THE ACCEPTANCE OF NEW MODEL OF BARAKAH HOUSE FINANCING AMONG PUBLIC IN MALAYSIA

1,2,3,4,5Faculty of Economic and Management Sciences, Universiti Sultan Zainal Abidin, Kuala 21300 Kuala Nerus, Terengganu, Malaysia

ABSTRACT

A new model of Barakah house financing among public in Malaysia has been constructed using the Integration model. The objective of this research is to examine the public acceptance towards the newly constructed model. The sum of 300 respondents has been chosen in conducting this survey in Malaysia. The distributed questionnaires comprise of one dependent variable and four independent variables to realize this study. In the application of SEM-Amos, it has been indicated that all of the independent variables of knowledge, quality, benefit, marketing and product have strong correlation with the premium dependent variable. Thus, it can be concluded that the new constructed model has been accepted by the public. Therefore, it is recommended that this new plan is can be implemented by the authority as well as the related companies those have offered a house financing plan in Malaysia.

Keywords:Integration model Barakah house financing SEM-Amos Islamic bank.

ARTICLE HISTORY: Received:17 August 2018 Revised:21 September 2018 Accepted:30 October 2018 Published:26 November 2018.

Contribution/ Originality:Model of house financing among public in Malaysia are Bay Bithaman Ajil (deferred payment sale), Musyarakah Mutanaqisah (diminishing partnership) and Tawarruq (direct instrument of debt creation) which are not affordable for lower income earners. A field study was performed to examine the public acceptance towards the new model of Barakah house financing among public. The results can be concluded that the new model of Barakah house financing would be accepted by the public in Malaysia. The Barakah model can be future model for home financing in Malaysia.

1. INTRODUCTION

Islamic house financing has gained its popularity since last three decades as a substitute for interest-based-debt financing. There are top three-syariah principle applied in Malaysia, which are Bai Bithaman Ajil, Musyarakah Mutanaqisah and Tawarruq. The purpose of this paper is to compare the Shariah principle applied in Islamic house financing in Malaysia namely Bai Bitahaman Ajil, Musyarakah Mutanaqisah and Tawarruq. Based on an extensive literature review, this paper aims to highlight the weakness, methods of computation and pricing, calculations and benefits of each shariah principles and its distinctive features when compared to each other.

The existence of Islamic banking in Malaysia was started on 1963 with the establishment of Tabung Haji. People start too aware with ‘halal’ and ‘haram’ transaction as the foundation of conventional home financing principle is contradict with the nature of Islamic rulings, where Gharar (uncertainty) and Riba (usury) are become the fundamental part of the conventional framework of financing. Furthermore, it has considered that the development of Islamic banks are very promising, given its activity exponentially growth in the country. This has encouraged the government to take a further improvement in the Islamic banking industry in Malaysia.

During the Malaysia’s economy crisis in 1997, many house owner felt burdened with the existing conventional loan. As with conventional, there’s no ceiling rate to maximize the fluctuate rate if the economy gone worst. Starting from that, people get more aware with product offered by the bank as it is a major investment decision that is made out of necessity. In conjunction to this, this research contributes to the constructing of new model of house financing, known as Barakah house financing which can be a guideline to the related industry institutions to provide a more comprehensive house financing model in the Malaysian market, thus facilitating a wide range of Shariah compliant house financing.

2. LITERATURE REVIEW

The Islamic part of the Islamic banking system is viewed as a standout amongst the most vital parts in separating it from conventional banking system. In this manner, for the Islamic banks to contend in the application of dual markets system, it is vital for them to keep in lined with the Shariah prerequisites that symbolize to the religious guidelines of Islam. In fact, as for the conventional banks intended to move into the Islamic banking market need to have first a Shariahboard or a Shariahcounselor in order to guarantee the conformity and minimize Shariahrisk.

Thus, this article emphasizes on the strength and weaknesses of 3 most top Shariah principles practiced for home financing in Malaysia. The top listed Shariah principles in Malaysia are Bay Bithaman Ajil (deferred payment sale), Musyarakah Mutanaqisah (diminishing partnership) and Tawarruq (direct instrument of debt creation). There are 16 Islamic Financial Institution (IFI) in Malaysia. Table 1 showed the summary of IFI in Malaysia as at March 2016.

Table-1. Summary of Islamic Home Financing in Malaysia

Islamic Financial Institution |

Name of Home Finance |

Shariah Concept |

Affin Islamic Bank Berhad |

Home Fin. -i |

MM |

Al Rajhi Banking & Investment Corporation Malaysia Bhd |

Home Fin-i |

BBA |

Alliance Islamic Bank Berhad |

i-Wish Home Fin-i |

BBA |

Am Islamic Bank Berhad |

Home Fin-i |

BBA & MM |

Asian Finance Bank Berhad |

Home Fin-I |

MM |

Bank Islam Malaysia Berhad |

Baiti Home Fin-i |

Tawarruq |

Bank Muamalat Malaysia Berhad |

Home Fin-i |

MM |

Cimb Islamic Bank Berhad |

Flexi Home Fin-i |

Tawarruq |

HSBC Amanah Malaysia Berhad |

Home Smart-i |

MM |

Hong Leong Islamic Malaysia Berhad |

Flexi Prop Fin-i |

Tawarruq |

Kuwait Finance House (Malaysia) Berhad |

MM home Fin-i |

Ijarah Muntahiah Bi Tamlik |

Maybank Islamic Berhad |

Home Equity & Maxi Home |

MM & Tawarruq |

OCBC Al Amin Bank Berhad |

Manarat Home-i |

Ijarah Muntahiah Bi Tamlik |

Public Islamic Bank Berhad |

ABBA Home Fin-i |

Bai Al Inah |

RHB Islamic Bank Berhad |

Equity Home Fin-i |

MM |

Standard Chartered Saadiq Berhad |

Saadiq My Home-i |

MM |

Source: Bank Negara Malaysia (2018 ![]() ).

).

3. METHODOLOGY

3.1. Investigating the Acceptance of Public on the New Model of Barakah House Financing

Based on survey by Azhar et al. (2017 ![]() ), Ismail et al. (2016

), Ismail et al. (2016 ![]() ) and Ghazali et al. (2015; 2017a; 2017b

) and Ghazali et al. (2015; 2017a; 2017b ![]() ) a field study was performed to examine the public acceptance towards the new model of Barakah house financing. In this case, 300 set of questionnaires were distributed in Malaysia. Respondents were chosen among the people who had house financing. The questionnaire has 5 construct, where 4 construct were independence variable comprised of 2 sections. In the first section which focused on demographic profile such as age, marital status, level of education and etc. While, in the second section of the questionnaire, comprised of the Likert scale questions with ranging from 1 to 10 of selection answer, where 1 denoted for strongly disagree and 10 for strongly agree in a continuous basis. As for the dependent variable, it became a reason of the public participating onto the new model of Barakah house financing. Table 2 highlighted the 4 hypotheses that would be tested in this research, which denoted as H1 to H4.

) a field study was performed to examine the public acceptance towards the new model of Barakah house financing. In this case, 300 set of questionnaires were distributed in Malaysia. Respondents were chosen among the people who had house financing. The questionnaire has 5 construct, where 4 construct were independence variable comprised of 2 sections. In the first section which focused on demographic profile such as age, marital status, level of education and etc. While, in the second section of the questionnaire, comprised of the Likert scale questions with ranging from 1 to 10 of selection answer, where 1 denoted for strongly disagree and 10 for strongly agree in a continuous basis. As for the dependent variable, it became a reason of the public participating onto the new model of Barakah house financing. Table 2 highlighted the 4 hypotheses that would be tested in this research, which denoted as H1 to H4.

Table-2. Research Hypotheses

| Hypothesis | |

H1 |

Knowledge among people in public of Malaysia has significantly correlated to the acceptance of the new model of Barakah house financing |

H2 |

Benefit among public has significantly correlated to the acceptance of the new model of Barakah house financing |

H3 |

Quality of product has significantly correlated to the acceptance of the new model of Barakah house financing |

H4 |

Marketing of product has significantly correlated to the acceptance of the new model of Barakah house financing |

Source: Sekaran and Bougie (2006 ![]() ).

).

The completed survey answered by the respondents then would be keyed in into SPSS version 21 and been analyzed using SEM-Amos. The research analyzed the collected data by adopting inferential statistical and correlation analyses among 5 independent variables and dependent variable.

4. RESULT AND DISCUSSION

4.1. KMO and Barlett’s Test

Kaiser-Meyer-Olkin (KMO) and Bartlett’s test were carried out to determine the adequacy of the items. The value of KMO and Bartlett’s Test for correlation between variables or items should be > 0.5. The significance of the scrutiny is 0.05. Kaiser (1974 ![]() ) stressed the value of KMO in the 0.90s as “Marvellous”, in the 0.80s as “Maritorious”, in the 0.70s as “Middling”, in the 0.60s “Mediocre”, in the 0.50 as “Miserable”. The two measures (KMO value close to 1.0 and the Bartlett’s test significance value close to 0.0) suggest that the data is appropriate to proceed with its reduction procedure. The table below presents the result of KMO and Bartlett’s test on the new model.

) stressed the value of KMO in the 0.90s as “Marvellous”, in the 0.80s as “Maritorious”, in the 0.70s as “Middling”, in the 0.60s “Mediocre”, in the 0.50 as “Miserable”. The two measures (KMO value close to 1.0 and the Bartlett’s test significance value close to 0.0) suggest that the data is appropriate to proceed with its reduction procedure. The table below presents the result of KMO and Bartlett’s test on the new model.

Table-3KMO and Bartlett's Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy. |

Bartlett's Test of Approx. Chi-Square Sphericity. |

df. |

Sig. |

0.804 |

383.079 |

6 |

0 |

source: Zainudin (2015 ![]() )

)

The Kaiser-Meyer-Olkin value in Table 3 was 0.804, which exceeded the recommended value of 0.60. This indicates that more than 80% of the variance in the measured variables is common variance. The Bartlett’s Test of Sphericity value from the data set showed statistically significant (Chi-Square with degree of freedom 6 = 383.079, p = .000). This means that there were strong relationships between the items to investigate. The Kaiser-Meyer-Olkin and Bartlett’s Test of Sphericity value suggest that the data on new model of barakah house financing in this research was suitable for factor analysis.

4.2. Communalities

Communality on new model of barakah house financing was carried out to measure the variability of each observed variable or item that could be explained by the extracted factors. According to Pallant (2007 ![]() ) a low value for communality (example, less than 0.3) is undesirable, as it could indicate that the items do not fit well with the other items in its component. Table 4 shows the communalities of the new model of barakah house financing, which consist of four items.

) a low value for communality (example, less than 0.3) is undesirable, as it could indicate that the items do not fit well with the other items in its component. Table 4 shows the communalities of the new model of barakah house financing, which consist of four items.

Table-4.Communalities

Initial |

Extraction |

|

P1 |

1 |

0.458 |

P2 |

1 |

0.88 |

P3 |

1 |

0.928 |

P4 |

1 |

0.89 |

Source: Zainudin (2015 ![]() )

)

New model of barakah house financing communalities result in Table 4 indicates that all the four items in the variable were relatively high, ranging between 0.458(P1) and 0.928(P3). This means that the items of the variable fit well with other items of the variable in their factor.

Table-5 Total Variance Explained

Initial Eigenvalues |

Extraction Sums of Squared Loadings |

|||||

Components |

Total |

% of Variance |

Cumulative % |

Total |

% of Variance |

Cumulative % |

1 |

3.156 |

78.896 |

74.896 |

3.156 |

78.896 |

78.896 |

2 |

0.634 |

15.859 |

94.755 |

|||

3 |

0.143 |

3.572 |

98.327 |

|||

4 |

0.067 |

1.673 |

100 |

|||

Source: Zainudin (2015 ![]() )

)

The output result in Table 5 shows that the Exploratory Factor Analysis for new model of barakah house financing has extracted one dimension for the construct with Eigenvalues exceeding 1.0. The table above shows the output result of the Factor Analysis for product items.

Table-6.Component Matrixa

Item |

Factor loading |

P1 |

0.677 |

P2 |

0.938 |

P3 |

0.963 |

P4 |

0.943 |

Source: Zainudin (2015 ![]() )

)

The validity of the instruments of the constructs, new model of barakah house financing was measured, and the items associated with each construct were examined. The EFA result for product in Table 6 indicates that the four items have a factor loading above the recommended value of 0.60, showing the convergent and discriminant validity of the scales and there are no deleted items, meaning that the construct is suitable for further analysis. According to Hair et al. (2010 ![]() ) the factor loading of +/- 0.30 meet the minimal standard while loading above +/- 0.50 were practically significant.

) the factor loading of +/- 0.30 meet the minimal standard while loading above +/- 0.50 were practically significant.

4.3. Reliability Analysis

A 100 of respondents would be chosen to conduct a pilot test in order to check the reliability of the developed questionnaires before conducting the real field study. Table 7 below depicted the reliability analysis result of the pilot test.

Table-7 Reliability Coefficient (Cronbach’s Alpha)

Construct |

Items |

Cronbach’s Alpha (above 0.7) |

Cronbach’s Alpha based on Standardized Items |

Number of Items |

Internal Reliability |

Product |

P1 |

0.89 |

0.892 |

4 |

Excellent |

P2 |

|||||

P3 |

|||||

P4 |

|||||

Knowledge |

K1 |

0.911 |

0.913 |

6 |

Excellent |

K2 |

|||||

K3 |

|||||

K4 |

|||||

K5 |

|||||

K6 |

|||||

Quality |

Q1 |

0.966 |

0.968 |

6 |

Excellent |

Q2 |

|||||

Q3 |

|||||

Q4 |

|||||

Q5 |

|||||

Q6 |

|||||

Benefit |

B1 |

0.967 |

0.969 |

4 |

Excellent |

B2 |

|||||

B3 |

|||||

B4 |

|||||

Marketing |

M1 |

0.921 |

0.923 |

6 |

Excellent |

M2 |

|||||

M3 |

|||||

M4 |

|||||

M5 |

|||||

M6 |

Source: Zainudin (2015 ![]() )

)

Table 7 presented the results obtained from the reliability test using Cronbach’s alpha measurement, where all the Cronbach’s alpha values of the constructs have recorded between 0.890 to 0.966, which more than 0.6 considered as excellent (Sekaran and Bougie, 2006 ![]() ).

).

4.4. Measurement Model

In the measurement model, it can determine the causal association of measuring items with the given latent constructs, which become first stage in conducting SEM. The measurement model of a construct allows the researcher to evaluate how well the observed variable is combined to measure the underlying hypothesized contrasts through the assessment of model fit (Bakar and Afthanorhan, 2016 ![]() ). On the other hand, the Confirmatory Factor Analysis (CFA) has been used to verify the measurement model of the underlying latent construct.

). On the other hand, the Confirmatory Factor Analysis (CFA) has been used to verify the measurement model of the underlying latent construct.

This measurement model was analyzed using four proposed factors or construct which comprises of finance, infrastructures, training, and performance of SMEs after EFA analysis has been conducted, thirty-one items representing four factors that are subjected to CFA analysis. During the EFA, no item was deleted because the entire factor loading of the items achieved the recommended value of > 0.06. Below is the CFA, measurement model.

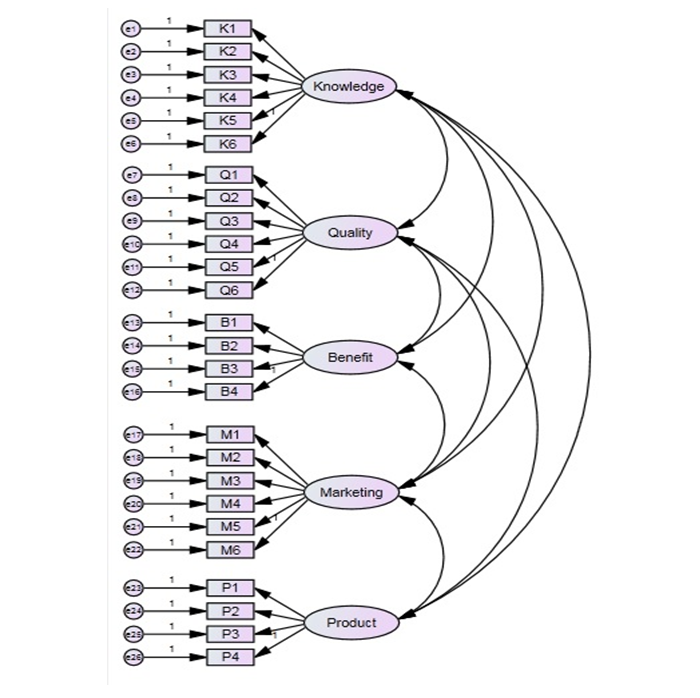

Figure-1. The CFA for Measurement Model Combining all Latent Constructs Simultaneously

Source: Zainudin (2015 ![]() )

)

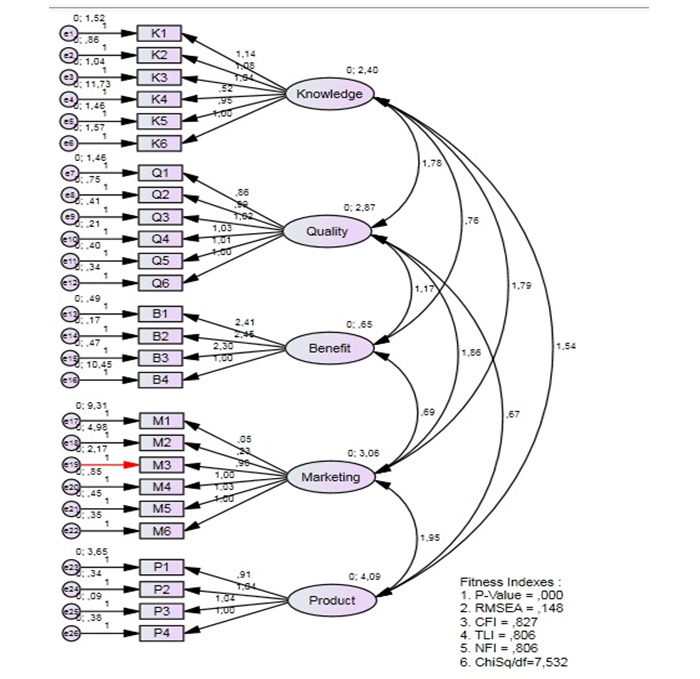

The outcomes from CFA provide a fitness indexes and factor loading each of the item together as well as the value of R2 as presented by Figure 2. Through the process, the correlations between constructs are computed simultaneously. If one has too many constructs, and thus cannot be pool them together into one measurement model, he can only pool the constructs into two separate measurement models (Zainudin, 2015 ![]() ) But in the case of this research the constructs are not much thereby it can be pool in one measurement model below.

) But in the case of this research the constructs are not much thereby it can be pool in one measurement model below.

Figure-2. The Factor Loading for all Items of the Respective Constructs (The CFA for Measurement Model)

Source: Zainudin (2015 ![]() )

)

Table-8.Items Description and Items Deleted

Item Label |

Factor Loading |

K1 |

1.14 |

K2 |

1.08 |

K3 |

1.84 |

K4 |

0.52 |

K5 |

0.95 |

K6 |

1 |

Q1 |

0.86 |

Q2 |

0.99 |

Q3 |

1.62 |

Q4 |

1.03 |

Q5 |

1.01 |

Q6 |

1 |

B1 |

2.41 |

B2 |

2.46 |

B3 |

2.3 |

B4 |

1 |

M1 |

0.05 |

M2 |

0.23 |

M3 |

0.96 |

M4 |

1 |

M5 |

1.03 |

M6 |

1 |

P1 |

0.91 |

P2 |

1.64 |

P3 |

1.04 |

P4 |

1 |

Note: Items was deleted.

Table-9. The Fitness Indexes for Measurement Model

Name of Category |

Name of Index |

Index Value |

Comments |

Absolute Fit |

RMSEA |

0.148 |

The Required Level is not Achieved |

Incremental Fit |

CFI |

0.827 |

The Required Level is not Achieved |

TLI |

0.806 |

The Required Level is not Achieved |

|

NFI |

0.806 |

The Required Level is not Achieved |

|

Parsimonious Fit |

Chisq/df |

7.532 |

The Required Level is not Achieved |

Source: Zainudin (2015 ![]() )

)

The CFA result confirms that the model cannot proceed with further analysis. Based on results in Figure 2 and Table 29, it has indicated that the RMSEA = 0.148, CFI = 0.827, TLI = 0.806, NFI = 0.806, and Chisq/df = 7.532. The results indicated that all the fitness indexes for the pooled constructs do not achieve the required level, and the model has not adequately appropriate for the data. Basically, the outcome from the assessment of the measurement model has not provides a solid evidence of unidimensionality, convergent validity, and reliability. Therefore, to achieve the fitness indexes of the measurement model, a modification have to be carry out in the model where any factor loading with less than 0.60 will be deleted in addition to in line with the research objective of a latent construct that also make the measurement model not to achieve its fitness indexes even though the factor loading is above 0.60 will be correlated or deleted if it won’t affect the model and make a new construct. The new modification model was presented below.

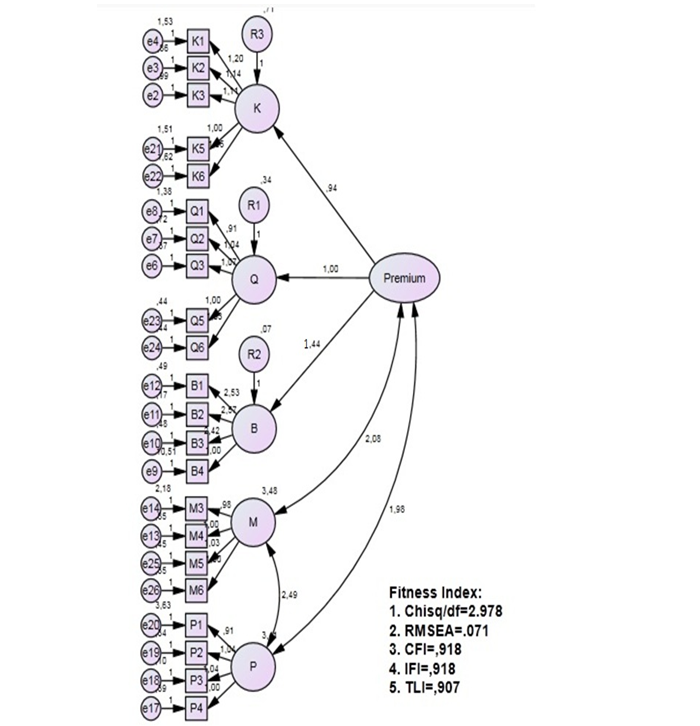

Figure-3. The New Factor Loading after Modification has taken place on Items (The CFA for Measurement Model)

Source: Zainudin (2015 ![]() ).

).

Table-10Items Description and Items Deleted

Item Label |

Factor Loading |

K1 |

1.2 |

K2 |

1.14 |

K3 |

1.14 |

K5 |

1 |

K6 |

1.06 |

Q1 |

0.91 |

Q2 |

1.04 |

Q3 |

1.07 |

Q5 |

1 |

Q6 |

1.05 |

B1 |

2.53 |

B2 |

2.57 |

B3 |

2.42 |

B4 |

1 |

M3 |

0.98 |

M4 |

1 |

M5 |

1.03 |

M6 |

1 |

P1 |

0.91 |

P2 |

1.04 |

P3 |

1.04 |

P4 |

1 |

Pr1 |

0.94 |

Pr2 |

1 |

Pr3 |

1.44 |

Note: All items have met the recommended value

Table-11The Fitness Indexes for New Measurement Model

Name of Category |

Name of Index |

Index Value |

Comments |

Absolute Fit |

RMSEA |

0.071 |

The Required Level is Achieved |

Incremental Fit |

CFI |

0.918 |

The Required Level is Achieved |

TLI |

0.907 |

The Required Level is Achieved |

|

NFI |

0.918 |

The Required Level is Achieved |

|

Parsimonious Fit |

Chisq/df |

2.978 |

The Required Level is Achieved |

Note: The fitness index has improved after the modification has taken place in the measurement model

The outcome of the CFA confirms that the model can proceed with further analysis. Based on the Figure 3 and Table 11, the outcomes of the CFA indicated that the RMSEA = 0.071. CFI = 0.918, TLI = 0.907, NFI = 0.918, and Chisq/df = 2.978. The fitness indexes, as presented in the Table 11, provides that the measurement model signifies a satisfactory fit to the data and the result of all the fit indexes yielded adequate fit. Basically, the result of the assessment of the measurement model showed solid evidence of unidimensionality, convergent validity, and reliability. Certainly, the model has enough measurement properties and hence is able to proceed with further analysis.

Table-12. The CFA Results for the Measurement Model for each Construct (After Modification)

Construct |

Item |

Factor Loading |

Cronbach’s Alpha |

C.R. |

AVE |

(Above 0.70) |

(Above 0.60) |

(Above 0.50) |

|||

Knowledge |

K1 |

1.2 |

0.911 |

0.913 |

0.593 |

K2 |

1.14 |

||||

K3 |

1.14 |

||||

K5 |

1 |

||||

K6 |

1.06 |

||||

Quality |

Q1 |

0.91 |

0.966 |

0.968 |

0.594 |

Q2 |

1.04 |

||||

Q3 |

1.07 |

||||

Q5 |

1 |

||||

Q6 |

1.05 |

||||

Benefit |

B1 |

2.53 |

0.967 |

0.969 |

0.601 |

B2 |

2.57 |

||||

B3 |

2.42 |

||||

B4 |

1 |

||||

Marketing |

M3 |

0.98 |

0.921 |

0.923 |

0.584 |

M4 |

1 |

||||

M5 |

1.03 |

||||

M6 |

1 |

||||

Product |

P1 |

0.91 |

0.89 |

0.892 |

0.588 |

P2 |

1.04 |

||||

P3 |

1.04 |

||||

P4 |

1 |

||||

Premium |

Pr1 |

0.94 |

0.882 |

0.89 |

0.59 |

Pr2 |

1 |

||||

Pr3 |

1.44 |

Source: Zainudin (2015 ![]() )

)

From Table 12 the model has adequate measurement properties for every factor model according the values of Cronbach’s Alpha, Composite Reliability, and Average Variance Extracted. Thus, with the above result, the model was adequately fit for further analysis. And the missing items are deleted as a result of low factor loading and adding a new construct.

Table-13 The Discriminant Validity Index Summary

Construct |

Knowledge |

Quality |

Benefit |

Marketing |

Product |

Premium |

Knowledge |

0.77 |

|||||

Quality |

0.245 |

0.771 |

||||

Benefit |

0.163 |

0.357 |

0.775 |

|||

Marketing |

0.078 |

0.364 |

0.443 |

0.777 |

||

Product |

0.181 |

0.382 |

0.362 |

0.385 |

0.781 |

|

Premium |

0.09 |

0.433 |

0.351 |

0.363 |

0.472 |

0.783 |

Source: Zainudin (2015 ![]() )

)

From Table 13 the diagonal value (in bold) is the Square root of AVE while other value is the correlation between the respective constructs. The discriminant validity of all constructs are achieved when the diagonal value (in bold) is higher than the values in its row and column. With this, it is concluded that the discriminant validity for all the six constructs is achieved.

5. CONCLUSION

Based on the measurement model, it can be concluded that the new model of Barakah house financing would be accepted by the public in Malaysia. Besides the facilities of comprehensive benefits, the model has also catered for all income level. Hence, this public acceptance towards the model also bring towards awareness by the public of importance having a protection for the house financing. Therefore, it is believed that the new model would be able to facilitate every people in Malaysia for an appropriate house financing.

| Funding: This study received no specific financial support. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: All authors contributed equally to the conception and design of the study. |

REFERENCES

Azhar, N.N.Z.B.A., P.L.B. Ghazali, M.B. Mamat, Y.B. Abdullah, S.B. Mahmud, S.B. Lambak and A.Z.B.A. Latif, 2017. Acceptance of integrated modification model of auto Takaful Insurance in Malaysia. Far East Journal of Mathematical Sciences, 101(8): 1771-1784. Available at: https://doi.org/10.17654/ms101081771.

Bakar, A.A. and A. Afthanorhan, 2016. Confirmatory factor analysis on family communication patterns measurement. Procedia-Social and Behavioral Sciences, 219: 33-40. Available at: https://doi.org/10.1016/j.sbspro.2016.04.029.

Bank Negara Malaysia, 2018. Centrel Bank of Malaysia. Available from http://www.bnm.gov.my/ .

Ghazali, P.L., A.N. Mazlina, M. Izah, M. Maslina, W. Zulqurnaim and M. Mustafa, 2015. Optimization of integration model in family Takaful. Applied Mathematical Sciences, 9(39): 1899-1909. Available at: https://doi.org/10.12988/ams.2015.411930. Ghazali, P.L.B., M. Mamat, L.B. Omar, N.H.M. Foziah, D.A. Guci, Y.B. Abdullah and N.E.S.B. Sazali, 2017a. Medical integration model of family Takaful for Blue collar. Far East Journal of Mathematical Sciences, 101(6): 1197-1205. Available at: https://doi.org/10.17654/ms101061197. Ghazali, P.L.B., L. Omar, M.S. Abdullah, H.C.A. Hamid, S.A.S. Jaffar, S. Yusof, N.I. Alias, D.A. Gucci, N.H.M. Foziah and A.Z.A. Latif, 2017b. Clinical work: Correlations of disability children between private classes, parenting advice and food supplements for rehabilitation. World Applied Sciences Journal, 35(4): 574-579.

Hair, J.F., W.C. Black, B.J. Babin and R.E. Anderson, 2010. Multivariate data analysis, a global perspective. 7 Edn.: Pearson. pp: 816.

Ismail, S.A., P.L. Ghazali, N.Z. Baharazi, N.A. Amran, F. Salleh, L. Omar, S. Jaafar, S. Arni and M. Mamat, 2016. Application of integration model for recovery fund in Takaful education plan. Far East Journal of Mathematical Sciences, 100(2): 301-313. Available at: https://doi.org/10.17654/ms100020301.

Kaiser, H.F., 1974. An index of factorial simplicity. Psychometrika, 39(1): 31-36. Available at: https://doi.org/10.1007/bf02291575.

Pallant, J., 2007. Spss survival manual: A step-by-step guide to data analysis using spss. Nova Lorque: McGraw Hill.

Sekaran, U. and R. Bougie, 2006. Research methods for business: A skill building approach. John Wiley & Sons.

Zainudin, A., 2015. Sem made simple. Kuala Lumpur: MPWS Rich Publication.