THE AWARENESS AND PRACTICES OF ISLAMIC VALUES IN PERFORMANCE MEASUREMENT SYSTEM (PMS): THE CASE OF A MALAYSIAN SMALL AND MEDIUM ENTERPRISE (SME)

1,2,3,4,5Department of Accountancy, Faculty of Economics and Management Sciences, Universiti Sultan Zainal Abidin,21300 Kuala Nerus, Terengganu, Malaysia

ABSTRACT

We explore the awareness and practices of Islamic values in the setting of a Malaysian Small and Medium Enterprise (SME), and how the values have been treated by the Performance Measurement System (PMS). In particular, we are interested in whether the Islamic values existed or were practised by the employees as well as adopted by the management of the SME in measuring the performance of their employees. Furthermore, the information on the importance and possible effects of the Islamic values have been sought after to see whether the values could improve the PMS and eventually the whole organisation. We present evidence from fieldwork conducted in the workplace of one SME in Terengganu, Malaysia, undertaken through participant-observation, casual conversations and interviews with four employees. Our findings suggest that Islamic values do exist and are widely practised, and at the same time, informally adopted by the management to a certain extent in measuring their employees’ performance. The management also reveals that there is a high hope in the future to see the practices of Islamic values improved among the employees, raising the possibility that it could eventually be officially adopted in their PMS.

Keywords:Performance measurement System (PMS) Islamic values Small and medium enterprise (SME) Performance measurement Employee performance Employee behaviour.

ARTICLE HISTORY: Received:7 August 2018 Revised:10 September 2018 Accepted:2 October 2018 Published:14 November 2018.

Contribution/ Originality:This study is one of the very few studies which have investigated the treatment of Islamic values by the Performance Measurement System (PMS) of a Small and Medium Enterprise (SME) in measuring the performance of their employees. The findings suggest that Islamic values are widely practised and informally adopted in the PMS of the SME.

1. INTRODUCTION

Established as one of the most important issues in business, management and accounting academic literature, many concepts, frameworks and model of the Performance Measurement System (PMS), have been researched, discussed, introduced and developed. External and internal environments in which businesses operate change and develop require countless improvements in many organisational techniques and approaches including PMS. One of the developments in PMS is the use of latest or new elements in measuring individual employee, as well as the whole, performance in an organisation. Islamic or religious value commonly known concepts in Islamic management literature, could naturally be incorporated as part of many elements discussed in the PMS literature in order to improve the measurement system as well as the overall business organisation.

This study uses a case study methodology; engage with four respondents through a semi-structured interview in one SME in Terengganu, a Muslim Malay majority state in Malaysia. Explore and gather valuable information related to the current practices in Islamic values and PMS within the business organisation. Guided with literature-based developed questionnaires, the study manages to get main evidence which translated into good findings, which suggest that Islamic values are widely practised by the employees in the SME. However, most of the respondents (except the manager/owner) are not very sure of how the Islamic values have been treated or linked with the formal reward system or current performance measurement system of the SME. At the same time, the manager/owner of the SME confidently stated that he is fully aware on the use of Islamic values but rather treated the elements in such an informal way in measuring his employees. Perhaps with more information and preparation in future, the manager places high hope that the organisation manages to improve their PMS by formally measuring the Islamic values and eventually manages to exploit or translate these positive values for the betterment of the SME overall performance.

2. REVIEW OF LITERATURE

2.1. The Importance of PMS

Regarded as one of the crucial elements for improving organisational overall performance by Epstein (2004 ![]() ) several previous studies have also argued that a performance measurement system (PMS) can play a critical role in observing the overall business functions, guiding ways to achieve organisational objectives as well as identifying any improvement required by an organisation (Najmi and Kehoe, 2001

) several previous studies have also argued that a performance measurement system (PMS) can play a critical role in observing the overall business functions, guiding ways to achieve organisational objectives as well as identifying any improvement required by an organisation (Najmi and Kehoe, 2001 ![]() ; Franco-Santos et al., 2007

; Franco-Santos et al., 2007 ![]() ). Meanwhile, looking from the decision making perspectives, Rejc and Slapnicar (2004

). Meanwhile, looking from the decision making perspectives, Rejc and Slapnicar (2004 ![]() ) have insisted that PMS could help an organisation in making a better decision, thus increasing the chances of improving the overall performance of the business organisation.

) have insisted that PMS could help an organisation in making a better decision, thus increasing the chances of improving the overall performance of the business organisation.

The importance of PMS could be seen from various previous research as Taticchi et al. (2010 ![]() ) in their study, listed 25 and 18 models and/or frameworks introduced respectively for large firms, and for small and medium enterprise (SMEs). This development shows how the importance of PMS as academics continue to measure and manage business performance in the best possible way in order to keep pace with modern, vibrant and ever-changing business environment. Specifically looking at SMEs, Garengo and Bernardi (2007

) in their study, listed 25 and 18 models and/or frameworks introduced respectively for large firms, and for small and medium enterprise (SMEs). This development shows how the importance of PMS as academics continue to measure and manage business performance in the best possible way in order to keep pace with modern, vibrant and ever-changing business environment. Specifically looking at SMEs, Garengo and Bernardi (2007 ![]() ) believe that PMS could promote the competitiveness of SMEs when treated as a key managerial system in supporting growth in that particular size of the organisation.

) believe that PMS could promote the competitiveness of SMEs when treated as a key managerial system in supporting growth in that particular size of the organisation.

2.2. The Important of Islamic Values in Business Activities and PMS

Islam is a complete and comprehensive religion (Quran, 5:3) and thus Islam provides comprehensive guidelines both for spiritual matters as well as worldly matters including the conduct of business (Foziaa et al., 2016 ![]() ). There are various characteristics of practices of Islamic values by entrepreneurs revealed by Foziaa et al. (2016

). There are various characteristics of practices of Islamic values by entrepreneurs revealed by Foziaa et al. (2016 ![]() ) in their study such as taqwā (faith), tawakkul (dependence on Allah), which relate directly with Islamic concepts/pillars. Meanwhile, there are also Islamic values explained in generic or layman’s terms such as “efficient and proper use of resources, the use of permissible sources of production and the production of permissible products, sincerity in efforts, trustworthiness in all dealings, concern for societal welfare and the environment, fairness and transparency in all activities, pursuance of knowledge, taking pride in work/labour, and consultation with stakeholders before decision making.” Foziaa et al. (2016

) in their study such as taqwā (faith), tawakkul (dependence on Allah), which relate directly with Islamic concepts/pillars. Meanwhile, there are also Islamic values explained in generic or layman’s terms such as “efficient and proper use of resources, the use of permissible sources of production and the production of permissible products, sincerity in efforts, trustworthiness in all dealings, concern for societal welfare and the environment, fairness and transparency in all activities, pursuance of knowledge, taking pride in work/labour, and consultation with stakeholders before decision making.” Foziaa et al. (2016 ![]() ).

).

In another comprehensive view of Islamic values in the business organisation, a study by Rafiki and Wahab (2014 ![]() ) could be considered a significant piece of information whereby they reviewed all related literature on Islamic values from various sources of study. The study highlights many practices of Islamic activities in the organisation whether they are specifically cited in Al-Qur’an and Hadith, or are based on the guidelines encompassing various shariah rules, muamalat and ethical values (akhlaq Islamiyyah). Listed are a few instances such as “Islamic finance, halal certification, Islamic motivation in work, Islamic education, Islamic business training, Islamic networking (jemaah), payment of zakat, honesty, good intention (niyyah), dedication, creativity, optimism, commitment, tenacity and hardworking” (Rafiki and Wahab, 2014

) could be considered a significant piece of information whereby they reviewed all related literature on Islamic values from various sources of study. The study highlights many practices of Islamic activities in the organisation whether they are specifically cited in Al-Qur’an and Hadith, or are based on the guidelines encompassing various shariah rules, muamalat and ethical values (akhlaq Islamiyyah). Listed are a few instances such as “Islamic finance, halal certification, Islamic motivation in work, Islamic education, Islamic business training, Islamic networking (jemaah), payment of zakat, honesty, good intention (niyyah), dedication, creativity, optimism, commitment, tenacity and hardworking” (Rafiki and Wahab, 2014 ![]() ).

).

Meanwhile, organisational resources such as “people, money, the physical plant, and technology” need be used and managed in the best possible way in order to help an organisation achieve efficiency in their performance (Gomez-Mejia and Balkin, 2012 ![]() ). However, managing people or human resources could be one of many critical tasks for an organisation to stay competitive in a business organisation. According to Katz (1964

). However, managing people or human resources could be one of many critical tasks for an organisation to stay competitive in a business organisation. According to Katz (1964 ![]() ) in his study way back in 1964, different types of approaches are needed to identify sources of variances in employee behaviours and their motivations in order to manage them. This is due to the reason that different types of employees differ in the way they perform their duties in an organisation.

) in his study way back in 1964, different types of approaches are needed to identify sources of variances in employee behaviours and their motivations in order to manage them. This is due to the reason that different types of employees differ in the way they perform their duties in an organisation.

Islamic values are closely related to people, human resources or employee behaviours, and thus the values seem very critical to be explored to gain more information on how to manage an organisation in more effective and efficient ways. One study conducted by Rego and Pina e Cunha (2008 ![]() ) showed that the spiritual values in the workplace have contributed to the effectiveness of an organisation through employees commitment. Viewing from PMS perspective, these spiritual (Islamic) values could be considered included as part of the formal way of measuring employee’s performance as it is proven from a few previous studies (Epstein, 2004

) showed that the spiritual values in the workplace have contributed to the effectiveness of an organisation through employees commitment. Viewing from PMS perspective, these spiritual (Islamic) values could be considered included as part of the formal way of measuring employee’s performance as it is proven from a few previous studies (Epstein, 2004 ![]() ; Crook et al., 2011; Franco-Santos et al., 2012

; Crook et al., 2011; Franco-Santos et al., 2012 ![]() ) the betterment or improvement of PMS could eventually increase organisational overall performance especially in SMEs.

) the betterment or improvement of PMS could eventually increase organisational overall performance especially in SMEs.

Performance measurement in Islam is based on the concept of justice (‘adl). Employers are urged to treat their employees equally regardless of their status or position in the organisation. Islam prohibits the idea of favouritism and discrimination. Islam makes it compulsory to be just in daily life as Allah says in the Quran:

“Thus when they fulfil their term appointed, either take them back on equitable terms or part with them on equitable terms; and take for witness two persons from among you, endued with justice, and established the evidence for the sake of Allah. Such is the admonition given to him who believes in Allah and the Last Day. And for those who fear Allah, He (ever) prepares a way out (Quran, 65:2).

“O you who believe! Stand out firmly for Allah and be just witnesses and let not the enmity and hatred of others make you avoid justice. Be just: that is nearer to piety, and fear Allah. Verily, Allah is well acquainted with what you do.” (Quran, 5:8).

“Be equitable. Verily, Allah loves those who are equitable.” (Quran, 49:9).

The above Quran verses show that there is no doubt that Islam has put high concern on the performance measure through the concept of justice (‘adl). A study by Muhammad (2002 ![]() ) showed that high concern on spiritual (Islamic) aspects have influenced manager/supervisor to evaluate their subordinates more accurate, uphold justice as well as be transparent while measuring employees’ overall performance. Echoing the above argument, Aziz (2015

) showed that high concern on spiritual (Islamic) aspects have influenced manager/supervisor to evaluate their subordinates more accurate, uphold justice as well as be transparent while measuring employees’ overall performance. Echoing the above argument, Aziz (2015 ![]() ) in his book specifically and thoroughly explored performance appraisal from Islamic perspectives and shows the importance Islamic values compared with the current way of measuring employee’s performance.

) in his book specifically and thoroughly explored performance appraisal from Islamic perspectives and shows the importance Islamic values compared with the current way of measuring employee’s performance.

3. RESEARCH METHODOLOGY

3.1. Qualitative Single Case Study Method

This study approaches one chosen SME in Terengganu, using several procedures and sources of information to answer very specific queries of ‘how’ and ‘why, therefore it seems applicable to just use a single case study line of inquiry (Creswell, 2007 ![]() ; Yin, 2009). There is a number of other supporting evidence on why case study is very much suited for this study are; the limited control of the researcher over the object of study; as well as the contemporary phenomenon of the real-life context as the focus of the study (Yin, 2009

; Yin, 2009). There is a number of other supporting evidence on why case study is very much suited for this study are; the limited control of the researcher over the object of study; as well as the contemporary phenomenon of the real-life context as the focus of the study (Yin, 2009 ![]() ).

).

On the same note, Azofra et al. (2003 ![]() ) have conducted an earlier study of PMS, choosing the same approach of a single case study to provide insight into ‘how’ and ‘why’ certain performance indicators were used to discover any interaction of the indicators and the various elements of the working environment. Meanwhile, Dawson (2010

) have conducted an earlier study of PMS, choosing the same approach of a single case study to provide insight into ‘how’ and ‘why’ certain performance indicators were used to discover any interaction of the indicators and the various elements of the working environment. Meanwhile, Dawson (2010 ![]() ) believed a single case study allows an in-depth analysis of that particular case through speaking to several members of the organisation. A single case study is proven as a good or at least an acceptable method for investigating performance measurement systems in an organisation, as shown in several previous studies before (Azofra et al., 2003

) believed a single case study allows an in-depth analysis of that particular case through speaking to several members of the organisation. A single case study is proven as a good or at least an acceptable method for investigating performance measurement systems in an organisation, as shown in several previous studies before (Azofra et al., 2003 ![]() ; Fried, 2010

; Fried, 2010 ![]() ; Jochem et al., 2010

; Jochem et al., 2010 ![]() ).

).

Characteristics of most data gathered in this study involves individual perceptions, opinions, and beliefs, are all in agreement with this single case study type of research approach. Meanwhile, descriptive information on the situational setting of the respondents’ organisation gathered through observations, informal conversation, and documents reviewed added more in terms of the suitability of the case study approach with this study. The case study approach also has its strength in research as it uses extensive data collection via multiple sources of information, such as interviews, observations, archival records and access to related documents (Denscombe, 2010 ![]() ) and most of these have been utilised in this study. In-depth information on Islamic values and PMS are gathered from various sources such as qualitative data from the filled-up questionnaire used in interviews, document reviews, as well as observation notes while in the fieldwork setting.

) and most of these have been utilised in this study. In-depth information on Islamic values and PMS are gathered from various sources such as qualitative data from the filled-up questionnaire used in interviews, document reviews, as well as observation notes while in the fieldwork setting.

3.2. Fieldwork of the Study

A strong relationship between fieldwork and case study is exposed in the literature as both are “used to refer to studies of accounting in its practical setting” (Ryan et al., 2002 ![]() ). Meanwhile, in management accounting, (as where PMS could be considered as part of it) intensive fieldwork and case study seemed to be more popular compared to the survey method. This is due to an argument that the latter approach tends to give a very superficial view of practice which, to some extent, could lead to misunderstanding about the use of management accounting techniques (Ryan et al., 2002

). Meanwhile, in management accounting, (as where PMS could be considered as part of it) intensive fieldwork and case study seemed to be more popular compared to the survey method. This is due to an argument that the latter approach tends to give a very superficial view of practice which, to some extent, could lead to misunderstanding about the use of management accounting techniques (Ryan et al., 2002 ![]() ).

).

Questionnaires and semi-structured interviews are the two main components to explain how fieldwork activities have been conducted by this study to gather primary data from respondents. Developed as a guide for the semi-structured interviews, questionnaires used by this study have fulfilled the three main elements listed by Denscombe (2010 ![]() ) to be qualified as research questionnaires. Firstly, the questionnaire is designed to collect and subsequently analyse the data, instead of to change respondents&rs quo; attitudes or give information to them, such as marketing a product, in which case it must consist of a written list of questions (occasionally pictures could be used), and finally the research questionnaire should gather information by asking respondents directly on the points of interest (Denscombe, 2010

) to be qualified as research questionnaires. Firstly, the questionnaire is designed to collect and subsequently analyse the data, instead of to change respondents&rs quo; attitudes or give information to them, such as marketing a product, in which case it must consist of a written list of questions (occasionally pictures could be used), and finally the research questionnaire should gather information by asking respondents directly on the points of interest (Denscombe, 2010 ![]() ).

).

Questionnaire of this study was prepared based on the relevant literature from PMS and Islamic values research area. Data to be gathered by the questionnaire were a plan under six sections with different themes for each of the sections. First and second sections of the questionnaires, typically just look for background information on both organisation and individual respondent. The third section seeks information on the current practices of PMS in the organisation. The fourth section focuses on the awareness and practices of Islamic values in the organisation. Meanwhile, the fifth section is on the treatment of Islamic values in PMS and final section attempts to gather any recommendation on the treatment of Islamic values in PMS in future for the organisation.

A semi-structured interview is the second component in fieldwork activities of this study. The interviews were planned to be conducted under the guidance of the questionnaire which was developed according to specific themes. Semi-structured interview in this study allows questions to be adapted to either employee or supervisor/manager, and in fact, interview method was argued favourably by Dawson (2010 ![]() ) as it could provide a richer data set to the study. Several important issues need to be concerned of while using the interview as a data collection (Gillham, 2005

) as it could provide a richer data set to the study. Several important issues need to be concerned of while using the interview as a data collection (Gillham, 2005 ![]() ; Denscombe, 2010

; Denscombe, 2010 ![]() ) to make sure the method obviously differs between ‘surveyed questionnaire’ and purely ‘conversation’.

) to make sure the method obviously differs between ‘surveyed questionnaire’ and purely ‘conversation’.

In order to make sure that the ethical elements of the data collection process were taken and followed correctly, the proper steps and procedures were planned and undertaken while conducting the interviews. At the same time, the limited time available for the data collection process could also have been a concern, thus the balance between these two factors (time and procedure) needs to be managed practically and wisely. Respondents value highly if we manage to stick with within the expected time we have informed them before conducting the interviews. On another issue, it is utmost important we should call off the interview session at any time requested by respondents without them having to produce any specific reason. This is to show how we impose a highly voluntarily concept in conducting research.

Generally, the flow of fieldwork activities taken by this study is firstly getting respondents’ consent to take part in the interviews. Then, they were clearly been briefed that all information gathered for this study will strictly be treated as private and confidential and used just for this study. Further, the interviews were conducted according to the agenda set in the questionnaire, to assure consistency across all respondents, as well as to successfully finish the interview approximately within the timeframe outlined to the respondents at the start of the interview session.

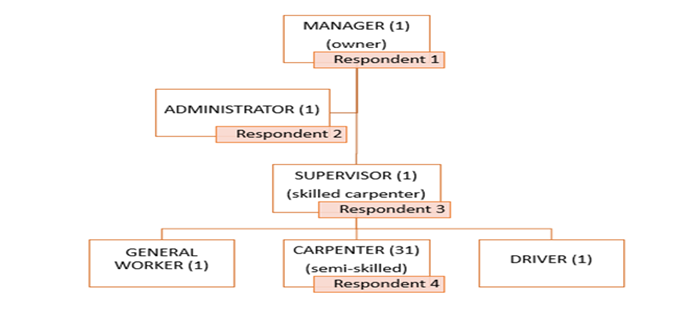

Respondents from the SME chosen to be interviewed included manager who acted as the assessor, as well as employees as the assessed. Information related to performance measurement is comprehensively gathered when both sides of the measurement system (assessor and assessed) are involved. Meanwhile, the decision to have several employees (three in this study) is used as a way of seeking consistent information from respondents regarding the PMS in the organisation (Figure 1).

Figure-1. Organisational chart

Source: Based on the interviews in the current research.

During the fieldwork, besides having a semi-structured interview, data have also been collected through observations and casual conversations with respondents as well as other employees in the organisation. Observation that could possibly be thought of as a simple and direct way of doing research, are instead highly rated by Creswell (2007 ![]() ) who said that it is difficult for the novice researcher. He believes it is also one of the reasons why the interviewing method is used more often that observation in qualitative research. Denscombe (2010

) who said that it is difficult for the novice researcher. He believes it is also one of the reasons why the interviewing method is used more often that observation in qualitative research. Denscombe (2010 ![]() ) echoes the positive argument on observation and states that observing people, events, or activities is the best to explain what actually happens in a research setting. This study has gathered some information through observation by preparing observation notes while visiting the organisation. Photos and several notices have been captured and included as part of the evidence from the observations and could contribute to the main source of information gathered through semi-structured interviews. Lastly, several types of written documents have been reviewed by this study such as employee attendance sheet, job contract, appointment letter, notice and paperwork.

) echoes the positive argument on observation and states that observing people, events, or activities is the best to explain what actually happens in a research setting. This study has gathered some information through observation by preparing observation notes while visiting the organisation. Photos and several notices have been captured and included as part of the evidence from the observations and could contribute to the main source of information gathered through semi-structured interviews. Lastly, several types of written documents have been reviewed by this study such as employee attendance sheet, job contract, appointment letter, notice and paperwork.

4. RESULTS AND DISCUSSION

4.1. Background of the Business Organisation

Started as wooden frame maker (for door and window), this business has developed sizeably with just a few employees back in 1991 to 35 full-time permanent employees currently. The owner has also proudly admitted they are the biggest furniture company in the local area of one of the districts in Terengganu, not only by hiring a big number of employees but also by recording revenues or turnover between 50,000 to 200,000 monthly. Other local competitors in the same furniture maker and joinery based business, normally manage to hire just seven to eight employees generally. In term of the level of competition, there are more or less ten main local competitors who actively operate in the local area, not including the small size businesses which operate from their own residential house. The owner believes that customers value fast delivery as a key factor when looking for the product and services, besides a few other factors such as quality, design and cost. Thus a big number of employees has been adopted as a tool for this company to compete where they try to satisfy their customers by offering competitive price together with fast delivery as promised.

4.2. Current Practices of PMS

One of the biggest challenges for this company while having a big number of employees is how to make them happy and satisfied with their job. A very good PMS is needed to be developed to make sure the company effectively manages their staff and makes every single of them feel motivated to work and enjoy their life while working for the organisation. This study has ascertained several key performance indicators (KPIs) from the questionnaire such as time, output (quantity), quality, financial, customer, and human-related factors to look into the company’s current indicators to measure employee performance. However, we find that only three KPIs which are time, output as well as quality, were agreed by all four respondents as current KPIs in this company, besides human-related factors which was only mentioned by the manager (the owner) of the company. In more specific information, time attendance, producing output within an agreed period (productivity), quality of work (product and installation services), commission for bringing a new project (sales), employee-customer relationships, and finally trustworthy (integrity), are among the performance measures quoted by the manager. On another note, the company has a good record of never dismissing employees after more than 25 years in business. However one of the respondents has rated that the owner was too lenient before, one who practises loose assessment and hesitant to even punish so-called problematic employees in the organisation. Currently, some notable changes have been done and implemented in seeking the betterment in managing and measuring employees’ performance.

Table-1. Islamic values mentioned by respondents

INTERVIEW |

OBSERVATION |

DOCUMENT |

|

Safety |

/ |

/ |

/ |

Cleanliness |

/ |

/ |

/ |

Ethics |

/ |

||

Religious class/lecture |

/ |

/ |

|

Welfare |

/ |

||

Cooperation |

/ |

||

Helping behaviour |

/ |

||

Discipline |

/ |

/ |

|

Volunteerism |

/ |

||

Hardworking |

/ |

||

Good manners |

/ |

||

Trustworthiness |

/ |

Source: Data collected from the current research.

4.3. Awareness and Practices of Islamic Values in the Organisation

Consistent with Foziaa et al. (2016 ![]() ) and Rafiki and Wahab (2014

) and Rafiki and Wahab (2014 ![]() ) some Islamic values have been clearly mentioned being practised in the organisation by all respondents, as well as a few values have been noted from our observation while conducting interviews.

) some Islamic values have been clearly mentioned being practised in the organisation by all respondents, as well as a few values have been noted from our observation while conducting interviews.

List of Islamic values in Table 1 is consistent with a study done by both Foziaa et al. (2016 ![]() ) and Rafiki and Wahab (2014

) and Rafiki and Wahab (2014 ![]() ). A very good discussion on the awareness and practices of Islamic values was held while interviewing all the respondents, especially with the manager. He has personally mentioned, the values could be abundance if we try to look every single element related to Islamic values and practices in their organisation. Several salient points or values have directly been mentioned such as; cooperation and helping behaviour among staff; good manners with customers as well as among themselves; discipline (punctuality); hardworking attitude and willingness to work extra miles while delivering project under short period of time; as well as the very important values of integrity/trustworthy of their employees.

). A very good discussion on the awareness and practices of Islamic values was held while interviewing all the respondents, especially with the manager. He has personally mentioned, the values could be abundance if we try to look every single element related to Islamic values and practices in their organisation. Several salient points or values have directly been mentioned such as; cooperation and helping behaviour among staff; good manners with customers as well as among themselves; discipline (punctuality); hardworking attitude and willingness to work extra miles while delivering project under short period of time; as well as the very important values of integrity/trustworthy of their employees.

The manager admitted that he personally believes at the spiritual (Islamic) values (Rego and Pina e Cunha, 2008 ![]() ) in such a daily basis. The manager tested their employees on the narration of ‘alfatihah verse’, just to make sure all employees not only perform solat but perform it in such a good or proper way. Lastly, after all the good values being demanded by the employees, the managers know how to compensate and make them happy by offering such a good welfare package to the employees. He also visibly mentioned how welfare element is really an important value in Islam. The generous welfare element has been confirmed by all other respondents in the interview session and this practice has contributed to the individual and organisational performance as mentioned in the previous literature (Epstein, 2004

) in such a daily basis. The manager tested their employees on the narration of ‘alfatihah verse’, just to make sure all employees not only perform solat but perform it in such a good or proper way. Lastly, after all the good values being demanded by the employees, the managers know how to compensate and make them happy by offering such a good welfare package to the employees. He also visibly mentioned how welfare element is really an important value in Islam. The generous welfare element has been confirmed by all other respondents in the interview session and this practice has contributed to the individual and organisational performance as mentioned in the previous literature (Epstein, 2004 ![]() ; Crook et al., 2011

; Crook et al., 2011 ![]() ; Franco-Santos et al., 2012

; Franco-Santos et al., 2012 ![]() ).

).

4.4. Treatment of Islamic values in PMS

Integrity/trustworthy is being assessed by the manager as part of the measuring employee performance but he considered that as an informal or unofficial assessment. He admitted that formal measuring system which is to include this Islamic element looks difficult to be implemented. However, in terms of intention and willpower the manager seems very adamant to include this element, just probably does not know how to do it. He is perhaps lacking in information and needs to do a proper or more study on the implementation as well as the consequences of formally measuring Islamic values as part of their PMS.

Citing an element of backfire, the manager feels measuring integrity as well as other Islamic values is more or less an intrusion of employee personal affairs, though thus far there are no cases of backfire as he has implemented it informally. Despite the findings revealed less information on the PMS implementation, the respondents (employees) admitted that their manager practising Islamic values as well as cultivating the values in their workplace besides the entire official KPIs which every employee has been made known of.

4.5. Suggestion on Practices and Treatment of Islamic values in PMS

Three respondents believe that there should be both formal and informal way of measuring Islamic values in their organisation, with just one prefers it to be implemented as informal. They feel while are some elements are just fine to be officially announced as their future KPIs, several other elements might be better to be kept hidden between the manager and that particular employee only.

There are also suggestions on how to increase the awareness and practices of Islamic values in the organisation, such as, management by example (by the manager and supervisor); never give up attitude, insistence on having utmost priority on solat as it could lead us to do more good deeds in life; giving a strong basic of Islamic knowledge; never stop giving advice and motivations; as well as developing better rules and regulations which are appropriate to improve the performance of the employees.

Finally, this study could contribute to the existing knowledge as well as to the practice by giving evidence on the practise of Islamic values and its relationship with PMS in this SME. A new framework for PMS incorporating behavioural elements has been long discussed and this evidence on the practices of Islamic values could be well suited as one of the many behavioural elements in the organisational context. Regarded as one of the successful and biggest SMEs in the local area, the practices of Islamic values in this organisation could possibly influence and motivates other SME to at least achieve the same levels as their current position.

5. CONCLUSIONS

The awareness and practices of Islamic values in the business organisation were confirmed by this study, following its discussion in a wide body of literature as reviewed by Rafiki and Wahab (2014 ![]() ). All respondents clearly spoke positively about the practices of Islamic values at their workplace, and some other evidence such as documents and notices clearly supported what has been narrated by them. Several values have been listed in Table 1, segregated by the sources of information those values have been taken from; whether from the interview, observation, and written document. The main source of information was obviously employed from semi-structured interviews conducted with all four respondents of the SME. The values exclusively from the interviews are welfare, cooperation, helping behaviour, volunteerism, hardworking, good manners as well as trustworthiness. Safety and cleanliness values are the only two mentioned from all the three resources. Ethics is the only value evidenced from written documents, and the final two values of religious class and discipline were from interviews as well as written documents. It could be concluded that the awareness and practices of Islamic values in this SME are considered at respectable level.

). All respondents clearly spoke positively about the practices of Islamic values at their workplace, and some other evidence such as documents and notices clearly supported what has been narrated by them. Several values have been listed in Table 1, segregated by the sources of information those values have been taken from; whether from the interview, observation, and written document. The main source of information was obviously employed from semi-structured interviews conducted with all four respondents of the SME. The values exclusively from the interviews are welfare, cooperation, helping behaviour, volunteerism, hardworking, good manners as well as trustworthiness. Safety and cleanliness values are the only two mentioned from all the three resources. Ethics is the only value evidenced from written documents, and the final two values of religious class and discipline were from interviews as well as written documents. It could be concluded that the awareness and practices of Islamic values in this SME are considered at respectable level.

However, when it comes to the relationship with performance measurement system (PMS), respondents have a few mixed responses. Trustworthiness or integrity is clearly mentioned by the manager as the value he uses to assess his employees’ performance. Most of the other respondents have not had much information on the performance measurement affairs due to the role of assessing employees’ performance being just handled by the manager. All of them, however, admitted that their manager does impose Islamic environment in their workplace. Discussing more on the PMS and its relationship with the Islamic value in the SME, the manager really has high hope on formally measuring employees in future, but raises his concerns on the element of backfire as if the employee feels that action is more or less an intrusion of personal affairs.

Fast forward to the future, three respondents believe that measuring Islamic values as part of the formal employee’s performance measurement system is indeed possible and acceptable but still reserve the system to be in both ways (formal and informal). Only one respondent made up his mind to let the element stay within the informal system. Suggestions have been made by all respondents in order to increase Islamic values awareness and practices such as through management by example (by the manager or supervisor), improve the basis of Islamic knowledge, as well as impose better rules and regulations. This study could also contribute to the basis of possibly developing a new framework for PMS to include behavioural elements including practices of Islamic values.

| Funding: This research is funded by the University Research Grant, Universiti Sultan Zainal Abidin, Malaysia. |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: The authors gratefully acknowledge to reviewers and the participants of World Academy of Islamic Management for their comments. |

REFERENCES

Aziz, A.Y., 2015. Achievement assessment from an islamic perspective. Kuala Lumpur: Dewan Bahasa dan Pustaka.

Azofra, V.n., B. Prieto and A. Santidrián, 2003. The usefulness of a performance measurement system in the daily life of an organisation: A note on a case study. The British Accounting Review, 35(4): 367-384. Available at: https://doi.org/10.1016/s0890-8389(03)00058-1.

Creswell, J.W., 2007. Qualitative inquiry and research design: Choosing among five approaches. 3rd Edn., Los Angeles: SAGE Publications.

Crook, T.R., S.Y. Todd, J.G. Combs, D.J. Woehr and D.J. Ketchen Jr, 2011. Does human capital matter? A meta-analysis of the relationship between human capital and firm performance. Journal of Applied Psychology, 96(3): 443-456. Available at: https://doi.org/10.1037/a0022147.

Dawson, A., 2010. A case study of impact measurement in a third sector umbrella organisation. International Journal of Productivity and Performance Management, 59(6): 519-533. Available at: https://doi.org/10.1108/17410401011063920.

Denscombe, M., 2010. The good research guide: For small-scale social research projects (Open UP Study Skills). McGraw-Hill.

Epstein, M.J., 2004. The drivers and measures of success in high performance organizations. Performance Measurement and Management Control: Superior Organizational Performance. Studies in managerial and Financial Accounting, 14: 3-18.

Foziaa, M., A. Rehmana and A. Farooq, 2016. Entrepreneurship and leadership: An islamic perspective. International Journal of Economics, Management and Accounting, 24(1): 15-47.

Franco-Santos, M., M. Kennerley, P. Micheli, V. Martinez, S. Mason, B. Marr, D. Gray and A. Neely, 2007. Towards a definition of a business performance measurement system. International Journal of Operations & Production Management, 27(8): 784-801. Available at: https://doi.org/10.1108/01443570710763778.

Franco-Santos, M., L. Lucianetti and M. Bourne, 2012. Contemporary performance measurement systems: A review of their consequences and a framework for research. Management Accounting Research, 23(2): 79-119. Available at: https://doi.org/10.1016/j.mar.2012.04.001.

Fried, A., 2010. Performance measurement systems and their relation to strategic learning: A case study in a software-developing organization. Critical Perspectives on Accounting, 21(2): 118-133. Available at: https://doi.org/10.1016/j.cpa.2009.08.007.

Garengo, P. and G. Bernardi, 2007. Organizational capability in SMEs: Performance measurement as a key system in supporting company development. International Journal of Productivity and Performance Management, 56(5/6): 518-532. Available at: https://doi.org/10.1108/17410400710757178.

Gillham, B., 2005. Research interviewing: The range of techniques: A practical guide. UK: McGraw-Hill Education.

Gomez-Mejia, L.R. and D. Balkin, 2012. Management: People, performance, change. Upper Saddle River: Pearson Education Inc.

Jochem, R., M. Menrath and K. Landgraf, 2010. Implementing a quality-based performance measurement system: A case study approach. The Total Quality Management Journal, 22(4): 410-422. Available at: https://doi.org/10.1108/17542731011053334.

Katz, D., 1964. The motivational basis of organizational behavior. Behavioral Science, 9(2): 131-146. Available at: https://doi.org/10.1002/bs.3830090206.

Muhammad, S.S., 2002. Islamic-centred development. Kuala Lumpur: Utusan Publications & Distributors and Penang: Islamic Development Management Project (IDMP), Universiti Sains Malaysia.

Najmi, M. and D.F. Kehoe, 2001. The role of performance measurement systems in promoting quality development beyond ISO 9000. International Journal of Operations & Production Management, 21(1/2): 159-172. Available at: https://doi.org/10.1108/01443570110358512.

Rafiki, A. and K.A. Wahab, 2014. Islamic values and principles in the organization: A review of literature. Asian Social Science, 10(9): 1. Available at: https://doi.org/10.5539/ass.v10n9p1.

Rego, A. and M. Pina e Cunha, 2008. Workplace spirituality and organizational commitment: An empirical study. Journal of Organizational Change Management, 21(1): 53-75. Available at: https://doi.org/10.1108/09534810810847039.

Rejc, A. and S. Slapnicar, 2004. Determinants of performance measurement system design and corporate financial performance. Studies in Managerial and Financial Accounting, 14: 47-73.

Ryan, B., R.W. Scapens and M. Theobald, 2002. Research method and methodology in finance and accounting. London, UK: Thomson.

Taticchi, P., F. Tonelli and L. Cagnazzo, 2010. Performance measurement and management: A literature review and a research agenda. Measuring Business Excellence, 14(1): 4-18. Available at: https://doi.org/10.1108/13683041011027418.

Yin, R.K., 2009. Case study research: Design and methods (applied social research methods). London and Singapore: Sage. pp: 5.