FACTORS AFFECTING TAX COMPLIANCE AMONG MALAYSIAN SMES IN E-COMMERCE BUSINESS

1,2,3,4,5,6Faculty of Accountancy, Universiti Teknologi MARA Puncak Alam Campus, Bandar Puncak Alam, Selangor, Malaysia

ABSTRACT

Tax compliance is a major concern among many governments in the world. The issue of tax compliance has long been discussed. Past studies have shown that there has always been a reluctance among taxpayers to pay taxes. From the works of literature, the small-scale sector is known to be a tough party when it comes to paying tax. Though the number of small and medium enterprises is growing, tax collection from this sector is still insignificant. Thus, this paper aims to determine factors affecting tax compliance among Malaysia’s Small and Medium Enterprises (SMEs) engaging in online businesses. The data was collected through interviews with six SMEs’ owners that have e-commerce business activities. The results reveal that tax knowledge plays a vital role in influencing tax compliance among online companies in Malaysia. In addition, the respondents claimed that the Malaysian tax rules and regulations are too complex to understand, and the current corporate tax rate is too high and burdensome. This paper contributes to the literature in the area of taxation especially in Malaysia.

Keywords:Small medium sized enterprise (SMEs), Tax compliance, Online business.

ARTICLE HISTORY: Received:17 September 2018 Revised:22 October 2018 Accepted:23 November 2018Published:18 December 2018.

Contribution/ Originality:This study provides more insights into the area of tax compliance and E-Commerce business. It is hope that this article will help other researchers and policy makers on the implementation of taxation towards online business company in Malaysia.

1. INTRODUCTION

1.1. Background of Study

Tax revenue collected is used by a government to develop the economy, education, society and security of the country. People who pay taxes are known as taxpayers. Taxpayers come from various parties such as individuals, trustees, clubs, cooperatives and corporations (Sumedi, 2010![]() ; Shaari et al., 2015

; Shaari et al., 2015![]() ). New technologies are emerging day by day in a fast speed in all fields. Many companies have made use of the Internet to handle information and have incorporated e-commerce into their business processes. E-commerce has brought numerous advantages such as reduction in costs of conducting business, penetration of new customers and suppliers, product or service quality improvement, the creation of new routes or directions for distribution of products (Pham et al., 2011

). New technologies are emerging day by day in a fast speed in all fields. Many companies have made use of the Internet to handle information and have incorporated e-commerce into their business processes. E-commerce has brought numerous advantages such as reduction in costs of conducting business, penetration of new customers and suppliers, product or service quality improvement, the creation of new routes or directions for distribution of products (Pham et al., 2011![]() ). The low cost of conducting electronic commerce enables small firms to access markets worldwide.

). The low cost of conducting electronic commerce enables small firms to access markets worldwide.

1.2. Small and Medium Enterprises (SMEs) and E-Commerce

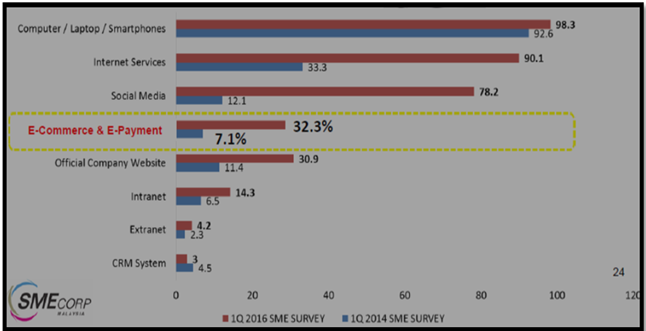

According to Hashim and Abdullah (2014![]() ) e-commerce can be defined as “the seamless application of Information and Communications Technology (ICT) from its point of origin to its end point along the entire value chain of business processes conducted electronically and designed to enable the accomplishment of a business goal”. The SME Annual Report 2015-2016 showed that many SMEs in Malaysia during the first quarter of 2016 utilised 3 common devices namely mobile phones, tablets and laptops for their business purposes. Table 1 shows a diagram of the horizontal bar chart to illustrate the significant differences between ICT and e-commerce adopted by SME in Malaysia.

) e-commerce can be defined as “the seamless application of Information and Communications Technology (ICT) from its point of origin to its end point along the entire value chain of business processes conducted electronically and designed to enable the accomplishment of a business goal”. The SME Annual Report 2015-2016 showed that many SMEs in Malaysia during the first quarter of 2016 utilised 3 common devices namely mobile phones, tablets and laptops for their business purposes. Table 1 shows a diagram of the horizontal bar chart to illustrate the significant differences between ICT and e-commerce adopted by SME in Malaysia.

Currently, only 10% of SMEs in Malaysia are involved in e-commerce (SME Association of Malaysia, 2016![]() ). As such, the Digital Free Trade Zone (DFTZ) should encourage and assist local SMEs in implementing e-commerce as SMEs take-up rate is still low as compared to large companies. According to the President of Young Entrepreneurs Organization Malaysia, SMEs in Malaysia should be upgraded and encouraged to transform the way they conduct business from business to business (B2B) to business to consumers (B2C) as propagated by Ali Baba. He believes that e-commerce adoption among SMEs is expected to grow from 23% in 2016 to 50% by 2020 due to the increasing number of online businesses.

). As such, the Digital Free Trade Zone (DFTZ) should encourage and assist local SMEs in implementing e-commerce as SMEs take-up rate is still low as compared to large companies. According to the President of Young Entrepreneurs Organization Malaysia, SMEs in Malaysia should be upgraded and encouraged to transform the way they conduct business from business to business (B2B) to business to consumers (B2C) as propagated by Ali Baba. He believes that e-commerce adoption among SMEs is expected to grow from 23% in 2016 to 50% by 2020 due to the increasing number of online businesses.

Table-1. SMEs Survey

Source: SME Corporation Malaysia

The industry is also expected to grow 11% per annum by 2020, accounting for 6.4% of the gross domestic product. SME Corp Malaysia through Go Global Malaysia programme will ensure strong support to SMEs. The Go Global Malaysia programme is more comprehensive since it is a total end-to-end package for SMEs that will help them in worldwide businesses. Through e-commerce, SMEs are assumed to be able to gain significant market access since the Internet offers equal access to both SMEs and large corporations (Hashim and Abdullah, 2014![]() ). The equal access may allow SMEs to compete with large firms.

). The equal access may allow SMEs to compete with large firms.

The potential benefits of adopting e-commerce are cost reduction, expansion of market targets, improved business processes and operational efficiencies as well as a greater competitive advantage (Omar et al., 2011![]() ; Solaymani et al., 2012

; Solaymani et al., 2012![]() ; Ahmad et al., 2015

; Ahmad et al., 2015![]() ) . Additionally, SMEs could enjoy opportunities to engage international companies by adopting e-commerce business (Poorangi et al., 2013

) . Additionally, SMEs could enjoy opportunities to engage international companies by adopting e-commerce business (Poorangi et al., 2013![]() ). E-commerce is not limited to the Internet as companies may also use social medias such as Facebook and Instagram as marketing tools which make businesses more customer friendly. Furthermore, it helps SMEs with limited resources in for marketing to offer both sellers and buyers with more information and make the market become more transparent (Sun et al., 2012

). E-commerce is not limited to the Internet as companies may also use social medias such as Facebook and Instagram as marketing tools which make businesses more customer friendly. Furthermore, it helps SMEs with limited resources in for marketing to offer both sellers and buyers with more information and make the market become more transparent (Sun et al., 2012![]() ). In addition, easy online payment can be established by linking payment gateways to their websites. As a result, the adoption of e-commerce by SMEs could improve their business sales and increase their income.

). In addition, easy online payment can be established by linking payment gateways to their websites. As a result, the adoption of e-commerce by SMEs could improve their business sales and increase their income.

Nevertheless, adopting e-commerce is not easy as technology and business needs are ever changing. Ahmad et al. (2015![]() ) and Shah et al. (2011

) and Shah et al. (2011![]() ) have argued that the cost of acquiring e-commerce infrastructure in developing countries is usually high for many SMEs. In addition, the use of ICT in suburban’s is still low because of poor level of ICT skills among SME owners and employees which has prevented them from adopting e-commerce in their businesses (SME, 2016

) have argued that the cost of acquiring e-commerce infrastructure in developing countries is usually high for many SMEs. In addition, the use of ICT in suburban’s is still low because of poor level of ICT skills among SME owners and employees which has prevented them from adopting e-commerce in their businesses (SME, 2016![]() ). Thus, in order to exploit these new digital business opportunities, financial investments and skills to manage ICT functions are required.

). Thus, in order to exploit these new digital business opportunities, financial investments and skills to manage ICT functions are required.

The rapid growth of e-commerce nowadays has created various challenges. One prominent issue among e-commerce practitioners is that they can avoid taxation because businesses are conducted online or over the phone. They assume that tax authorities will not be able to detect their business income. This is because e-commerce business conducted over the Internet is completely different from other forms of businesses (Coupey, 2001![]() ). Li (2004

). Li (2004![]() ) and Mukti (2000

) and Mukti (2000![]() ) argued that not taxing or granting tax preferences to this industry could greatly harm tax collection. Tax is more than just a source of revenue as it plays a significant role to a nation’s development. In accordance to the tax neutrality principle, a tax system generally should be neutral so that decisions are made not for business tax reasons but based on their economic merits.

) argued that not taxing or granting tax preferences to this industry could greatly harm tax collection. Tax is more than just a source of revenue as it plays a significant role to a nation’s development. In accordance to the tax neutrality principle, a tax system generally should be neutral so that decisions are made not for business tax reasons but based on their economic merits.

Recently, both individuals and companies have shown interest e-commerce as they realized the many benefits they can enjoy. A study conducted by Poorangi et al. (2013![]() ) shows that SMEs in Malaysia are beginning to embrace e-commerce as they have become aware that e-commerce may provide a competitive advantage in today’s borderless economy regardless of business size and scope. E-commerce in Malaysia has been growing rapidly with the increase in the number of companies including SMEs engaging in e-commerce.

) shows that SMEs in Malaysia are beginning to embrace e-commerce as they have become aware that e-commerce may provide a competitive advantage in today’s borderless economy regardless of business size and scope. E-commerce in Malaysia has been growing rapidly with the increase in the number of companies including SMEs engaging in e-commerce.

However, from the unpublished data of the Inland Revenue Board of Malaysia (IRBM), from 2013 to 2015, there are still many SMEs with online businesses that do not submit their tax returns to IRBM. Non-compliance here is referred to as non-submission or late submission of tax returns to IRBM. If there is a large number of e-commerce SMEs that do not submit or understate their tax returns, the government would lose potential tax revenue. It may affect the development of the country. Therefore, the objective of this study is to explore factors affecting tax compliance among Malaysian SME engaging in e-commerce.

The rest of the paper is organized as follows. The next section provides a discussion on literature review which includes a discussion on factors that influenced tax compliance. Section 3 provides the research methodology followed by the findings and discussions. The final part of this paper is the conclusion of the study.

2. LITERATURE REVIEW

With the rapid growth of the Internet and technology, it did not take long before someone realized that the World Wide Web would give unlimited possibilities for commercial entrepreneurs. According to the Malaysia Digital Economy Corporation (MDEC), Malaysia has 20.62 million active Internet users in the year 2016. The increase of Internet users and growth of e-commerce in Malaysia shows the importance of e-commerce.

This situation makes e-commerce an essential tool for existing businesses to expand their market access. Currently, a huge number of global businesses conduct their operation without people and a physical location in the market place (Gibbs et al., 2003![]() ). The intangible products may cross boundaries without going through the normal business process using digitization and electronic delivery. Therefore, taxation on e-commerce has becomes a high priority for governments of most countries. All tax authorities around the world found themselves struggling to provide timely responses to the challenges of e-commerce.

). The intangible products may cross boundaries without going through the normal business process using digitization and electronic delivery. Therefore, taxation on e-commerce has becomes a high priority for governments of most countries. All tax authorities around the world found themselves struggling to provide timely responses to the challenges of e-commerce.

According to Ward and Sipior (2004![]() ) there are several factors that affect contribute to the complexity of e-commerce taxation which are borderless commerce, digital convergence, virtual organizations and automated transactions. The most fundamental question at hand is how e-commerce should be taxed. The consumption of tax was developed under the principle of physical presence of a product within a specific tax jurisdiction but there is no physical presence of a product in e-commerce transaction.

) there are several factors that affect contribute to the complexity of e-commerce taxation which are borderless commerce, digital convergence, virtual organizations and automated transactions. The most fundamental question at hand is how e-commerce should be taxed. The consumption of tax was developed under the principle of physical presence of a product within a specific tax jurisdiction but there is no physical presence of a product in e-commerce transaction.

A business that runs through electronic channel can be located anywhere and their customers are everywhere (Ho et al., 2001![]() ). In other words, e-commerce is borderless, with transactions coming from around the world. Ho et al. (2001

). In other words, e-commerce is borderless, with transactions coming from around the world. Ho et al. (2001![]() ) claimed that a business environment for e-commerce may have some identification problems in the context of where the implementation of contracts of purchase and sale. This situation causes a real challenge to tax authorities in identifying which transactions are taxable.

) claimed that a business environment for e-commerce may have some identification problems in the context of where the implementation of contracts of purchase and sale. This situation causes a real challenge to tax authorities in identifying which transactions are taxable.

2.1. Tax Compliance

As e-commerce is rapidly growing around the world, tax compliance is becoming more complex with globalization. Therefore, tax compliance continues to be the main focus of all tax administrators around the world. Many studies has defined the element of compliance or non-compliance differently (Fauziati et al., 2016![]() ). However, Azrina et al. (2014

). However, Azrina et al. (2014![]() ) noted that there is no standard definition for tax non-compliance. The simple definition of tax compliance is the degree to which taxpayers comply with the tax law. Kirchler et al. (2008

) noted that there is no standard definition for tax non-compliance. The simple definition of tax compliance is the degree to which taxpayers comply with the tax law. Kirchler et al. (2008![]() ) describe tax compliances as the degree to which a taxpayer complies (or fails to comply) with the tax rules of the country. Tax compliance process such as declaring income, filing a return, and paying the tax due in a timely manner.

) describe tax compliances as the degree to which a taxpayer complies (or fails to comply) with the tax rules of the country. Tax compliance process such as declaring income, filing a return, and paying the tax due in a timely manner.

There are two theories that suit for this study. They are economic and non-economic based theories. According to Loo (2006![]() ) economic based theory is related to costs and benefits when performing an action which is in this case the action is referred to as tax compliance. This theory is also known as the deterrence theory. It suggests the taxpayers as a moral utility maximize. In other words, taxpayers are influenced by economic motive such as profit maximization. In this study, this theory implies that the cost of tax compliance affects tax compliance.

) economic based theory is related to costs and benefits when performing an action which is in this case the action is referred to as tax compliance. This theory is also known as the deterrence theory. It suggests the taxpayers as a moral utility maximize. In other words, taxpayers are influenced by economic motive such as profit maximization. In this study, this theory implies that the cost of tax compliance affects tax compliance.

On the other hand, non-economic based theories or also known as psychological based theories focusing on taxpayers’ moral and ethics. Based on the study by Alm (2012![]() ) the theories suggest that taxpayers may comply based on their perception and attitude. Therefore, if the corporate taxpayer has a good perception and attitude towards tax rules and regulations, this may lead to higher compliance.

) the theories suggest that taxpayers may comply based on their perception and attitude. Therefore, if the corporate taxpayer has a good perception and attitude towards tax rules and regulations, this may lead to higher compliance.

Past studies have highlighted that there are various factors influencing tax compliance. For the purpose of this study, the concerned is targeted on four factors which are tax knowledge, tax complexity, tax morale and compliance cost.

2.2. Tax Knowledge

Knowledge can be defined as facts, information, and expertise obtained through experience or education. In order to achieve voluntary compliance, tax knowledge is important. This is because a taxpayer’s ability to understand tax system depends on his/her knowledge on the tax system and law. For instance, the Self-Assessment System (SAS) holds taxpayers accountable to declare and compute their own tax. In addition, it also requires taxpayers to have additional record-keeping, advanced tax estimates, and monthly advanced tax payments.

Knowledge in understanding the tax law will certainly help taxpayers to compute their tax when using SAS (Jabbar and Pope, 2008![]() ). For that reason, Redae and Sekhon (2016

). For that reason, Redae and Sekhon (2016![]() ) state that understanding tax payers’ knowledge and compliance behavior is a challenge for any government and tax authority especially when employing a self‐assessment system. The interviews’ result from a study by Saad (2014

) state that understanding tax payers’ knowledge and compliance behavior is a challenge for any government and tax authority especially when employing a self‐assessment system. The interviews’ result from a study by Saad (2014![]() ) showed that taxpayers seemed to have a lack of knowledge on the technical aspects of the income tax system. Thus, tax knowledge is essential as it may affect taxpayers’ understanding and indirectly may increase voluntary compliances and therefore, may cause a decline in tax evasion.

) showed that taxpayers seemed to have a lack of knowledge on the technical aspects of the income tax system. Thus, tax knowledge is essential as it may affect taxpayers’ understanding and indirectly may increase voluntary compliances and therefore, may cause a decline in tax evasion.

Knowledge of tax law and regulations is vital in order to create positive attitude among SME especially when using the SAS system which may reduce the inclination to evade taxes (Saad, 2009![]() ; Hai and See, 2011

; Hai and See, 2011![]() ). Tax knowledge can be acquired through self-learning, attending formal education, and informal ones (Hastuti, 2014

). Tax knowledge can be acquired through self-learning, attending formal education, and informal ones (Hastuti, 2014![]() ). Unfortunately, acquiring tax knowledge is a time consuming process (Palil, 2010

). Unfortunately, acquiring tax knowledge is a time consuming process (Palil, 2010![]() ).

).

Prior studies on “The impact of tax knowledge on the perceptions of tax fairness and attitudes towards compliance” by Tan and Fatt (2000![]() ) indicated that not only knowledge but an understanding of the tax system may have an effect on taxpayers' perceptions of fairness and attitudes towards compliance. A number of studies have indicated that there is a positive influence of tax knowledge on tax compliance behavior (Saad, 2009

) indicated that not only knowledge but an understanding of the tax system may have an effect on taxpayers' perceptions of fairness and attitudes towards compliance. A number of studies have indicated that there is a positive influence of tax knowledge on tax compliance behavior (Saad, 2009![]() ; Palil, 2010

; Palil, 2010![]() ; Alabede et al., 2011

; Alabede et al., 2011![]() ; Kamleitner et al., 2012

; Kamleitner et al., 2012![]() ; Hamid et al., 2017

; Hamid et al., 2017![]() ) .

) .

2.3. Tax Complexity

Tax simplicity appears to be a desirable feature in a taxation system. A simple tax system could result in a reduction in complexity which is one of the identified variables that affects tax compliance (Jackson and Milliron, 1986![]() ). From previous studies, when a taxpayers stated that they have difficulty in complying with the rules, this is indicative that a complexity has been encountered. For example, tax returns which involved complicated calculation, the feelings of uncertainty as well as the demand for legal actions are some of the tax complexities faced by many taxpayers. It has subsequently deterred them from complying with the rules and regulations (Vogel, 1974

). From previous studies, when a taxpayers stated that they have difficulty in complying with the rules, this is indicative that a complexity has been encountered. For example, tax returns which involved complicated calculation, the feelings of uncertainty as well as the demand for legal actions are some of the tax complexities faced by many taxpayers. It has subsequently deterred them from complying with the rules and regulations (Vogel, 1974![]() ).

).

According to McKerchar (2002![]() ) a simple taxation system which includes predicable solutions, consistent rules which are clearly communicated and well-integrated with other tax regulations may consequently resulted in high compliance. Findings from previous studies reveal that tax complexities helped tax authorities design a good system with a trade-off between the basic principles of efficiency, equity, simplicity and fairness that is best fitted (McKerchar, 2002

) a simple taxation system which includes predicable solutions, consistent rules which are clearly communicated and well-integrated with other tax regulations may consequently resulted in high compliance. Findings from previous studies reveal that tax complexities helped tax authorities design a good system with a trade-off between the basic principles of efficiency, equity, simplicity and fairness that is best fitted (McKerchar, 2002![]() ).

).

Long and Swingen (1987![]() ) explained the six dimensions of tax complexities: ambiguity on the tax law, frequent changes in tax law, tedious computation, numerous rules, confusing forms and record keeping issues. These dimensions are believed to provide a valid and reliable measurement of tax complexities which can be utilized for further studies. Tax complexity also can be divided into effective simplicity (the ability to determined tax liability correctly) and legal simplicity (the comprehensibility and readability of the taxation law) (Evans and Tran Nam, 2010

) explained the six dimensions of tax complexities: ambiguity on the tax law, frequent changes in tax law, tedious computation, numerous rules, confusing forms and record keeping issues. These dimensions are believed to provide a valid and reliable measurement of tax complexities which can be utilized for further studies. Tax complexity also can be divided into effective simplicity (the ability to determined tax liability correctly) and legal simplicity (the comprehensibility and readability of the taxation law) (Evans and Tran Nam, 2010![]() ).

).

It is also found that tax complexity could lead to unintentional non-compliance. Unintentional non-compliance happens when a taxpayer has the intention to be compliant but was incompliant as a result of the complexity of the system. McKerchar (2002![]() ) concludes that by using a multi-paradigm research method, both intentional and unintentional non-compliance could be reduced by minimizing tax complexity. Recently, Richardson (2006

) concludes that by using a multi-paradigm research method, both intentional and unintentional non-compliance could be reduced by minimizing tax complexity. Recently, Richardson (2006![]() ) conducted regression analysis by using the Ordinary Least Square (OLS) method which examined the impact of 10 elements of compliance variables based on the data obtained from 45 countries. He found that tax complexity is the most crucial factors in evading tax across countries and tax compliance is low in a county with a complex tax system.

) conducted regression analysis by using the Ordinary Least Square (OLS) method which examined the impact of 10 elements of compliance variables based on the data obtained from 45 countries. He found that tax complexity is the most crucial factors in evading tax across countries and tax compliance is low in a county with a complex tax system.

2.4. Tax Morale

Tax morale is related to the concepts of personal and social norms as well as trust in authorities. This indicates that high tax morale will contribute to high tax compliance. Previous studies have differentiated between personal and social norms (Hoffman et al., 2008![]() ). Basically, personal norms cover inequality aversion, ethic reasoning, personal values and deal with what is generally perceived as good or bad. For instance, voluntary compliance may be influenced by the religion of individuals (Torgler, 2012

). Basically, personal norms cover inequality aversion, ethic reasoning, personal values and deal with what is generally perceived as good or bad. For instance, voluntary compliance may be influenced by the religion of individuals (Torgler, 2012![]() ). According to Konrad and Qari (2012

). According to Konrad and Qari (2012![]() ) social norms are related to socially shared beliefs on how members of a group should behave. This indicates that tax compliance is mostly influenced by the people around us such as friends, colleagues or neighbours.

) social norms are related to socially shared beliefs on how members of a group should behave. This indicates that tax compliance is mostly influenced by the people around us such as friends, colleagues or neighbours.

Another important factor for tax morale is the trust in authorities where authorities are represented by public institutions where the perception of fairness and efficiency play an important role. The relationship between taxpayers and the authorities can be defined as ‘psychological contract’. Basically, taxpayers expect the government to provide good and services in exchange of with their tax payments. Therefore, tax compliance will be higher in situations in which taxpayers are satisfied with the services provided by the government (Barone and Mocetti, 2011![]() ). In addition, Alm and McKee (2006

). In addition, Alm and McKee (2006![]() ) states that the trust in public leadership and public administration would contribute to more voluntary tax compliance. Doerrenberg and Peichl (2013

) states that the trust in public leadership and public administration would contribute to more voluntary tax compliance. Doerrenberg and Peichl (2013![]() ) states that taxpayers in countries with a more progressive tax rate system are more likely to exhibit higher tax morale and will contribute to high tax compliance.

) states that taxpayers in countries with a more progressive tax rate system are more likely to exhibit higher tax morale and will contribute to high tax compliance.

2.5. Compliance Cost

The costs to fulfill the liabilities imposed on taxpayers by the tax legislation and tax administration is in addition to their paid taxes (Pavel and Vítek, 2014![]() ). Compliance cost incur in order to comply with the tax laws and regulations. This has led to non-compliance among the SMEs business. It may have involved the “classic” compliance costs which are costs of employees, time, premises and external supplies of goods and services, cash flows and psychological costs (Sanusi et al., 2017

). Compliance cost incur in order to comply with the tax laws and regulations. This has led to non-compliance among the SMEs business. It may have involved the “classic” compliance costs which are costs of employees, time, premises and external supplies of goods and services, cash flows and psychological costs (Sanusi et al., 2017![]() ). Those costs incurred by taxpayers or third parties such as businesses, in meeting the requirements in complying tax rules and regulation.

). Those costs incurred by taxpayers or third parties such as businesses, in meeting the requirements in complying tax rules and regulation.

Taxpayers will hire tax agents to assist them or they themselves would need to go for training and attend a seminar in order to understand tax concepts. This will incur financial and non-financial costs. More time is needed to file tax returns because of the lack of understanding on the tax regulation. In terms of the psychological cost, submitting tax returns and record keeping might be stressful for taxpayers.

3. RESEARCH METHODOLOGY

For this study, the interview method was adopted for data collection. However, out of the 20 SMEs involving in e-commerce, only six were willing to be interviewed. Table 2 gives the profile of the respondents.

Table-2. Profile of the Respondents

No |

Gender |

Race |

Age |

Education level |

Department |

1 |

Female |

Malay |

21-26 |

Bachelor |

Taxation |

2 |

Female |

Chinese |

21-26 |

Diploma |

Account |

3 |

Male |

Malay |

21-26 |

Diploma |

Account |

4 |

Female |

Malay |

27-35 |

Master |

Taxation |

5 |

Female |

Malay |

27-35 |

Bachelor |

Account |

6 |

Male |

Malay |

21-26 |

Diploma |

Marketing |

4. FINDINGS AND DISCUSSION

The findings revealed that some SMEs were compliant when submitting their tax returns while others were not. This situation drew the researcher’s interest to include SMEs that complied and those who did not. All respondents as shown in Table 2 are from the foods and beverages industry.

4.1. Tax Knowledge

The first question asked was whether the respondents were aware of the date they need to submit their tax returns to IRBM. All the respondents are aware of the date of submission except respondent no 3 and 6, who answered as follow:

“Sorry, I am not so sure about the exact date to submit my tax returns and every year I need to confirm with my tax agent”. (Respondent 3)

“I am not exactly sure but I think the submission is in the month of April”. ( Respondent 6)

According to the Income Tax Act of 1967, the tax penalty laws impose a huge punishment on failure to furnish tax returns or making incorrect returns by omitting or understating income or evading tax as stated in Section 112, 113 and 114. Thus, the question asked was whether the respondents were aware of the penalty due to tax non-compliance. Their feedbacks are as follows:

“Yes, we are aware about the penalty since we are always being sent to IRBM for training, seminars or workshops and the tax authority did highlight the punishment if we fail to comply with the tax law”. (Respondent 1)

“Of course, I am aware because this company had already experienced penalty charges due to late submission”. (Respondent 2)

However, Respondents 4 and 5 were not aware of tax penalty imposed on late submission and their feedbacks are as follows:

“Our company is not aware about fines because of late submission of the tax returns”.(Respondent 4)

“I certainly do not know that there is tax penalty when the company’s tax returns is submitted late”. (Respondent 5)

From the feedbacks, many of the respondents are knowledgeable of the Malaysian tax system and are able to understand the tax laws (Kamleitner et al., 2012![]() ). However, those who are lacking in tax knowledge are the concern of this study. More tax education programs should be conducted by the tax authority and the companies must also be proactive to ensure that their staff especially in the Accounts Department attend training related to taxation.

). However, those who are lacking in tax knowledge are the concern of this study. More tax education programs should be conducted by the tax authority and the companies must also be proactive to ensure that their staff especially in the Accounts Department attend training related to taxation.

4.2. Tax Complexity

The first question is related to tax complexity, whether the current Malaysian tax law is too complex and difficult to follow. Surprisingly, the feedbacks from the respondents are as follows:

“Yes, actually I do not really understand tax policies”. (Respondent 1)

“In my opinion, I think the Malaysian tax law is really hard to follow”. (Respondent 2,3,4 and 5)

“I do not know much about the tax law, however I think some of the law is are easy to follow and some are not”. (Respondent 6)

In addition, the respondents also added that the Malaysian tax law changes from year to year which is difficult for small companies to follow and keep up. For example, Tan and Fatt (2000![]() ) agreed that the Income Tax Act of 1967 which is revised annually by the Finance Act and Income Tax Amendments Act contributes to the complexity of the revenue law and is not an easy subject to understand by both tax practitioners and legal counsels. Moreover, in another study, Hanefah (1996

) agreed that the Income Tax Act of 1967 which is revised annually by the Finance Act and Income Tax Amendments Act contributes to the complexity of the revenue law and is not an easy subject to understand by both tax practitioners and legal counsels. Moreover, in another study, Hanefah (1996![]() ) also mentioned that Malaysia’s tax laws are too complex, confusing and frequently amended. These factors contribute to the increase in tax non-compliance.

) also mentioned that Malaysia’s tax laws are too complex, confusing and frequently amended. These factors contribute to the increase in tax non-compliance.

For the second question, “Do you think that the tax rate is too high?”, 5 out of 6 respondents (No. 1, 2, 4, 5 and 6) responded that the high tax rate is a burden on them. The majority of them agreed that the tax rate is too high. These feedbacks are consistent with the study carried out by Atawodi and Ojeka (2012![]() ) where they found that a high tax rate is a major problem for SMEs. It could encourage them not to comply. Moreover, it also pushes SMEs to remain in the informal sector and become less competitive in the business markets.

) where they found that a high tax rate is a major problem for SMEs. It could encourage them not to comply. Moreover, it also pushes SMEs to remain in the informal sector and become less competitive in the business markets.

4.3. Tax Morale

The third factor that affecting tax compliance among Malaysian SME’s online businesses is tax morale. During the interview sessions, two questions regarding tax moral were asked. The first question is “Do you think that tax is a burden to your company?” and the second question is “Do you think the tax system is fair?” Based on first question, the two respondents from compliant companies did not agreed that the tax system is a burden to their companies. They felt satisfy in fulfilling their tax obligation. This shows that they have a high tax morale which caused them to comply with the tax laws and obligations. This is supported by Alm and Torgler (2006![]() ) that tax morale make taxpayers to trust in the legal system. Below are feedbacks from the respondents:

) that tax morale make taxpayers to trust in the legal system. Below are feedbacks from the respondents:

“I think paying tax is not a burden to my company and I am satisfied in fulfilling the tax obligation”. (Respondent 1)

“Honestly, I am satisfied in paying the amount of tax since I can see that my company is able to contribute towards the country’s economic development”. (Respondent 2)

Three of the respondents from the non-compliance companies also did not agree that tax is a burden to their companies based on their feedbacks. Only one respondent agreed that tax is a burden to the company. Although the three respondents did not agree that tax is a burden, they did not comply with the tax law and regulations. It might be due to their mistrust of the government. Taxpayers’ relationship with their government, including their trust, is an important consideration when examining voluntary tax compliance (Frey and Torgler, 2007![]() ). Below are the feedbacks from the respondents:

). Below are the feedbacks from the respondents:

“Tax is not really a burden because the company can claim tax incentives”. (Respondent 4)

“In my opinion, tax is not a burden. However, there are too many types of taxes that a company needs to pay, for example, goods and services tax (GST) and income tax. It should be either one”. (Respondent 5)

“Tax is not a burden and if a company suffers losses, they do not need to pay. Only companies that are making profits will have to pay taxes”. (Respondent 6)

The second question has to do with the fairness of a tax system. The respondents from companies which complied agreed that the tax system in Malaysia is fair and equitable. They are also satisfied with the current Self-Assessment System (SAS) implemented since year of assessment 2001. The SAS system is very user friendly and easily accessible. Taxpayers are able to compute their own tax liabilities and submit their own tax returns. In contrast, two respondents from companies which did not comply did not to agree that the current tax system or SAS is fair and equitable. For them, the current tax system is difficult to understand, and the SAS system is also difficult to access since a password is required to log in.

4.4. Compliance Cost

The fourth factor affecting tax compliance is compliance cost. During the phone interview sessions, two questions were asked on compliance cost. The first question is “Do you hire any tax agent to assist you to submit tax return?” and the second question is “Do you think submitting tax return is stressful?”. Based on the first question, four of the respondents admitted that they hired tax agents, one respondent was not sure, and one respondent did not hire a tax agent.

Based on these responds, it shows that respondents prefer to hire agents rather than have their own staff file their tax return. Those who hired tax agents believe that tax agents are more knowledgeable. Hence, tax agents can handle any problem that may arise. However, based on one of the respondents who hired a tax agent, they respondent’s company did not comply because of documentation problem. From the interviews, it can be concluded that when companies hire tax agents, they tend to be more compliant as compared to those who do not. One respondent claimed that hiring a tax agent was cheaper than to have their company’s own staff submit its tax return. This is supported by Alm and Torgler (2006![]() ) where they affirm that low compliance cost may lead to tax compliance. A feedback from respondent 2:

) where they affirm that low compliance cost may lead to tax compliance. A feedback from respondent 2:

“Yes, hiring a tax agent would eventually increase company’s compliance cost but overall it benefits my company.”

The findings from the questions on compliance cost are in line with Pavel and Vítek (2014![]() ) which cited that compliance cost may influence tax compliance. An interview with tax consultants was conducted in order to get his/her perspective on these issues. They explained that pricing of tax services to SMEs is a tricky issue. Even if, the service price is not very significant, compared to the services provided to them, most of the small and medium businesses do not understand the value of the services. As a result, they are requesting for payment as soon as they have completed their tasks but before delivering to the customers due to the above reasons. Many cases happened whereby service is delivered, however most of the small and medium businesses owners hesitate or take time to settle their service fees. It shows that the compliance cost give impact to comply with tax.

) which cited that compliance cost may influence tax compliance. An interview with tax consultants was conducted in order to get his/her perspective on these issues. They explained that pricing of tax services to SMEs is a tricky issue. Even if, the service price is not very significant, compared to the services provided to them, most of the small and medium businesses do not understand the value of the services. As a result, they are requesting for payment as soon as they have completed their tasks but before delivering to the customers due to the above reasons. Many cases happened whereby service is delivered, however most of the small and medium businesses owners hesitate or take time to settle their service fees. It shows that the compliance cost give impact to comply with tax.

The two respondents from compliant companies gave different answers to the second question on the level of stressfulness when submitting tax return. One of them agreed that filing tax return is stressful while the other did not agree. Below are their answers:

“It was not stressful for me. I understand the process of tax returns and send it on a timely basis as required by law”. (Respondent 1 )

“The submission is stressful when the line is slow towards the end of submission date”. (Respondent 2)

Three respondents out of four respondents from the non-compliant companies agreed that the submission of tax return was stressful while the fourth respondent could not decide if the experience is stressful. or not. Below are the responses:

“Very stressful but what we need to understand is the filing and submitting of tax return is a mandatory obligation for all companies under the ITA of 1967”. (Respondent 4)

“It is hard to fill up the form for beginner.” (Respondent 5)

“It is stressful when you do not understand the tax legislation”. (Respondent 6)

These findings are consistent with the findings of scholars such as Pope, J. & Abdul-Jabbar, H. (2008) who mentioned that psychological factors contribute to tax compliance. In this study, it is found that higher level of stress will contribute to higher tax compliance cost. The responses received from most of the non-compliant companies is stress and this may impact to tax compliance. In other words, to reduce the stress level, companies may ignore tax compliance.

5. CONCLUSION

In conclusion, tax knowledge, tax complexity, tax morale and compliance cost provide mixed results. For tax knowledge, half of the respondents have adequate understanding for them to comply. In terms of tax complexity, the majority of them have a common opinion that tax law and regulations are is complicated and tax rate is burdensome. In terms of morality, they have accepted the tax system and on compliance cost, they have engaged tax agents to assist in submitting their tax returns within the deadline.

The Income Tax Act of 1967 also recognises the rights of taxpayers to arrange their financial affairs to mitigate liabilities. Be that as it may, in order for taxpayers to avoid interference from tax authorities, taxpayers must ensure that the submission is bona fide. In order to create awareness in tax compliance among the Malaysian SMEs’ online business, the study suggests that the government can create tax awareness by using the mass media such as advertisements, television, newspapers, and magazines. It might be helpful to increase the level of compliance among taxpayers especially in online businesses.

Like most studies of a similar nature, this study has several limitations. Firstly, it is the phone interviews. They were short due to time constraint. This is because most of the respondents were busy and only gave 10 to 15 minutes to answer all the questions. Secondly, the limitation is the business owners have less control during the phone interviews. For one, they cannot view the respondents’ facial experience during the interview to determine if the answers were truthful.

Lastly, the limitation of phone interviews is the difficulty of getting interviewees to elaborate on their answers. People would hang up on longer telephone surveys resulting in partially completed interviews. Therefore, interviewers generally keep their questions and answers relatively brief. Many of these questions are multiple-choice in nature rather than open-ended questions. The open-ended questions are more informative because they allow respondents to elaborate why they responded as they did.

| Funding: The authors would like to express their gratitude to Universiti Teknologi MARA for granting LESTARI grant ref no: 600-IRMI/DANA KCM 5/3/LESTARI (143/2017). |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: Special thanks also go to the Faculty of Accountancy and Research Management Centre (RMC) of Universiti Teknologi MARA for their trust and continuous support. |

REFERENCES

Ahmad, S.Z., A.R. Abu Bakar, T.M. Faziharudean and K.A. Mohamad Zaki, 2015. An empirical study of factors affecting e-commerce adoption among small-and medium-sized enterprises in a developing country: Evidence from Malaysia. Information Technology for Development, 21(4): 555-572. Available at: https://doi.org/10.1080/02681102.2014.899961.

Alabede, J.O., Z.B.Z. Ariffin and K.M. Idris, 2011. Determinants of tax compliance behaviour: A proposed model for Nigeria. International Research Journal of Finance and Economics, 78: 121–136.

Alm, J., 2012. Measuring, explaining, and controlling tax evasion: Lessons from theory, experiments, and field studies. International Tax and Public Finance, 19(1): 54-77. Available at: https://doi.org/10.1007/s10797-011-9171-2.

Alm, J. and M. McKee, 2006. Audit certainty, audit productivity, and taxpayer compliance. National Tax Journal, 59(4): 801-816. Available at: https://doi.org/10.17310/ntj.2006.4.03.

Alm, J. and B. Torgler, 2006. Culture differences and tax morale in the United States and in Europe. Journal of Economic Psychology, 27(2): 224-246. Available at: https://doi.org/10.1016/j.joep.2005.09.002.

Atawodi, O.W. and S.A. Ojeka, 2012. Factors that affect tax compliance among small and medium enterprises (smes) in North Central Nigeria. International Journal of Business and Management, 7(12): 87–96.

Azrina, M.Y.N., L. Ming Ling and Y. Bee Wah, 2014. Tax non-compliance among SMCs in Malaysia: Tax audit evidence. Journal of Applied Accounting Research, 15(2): 215-234. Available at: https://doi.org/10.1108/jaar-02-2013-0016.

Barone, G. and S. Mocetti, 2011. Tax morale and public spending inefficiency. International Tax and Public Finance, 18(6): 724-749. Available at: https://doi.org/10.1007/s10797-011-9174-z.

Coupey, E., 2001. Marketing and the internet. Prentice Hall PTR.

Doerrenberg, P. and A. Peichl, 2013. Progressive taxation and tax morale. Public Choice, 155(3-4): 293-316. Available at: https://doi.org/10.1007/s11127-011-9848-1.

Evans, C. and B. Tran Nam, 2010. Tran-Nam, B., & Evans, C. (2010). Managing tax system complexity: building bridges through pre-filled tax returns. [This is a revised version of a paper originally presented at the International Tax Administration (Building Bridges) Conference (9th: 2010: Sydney)]. In Australian Tax Forum. Tax Institute, 25(2): 245.

Fauziati, P., A.F. Minovia, R.Y. Muslim and R. Nasrah, 2016. The impact of tax knowledge on tax compliance. Case Study in Kota Padang, Indonesia. Journal of Advanced Research in Business and Management Studies, 2(1): 22–30.

Frey, B.S. and B. Torgler, 2007. Tax morale and conditional cooperation. Journal of Comparative Economics, 35(1): 136-159. Available at: https://doi.org/10.1016/j.jce.2006.10.006.

Gibbs, J., K.L. Kraemer and J. Dedrick, 2003. Environment and policy factors shaping global e-commerce diffusion: A cross-country comparison. The Information Society, 19(1): 5-18. Available at: https://doi.org/10.1080/01972240309472.

Hai, O.T. and L.M. See, 2011. Behavioral intention of tax non-compliance among sole-proprietors in Malaysia. International Journal of Business and Social Science, 2(6): 142-152.

Hamid, A.N., M.D. Mat Dangi, R.R.H. Mohd and N. Md Azali, 2017. The effectiveness of GST education providers: Royal Malaysian customs department vs tax agents in Malaysia. Advanced Science Letter, 8(2): 35 – 45. Available at: https://doi.org/10.21102/wjm.2017.09.82.01.03.

Hanefah, H.M.M., 1996. An evaluation of Malaysian tax administrative system, and taxpayers’ perception towards assessment system, tax law fairness and tax law complexity. Unpublished Doctoral Thesis, Faculty of Accountancy, Universiti Utara Malaysia.

Hashim, N.A. and N.L. Abdullah, 2014. Catastrophe of e-commerce among Malaysian SMEs-Between its perceived and proven benefits. Journal of Management, 42: 145-157. Available at: https://doi.org/10.17576/pengurusan-2014-42-12.

Hastuti, R., 2014. Tax awareness and tax education: A perception of potential taxpayers. International Journal of Business, Economics and Law, 5(1): 83-91.

Ho, D., A. Mak and B. Wong, 2001. Assurance of functionality of tax in the e-business world: The Hong Kong experience. Managerial Auditing Journal, 16(6): 339-346. Available at: https://doi.org/10.1108/02686900110395488.

Hoffman, W.H., J.E. Smith and E. Willis, 2008. West federal taxation: Individual income Taxes. (United States, Thomson South-Western).

Jabbar, H.A. and J. Pope, 2008. The effects of the self-assessment system on the tax compliance costs of small and medium enterprises in Malaysia. Journals in Business & Management, 3(4): 289–307.

Jackson, B.R. and V.C. Milliron, 1986. Tax compliance research: Findings, problems, and prospects. Journal of Accounting Literature, 5(1): 125-165.

Kamleitner, B., C. Korunka and E. Kirchler, 2012. Tax compliance of small business owners: A review. International Journal of Entrepreneurial Behavior & Research, 18(3): 330-351. Available at: https://doi.org/10.1108/13552551211227710.

Kirchler, E., E. Hoelzl and I. Wahl, 2008. Enforced versus voluntary tax compliance: The “slippery slope” framework. Journal of Economic Psychology, 29(2): 210-225. Available at: https://doi.org/10.1016/j.joep.2007.05.004.

Konrad, K.A. and S. Qari, 2012. The last refuge of a scoundrel? Patriotism and tax compliance. Economica, 79(315): 516-533. Available at: https://doi.org/10.1111/j.1468-0335.2011.00900.x.

Li, J., 2004. International taxation in the age of electronic commerce: A comparative study. Canadian Tax Journal, 52(1): 106-108.

Long, S.B. and J.A. Swingen, 1987. An approach to the measurement of tax law complexity. Journal of the American Taxation Association, 8(2): 22-36.

Loo, E.C., 2006. Tax knowledge, tax structure and compliance: A report on a quasi-experiment. New Zealand Journal of Taxation Law and Policy, 12(2): 117-140.

McKerchar, M., 2002. The effects of complexity on unintentional noncompliance for personal taxpayers in Australia. Austl. Tax F., 17: 3.

Mukti, A.N., 2000. Barriers to putting businesses on the internet in Malaysia. The Electronic Journal of Information Systems in Developing Countries, 2(1): 1-6. Available at: https://doi.org/10.1002/j.1681-4835.2000.tb00013.x.

Omar, A., T. Ramayah, L.B. Lin, O. Mohamad and M. Marimuthu, 2011. Determining factors for the usage of web based marketing applications among small medium enterprises (SMEs) in Malaysia. Journal of Marketing Development and Competitiveness, 5(2): 70–86.

Palil, M.R., 2010. Tax knowledge and tax compliance determinants in self assessment system in Malaysia. Unpublished Doctoral Thesis, Department of Accounting and Finance, University of Birmingham, UK.

Pavel, J. and L. Vítek, 2014. Tax compliance costs: Selected post-transitional countries and the Czech Republic. Procedia Economics and Finance, 12: 508-515. Available at: https://doi.org/10.1016/s2212-5671(14)00373-6.

Pham, L., L.N. Pham and D.T.T. Nguyen, 2011. Determinants of e-commerce adoption in Vietnamese small and medium sized enterprises. International Journal of Entrepreneurship, 15(1): 45-72.

Poorangi, M.M., E.W. Khin, S. Nikoonejad and A. Kardevani, 2013. E-commerce adoption in Malaysian small and medium enterprises practitioner firms: A revisit on Rogers' model. Annals of the Brazilian Academy of Sciences, 85(4): 1593-1604. Available at: https://doi.org/10.1590/0001-37652013103512.

Redae, R.B. and S. Sekhon, 2016. Taxpayers’ knowledge and tax compliance behavior in Ethiopia: A study of Tigray State. International Journal of Management and Commerce Innovations, 3(2): 1090-1102.

Richardson, G., 2006. Determinants of tax evasion: A cross-country investigation. Journal of International Accounting, Auditing and Taxation, 15(2): 150-169. Available at: https://doi.org/10.1016/j.intaccaudtax.2006.08.005.

Saad, N., 2009. Fairness perceptions and compliance behaviour: The case of salaried taxpayers in Malaysia after implementation of the selfassessment system. E Journal of Tax Research, 8(1): 32–63.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-Social and Behavioral Sciences, 109: 1069-1075. Available at: https://doi.org/10.1016/j.sbspro.2013.12.590.

Sanusi, S., R. Noor, N. Omar and Z.M. Sanusi, 2017. The readiness of small and medium enterprises (SME) in Malaysia for implementing goods and services tax (GST). Social Sciences & Humanities, 25: 241–250.

Shaari, N., A. Ali and N. Ismail, 2015. Student’s awareness and knowledge on the implementation of goods and services tax (GST) in Malaysia. Procedia Economics and Finance, 31: 269–279. Available at: https://doi.org/10.1016/s2212-5671(15)01229-0.

Shah, A.S., M.Y. Ali and M.F. Mohd. Jani, 2011. An empirical study of factors affecting electronic commerce adoption among SMEs in Malaysia. Journal of Business Economics and Management, 12(2): 375-399. Available at: https://doi.org/10.3846/16111699.2011.576749.

SME Association of Malaysia, 2016. E-commerce: A new horizon. Available from http://smeam.org/en/news/28123 [Accessed November 22, 2017].

Solaymani, S., K. Sohaili and E.A. Yazdinejad, 2012. Adoption and use of e-commerce in SMEs. Electronic Commerce Research, 12(3): 249-263. Available at: https://doi.org/10.1007/s10660-012-9096-6.

Sumedi, N.A., 2010. Acceptance of e-payment for tax purposes in Malaysia. Doctoral Dissertation, University of Malaya, Malaysia.

Sun, H., P.-L. Teh and A. Chiu, 2012. An empirical study on the websites service quality of Hong Kong small businesses. Total Quality Management & Business Excellence, 23(7-8): 931-947. Available at: https://doi.org/10.1080/14783363.2012.704273.

Tan, L.M. and C.C. Fatt, 2000. The impact of tax knowledge on the perceptions of tax fairness and attitudes towards compliance. Asian Review of Accounting, 8(1): 44–58. Available at: https://doi.org/10.1108/eb060720.

Torgler, B., 2012. Tax morale, Eastern Europe and European enlargement. Communist and Post Communist Studies, 45(1-2): 11-25. Available at: https://doi.org/10.1016/j.postcomstud.2012.02.005.

Vogel, J., 1974. Taxation and public opinion in Sweden: An interpretation of recent survey data. National Tax Journal, 27(4): 499-513.

Ward, B.T. and J.C. Sipior, 2004. To tax or not to tax e-commerce: A United States perspective. Journal of Electronic Commerce Research, 5(3): 172-180.

Views and opinions expressed in this article are the views and opinions of the author(s), International Journal of Asian Social Science shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |