in the financial markets to control its effect, present study has considered the GDP as a 2nd control variable to analyze the relationship between credit risk and financial stability in selected banks.

). Better economic growth in the country will lead to the better stability in the financial markets to control its effect, present study has considered the GDP as a 2nd control variable to analyze the relationship between credit risk and financial stability in selected banks.

2.5. Inflation (INF)

Rate of inflation reflects the gradual increase in the prices of goods and services of the economy during a period. It is known as the quantitative measure of average prices of all the items and their relative variation in the economy (Krugman, 2008![]() ). The factor of inflation decreases the purchasing power of the consumers in the economy. Higher inflation in the economy means low purchasing power with the adverse impact stability of the economy and business firms working in it. Therefore, present study has controlled the effect of inflation to analyze the robust relationship between the credit risk and financial stability in banking firms of GCC.

). The factor of inflation decreases the purchasing power of the consumers in the economy. Higher inflation in the economy means low purchasing power with the adverse impact stability of the economy and business firms working in it. Therefore, present study has controlled the effect of inflation to analyze the robust relationship between the credit risk and financial stability in banking firms of GCC.

2.6. Regression Models and Method of Analysis

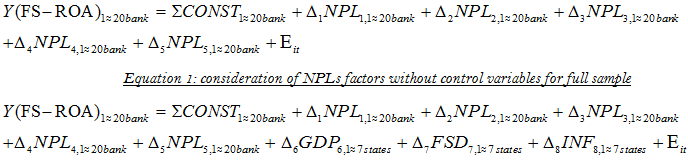

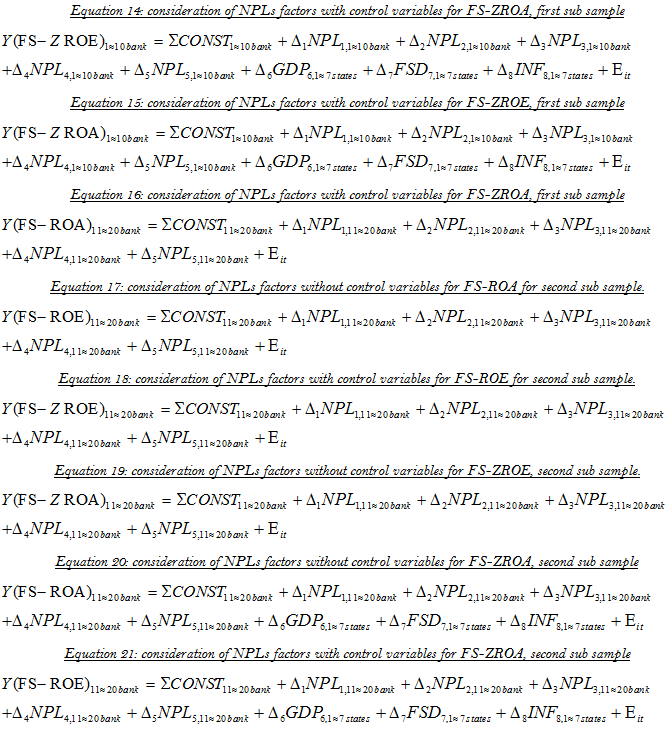

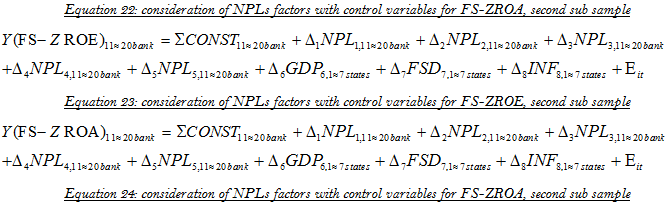

To examine the association between financial stability and credit risk indicators, following regression equations have been developed. For the first equation, effect of credit risk indicators (NPL ratios 1-5) have been examined, without controlling the effect of FSD, GDP and INF. For the equation 1 & 2, ROA is assumed as key determinant of financial stability. While equation 2 indicates the effect of NPLs ratios with control variables of the study.

Equation 2: consideration of NPLs factors with control variables for FS-ROA for full sample

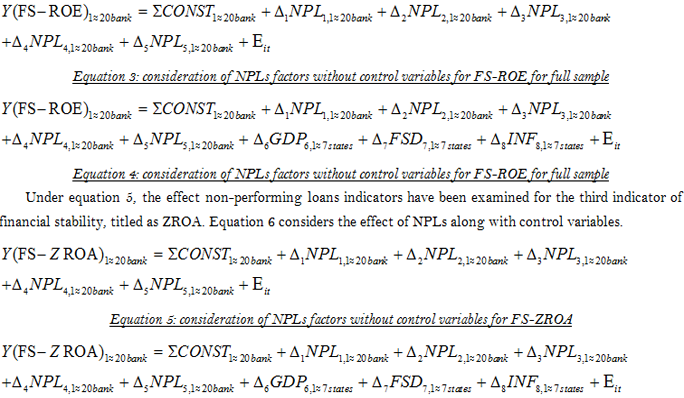

Under equation 3 & 4, effect of credit risk indicators along with control variables is observed for ROE; 2nd proxy for financial stability for the whole sample of 20 banks. For equation, 5 & 6, financial stability is examined through Z-score which is the most cited measure in the banks as explained by Gamaginta (2015![]() ) ; Soedarmono et al. (2011;2013

) ; Soedarmono et al. (2011;2013![]() ) ; Stiroh (2004

) ; Stiroh (2004![]() ) ; Trinugroho et al. (2017

) ; Trinugroho et al. (2017![]() ) .

) .

Equation 6: consideration of NPLs factors without control variables for FS-ZROA

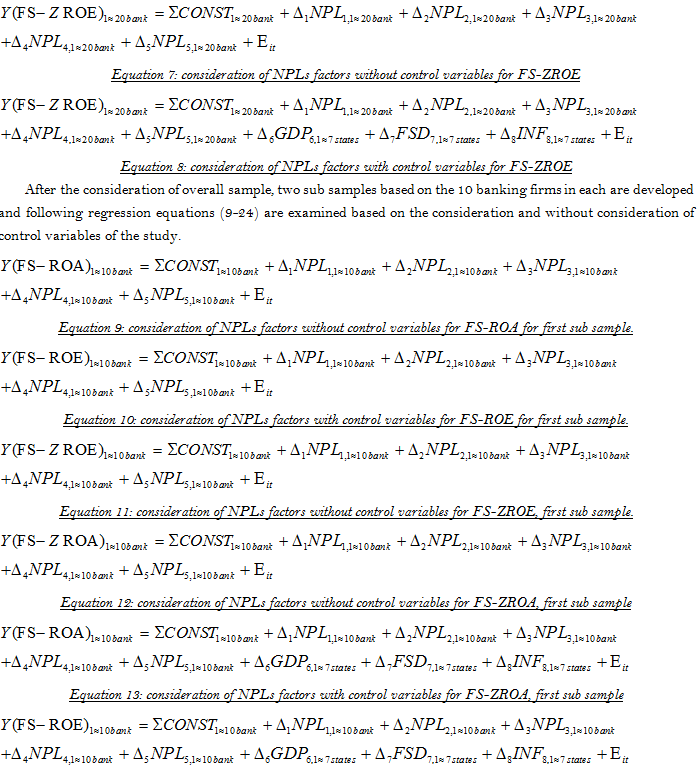

Equation 7 & 8 explains the effect of asset quality factors (NPLs) for the fourth indicator of financial stability; ZROE, and for the control variables respectively. The effect of unobserved factors is under observation through error factors of the model, entitled as E for entities (i) and time period (t). Besides Equation 9 and 10 reflects the econometric relationship between financial stability through ROA and ROE for first sub sample (1-10 banks).

The above stated econometric equations will be empirically examined through multivariate multiple regression approach which deals with the various indicators of financial stability (ROA, ROE, FS-ROA, FS-ROE) and credit risk determinants. It considers the coefficients for outcome factors through explanatory variables of the study. The findings for the multivariate analysis considers the descriptive statistics, correlational analysis and finally the empirical findings. Descriptive analysis will explain the characteristics and trends of the dataset. While the focus of correlation is to explain the strength and direction of association between the variables of the study. Finally, regression findings indicate the causal association between explanatory and outcome factors, while controlling the effect of economic growth, FSD, and inflation.

3. RESULTS AND DISCUSSIONS

Descriptive results are presented under table 1, while considering the mean score for dependent, explanatory and controlled variables of the study. For dependent variables, mean score for ROA is 6.360 explains that on average top 20 banking firms in the region of GCC. For ROE, mean score of 8.299 indicates a reasonable trend of financial stability, based on the return on their equity. An average deviation between the mean score of ROA and ROE of .954 and 1.681 is observed, indicating a low value of dispersion. For ZROA, average trend of 2.81 is observed in overall 20 banking firms of Gulf, with the standard deviation of 3.520. For ZROE, this trend is 4.89 for the average score and for deviation from the mean is 1.380 respectively. For the NPLs, five proxies as explained in the variable section are added and reviewed for descriptive and regression findings. The mean score for NPL2GA is 5.128 with the deviation value of .237. For provision against NPLS, the value of mean is 8.034 and standard deviation of .027 respectively. The highest mean score is observed for the ROE, while lowest belongs to inflation; 2.782. The maximum value of risk factor in mean score is observed for ZROE and lowest for PNPL; .027.

Table-1. Descriptive Findings

Variable |

Obs |

Mean |

Std.Dev. |

Min |

Max |

ROA |

140 |

6.36 |

0.954 |

0.081 |

4.33 |

ROE |

140 |

8.929 |

1.681 |

0.106 |

13.1 |

ZROA |

140 |

2.81 |

3.52 |

0.56 |

6.901 |

ZROE |

140 |

4.89 |

1.38 |

3.329 |

3.27 |

NPL2GA |

140 |

5.128 |

0.237 |

0.017 |

0.852 |

PNPL |

140 |

8.034 |

0.027 |

0.025 |

0.112 |

NPLTE |

140 |

2.503 |

0.214 |

0.917 |

0.993 |

NPLW_P |

140 |

9.098 |

0.053 |

0.965 |

0.263 |

PANPLs |

140 |

6.019 |

0.017 |

0.631 |

0.091 |

GDP |

140 |

6.006 |

5.494 |

1.594 |

20.514 |

FSD |

140 |

3.841 |

1.991 |

2.163 |

7.667 |

INFL |

140 |

2.782 |

4.409 |

1.233 |

6.286 |

Table 2 expresses the findings for pairwise correlation coefficient between both explanatory and explained factors of the study. under correlation findings, ROA has a higher value of association with the GDP, EXP. and Inflation. While the factor of ROE is highly correlated with ZROE, ZROA as well. Its association with NPLS item 4 and 5 is found to be weak and for NPL3 it is low. For the correlation between ZROA and ZROE, highly positive association is observed. In addition, correlation coefficient between NPL2GA and ZROE is .648, and for GDP is .928 which is positive and high. While the relationship between NPLTE and GDP is -.723, indicating a negative but good correlation. It explains that both the factors of NPLs against equity ratio is highly but negatively associated to each other. Meanwhile, GDP, and provision against NPLS are positively associated. The rest of the indicators are explaining a mixed trend in terms of correlation coefficient.

Table-2. Pairwise Correlations

Variables |

-1 |

-2 |

-3 |

-4 |

-5 |

-6 |

-7 |

-8 |

-9 |

-10 |

-11 |

-12 |

(1) ROA |

1 |

|||||||||||

(2) ROE |

0.358 |

1 |

||||||||||

(3) ZROA |

0.291 |

0.914 |

1 |

|||||||||

(4) ZROE |

0.612 |

0.823 |

0.91 |

1 |

||||||||

(5) NPL2GA |

0.862 |

0.392 |

0.31 |

0.648 |

1 |

|||||||

(6) PNPL |

0.624 |

0.415 |

0.352 |

0.584 |

0.732 |

1 |

||||||

(7) NPLTE |

-0.751 |

-0.23 |

-0.163 |

-0.466 |

-0.752 |

-0.581 |

1 |

|||||

(8) NPLW_P |

-0.537 |

-0.203 |

-0.151 |

-0.377 |

-0.587 |

-0.329 |

0.397 |

1 |

||||

(9) PANPLs |

0.667 |

0.458 |

0.38 |

0.641 |

0.71 |

0.761 |

-0.591 |

-0.403 |

1 |

|||

(10) GDP |

0.877 |

0.305 |

0.229 |

0.584 |

0.928 |

0.624 |

-0.723 |

-0.582 |

0.632 |

1 |

||

(11) FSD |

0.84 |

0.238 |

0.163 |

0.516 |

0.807 |

0.547 |

-0.732 |

-0.572 |

0.536 |

0.974 |

1 |

|

(12) INF |

0.786 |

0.466 |

0.388 |

0.68 |

0.712 |

0.739 |

-0.683 |

-0.55 |

0.792 |

0.759 |

0.703 |

1 |

Table 3 presents the findings for econometric equation 1 &2. For the equation 1, effect of NPLs indicators is examined without considering the controlling effect of financial sector development, GDP and inflation. It is observed that financial stability indicator (ROA), has a significant and negative association with non-performing loans to gross advances. It assumes that higher level of credit risk under NPLs is putting an adverse and significant impact on FS-ROA. For provision against NPLS, effect of -2.887 with the standard error of 1.488 is observed respectively. It also assumes the same impact as observed under the first indicator of non-performing loans. For NPLs ratio of equity amount, coefficient of -1.029 indicates that increasing level in the credit risk causing a decline in the value of FS-ROA.

This effect is consistent under the NPLs ratio for the write off amount with the coefficient of -.974 and standard error of .503. However, the effect of PANPLs is found to be positive but insignificant for ROA under full sample of the study. findings for the equation 2 consider the combine effect of credit risk indicators and for the control variables of the study. with the addition of control variables, the effect of NPLTE is positive and highly significant for ROE while rest of the indicators are found to be insignificant for the financial stability. Among the control variables, effect of financial sector development (FSD) and GDP is significantly positive for the banking sector stability. It shows higher economic activities and development in the financial sector leads to more stability for the banks in recent years. While the effect of inflation is found to be insignificant among the control variables for the whole sample of the study. The value of R-square for model 1 is .778, explains a good variation in FS-ROA while for model 2, this effect is .882; a slight higher comparatively to the model 1 due to the addition of FSD, GDP and Inflation in the model.

Table-3. Findings for Equation 1 & 2 (Full Sample)

-1 |

-2 |

|

VARIABLES |

FS-ROA |

FS-ROA |

NPL2GA |

-2.528*** |

0.347 |

-0.634 |

-0.875 |

|

PNPL |

-2.887* |

0.542 |

-1.488 |

-1.227 |

|

NPLTE |

-1.029*** |

0.399*** |

-0.269 |

-0.138 |

|

NPLW_P |

-0.974* |

0.804 |

-0.503 |

-0.321 |

|

PANPLs |

7.162 |

2.163 |

-7.748 |

-21.64 |

|

GDP |

1.159* |

|

-0.0954 |

||

FSD |

0.936*** |

|

-0.184 |

||

INFL |

1.075 |

|

-0.0837 |

||

Constant |

0.611** |

1.599* |

-0.247 |

-0.395 |

|

Observations |

140 |

140 |

R-squared |

0.776 |

0.822 |

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Table 4 explains the findings for the 2nd indicator of financial stability, observed through return on equity for the whole sample. The process for the findings is same as the one presented under table 2; without and with control variables. The effect of NPL2GA is -3.911 indicating a negative and significant impression for FS-ROE with the standard error of 1.93 approximately. For NPLTE the effect on FS-ROE is found to be -3.341 with the standard error of 1.9, assumed a negative but significant effect. The effect for the rest of the indicator of credit risk is found to be insignificant for the stability measures of banking firms in GCC. With the presence of control variables, it is observed that none of the credit risk indicator is significantly affecting financial stability of banks. However, the effect of FSD and GDP is positive and significant with the coefficient of 2.78 and 12.265 respectively. The explanatory power for 2nd stability measure of ROE is .241 for model 3 and .275 for model 4, explaining a weak coefficient of determination.

Table-4. Findings for Equation 3 & 4 (Full Sample)

-3 |

-4 |

|

VARIABLES |

FS-ROE |

FS-ROE |

NPL2GA |

-3.911** |

5.514 |

-1.9311 |

-1.15 |

|

PNPL |

149,665 |

5.475 |

-103,774 |

-1.963 |

|

NPLTE |

-3.341* |

2.837 |

-1.98 |

-2.876 |

|

NPLW_P |

22.464 |

20.375 |

-2.295 |

-1.284 |

|

PANPLs |

1.244 |

3.804 |

-4.255 |

-5.511 |

|

GDP |

2.786*** |

|

-4.157 |

||

FSD |

12.265** |

|

-10.55 |

||

INFL |

1.702 |

|

-4.046 |

||

Constant |

-38,083* |

-24.944** |

-19.603 |

-18.332 |

|

Observations |

140 |

140 |

R-squared |

0.241 |

0.275 |

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Findings for equation five and six are presented under table 5 for the third measure of financial stability through Z-Score. In the recent time, the trends of banking firms have been shifted towards the stability and various measures have been considered. However, Z-Score is the most cited indicator in the present and contemporary literature.

Table-5. Findings for Equation 5 & 6 (Full Sample)

-5 |

-6 |

|

VARIABLES |

FS-ZROA |

FS-ZROA |

NPL2GA |

-2.376*** |

-5.015** |

-2.512 |

-1.1701 |

|

PNPL |

1.623 |

6.021 |

-1.039 |

-1.481 |

|

NPLTE |

3.459* |

2.091** |

-1.8921 |

-2.745 |

|

NPLW_P |

4.571 |

2.424 |

-0.071 |

-0.332 |

|

PANPLs |

6.011 |

2.479 |

-4.598 |

-3.028 |

|

GDP |

4.716 |

|

-4.58 |

||

FSD |

12.9781*** |

|

-1.007 |

||

INF |

16.719* |

|

-4.842 |

||

Constant |

3.63123* |

2.2920** |

-1.277 |

-1.042 |

|

Observations |

140 |

140 |

R-squared |

0.501 |

0.625 |

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

The effect of NPL2GA on ZROA under both the equation five and six is negatively significant at 1 percent and 5 percent level of significance. While the value of standard error is 2.512 and 1.1701. however, the effect of PNPL is insignificant under both models as presented in table 5. For NPLTE, positive and significant effect for stability through ZORA is examined as per the whole sample. The effect on FS-ROA through FSD is 12.9781 is positive and significant at 1 percent, while for the GDP the effect is insignificant. Meanwhile, it is observed that level of average inflation in the GCC is positively and significantly affecting the financial stability of selected banks. It means that average inflation in the Gulf states is assumed to a positive determinant for the better banking sector stability. Under model five and six, overall variation through explanatory variables is .501 in FS-ROA, while for model six, the effect of control variables along NPLS indicators is 62.5 percent as well.

To examine the effect of credit risk indicators with and without considering the effect of control variables on FS-ZROE table 6 presents the regression findings. The effect of NPL2GA is 6.448 for FS-ZROE without control variables. With the addition of control variables, the effect of NPL2GA is 2.484 is positively significant for ZROE for top 20 banking firms in GCC. In addition, the effect of PANPLs is positively significant under model seven and eight as presented in table below.

Table-6. Findings for Equation 7 & 8 (Full Sample)

-7 |

-8 |

|

VARIABLES |

FS-ZROE |

FS-ZROE |

NPL2GA |

6.448*** |

2.484** |

-1.74 |

-1.03 |

|

PNPL |

8.673 |

5.224 |

-5.144 |

-1.092 |

|

NPLTE |

1.569 |

9.373 |

-1.314 |

-5.584 |

|

NPLW_P |

24.654 |

6.518 |

-1.119 |

-9.033 |

|

PANPLs |

6.962** |

3.948* |

-3.372 |

-2.323 |

|

GDP |

3.896*** |

|

-9.204 |

||

FSD |

7.314** |

|

-7.763 |

||

INF |

22.732 |

|

-9.733 |

||

Constant |

22.838 |

-16.9 |

-1.63 |

-30658 |

|

Observations |

140 |

140 |

R-squared |

0.492 |

0.511 |

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

It means that some of the credit risk indicators are positively associated with financial stability of selected banks in GCC. The effect of financial sector development is assumed to significantly positive along with GDP at 5 percent and 1 percent level of significance. However, with the control variables, explanatory power is found to be .511 percent.

After the consideration of overall sample of 20 banks and their empirical analyses, two sub samples covering 1-10, and 11-20 banks are also observed separately. Table 7 indicates the effect of NPL indicators for all four measures of financial stability. It is found that impact of NPL2GA for all four measures of financial stability is significant for top ten banking firms. While for the PNPL, similar positive and significant effect is observed with low level of standard error in the regression coefficients. In addition, the effect of NPLTE is significantly positive only for the FS-ROA, and FS-ZROA. For NPLW_P and PANPLs, it is examined that FS-ROA is positively and significantly associated with both credit risk measures. For FS-ROA, an overall variation is 42.1 percent for ROA.

Table-7. Findings for Equation 9-12 (First Sub-sample)

-9 |

-10 |

-11 |

-12 |

|

VARIABLES |

FS-ROA |

FS-ROE |

FS-ZROE |

FS-ZROA |

NPL2GA |

-0.0761** |

0.0624** |

-3.976* |

-3.963**** |

-0.166 |

-0.263 |

-5.393 |

-2.254 |

|

PNPL |

0.377*** |

0.464** |

9.153** |

6.227*** |

-0.122 |

-0.194 |

-3.967 |

-1.658 |

|

NPLTE |

0.0192* |

0.019 |

0.49 |

0.411*** |

-0.011 |

-0.0174 |

-0.357 |

-0.149 |

|

NPLW_P |

0.0441* |

0.056 |

1.088 |

0.512 |

-0.0234 |

-0.0372 |

-0.762 |

-0.319 |

|

PANPLs |

0.406* |

0.544 |

4.322 |

4.239 |

-0.241 |

-0.382 |

-7.829 |

-3.273 |

|

Constant |

-0.0195** |

-0.0252** |

-0.379 |

-0.238** |

-0.00783 |

-0.0124 |

-0.255 |

-0.106 |

|

Observations |

68 |

68 |

68 |

68 |

R-squared |

0.421 |

0.376 |

0.211 |

0.377 |

Standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Table 8 presents the findings for the top ten banking firms while taking all the explanatory and control variables into consideration for all measures of financial stability. Under model 13 the effect of GDP and FSD is significantly positive. While for the model 14, the effect of NPL2GA is .601, indicates a positive impact on the value of FS-ROA. For the economic growth and financial sector development, the impact on ROA is positively significant, in favoring for the assumption that financial development along economic growth are significant determinants of banking sector stability.

Table-8. Findings for Equation 13-16 (First Sub-sample)

-13 |

-14 |

-15 |

-16 |

|

VARIABLES |

FS-ROA |

FS-ROE |

FS-ZROE |

FS-ZROA |

NPL2GA |

8.506 |

0.601** |

0.011** |

1.593 |

-5.474 |

-0.259 |

-0.319 |

-2.303 |

|

PNPL |

2.198 |

0.177 |

0.521 |

2.734* |

-3.772 |

-0.179 |

-0.632 |

-1.587 |

|

NPLTE |

-0.264 |

-0.0115 |

-0.365 |

0.0315 |

-0.356 |

-0.0169 |

-0.152 |

-0.15 |

|

NPLW_P |

-0.391 |

-0.00857 |

-0.9632 |

-0.1 |

-0.775 |

-0.0367 |

-0.32 |

-0.326 |

|

PANPLs |

-16.95* |

-0.473 |

-0.854 |

-3.141 |

-9.301 |

-0.441 |

-0.144 |

-3.914 |

|

GDP |

2.171*** |

0.0966*** |

-0.3621*** |

-0.830** |

-0.748 |

-0.0354 |

-0.632 |

-0.315 |

|

FSD |

2.546*** |

0.144*** |

-0.966*** |

-0.795*** |

-0.619 |

-0.0293 |

-0.695 |

-0.26 |

|

INF |

0.43 |

0.0758* |

0.201* |

-0.673* |

-0.915 |

-0.0434 |

-0.632 |

-0.385 |

|

Constant |

2.255*** |

0.0886** |

0.9623** |

0.867** |

-0.796 |

-0.0377 |

-0.337 |

-0.335 |

|

Observations |

68 |

68 |

68 |

68 |

R-squared |

0.455 |

0.593 |

0.593 |

0.564 |

Standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

After considering top 10 banking firms, table 9 explains the impact of credit risk indicators on four measures of financial stability on rest of banking firms. The effect of NPL2GA is positive and significant for the all stability measures under table 9. While the effect of NPLW_P is -1.308 is significantly negative for 11-20 banks. While for the FS-ZROE, the effect of PANLs is 7.0107 which indicates that unit change in credit risk, causing a positive impact on stability. The explanatory power for the FS-ROA is .749, explaining that overall good variation is examined through credit risk indicators for 2nd sub sample of the study.

Table-9. Findings for Equation 17-120 (second sub-sample)

-17 |

-18 |

-19 |

-20 |

|

VARIABLES |

FS-ROA |

FS-ROE |

FS-ZROE |

FS-ZROA |

NPL2GA |

2.334*** |

4.555** |

6.193* |

3.528 |

-0.601 |

-1.912 |

-0.096 |

-4.279 |

|

PNPL |

-3.799 |

2.126 |

1.659 |

2.763 |

-4.954 |

-1.529 |

-2.654 |

-3.526 |

|

NPLTE |

-1.308*** |

4.966 |

2.011 |

4.211 |

-0.453 |

-32,362 |

-2.012 |

-3.012 |

|

NPLW_P |

-1.452 |

1.484 |

491,110 |

1.166 |

-2.75 |

-0.263 |

-1.473 |

-1.957 |

|

PANPLs |

7.635 |

8.727 |

7.107** |

6.006 |

-6.505 |

-464,247 |

-3.481 |

-4.63 |

|

Constant |

0.840** |

-5.846* |

-3.934 |

-5.008* |

-0.396 |

-2.46 |

-20.238 |

-2.198 |

|

Observations |

70 |

70 |

70 |

70 |

R-squared |

0.749 |

0.491 |

0.464 |

0.182 |

Standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Table 10 explains the findings for the 2nd sub sample while adding the control variables into regression models. It is examined that NPLTE is negatively and significantly affecting ROA along with GDP. For the FS-ROE, effect of NPLTE is positively significant along with the economic growth and financial sector development in GCC. For FS-ZROE, effect of NPLW_P is 5.250, significant at 5 percent level of significance. For FS-ZROA, significant impact of control variables like GDP and FSD is observed.

Table-10. Findings for Equation 21-24 (second sub-sample)

-21 |

-22 |

-23 |

-24 |

|

VARIABLES |

FS-ROA |

FS-ROE |

FS-ZROE |

FS-ZROA |

NPL2GA |

-0.99 |

8.912 |

2.0351 |

4.982 |

-1.444 |

-11.621 |

-0.667 |

-1.1396 |

|

PNPL |

-2.553 |

0.3254 |

1.216 |

1.4906 |

-4.77 |

-0.022 |

-2.446 |

-3.706 |

|

NPLTE |

-1.265*** |

.4080** |

1.998 |

3.3641 |

-0.449 |

-3.021 |

-2.883 |

-6.593 |

|

NPLW_P |

-0.0505 |

2.0214 |

5.250** |

9.949 |

-2.564 |

-3.012 |

-1.5291 |

-2.024 |

|

PANPLs |

0.45 |

4.142 |

4.571* |

3.057 |

-6.888 |

-5.32 |

-10.076 |

-5.436 |

|

GDP |

0.161*** |

1.960* |

7.756 |

3.561** |

-0.0543 |

-4.302 |

-32.378 |

-42.858 |

|

FSD |

-0.119 |

9.192** |

4.24 |

10.018** |

-0.167 |

-13.6 |

-99.791 |

-13.092 |

|

INFL |

0.0719 |

1.604 |

21.252 |

16.234 |

-0.047 |

-3.727 |

-28.047 |

-3.026 |

|

Constant |

0.692* |

-40.333 |

-25.018 |

-3.912 |

-0.4 |

-20.692 |

-20.509 |

-3.711 |

|

Observations |

70 |

70 |

70 |

70 |

R-squared |

0.632 |

0.365 |

0.477 |

0.397 |

Standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

4. CONCLUSIONS AND RECOMMENDATIONS

This article is examining the effect of credit risk indicators along with the control variables on financial stability measures of top 20 banking firms, currently working in the region of GCC. While seeing the factors of return on assets, return on equity, Z-score for return on assets, and Z-score for return on equity as major stability measures, various regression models have been developed and empirically examined for both explanatory and control variables. To measure the effect of credit risk, five proxies have been identified from the literature and added in the study. while for the control variables, financial sector development along with economic growth and inflation are assumed as control variables.

Two approaches for the samples have been considered. In the very first sample, all 20 banking firms have been considered to check the impact of credit risk and control variables of the study. For the first measure of stability; ROA, key indicators are NPL2GA, PNPL, NPLTE and NPLW_P without the consideration of control variables. While under the presence of control variables, NPLTE is the only determinant for the stability in overall banking firms with the controlling effect of GDP and FSD. Findings for the FSROE, factor of NPL2GA and NPLTE are significant determinants. When the model is observed through control variables, none of the credit risk determinants are found to be significant predictors of ROE, except the GDP and FSD. For the stability measure through Z-score, effect of NPL2GA along NPLTE is significant with both conditions of presence and non-presence of control variables. However, for ZROA, effect of FSD and INFL is positively significant, indicating an increasing trend for the stability. for the ZROE, again the effect of NPL2GA is significant with PANPLs. While control variables like GDP and FSD are again significantly and positively associated with financial stability. After overall sample, two sub samples for top 10 and subsequent 10 banking firms are also generated to check the impact of credit risk determinants with and without the presence of control variables. With the existence of control variables, effect of NPL2GA is positively significant with GDP and financial sector development. Meanwhile, under all the models with the presence of control variables, both GDP and FSD are significantly and positively contributing towards financial stability measures. For the 2nd sub sample of banks, effect of NPL2GA is found to be positively and significantly associate with the stability. While with the presence of control variables, effect of GDP is significantly positively except for ZROE.

Based on the above stated findings, consideration of credit risk indicators both in the presence and non-presence of control variables is very important in banking firms of GCC. The impact of credit risk is found to be crucial while creating instability in the banks and provide enough evidence to support the argument that low asset quality should be under consideration. The focus of earlier studies is primarily from the context of developed and developing economies, with the little consideration for GCC countries. In this regard, empirical findings for current study can be assumed as significant addition in the literature to cope with this gap. Besides, increasing credit risk for the banking firms in GCC provides another way for the discussion to consider the role of risk management team in the banks, responsible for tackling and dealing with the financial shocks of non-performing loans. Yet, this study is based on some limitations as well. At first, sample is developed through top 20 banking firms, while ignoring the rest of the banks working in GCC. At second, time span is limited to the present decade, while lacking with past decade, where the global financial crisis has targeted the world economy and banking sector. Future research can be conducted while adding more time, and better sample size. Besides, present study is highly recommended to the banking sector management, responsible for the stability and risk supervision mechanism. More attention is required towards credit risk as it is an emerging issue in the Gulf economies and financial sector. Policy implication of the study can be viewed as it is a significant evidence while developing strategic planning for the stability of banking sector.

| Funding: This study received no specific financial support. |

| Competing Interests: The author declares that there are no conflicts of interests regarding the publication of this paper. |

REFERENCES

Acemoglu, D., A. Ozdaglar and A. Tahbaz-Salehi, 2015. Systemic risk and stability in financial networks. American Economic Review, 105(2): 564-608.

Acharya, V., I. Drechsler and P. Schnabl, 2014. A pyrrhic victory? Bank bailouts and sovereign credit risk. The Journal of Finance, 69(6): 2689-2739. Available at: https://doi.org/10.1111/jofi.12206.

Armstrong, A., O. Carreras, S. Kirby, J. Meaning, R. Piggott, M. Dooley, R. Flood, P. Garber and M. Goodfriend, 2015. Interest on reserves and monetary policy. National Institute Economic Review, 233(1): F44-F52.

Board, F.S., 2017. Assessment of shadow banking activities, risks and the adequacy of post-crisis policy tools to address financial stability concerns. July, Basel. Available from http://www.fsb.org/wp-content/uploads/P300617-1.pdf .

Bouheni, B.F. and A. Hasnaoui, 2017. Cyclical behavior of the financial stability of eurozone commercial banks. Economic Modelling, 67(C): 392-408. Available at: https://doi.org/10.1016/j.econmod.2017.02.018.

Crockett, A., 2000. Marrying the micro-and macro-prudential dimensions of financial stability. BIS Speeches, 21. Available from https://www.bis.org/speeches/sp000921.htm .

Dell'Ariccia, G., 2016. Financial fragmentation, real-sector lending, and the European banking union. In The New International Financial System: Analyzing the Cumulative Impact of Regulatory Reform. pp: 459-471.

Diallo, B. and A. Al-Mansour, 2017. Shadow banking, insurance and financial sector stability. Research in International Business and Finance, 42(C): 224-232. Available at: https://doi.org/10.1016/j.ribaf.2017.04.024.

Duffie, D., 2008. Innovations in credit risk transfer: Implications for financial stability. BIS Working Paper No. 255. Available from https://www.bis.org/publ/work255.pdf .

Fatemi, A. and I. Fooladi, 2006. Credit risk management: A survey of practices. Managerial Finance, 32(3): 227-233. Available at: https://doi.org/10.1108/03074350610646735.

Fu, X.M., Y.R. Lin and P. Molyneux, 2014. Bank competition and financial stability in Asia pacific. Journal of Banking & Finance, 38(C): 64-77. Available at: https://doi.org/10.1016/j.jbankfin.2013.09.012.

Gamaginta, R.R., 2015. The stability comparison between Islamic banks and conventional banks: Evidence in Indonesia. Financial Stability and Risk Management in Islamic Financial Institutions: 8th International Conference on Islamic Economics and Finance.

Ghosh, A., 2015. Banking-industry specific and regional economic determinants of non-performing loans: Evidence from US states. Journal of Financial Stability, 20(C): 93-104. Available at: https://doi.org/10.1016/j.jfs.2015.08.004.

Ghosh, A., 2017. Sector-specific analysis of non-performing loans in the US banking system and their macroeconomic impact. Journal of Economics and Business, 93(C): 29-45. Available at: https://doi.org/10.1016/j.jeconbus.2017.06.002.

Goodhart, C.A., 2005. Financial regulation, credit risk and financial stability. National Institute Economic Review, 192(1): 118-127. Available at: https://doi.org/10.1177/002795010519200111.

Goodhart, C.A., 2006. A framework for assessing financial stability? Journal of Banking & Finance, 30(12): 3415-3422. Available at: https://doi.org/10.1016/j.jbankfin.2006.06.003.

Gulf Business, 2018. Top 50 banks in GCC. Available from https://gulfbusiness.com/lists/top-50-gcc-banks-2017/#.XB6SdVwzaM8 [Accessed 15 Jan 2018].

Guy, K. and S. Lowe, 2011. Non-performing loans and bank stability in Barbados. Economic Review, 37(1): 77-82.

Hidayat, C., I. Putong and R. Puspokusumo, 2016. The interrelationship between intellectual capital and financial performance: A case study of Indonesian insurance companies. Pertanika Journal of Social Sciences & Humanities, 24(Special Issue): 83-97.

Ihsan, A. and M.A. Jadoon, 2016. Comparative analysis of asset quality: Evidence from the public and private sector banks of Pakistan. Abasyn University Journal of Social Sciences, 9(1): 281-301.

Jassaud, N. and M.K. Kang, 2015. A strategy for developing a market for nonperforming loans in Italy (No. 15-24). International Monetary Fund.

Krugman, P.R., 2008. International economics: Theory and policy, 8/E. Pearson Education India. Available from: https://www.amazon.com/International-Economics-Theory-Policy-Pearson/dp/0133423646 .

Le, T.H., J. Kim and M. Lee, 2016. Institutional quality, trade openness, and financial sector development in Asia: An empirical investigation. Emerging Markets Finance and Trade, 52(5): 1047-1059. Available at: https://doi.org/10.1080/1540496x.2015.1103138.

Morgan, P.J. and V. Pontines, 2018. Financial stability and financial inclusion: The case of sme lending. The Singapore Economic Review, 63(01): 111-124. Available at: https://doi.org/10.1142/s0217590818410035.

Murry, D.A. and G.D. Nan, 1994. A definition of the gross domestic product-electrification interrelationship. The Journal of Energy and Development, 19(2): 275-283.

Otchere, I., L. Senbet and W. Simbanegavi, 2017. Financial sector development in africa-an overview. Review of development finance. 7(1): 1-5. Available at: https://doi.org/10.1016/j.rdf.2017.04.002.

Pisedtasalasai, A. and K. Rujiratpichathorn, 2017. Competition, stability and financial crisis in Thai banking sector. Journal of Advanced Studies in Finance, 8(1 (15)): 5-18.

Saba, I., R. Kibriya and R. Kouser, 2015. Antecedents of Financial performance of banking sector: Panel analysis of islamic, conventional and mix banks in Pakistan. Journal of Accounting and Finance in Emerging Economies, 1(1): 9-30. Available at: https://doi.org/10.26710/jafee.v1i1.61.

Soedarmono, W., F. Machrouh and A. Tarazi, 2011. Bank market power, economic growth and financial stability: Evidence from Asian banks. Journal of Asian Economics, 22(6): 460-470. Available at: https://doi.org/10.1016/j.asieco.2011.08.003.

Soedarmono, W., F. Machrouh and A. Tarazi, 2013. Bank competition, crisis and risk taking: Evidence from emerging markets in Asia. Journal of International Financial Markets, Institutions and Money, 23: 196-221.Available at: https://doi.org/10.1016/j.intfin.2012.09.009.

Stiroh, K., 2004. Diversification in banking: Is noninterest income the answer? Journal of Money, Credit and Banking, 36(5): 853-882. Available at: https://doi.org/10.1353/mcb.2004.0076.

Sutton, P.C., C.D. Elvidge and T. Ghosh, 2007. Estimation of gross domestic product at sub-national scales using nighttime satellite imagery. International Journal of Ecological Economics & Statistics, 8(S07): 5-21.

Trinugroho, I., T. Risfandy, M.D. Ariefianto, M.A. Prabowo, H. Purnomo, & and Y. Purwaningsih, 2017. Does religiosity matter for Islamic banks’ performance? Evidence from Indonesia. International Journal of Economics and Management, 11(2): 419-435.

Umoren, A., B. Akpan and E. Udoh, 2016. Analysis of empirical relationship among agricultural lending, agricultural growth and non-performing loans in Nigerian banking system. Economy, 3(2): 94-101. Available at: https://doi.org/10.20448/journal.502/2016.3.2/502.2.94.101.

Wagner, W. and I.W. Marsh, 2006. Credit risk transfer and financial sector stability. Journal of Financial Stability, 2(2): 173-193. Available at: https://doi.org/10.1016/j.jfs.2005.11.001.

Wahid, A., K. Azam, G. Khan and N. Talib, 2015. 2 credit risk affects shareholder’s wealth in banking sector of Pakistan, does it matter? Journal of Rural Development and Administration, 46(2): 9-15.

APPENDIX

Note: Following Notions are used for the econometric equations:

Sr. No. |

Variable Abbreviations |

Notion in Equations |

1 |

NPL2GA |

NPL1 |

2 |

PNPL |

NPL2 |

3 |

NPLTE |

NPL3 |

4 |

NPLW_P |

NPL4 |

5 |

PANPLs |

NPL5 |

Views and opinions expressed in this article are the views and opinions of the author(s), International Journal of Asian Social Science shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |