CORPORATE GOVERNANCE, SUSTAINABILITY INITIATIVES AND FIRM PERFORMANCE: THEORETICAL AND CONCEPTUAL PERSPECTIVES

1,3,5PhD Student, Faculty of Economics and Management, Universiti Putra Malaysia (UPM), Malaysia

2Associate Professor, Faculty of Economics and Management, Universiti Putra Malaysia (UPM), Malaysia

3PhD Student, College of Business, Universiti Utara Malaysia (UUM), Malaysia

ABSTRACT

The objective of this paper is to generate a discuss as to the degree to which corporate governance and sustainability initiatives are predictor variables for firm performance, with the premise that firms have to be deliberately placed for them to harness the prospects available in their immediate environments. In relation to this study, the stakeholders, agency and institutional theories form the bedrock for the underpinning theories used for formulating the research framework with respect to the relationships among firm performance, corporate governance and sustainability initiatives respectfully. Less research efforts are involved in this area of study in the less developed nations, particularly with respect to the impacts of corporate governance on the environmental and social initiatives as well the financial and non-financial corporate performances of firms. Therefore, scholars and practitioners are encouraged to advance the body of knowledge in this study area for the global enhancement of productivity, as the review has conceptualised the integration of corporate governance and sustainability initiatives as strategic tools for enhancing firm performances locally and internationally.

Keywords:Corporate governance, Firm performance, Sustainability initiatives

JEL Classification :B26, G18

ARTICLE HISTORY: Received:30 August 2018 Revised:3 October 2018 Accepted:9 November 2018Published:5 December 2018.

Contribution/ Originality:This study documents the required awareness for more study efforts by researchers and practitioners in the emerging and developing climes with respect to the relationships among corporate governance, sustainability initiatives and firm performance.

1. INTRODUCTION

A measure or an indicator of a firm’s ability that is not only traceable to the efficiency of the entity itself, but also with respect to the market where its operations are involved is performance. Any performance measure or indicator must fulfill the following conditions: distinct and quantifiable; communicable throughout the firm and departments; fundamental to attaining objectives; and applicable to strategic business units (SBUs) (Jackson, 2017![]() ). Nevertheless, in management studies, performance is a construct generally used as a dependent variable (Richard et al., 2009

). Nevertheless, in management studies, performance is a construct generally used as a dependent variable (Richard et al., 2009![]() ) as well as being multidimensional in nature (Dess and Robinson, 1984

) as well as being multidimensional in nature (Dess and Robinson, 1984![]() ; Rauch et al., 2009

; Rauch et al., 2009![]() ). However, researchers have not agreed among themselves on an acceptable measure of performance (Mahmood and Hanafi, 2013

). However, researchers have not agreed among themselves on an acceptable measure of performance (Mahmood and Hanafi, 2013![]() ) so, there are no common and adequate bases for evaluating the corporate performance in order to have a concise picture of business and non-commercial concerns (Falshaw et al., 2006

) so, there are no common and adequate bases for evaluating the corporate performance in order to have a concise picture of business and non-commercial concerns (Falshaw et al., 2006![]() ; Akinboade, 2015

; Akinboade, 2015![]() ). Due to the aforementioned, various researchers have applied different performance criteria in their studies. Richard et al. (2009

). Due to the aforementioned, various researchers have applied different performance criteria in their studies. Richard et al. (2009![]() ) have shown in their review of 213 papers, that 207 diverse performance measures are involved. Hence, with performance being a contextual concept linked with the circumstance studied, the bases adopted to show performance are with respect to the circumstances of the organisations concerned (Carton and Hofer, 2006

) have shown in their review of 213 papers, that 207 diverse performance measures are involved. Hence, with performance being a contextual concept linked with the circumstance studied, the bases adopted to show performance are with respect to the circumstances of the organisations concerned (Carton and Hofer, 2006![]() ; Adedeji et al., 2017

; Adedeji et al., 2017![]() ). For instance, the firms’ financial performance measures are of relevance particularly when a firm expects to take full advantage of its profits. However, apart from the financial performance, the non-financial performance ( such as employees’ satisfaction and firm reputation) is an additional strategic issue to be emphasised on by a researcher in order to effectively evaluate the well-being of a firm in comparison to others within the same industry or outside thereof.

). For instance, the firms’ financial performance measures are of relevance particularly when a firm expects to take full advantage of its profits. However, apart from the financial performance, the non-financial performance ( such as employees’ satisfaction and firm reputation) is an additional strategic issue to be emphasised on by a researcher in order to effectively evaluate the well-being of a firm in comparison to others within the same industry or outside thereof.

The concerns for corporate governance have gained special recognition in the corporate world in the recent times, due to the occurrences of corporate scandals as witnessed with respect to Enron and WorldCom in the USA, Megan Media Holdings Berhad, and Transmile Group in Malaysia as well as Cadbury Plc in Nigeria respectively (Olaoye et al., 2016![]() ; Tan et al., 2016

; Tan et al., 2016![]() ). Due to the aforementioned, Olaoye et al. (2016

). Due to the aforementioned, Olaoye et al. (2016![]() ) are of the opinion that various countries (USA, Malaysia and Nigeria) have to through their Securities and Exchange Commission create corporate governance codes of ethics that will generate the need for effective operations in the business arena. In addition, the corporate and national structures have not provided mutual basis for the realisation of best practices expected in relation to integrity, accountability, and transparency with respect to all areas of management (Teh et al., 2016

) are of the opinion that various countries (USA, Malaysia and Nigeria) have to through their Securities and Exchange Commission create corporate governance codes of ethics that will generate the need for effective operations in the business arena. In addition, the corporate and national structures have not provided mutual basis for the realisation of best practices expected in relation to integrity, accountability, and transparency with respect to all areas of management (Teh et al., 2016![]() ). Therefore, the examination of the reason for the influence of corporate governance mechanisms on firm performance becomes relevant for the benefit of evolving best practices by policy makers and operators in the global business arena.

). Therefore, the examination of the reason for the influence of corporate governance mechanisms on firm performance becomes relevant for the benefit of evolving best practices by policy makers and operators in the global business arena.

The issue of corporate sustainability emerged primarily as environmental occurrences with eventual transformation to being an economic portent with the advent of literature on economic phenomena. The debate on sustainability as far as business and management are involved never gained recognition until the 1980’s and 1990’s due to the stakeholder's clamour for the acknowledgment of responsibility for social issues from the managers of businesses (Kakabadse et al., 2005![]() ). Nevertheless, business sustainability initiatives especially in the developed nations regarding depth, quantity, quality and content had encompassed both financial and non-financial exposés (Ioannou and Serafeim, 2014

). Nevertheless, business sustainability initiatives especially in the developed nations regarding depth, quantity, quality and content had encompassed both financial and non-financial exposés (Ioannou and Serafeim, 2014![]() ). Furthermore, the survival level of business entities have been censure the more as a result of increased social, regulatory, cultural, legal, environmental disclosures as well as technological advancements which have been responsible for the modernisation of businesses (Ernst and Young, 2013

). Furthermore, the survival level of business entities have been censure the more as a result of increased social, regulatory, cultural, legal, environmental disclosures as well as technological advancements which have been responsible for the modernisation of businesses (Ernst and Young, 2013![]() ).

).

This study covers in the first instance the conceptual framework based on theoretical foundation, with focus on the concepts of firm performance, corporate governance and sustainability initiatives. The second part is the development of hypotheses in relation to the conceptual framework in terms of the relationships among corporate governance and firm performance, corporate governance and sustainability initiatives, sustainability initiatives and firm performance and the mediating role of sustainability initiatives between corporate governance and firm performance. The next is contribution and implications while the last is the conclusion and recommendations for future research.

2. CONCEPTUAL FRAMEWORK BASED ON THEORETICAL FOUNDATION

For the purpose of this study, the review of the theoretical bases is in order to formulate the conceptual framework and provide a better understanding of the justification for the interrelatedness of the variables.

In an earlier part of this submission, firm performance involves the financial and non-financial aspects. The stakeholder theory states that a firm owes a responsibility to the other various groups of stakeholders, apart from just the shareholders, who are any person/group that can impact/be impacted by the decisions of a firm. According to Jensen and Meckling (1976![]() ) the stakeholder theory is in relation to the aspects of corporate wellness with emphasis on the activities and performance of a firm in terms of the capability to sustain the relationships it has with the diverse interested groups in its sphere of operations. This is not in agreement with the background of the norm that a firm is for improving the net-worth of the shareholders alone. However, in comparison, a firm has a role to itself as well as the other parties connected to for effectiveness and efficiency in order to take advantage of legitimate rights for existence (Jizi et al., 2014

) the stakeholder theory is in relation to the aspects of corporate wellness with emphasis on the activities and performance of a firm in terms of the capability to sustain the relationships it has with the diverse interested groups in its sphere of operations. This is not in agreement with the background of the norm that a firm is for improving the net-worth of the shareholders alone. However, in comparison, a firm has a role to itself as well as the other parties connected to for effectiveness and efficiency in order to take advantage of legitimate rights for existence (Jizi et al., 2014![]() ). In addition, this theory has assisted researchers to examine the difference between performance antecedents and outcomes, even though it has enhanced the basis for evaluating performance in a more all-inclusive manner since one stakeholder group or the other can have their satisfaction determined through a measure of performance or the other. This perspective of assessing firm performance is peculiar to different groups of firms (Carneiro et al., 2007

). In addition, this theory has assisted researchers to examine the difference between performance antecedents and outcomes, even though it has enhanced the basis for evaluating performance in a more all-inclusive manner since one stakeholder group or the other can have their satisfaction determined through a measure of performance or the other. This perspective of assessing firm performance is peculiar to different groups of firms (Carneiro et al., 2007![]() ) due to its ability to generate the background on which the various stakeholders evaluate the firms. Furthermore, in order to enhance the performance of the firm to the advantage of the stakeholders, the resources and capabilities owned are to be fully utilised alongside knowledge and information sharing through sustainability initiatives. This theory is, recommended for the benefits of creating a high level of awareness for its importance to an area of study like this, whereby it creates the needed perception for responsibility with respect to everyone group that is linked to a firm and vice versa. Consequently, the agency theory is to generate evidence as to the relationships between principals and agents in the corporate world, in terms of issues that generate conflict of interests such as enhanced rewards to the business owners, increased packages for responsibilities handled by the agent, minimisation of transaction and administrative costs, maintenance of mutual relationships with regulatory public agencies, etc. Nonetheless, in corporate finance, the problems with agency issues are in relation to the conflict of interests that exist between the management and shareholders of an entity. Additionally, Jensen and Meckling (1976

) due to its ability to generate the background on which the various stakeholders evaluate the firms. Furthermore, in order to enhance the performance of the firm to the advantage of the stakeholders, the resources and capabilities owned are to be fully utilised alongside knowledge and information sharing through sustainability initiatives. This theory is, recommended for the benefits of creating a high level of awareness for its importance to an area of study like this, whereby it creates the needed perception for responsibility with respect to everyone group that is linked to a firm and vice versa. Consequently, the agency theory is to generate evidence as to the relationships between principals and agents in the corporate world, in terms of issues that generate conflict of interests such as enhanced rewards to the business owners, increased packages for responsibilities handled by the agent, minimisation of transaction and administrative costs, maintenance of mutual relationships with regulatory public agencies, etc. Nonetheless, in corporate finance, the problems with agency issues are in relation to the conflict of interests that exist between the management and shareholders of an entity. Additionally, Jensen and Meckling (1976![]() ) are of the view that, it is of fundamental value in corporate governance, especially with respect to the ownership of the firm by the shareholders and the directors saddled with the everyday activities of the firm. In this study, the importance of this theory is to determine the degree to which it is undertaken, to describe the relationship between corporate governance and firm performance. Therefore, in line with the aforementioned theories, the following framework has been generated show the relationship between the Independent Variable (IV) and the Dependent Variable (DV).

) are of the view that, it is of fundamental value in corporate governance, especially with respect to the ownership of the firm by the shareholders and the directors saddled with the everyday activities of the firm. In this study, the importance of this theory is to determine the degree to which it is undertaken, to describe the relationship between corporate governance and firm performance. Therefore, in line with the aforementioned theories, the following framework has been generated show the relationship between the Independent Variable (IV) and the Dependent Variable (DV).

Figure-1. Framework IV and DV using Stakeholders and Agency Theories

In the recent times, the perspective of the institutional theory is required to substantiate sustainability initiatives (Caprar and Neville, 2012![]() ). This is due to the choice for the acceptance of sustainability, support for the relevance of national posture as a way for determining why firms favour institutional forces for evaluating performance and the embracing of cultural studies as the knowledge base for corporate values in relation to national perceptions. In addition, the theory aligns with the perspective that at the core of every social creation there is an institution, with many self-sustaining dimensions such as its cultural- regulative, normative, and cognitive possibilities. Hence, institutional norms and values are enduring, moveable and thus, create the basis for social attitudes and interactions (Scott, 1995

). This is due to the choice for the acceptance of sustainability, support for the relevance of national posture as a way for determining why firms favour institutional forces for evaluating performance and the embracing of cultural studies as the knowledge base for corporate values in relation to national perceptions. In addition, the theory aligns with the perspective that at the core of every social creation there is an institution, with many self-sustaining dimensions such as its cultural- regulative, normative, and cognitive possibilities. Hence, institutional norms and values are enduring, moveable and thus, create the basis for social attitudes and interactions (Scott, 1995![]() ). Therefore, institutional theory is significant for explaining how corporate engagements within a period enhance the structuring of sustainability and environmental disclosures due to its attention to the procedures undertaken to ensure their entrenchment in institutions or accepted initiatives. Institutional theorists have also admitted that institutional arrangements affect corporate members by reducing the available preferences, constraint particular configurations of resources distribution and limit specific sequences of actions (Di Maggio and Powell, 1991

). Therefore, institutional theory is significant for explaining how corporate engagements within a period enhance the structuring of sustainability and environmental disclosures due to its attention to the procedures undertaken to ensure their entrenchment in institutions or accepted initiatives. Institutional theorists have also admitted that institutional arrangements affect corporate members by reducing the available preferences, constraint particular configurations of resources distribution and limit specific sequences of actions (Di Maggio and Powell, 1991![]() ). In general terms, the main focus of the institutional proponents is that a firm’s survival is with respect to its ability to comply with the social norms or the conventional behaviour’ (Covaleski and Dirsmith, 1988

). In general terms, the main focus of the institutional proponents is that a firm’s survival is with respect to its ability to comply with the social norms or the conventional behaviour’ (Covaleski and Dirsmith, 1988![]() ). Many studies have engaged the institutional theory to validate social and environmental reporting (Chih et al., 2010

). Many studies have engaged the institutional theory to validate social and environmental reporting (Chih et al., 2010![]() ; Jackson and Apostolakou, 2010

; Jackson and Apostolakou, 2010![]() ) in alignment with other theories of stakeholder, legitimacy and social contract. In addition, the institutional theory perceives CG in relation to social and cultural impacts on organizations (Hilb, 2012

) in alignment with other theories of stakeholder, legitimacy and social contract. In addition, the institutional theory perceives CG in relation to social and cultural impacts on organizations (Hilb, 2012![]() ). This theory further substantiates the mediating role of sustainability initiatives, thus, the development of the conceptual framework for this study.

). This theory further substantiates the mediating role of sustainability initiatives, thus, the development of the conceptual framework for this study.

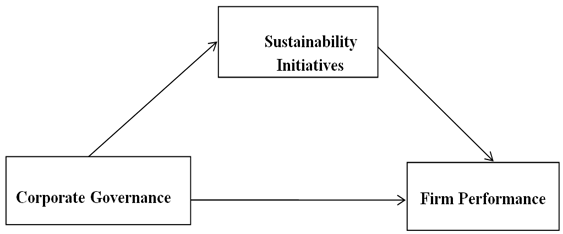

Figure-2. The Conceptual Framework of the Study

The conceptual framework of the study investigates the relationship between corporate governance and firm performance as a direct effect on one hand and CG and SI as well as SI and FP on the other hand. The indirect effect of SI as mediator on the relationship between CG and FP . Most studies reviewed have only argued based on the direct relationship between CG, and the individual sustainability elements (Emeni and Ugbogbo, 2014![]() ) assessed the relationship from the financial initiatives point of view. Once and Almogtome (2014

) assessed the relationship from the financial initiatives point of view. Once and Almogtome (2014![]() ) viewed the relationship from the perspective of the environmental initiatives while the studies by Orij (2010

) viewed the relationship from the perspective of the environmental initiatives while the studies by Orij (2010![]() ) and Adelopo et al. (2013

) and Adelopo et al. (2013![]() ) were from the social point of view. Therefore, the view in this paper is that studies are emphasised along this line of thought.

) were from the social point of view. Therefore, the view in this paper is that studies are emphasised along this line of thought.

2.1. Firm Performance (FP)

One of the ways by which investors can easily be encouraged is through the provision of grander financial performance which are premised on the increase in market value, growth and profitability (Filippetti, 2011![]() ; Chen and Huang, 2012

; Chen and Huang, 2012![]() ; Raposo et al., 2014

; Raposo et al., 2014![]() ; Rahman et al., 2017

; Rahman et al., 2017![]() ). On the other hand, the non-financial performance aspects are also of significance in a study of this nature (Harter et al., 2002

). On the other hand, the non-financial performance aspects are also of significance in a study of this nature (Harter et al., 2002![]() ); (Neville et al., 2005

); (Neville et al., 2005![]() ). Therefore, in this study, the firms’ financial performance and non- financial performance are the combined bases for the evaluation of performance. The latter is with respect to increasing employee satisfaction, and reputation of the firm while the former will emphasise on the growth in sales turnover and profit premised on the understanding and insights of the managers of the respective companies. Nevertheless, the issue of firm performance is important, therefore; there is a need to focus on the institutional factors of corporate governance, and sustainability initiatives.

). Therefore, in this study, the firms’ financial performance and non- financial performance are the combined bases for the evaluation of performance. The latter is with respect to increasing employee satisfaction, and reputation of the firm while the former will emphasise on the growth in sales turnover and profit premised on the understanding and insights of the managers of the respective companies. Nevertheless, the issue of firm performance is important, therefore; there is a need to focus on the institutional factors of corporate governance, and sustainability initiatives.

2.2. Corporate Governance (CG)

A tool adopted for the sake of mitigating the agency cost that is responsible for the creation of conflict of interest between the managers and shareholders is CG (Uwuigbe and Ajibolade, 2013![]() ). The latter can also otherwise, be the basis for reducing the lack of agreement of interests between shareholders and managers. It is, therefore, a corporate mechanism for maintaining the value of life for organisations in relation to the various stakeholders which include the shareholders, management, employees, government and their agencies, creditors, suppliers, consumers, and the public. Consequently, it has continued to feature prominently in the corporate arena due to the inconsequential performances of large multinational organisations such as Adelphia Parmalat, Enron, Cadbury, WorldCom, and Transmile Group in the time past. CG is the set of institutional arrangements deployed to evaluate corporate decision making efforts and as such required to examine the relationships among various groups to determine the direction and performance of organisations concerned. Nevertheless, having a solid CG in existence will bring about improved financial performance and rationalisation for creating the reward systems for shareholders and the various stakeholders collectively (Manolescu et al., 2011

). The latter can also otherwise, be the basis for reducing the lack of agreement of interests between shareholders and managers. It is, therefore, a corporate mechanism for maintaining the value of life for organisations in relation to the various stakeholders which include the shareholders, management, employees, government and their agencies, creditors, suppliers, consumers, and the public. Consequently, it has continued to feature prominently in the corporate arena due to the inconsequential performances of large multinational organisations such as Adelphia Parmalat, Enron, Cadbury, WorldCom, and Transmile Group in the time past. CG is the set of institutional arrangements deployed to evaluate corporate decision making efforts and as such required to examine the relationships among various groups to determine the direction and performance of organisations concerned. Nevertheless, having a solid CG in existence will bring about improved financial performance and rationalisation for creating the reward systems for shareholders and the various stakeholders collectively (Manolescu et al., 2011![]() ). However, the research efforts undertaken by Joe and Kankpang (2011

). However, the research efforts undertaken by Joe and Kankpang (2011![]() ) and Babatunde and Olaniran (2009

) and Babatunde and Olaniran (2009![]() ) have indicated that no significant emphasis had been on the explanatory and empirical investigations of the popular concept of CG despite haven gained prominence in the developed and emerging economies due to the reforms put in place with respect to the institutions. In particular, many of the significant research on CG in the last two decades or more have been associated with nations such as USA, Europe, South America and currently the Asian tiger nations (China, Japan, Taiwan, Hong Kong, Singapore, Malaysia, etc.) as a result of their commitment to spectacular research activities (Finegold et al., 2007

) have indicated that no significant emphasis had been on the explanatory and empirical investigations of the popular concept of CG despite haven gained prominence in the developed and emerging economies due to the reforms put in place with respect to the institutions. In particular, many of the significant research on CG in the last two decades or more have been associated with nations such as USA, Europe, South America and currently the Asian tiger nations (China, Japan, Taiwan, Hong Kong, Singapore, Malaysia, etc.) as a result of their commitment to spectacular research activities (Finegold et al., 2007![]() ; Siyanbola et al., 2014

; Siyanbola et al., 2014![]() ). In sum, the clamour here is to encourage intensive studies in this area of study with focus on the developing and less developed nations of Africa and other Asian and Latin American nations. In addition, the particularities, degree of readiness and implementation of the various codes of ethics already in existence, both locally and internationally in terms of their impact in ensuring adequate sustainability initiatives in these domains require proper investigation.

). In sum, the clamour here is to encourage intensive studies in this area of study with focus on the developing and less developed nations of Africa and other Asian and Latin American nations. In addition, the particularities, degree of readiness and implementation of the various codes of ethics already in existence, both locally and internationally in terms of their impact in ensuring adequate sustainability initiatives in these domains require proper investigation.

2.3. Sustainability Initiatives (SI)

The need for sustainability came alive with the release of the Brundtland Report of 1987 with the understanding that it is a “development that meets the needs of the present without compromising the ability of the future generations to meet their own needs” (WCED (World Commission on Environment and Development), 1987![]() ). This report awakened the attention of researchers and practitioners with a need to integrating the developmental dimensions of social, economic, and environmental concerns required to address the griefs of the globally poor people. Nevertheless, the issue of sustainability got to the peak in 1990 with the United Nations Conference on Sustainable Development held in Rio de Janeiro in Brazil. However, twenty years down the lane, the Rio+20 meeting reconsidered the subject of sustainability and this was followed by the Millennium Development Goals (MDGs) and was concluded with focus on the economic and environmental developmental goals without losing sight of the relevant element of social goals as effectively contained in the Sustainable Development Goals (SDGs). Furthermore, the Global Reporting Initiative (GRI, 2006

). This report awakened the attention of researchers and practitioners with a need to integrating the developmental dimensions of social, economic, and environmental concerns required to address the griefs of the globally poor people. Nevertheless, the issue of sustainability got to the peak in 1990 with the United Nations Conference on Sustainable Development held in Rio de Janeiro in Brazil. However, twenty years down the lane, the Rio+20 meeting reconsidered the subject of sustainability and this was followed by the Millennium Development Goals (MDGs) and was concluded with focus on the economic and environmental developmental goals without losing sight of the relevant element of social goals as effectively contained in the Sustainable Development Goals (SDGs). Furthermore, the Global Reporting Initiative (GRI, 2006![]() ) definition is more interesting because of its attention on six specific dimensions of economic, human rights, product responsibilities, labour practices and decent work, society, and the environment. In a similar manner, Chang (2016

) definition is more interesting because of its attention on six specific dimensions of economic, human rights, product responsibilities, labour practices and decent work, society, and the environment. In a similar manner, Chang (2016![]() ) views corporate sustainability as a comprehensive concept that addresses many socially inclined issues such as environmental protection, social justice, governance, diversity, product safety, employee welfare, and community well-being. Hence, sustainability challenges are significant integrated elements of strategic thought processes for everyone firm (Håkanson, 2010

) views corporate sustainability as a comprehensive concept that addresses many socially inclined issues such as environmental protection, social justice, governance, diversity, product safety, employee welfare, and community well-being. Hence, sustainability challenges are significant integrated elements of strategic thought processes for everyone firm (Håkanson, 2010![]() ; Moura-Leite et al., 2014

; Moura-Leite et al., 2014![]() ; Adedeji et al., 2017

; Adedeji et al., 2017![]() ; Rahman et al., 2017

; Rahman et al., 2017![]() ).

).

Previous literatures on sustainability issues are evidenced on the various types of studies that have been embarked upon in particular from the standpoints of the developing and developed countries with respect to the many dimensions of sustainability. They include financial disclosures (Imeokparia and Olagunju, 2013![]() ; Madawaki, 2014

; Madawaki, 2014![]() ) environmental management, performance and disclosures (Adebambo et al., 2014

) environmental management, performance and disclosures (Adebambo et al., 2014![]() ; Chaklader and Gulati, 2015

; Chaklader and Gulati, 2015![]() ) and social and environmental disclosures (Adhikari et al., 2015

) and social and environmental disclosures (Adhikari et al., 2015![]() ). Others are governance on social reporting (Haniffa and Cooke, 2005

). Others are governance on social reporting (Haniffa and Cooke, 2005![]() ; Orij, 2010

; Orij, 2010![]() ) legal institutions on corporate social disclosure (Adelopo et al., 2013

) legal institutions on corporate social disclosure (Adelopo et al., 2013![]() ) and legal origin or systems on financial disclosures (Hope, 2003

) and legal origin or systems on financial disclosures (Hope, 2003![]() ). The evidences available from the various studies, show proofs that the challenges of corporate sustainability require the desired attention in the less developed nations or emerging economies of Africa and Asia. This is especially in relation to the low focus with respect to quantity, quality, and content when a comparison is made with the developed nations of Europe, America, Australia, Russia and Japan, India, China in the Eastern bloc (Ioannou and Serafeim, 2014

). The evidences available from the various studies, show proofs that the challenges of corporate sustainability require the desired attention in the less developed nations or emerging economies of Africa and Asia. This is especially in relation to the low focus with respect to quantity, quality, and content when a comparison is made with the developed nations of Europe, America, Australia, Russia and Japan, India, China in the Eastern bloc (Ioannou and Serafeim, 2014![]() ). However, for the purpose of encouraging research work world-wide, initiatives have been evolved through groups such as B Corporation, Dow Jones Sustainability Index, Aspen Institute, Global Reporting Initiatives, ISO 26000, International Society of Sustainability Professionals, Sustainability Accounting Standards Board, UN Global Impact and MSCI ESG (formerly KLD) (Chang, 2016

). However, for the purpose of encouraging research work world-wide, initiatives have been evolved through groups such as B Corporation, Dow Jones Sustainability Index, Aspen Institute, Global Reporting Initiatives, ISO 26000, International Society of Sustainability Professionals, Sustainability Accounting Standards Board, UN Global Impact and MSCI ESG (formerly KLD) (Chang, 2016![]() ). In sum, the essence of this paper is to further inspire research on the regulatory and environmental issues with respect to sustainability initiatives world-wide.

). In sum, the essence of this paper is to further inspire research on the regulatory and environmental issues with respect to sustainability initiatives world-wide.

3. DEVELOPMENT OF HYPOTHESES IN RELATION TO THE CONCEPTUAL FRAMEWORK

3.1. Corporate Governance and Firm Performance

A well-defined corporate governance structure will ensure reduction of funds costs, easy funds accessibility, improved sound corporate firm performance through stakeholders’ support for greater firm value, and enhanced investment rate of return (Brown and Caylor, 2009![]() ). Many of the studies in Asia have produced positive significant outcomes (Black and Kim, 2012

). Many of the studies in Asia have produced positive significant outcomes (Black and Kim, 2012![]() ; Shukeri et al., 2012

; Shukeri et al., 2012![]() ; Ahmed and Hamdan, 2015

; Ahmed and Hamdan, 2015![]() ) while negative significant result were revealed by others (Garg, 2007

) while negative significant result were revealed by others (Garg, 2007![]() ). Darmadi (2011

). Darmadi (2011![]() ) examined the association between educational qualifications of directors and the value of the company and the result show that the educational qualifications of directors have a significant role in enhancing the performance of the company. Again, Darmadi examined the impact of the size of other directors (both director and commissioner) excluding the females on firm performance, and confirmed a positive and significant effect. However, Dong and Ozkan (2008

) examined the association between educational qualifications of directors and the value of the company and the result show that the educational qualifications of directors have a significant role in enhancing the performance of the company. Again, Darmadi examined the impact of the size of other directors (both director and commissioner) excluding the females on firm performance, and confirmed a positive and significant effect. However, Dong and Ozkan (2008![]() ) find a positive relationship between remuneration and firm performance. Nonetheless, Basyith (2016

) find a positive relationship between remuneration and firm performance. Nonetheless, Basyith (2016![]() ) asserts that the government and private ownership status are negative and not significant, revealing that ownership status has no influence on firm performance whereas the foreign ownership status is positive and not significant, meaning that foreign ownership status has no impact on firm performance. In the case of Nigeria, Kajola (2008

) asserts that the government and private ownership status are negative and not significant, revealing that ownership status has no influence on firm performance whereas the foreign ownership status is positive and not significant, meaning that foreign ownership status has no impact on firm performance. In the case of Nigeria, Kajola (2008![]() ) indicate that ROE and board size, profit margin and chief executive officer’s status have positive and significant relationship between them, as well as ROE, board composition and audit committees, and finally between profit margin and board size, board composition and audit committee. However, Eyenubo (2013

) indicate that ROE and board size, profit margin and chief executive officer’s status have positive and significant relationship between them, as well as ROE, board composition and audit committees, and finally between profit margin and board size, board composition and audit committee. However, Eyenubo (2013![]() ) and Uwuigbe and Ajibolade (2013

) and Uwuigbe and Ajibolade (2013![]() ) found negative significant relationship between large board size and Net Profit after Tax (NPAT) and negative and insignificant relationship between ownership structure and firm share value while the audit committee independence show a positive and significant correlation with share price respectively. From the findings as above, the outcomes have not been consistent apart from the fact that they mostly focused on the listed companies and not on the medium sized companies. Therefore, the following is the hypothesis:

) found negative significant relationship between large board size and Net Profit after Tax (NPAT) and negative and insignificant relationship between ownership structure and firm share value while the audit committee independence show a positive and significant correlation with share price respectively. From the findings as above, the outcomes have not been consistent apart from the fact that they mostly focused on the listed companies and not on the medium sized companies. Therefore, the following is the hypothesis:

H1: CG has a positive relationship with FP of companies.

3.2. CG and SI

Corporate governance is beginning to gain relevance as an area of study in relation to the execution of sustainability issues as businesses are gradually emphasising on sustainability as an avenue for increasing corporate value (Warren-Myers, 2013![]() ). Again, CG enhances corporate performance in general (Klettner et al., 2014

). Again, CG enhances corporate performance in general (Klettner et al., 2014![]() ) as well as minimising costs of doing business and increasing profits (Lacy and Hayward, 2011

) as well as minimising costs of doing business and increasing profits (Lacy and Hayward, 2011![]() ). Therefore, there is a need to identify the interrelatedness of the concepts of CG and SI. Solid CG is the bedrock on which the board and management decide on goals that are helpful to the company and its stakeholders and ensure proper coordination (OECD, 2004; cited by Honoré et al. (2015

). Therefore, there is a need to identify the interrelatedness of the concepts of CG and SI. Solid CG is the bedrock on which the board and management decide on goals that are helpful to the company and its stakeholders and ensure proper coordination (OECD, 2004; cited by Honoré et al. (2015![]() )). Hence, sustainable CG is a practice generally used to envisage and cope with potential risks to legitimacy and corporate reputation (Blowfield and Dolan, 2010

)). Hence, sustainable CG is a practice generally used to envisage and cope with potential risks to legitimacy and corporate reputation (Blowfield and Dolan, 2010![]() ) cited by Li et al. (2014

) cited by Li et al. (2014![]() ). However, Janggu et al. (2014

). However, Janggu et al. (2014![]() ) in their study of the impact of CG on the sustainability of firms in Malaysia in 2010 premised on agency theory show that the professionalism and size of the board and the members’ composition have a significant effect on sustainability initiatives efforts. In the same vein, Klettner et al. (2014

) in their study of the impact of CG on the sustainability of firms in Malaysia in 2010 premised on agency theory show that the professionalism and size of the board and the members’ composition have a significant effect on sustainability initiatives efforts. In the same vein, Klettner et al. (2014![]() ) in their study of CG activities with respect to sustainability initiatives in 50 Australian companies, found that leadership structures included both the board of directors and the general management in the expansion of sustainability initiatives with the objective of getting financial compensations. Hence, sustainability initiatives are keys to sustaining or enhancing the value of a firm. Based on the aforementioned, the hypothesis is:

) in their study of CG activities with respect to sustainability initiatives in 50 Australian companies, found that leadership structures included both the board of directors and the general management in the expansion of sustainability initiatives with the objective of getting financial compensations. Hence, sustainability initiatives are keys to sustaining or enhancing the value of a firm. Based on the aforementioned, the hypothesis is:

H2: CG has a positive relationship with SI of companies.

3.3. SI and FP

Sustainability initiatives issues are gradually becoming sources of worry for both local and multinational enterprises. In the light of this, the ultimate consumers of their goods and services are agitated as to the manner in which these enterprises care for their workers and the immediate societies where they are located. Despite the challenges faced administratively, theoretical and empirical studies indicate that a positive relationship exists between sustainability initiatives and competitiveness in the international environments (Weber et al., 2010![]() ). Hence, conscientious determination to guarantee a reputation of social sustainability initiatives could influence the profit limits of the firm, with top managers being conscious of the latter. Therefore, the principal officers of the highly rated firms understand “that sustainability initiatives can promote respect for their company in the marketplace,” resulting in “higher sales, enhanced employee loyalty,” and better attraction and retention of personnel to the firm (Cho et al., 2015

). Hence, conscientious determination to guarantee a reputation of social sustainability initiatives could influence the profit limits of the firm, with top managers being conscious of the latter. Therefore, the principal officers of the highly rated firms understand “that sustainability initiatives can promote respect for their company in the marketplace,” resulting in “higher sales, enhanced employee loyalty,” and better attraction and retention of personnel to the firm (Cho et al., 2015![]() ).

).

According to Gray et al. (1995![]() ) and Bebbington et al. (2008

) and Bebbington et al. (2008![]() ) the creation of sustainability initiatives (SI) will enable firms to enhance the exhibition of social image that will ensure increased corporate performance in terms of reputation and minimise reputational risks. Furthermore, SI contributes to corporate performance from the point of view of ensuring increased market value, creation of investment appeal and causing firms to be more attractive. In addition, firms can be able to fulfill their responsibilities to their numerous stakeholders by being socially responsible. Therefore, the incorporation of environmental and social initiatives in the corporate profile of firms goes a long way in consolidating the relationship between the firm and the stakeholders which will enhance the ability to generate information on the endeavours of the firms to the extent of informing, educating and varying the perceptions and prospects of the interested parties. In addition, Jo and Harjoto (2012

) the creation of sustainability initiatives (SI) will enable firms to enhance the exhibition of social image that will ensure increased corporate performance in terms of reputation and minimise reputational risks. Furthermore, SI contributes to corporate performance from the point of view of ensuring increased market value, creation of investment appeal and causing firms to be more attractive. In addition, firms can be able to fulfill their responsibilities to their numerous stakeholders by being socially responsible. Therefore, the incorporation of environmental and social initiatives in the corporate profile of firms goes a long way in consolidating the relationship between the firm and the stakeholders which will enhance the ability to generate information on the endeavours of the firms to the extent of informing, educating and varying the perceptions and prospects of the interested parties. In addition, Jo and Harjoto (2012![]() ) show that SI positively influences Corporate Financial Performance (CFP) and that firms’ SI in relation to the employees, diversity, community, and environment play a significantly positive role in enhancing CFP. In the light of the foregoing, the hypothesis is:

) show that SI positively influences Corporate Financial Performance (CFP) and that firms’ SI in relation to the employees, diversity, community, and environment play a significantly positive role in enhancing CFP. In the light of the foregoing, the hypothesis is:

H3: Sustainability initiatives have positive relationship with FP of companies.

3.4. CG---SI----FP

Jaswadi et al. (2015![]() ) are of the opinion that Supervisory and Management Board can come together to generate innovative and creative philosophies or thoughts for the managements of SMEs. In addition, the supervisory board can complement the efforts of the management board with respect to strategic planning, sourcing for capital and achievement of the confidence of lenders or investors. Furthermore, Jo and Harjoto (2012

) are of the opinion that Supervisory and Management Board can come together to generate innovative and creative philosophies or thoughts for the managements of SMEs. In addition, the supervisory board can complement the efforts of the management board with respect to strategic planning, sourcing for capital and achievement of the confidence of lenders or investors. Furthermore, Jo and Harjoto (2012![]() ) assert that CG variables positively affect firms’ SI, after controlling for various firm characteristics. Janggu et al. (2014

) assert that CG variables positively affect firms’ SI, after controlling for various firm characteristics. Janggu et al. (2014![]() ) and Shamil et al. (2014

) and Shamil et al. (2014![]() ) opined that large boards have more effect on sustainability matters and are likely to enhance their sustainability initiatives. In addition, many of the past studies show that a positive relationship exist between board size and corporate sustainability initiatives disclosable (Esa and Anum, 2012

) opined that large boards have more effect on sustainability matters and are likely to enhance their sustainability initiatives. In addition, many of the past studies show that a positive relationship exist between board size and corporate sustainability initiatives disclosable (Esa and Anum, 2012![]() ). Still, the independent directors have greater tendency to promote more initiatives to increase the sustainability performance of the firms. Meanwhile, many studies according to Akhtaruddin and Haron (2010

). Still, the independent directors have greater tendency to promote more initiatives to increase the sustainability performance of the firms. Meanwhile, many studies according to Akhtaruddin and Haron (2010![]() ) have indicated a positive association between the proportion of independent directors and voluntary sustainability initiatives issues.

) have indicated a positive association between the proportion of independent directors and voluntary sustainability initiatives issues.

The array of causal relationship through which independent variable shows its impact on the dependent variable through the effect of overriding third variable is mediation (Hayes, 2013![]() ). The latter aids the ability to determine the total effect (direct effect plus indirect effect). Therefore, in order to understand the mediation process, adopt (Baron and Kenny, 1986

). The latter aids the ability to determine the total effect (direct effect plus indirect effect). Therefore, in order to understand the mediation process, adopt (Baron and Kenny, 1986![]() ) four steps that help to justify SI as a mediator in relation to this study.

) four steps that help to justify SI as a mediator in relation to this study.

i) There must be a significant association between the independent and dependent variables. From our earlier reviews, it was ascertained that there is a significant relationship between CG and FP (Cheung et al., 2010![]() ; Sami et al., 2011

; Sami et al., 2011![]() ; Ahmed and Hamdan, 2015

; Ahmed and Hamdan, 2015![]() ).

).

ii) There must be a significant relationship between the independent and mediator variables. Based on the reviews made earlier, CG and SI have significant relationship (Janggu et al., 2014![]() )(Klettner et al., 2014

)(Klettner et al., 2014![]() ).

).

iii) There must be a significant relationship between the dependent and mediator. The reviews show that a significant relationship exist between SI and FP (Jo and Harjoto, 2012![]() ) and

) and

iv) There must be the inclusion of SI, (i.e. mediator and indirect association become significant) that makes the direct association between CG and FP turns out to be zero. Then, there is a full mediation. However, if the direct connection is significantly minimised, then, there is partial mediation, but where the direct link is still significant, no mediation takes place.

In addition to the assumptions of Hayes (2013![]() ) and from the above discussed literatures, it is clear that SI can be a mediator in the relationship between CG and FP, because, it has significant relations with both independent (CG) and dependent (FP) variables. Therefore, the hypothesis is:

) and from the above discussed literatures, it is clear that SI can be a mediator in the relationship between CG and FP, because, it has significant relations with both independent (CG) and dependent (FP) variables. Therefore, the hypothesis is:

H4: Sustainability initiatives may mediate the relationship between corporate governance and FP of companies.

4. CONTRIBUTION AND IMPLICATIONS

The effect of CG on social and environmental initiatives and performance have been the subject of discuss in the developed economies, but little has been done in this area in the less developed nations. Therefore, it is important to determine the influence of CG as a variable for ensuring effectiveness and efficiency in sustainability initiatives by listed corporate and unlisted entities especially in the developing climes for the enhancement of firm performance.

5. CONCLUSION AND RECOMMENDATIONS FOR FUTURE RESEARCH

It is indeed necessary to be clear about the need for applying these theories in practice or in any other study that, they are not adoptable at the same time, but a mix of them, will help to have numerous studies carried out based on strong theoretical underpinnings that are required to substantiate the outcome of research efforts. The issues related to CG can inform the perception of operators in the various facets of human endeavours that includes sustainability initiatives. However, the efficiency and effectiveness of these initiatives are improvable with the introduction of intellectual capital (human, relational, structural and spiritual) that helps to focus attention on the resources and capabilities of a firm in order to have competitive advantage. Therefore, this study has suggested the conceptual relationships between CG and FP on one hand and on the other hand the relationships between CG and SI as well as the mediating role of SI between CG and FP especially from the perspective of emerging and developing nations. However, further studies are required with respect to intellectual capital, sustainability initiatives, and firm performance, especially with emphasis on the mediating role of SI.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Adebambo, H.O., H. Ashari and N. Nordin, 2014. Sustainable environmental manufacturing practice (SEMP) and firm performance: Moderating role of environmental regulations. Journal of Management and Sustainability, 4(4): 167–177. Available at: https://doi.org/10.5539/jms.v4n4p167.

Adedeji, B.S., O.M.J. Popoola and T. San Ong, 2017. National culture and sustainability disclosure practices: A literature review. Indian-Pacific Journal of Accounting and Finance, 1(1): 26-50.

Adedeji, S.B., M.M. Rahman, I.S. Khairdddin, M.J. Uddin and M.S. Rahaman, 2017. A synthesised literature review on organisational culture and corporate performance. Journal of Advanced Research in Social and Behavioural Sciences, 7(1): 83-95.

Adelopo, I., C.R. Moure and M. Obalola, 2013. On the effects of legal and cultural institutions on corporate social disclosures by banks, Occasional Paper No. 87, Leicester Business School, De Montfort University, Leicester. UK: 1-21.

Adhikari, A., D. Emerson, A. Gouldman and R. Tondkar, 2015. An examination of corporate social disclosures of multinational corporations: A cross-national investigation. Advances in Accounting, 31(1): 100-106. Available at: https://doi.org/10.1016/j.adiac.2015.03.010.

Ahmed, E. and A. Hamdan, 2015. The impact of corporate governance on firm performance: Evidence from Bahrain Bourse. International Management Review, 11(2): 21-37.

Akhtaruddin, M. and H. Haron, 2010. Board ownership, audit committees' effectiveness and corporate voluntary disclosures. Asian Review of Accounting, 18(1): 68-82. Available at: https://doi.org/10.1108/13217341011046015.

Akinboade, O.A., 2015. Regulation, SMEs' growth and performance in Cameroon's central and littoral provinces' manufacturing and retail sectors. African Development Review, 26(4): 597-609. Available at: https://doi.org/10.1111/1467-8268.12116.

Babatunde, M.A. and O. Olaniran, 2009. The effects of internal and external mechanism on governance and performance of corporate firms in Nigeria. Corporate Ownership & Control, 7(2): 330-344. Available at: https://doi.org/10.22495/cocv7i2c3p1.

Baron, R.M. and D.A. Kenny, 1986. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6): 1173. Available at: https://doi.org/10.1037//0022-3514.51.6.1173.

Basyith, A., 2016. Corporate governance, intellectual capital and firm performance. Research in Applied Economics, 8(1): 17-41. Available at: https://doi.org/10.5296/rae.v8i1.8675.

Bebbington, J., C. Larrinaga and J.M. Moneva, 2008. Corporate social reporting and reputation risk management. Accounting, Auditing & Accountability Journal, 21(3): 337-361. Available at: https://doi.org/10.1108/09513570810863932.

Black, B. and W. Kim, 2012. The effect of board structure on firm value: A multiple identification strategies approach using Korean data. Journal of Financial Economics, 104(1): 203-226. Available at: https://doi.org/10.1016/j.jfineco.2011.08.001.

Blowfield, M. and C. Dolan, 2010. Outsourcing governance: Fairtrade's message for C21 global governance. Corporate Governance: The International Journal of Business in Society, 10(4): 484-499. Available at: https://doi.org/10.1108/14720701011069704.

Brown, L.D. and M.L. Caylor, 2009. Corporate governance and firm operating performance. Review of Quantitative Finance and Accounting, 32(2): 129-144.

Caprar, D.V. and B.A. Neville, 2012. Norming and “conforming”: Integrating cultural and institutional explanations for sustainability adoption in business. Journal of Business Ethics, 110(2): 231-245. Available at: https://doi.org/10.1007/s10551-012-1424-1.

Carneiro, J.M., J.D. Silva, A.D. Rocha and L.D.R. Dib, 2007. Building a better measure of business performance. RAC-Eletrônica, 1(2): 114-135.

Carton, R.B. and C.W. Hofer, 2006. Measuring organizational performance: Metrics for entrepreneurship and strategic management research. Cheltenham, UK: Edward Elgar Publishing.Limited.

Chaklader, B. and P.A. Gulati, 2015. A study of corporate environmental disclosure practices of companies doing business in India. Global Business Review, 16(2): 321-335. Available at: https://doi.org/10.1177/0972150914564430.

Chang, S.J., 2016. Sustainable evolution for global business: A synthetic review of the literature. Journal of Management and Sustainability, 6(1): 1-23. Available at: https://doi.org/10.5539/jms.v6n1p1.

Chen, Y.-Y. and H.-L. Huang, 2012. Knowledge management fit and its implications for business performance: A profile deviation analysis. Knowledge-Based Systems, 27: 262–270. Available at: https://doi.org/10.1016/j.knosys.2011.11.012.

Cheung, Y.L., P. Jiang, P. Limpaphayom and T. Lu, 2010. Corporate governance in China: A step forward. European Financial Management, 16(1): 94-123. Available at: https://doi.org/10.1111/j.1468-036x.2008.00446.x.

Chih, H.-L., H.-H. Chih and T.-Y. Chen, 2010. On the determinants of corporate social responsibility: International evidence on the financial industry. Journal of Business Ethics, 93(1): 115-135. Available at: https://doi.org/10.1007/s10551-009-0186-x.

Cho, C.H., M. Laine, R.W. Roberts and M. Rodrigue, 2015. Organized hypocrisy, organizational façades, and sustainability reporting. Accounting, Organizations and Society, 40(C): 78-94. Available at: https://doi.org/10.1016/j.aos.2014.12.003.

Covaleski, M.A. and M.W. Dirsmith, 1988. An institutional perspective on the rise, social transformation, and fall of a university budget category. Administrative Science Quarterly, 33(4): 562-587. Available at: https://doi.org/10.2307/2392644.

Darmadi, S., 2011. Board compensation, corporate governance, and firm performance in Indonesia: 1-45. Available from https://ssrn.com/abstract=1907103 or http://dx.doi.org/10.2139/ssrn.1907103 .

Dess, G.G. and J.R.B. Robinson, 1984. Measuring organizational performance in the absence of objective measures: The case of the privately-held firm and conglomerate business unit. Strategic Management Journal, 5(3): 265-273. Available at: https://doi.org/10.1002/smj.4250050306.

Di Maggio, P.J. and W.W. Powell, 1991. The iron cage revisited institutional isomorphism and collective rationality in organizational fields. In: Powell WW og DiMaggio, PJ (red.). The New Institutionalism in Organizational Analysis.

Dong, M. and A. Ozkan, 2008. Institutional investors and director pay: An empirical study of UK companies. Journal of Multinational Financial Management, 18(1): 16-29. Available at: https://doi.org/10.1016/j.mulfin.2007.06.001.

Emeni, F.K. and S.N. Ugbogbo, 2014. Accounting frameworks and cross-cultural effects on accounting disclosure practices in Nigeria. Covenant Journal of Business and Social Sciences, 6(2): 48-69.

Ernst and Young, 2013. Global review. Available from https://www.ey.com/Publication/vwLUAssets/EY_Global_review_2013/$FILE/EY_Global_review_2013.pdf .

Esa, E. and M.G.N. Anum, 2012. Corporate social responsibility and corporate governance in Malaysian government-linked companies. Corporate Governance: The International Journal of Business in Society, 12(3): 292-305. Available at: https://doi.org/10.1108/14720701211234564.

Eyenubo, A.S., 2013. The impact of bigger board size on financial performance for firms: The Nigerian experience. Journal of Research in International Business and Management, 3(3): 85-90.

Falshaw, J.R., K.W. Glaister and E. Tatoglu, 2006. Evidence on formal strategic planning and company performance. Management Decision, 44(1): 9-30. Available at: https://doi.org/10.1108/00251740610641436.

Filippetti, A., 2011. Innovation modes and design as a source of innovation: A firm-level analysis. European Journal of Innovation Management, 14(1): 5-26. Available at: https://doi.org/10.1108/14601061111104670.

Finegold, D., G.S. Benson and D. Hecht, 2007. Corporate boards and company performance: Review of research in light of recent reforms. Corporate Governance: An International Review, 15(5): 865-878. Available at: https://doi.org/10.1111/j.1467-8683.2007.00602.x.

Garg, A.K., 2007. Influence of board size and independence on firm performance: A study of Indian companies. Vikalpa, 32(3): 39-60.

Gray, R., R. Kouhy and S. Lavers, 1995. Corporate social and environmental reporting: A review of the literature and a longitudinal study of UK disclosure. Accounting, Auditing & Accountability Journal, 8(2): 47-77. Available at: https://doi.org/10.1108/09513579510146996.

GRI, 2006. G4 Sustainability reporting guidelines. Available from https://www.globalreporting.org/resourcelibrary/GRIG4-Part2-Implementation-Manual.pdf [Accessed 01/10/2016].

Håkanson, L., 2010. The firm as an epistemic community: The knowledge-based view revisited. Industrial and Corporate Change, 19(6): 1801-1828. Available at: https://doi.org/10.1093/icc/dtq052.

Haniffa, R.M. and T.E. Cooke, 2005. The impact of culture and governance on corporate social reporting. Journal of Accounting and Public Policy, 24(5): 391-430. Available at: https://doi.org/10.1016/j.jaccpubpol.2005.06.001.

Harter, J.K., F.L. Schmidt and T.L. Hayes, 2002. Business-unit-level relationship between employee satisfaction, employee engagement, and business outcomes: A meta-analysis. Journal of Applied Psychology, 87(2): 268-279. Available at: https://doi.org/10.1037//0021-9010.87.2.268.

Hayes, A.F., 2013. Introduction to mediation, moderation, and conditional process analysis: A regression-based approach. New York: The Guilford Press.

Hilb, M., 2012. New corporate governance successful board management tools. 4th Edn., Berlin: Springer. pp: 1-237.

Honoré, F., F. Munari and B.V.P. De La Potterie, 2015. Corporate governance practices and companies’ R&D intensity: Evidence from European countries. Research Policy, 44(2): 533-543. Available at: https://doi.org/10.1016/j.respol.2014.10.016.

Hope, O.K., 2003. Firm‐level disclosures and the relative roles of culture and legal origin. Journal of International Financial Management & Accounting, 14(3): 218-248. Available at: https://doi.org/10.1111/1467-646x.00097.

Imeokparia, L. and A. Olagunju, 2013. Impact of environmental factors on the practice of accounting in Nigeria: A 10-year longitudinal study (2001-2011). Prime Journal of Business Administration and Management, 3(4): 2251-1261.

Ioannou, I. and G. Serafeim, 2014. The consequences of mandatory corporate sustainability reporting: Evidence from four countries. Harvard Business School Review, Working Paper, 11-100: 1-34.

Jackson, G. and A. Apostolakou, 2010. Corporate social responsibility in Western Europe: An institutional mirror or substitute? Journal of Business Ethics, 94(3): 371-394.

Jackson, L.A., 2017. Women and work culture: Britain c. 1850–1950. Oxford, UK: Routledge. Taylor & Francis Group Ltd. 1-264.

Janggu, T., F. Darus, M.M. Zain and Y. Sawani, 2014. Does good corporate governance lead to better sustainability reporting? An analysis using structural equation modelling. Procedia-Social and Behavioural Sciences, 145: 138-145. Available at: https://doi.org/10.1016/j.sbspro.2014.06.020.

Jaswadi, M. Igbal and Sumiadji, 2015. SME governance in Indonesia: A survey and insight from private companies. Procedia Finance and E-economics Journal, 31: 387-398.

Jensen, M.C. and W.H. Meckling, 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4): 305-360. Available at: https://doi.org/10.1016/0304-405x(76)90026-x.

Jizi, M.I., A. Salama, R. Dixon and R. Stratling, 2014. Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. Journal of Business Ethics, 125(4): 601-615. Available at: https://doi.org/10.1007/s10551-013-1929-2.

Jo, H. and M.A. Harjoto, 2012. The causal effect of corporate governance on corporate social responsibility. Journal of Business Ethics, 106(1): 53-72.

Joe, D.I.I. and K.A. Kankpang, 2011. Linking corporate governance with organizational performance: New insights and evidence from Nigeria. Global Journal of Management and Business Research, 11(12): 46-58.

Kajola, S.O., 2008. Corporate governance and firm performance: The case of Nigerian listed firms. European Journal of Economics, Finance and Administrative Sciences, 14(14): 16-28.

Kakabadse, N.K., C. Rozuel and L. Lee-Davies, 2005. Corporate social responsibility and stakeholder approach: A conceptual review. International Journal of Business Governance and Ethics, 1(4): 277-302.

Klettner, A., T. Clarke and M. Boersma, 2014. The governance of corporate sustainability: Empirical insights into the development, leadership and implementation of responsible business strategy. Journal of Business Ethics, 122(1): 145-165. Available at: https://doi.org/10.1007/s10551-013-1750-y.

Lacy, P. and R. Hayward, 2011. A new era of sustainability in emerging markets? Insights from a global CEO study by the united nations global compact and accenture. Corporate Governance: The International Journal of Business in Society, 11(4): 348-357. Available at: https://doi.org/10.1108/14720701111159208.

Li, Y., X. Zhao, D. Shi and X. Li, 2014. Governance of sustainable supply chains in the fast fashion industry. European Management Journal, 32(5): 823-836. Available at: https://doi.org/10.1016/j.emj.2014.03.001.

Madawaki, A., 2014. The impact of regulatory framework and environmental factors on accounting practices by firms in Nigeria. Procedia - Social and Behavioral Sciences, 164: 282–290. Available at: https://doi.org/10.1016/j.sbspro.2014.11.078.

Mahmood, R. and N. Hanafi, 2013. Entrepreneurial orientation and business performance of women-owned small and medium enterprises in Malaysia: Competitive advantage as a mediator. International Journal of Business and Social Science, 4(1): 82-90.

Manolescu, M., A.G. Roman and M. Mocanu, 2011. Corporate governance in Romania: From regulation to implementation. Accounting and Management Information Systems, 10(1): 4-24.

Moura-Leite, R., P. Robert and G. José, 2014. Stakeholder management and non-participation in controversial business. Business and Society, 53(1): 45-70. Available at: https://doi.org/10.1177/0007650310395547.

Neville, B.A., S.J. Bell and B. Mengüç, 2005. Corporate reputation, stakeholders and the social performance-financial performance relationship. European Journal of Marketing, 39(9/10): 1184-1198. Available at: https://doi.org/10.1108/03090560510610798.

Olaoye, S.O., A.N. Nwaobia and O.A. Oshadiya, 2016. Corporate governance and organizational growth: An assessment of the Nigerian manufacturing industry. Journal of Accounting and Financial Management, 2(5): 1-14.

Once, S. and A. Almogtome, 2014. The relationship between Hofsted’s national cultural values and corporate environmental disclosure: An international perspective. Research Journal of Business and Management, 1(3): 279-304.

Orij, R., 2010. Corporate social disclosures in the context of national cultures and stakeholder theory. Accounting, Auditing & Accountability Journal, 23(7): 868-889. Available at: https://doi.org/10.1108/09513571011080162.

Rahman, M.M., S.B. Adedeji, M.J. Uddin and M.S. Rahaman, 2017. Entrepreneurship mindset for students’ entrepreneurship build-up: A review paper. International Journal of Multidisciplinary Advanced Scientific Research and Innovation, 1(1): 26-34.

Raposo, M.L., J.J. Ferreira and C.I. Fernandes, 2014. Local and cross-border SME cooperation: Effects on innovation and performance. European Journal of Business Management and Economics, 23(4): 157-165. Available at: https://doi.org/10.1016/j.redee.2014.08.001.

Rauch, A., J. Wiklund, G.T. Lumpkin and M. Frese, 2009. Entrepreneurial orientation and business performance: An assessment of past research and suggestions for the future. Entrepreneurship Theory and Practice, 33(3): 761-787. Available at: https://doi.org/10.1111/j.1540-6520.2009.00308.x.

Richard, P.J., T.M. Devinney, G.S. Yip and G. Johnson, 2009. Measuring organizational performance: Towards methodological best practice. Journal of Management, 35(3): 718-804. Available at: https://doi.org/10.1177/0149206308330560.

Sami, H., J. Wang and H. Zhou, 2011. Corporate governance and operating performance of Chinese listed firms. Journal of International Accounting, Auditing and Taxation, 20(2): 106-114. Available at: https://doi.org/10.1016/j.intaccaudtax.2011.06.005.

Scott, W.R., 1995. Institutions and organizations. Foundations for organizational science. London: A Sage Publication Series.

Shamil, M.M., J.M. Shaikh, P.-L. Ho and A. Krishnan, 2014. The influence of board characteristics on sustainability reporting: Empirical evidence from Sri Lankan firms. Asian Review of Accounting, 22(2): 78-97. Available at: https://doi.org/10.1108/ara-09-2013-0060.

Shukeri, S.N., O.W. Shin and M.S. Shaari, 2012. Does board of director’s characteristics affect firm performance? Evidence from Malaysian public listed companies. International Business Research, 5(9): 120-127. Available at: https://doi.org/10.5539/ibr.v5n9p120.

Siyanbola, T.T., S.B. Adedeji and D. Sobande, 2014. Effective corporate governance as a panacea to business survival in Nigeria. International Journal of Advanced Studies in Business Strategies and Management, 2(1): 139-153.

Tan, I.K., T.S. Ong, S.B. Adedeji and L.L. Chong, 2016. Auditors switching in the relationship between corporate governance and financial performances-evidence from Malaysian public listed companies (PLCs). International Journal of Economics and Management, 10(1): 53-68.

Teh, B.H., T.S. Ong, B.S. Adedeji and S.H. Ng, 2016. An empirical study of auditors switching, corporate governance and financial performances of Malaysian public listed companies (PLCs). Journal of Management, 47(1): 43-53.

Uwuigbe, U. and S. Ajibolade, 2013. Effects of corporate governance on corporate social and environmental disclosure among listed firms in Nigeria. European Journal of Business and Social Sciences, 2(5): 76-92.

Warren-Myers, G., 2013. Is the valuer the barrier to identifying the value of sustainability? Journal of Property Investment & Finance, 31(4): 345-359. Available at: https://doi.org/10.1108/jpif-01-2013-0004.

WCED (World Commission on Environment and Development), 1987. Our common future. Oxford, England: Oxford University Press.

Weber, O., R.W. Scholz and G. Michalik, 2010. Incorporating sustainability criteria into credit risk management. Business Strategy and the Environment, 19(1): 39-50.

Views and opinions expressed in this article are the views and opinions of the author(s), International Journal of Asian Social Science shall not be responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content. |