CORPORATE GOVERNANCE STRUCTURE OF STATE ISLAMIC RELIGIOUS COUNCILS IN MALAYSIA

1,2,3,4,5Faculty of Business, Economics and Accountancy Universiti Malaysia Sabah Sabah, Malaysia

ABSTRACT

Little is known about corporate governance in Islamic perspective, particularly in the context of emerging economy and in the perspective of religious institutions. The distinguishing feature of Tawhid (oneness of God) in the Islamic corporate governance structure makes it worthwhile to investigate the corporate governance structure of the State Islamic Religious Councils (SIRCs) in Malaysia. The study incorporates Iqbal and Mirakhor (2004). Islamic corporate governance stakeholder-oriented model to reflect the structure of corporate governance in the SIRCs. A qualitative approach is utilised where data is drawn primarily from interviews and reviews of documents. Findings show that the corporate governance structure of the SIRCs is similar to the model proposed by Iqbal and Mirakhor (2004). Firstly, the Shariah rules play as a principal foundation which guides the operation, management and governance of the SIRCs. Then, Council Members act as the Shariah Board who advise and supervise the SIRCs. The research also suggests the shareholders component be replaced with main stakeholders component consisting of zakat payers, trustors and customers who suit the context of SIRCs. The SIRC is then directed by a Chief Executive Officer who represents the Board of Directors while the management is represented by the directors or managers of each division in the SIRCs who are responsible to manage their own divisions according to the Shariah principles. Finally, the other stakeholders are represented by many such as the employees, rightful recipients and the public who have direct and indirect participation in the SIRCs.

Keywords:Corporate governance, Religious institutions, Malaysia

ARTICLE HISTORY: Received:20 March 2018. Revised:30 April 2018. Accepted:7 May 2018. Published:16 May 2018.

1. INTRODUCTION

Corporate governance has been at the forefront of discussions by scholars and regulators for decades. Often being discussed is that failure or ineffective corporate governance led to a series of major financial scandals that sent the world’s economy into collapses. However, little is known about corporate governance in Islamic perspective. Majority of the literature on Islamic corporate governance is found in the context of advanced economies (Hardy and Ballis, 2013; Srairi, 2015) leaving a gap in the literature for Islamic corporate governance in the context of emerging economies. Additionally, most of the literature on Islamic corporate governance is related to Islamic banking industry (Safieddine, 2009; Samra, 2016) and less corporate governance research has been conducted in the perspective of religious institutions. Therefore, the study attempts to fill the gap in the literature by investigating the corporate governance structure of the State Islamic Religious Councils in Malaysia, by incorporating an Islamic corporate governance stakeholder model proposed by Iqbal and Mirakhor (2004).

In Malaysia, the administration of Islamic religious affairs is given to Majlis Agama Islam or the State Islamic Religious Council (SIRC). The SIRC is responsible to advise the Head of Islamic Religion in all Islamic matters except for Islamic law and administration of justice which is within the power of the Shariah courts and muftis. The SIRCs also manage Islamic wealth such as zakat, waqf, baitulmal and other Islamic funds. Currently, there are fourteen SIRCs in Malaysia. Each of the SIRCs is established based on the Federal Constitution in accordance with Schedule 9 List 2, List of State that stated the states are authorised to have the jurisdiction to govern the collection of zakat fitrah, baitulmal or other similar Islamic funds. This leads to different functions and jurisdictions of the SIRCs as each of the SIRCs is subjected to its respective state’s administration.

The SIRCs play a very important role in promoting, driving, assisting and initiating the economy, social development and well-being of Muslim community in Malaysia, in line with Shariah laws. However, they are not excluded from being scrutinised by the Muslim public. They are often being criticised for their performance and inefficiency in managing Muslim wealth (Mohd et al., 2015) in addition to increasing concerns raised by the public about the possibility of fraud and corruption as seen in many recent headlines of newspapers and online articles related to these institutions (see Berita Harian Online (2017)). Consequently, the accountability of the SIRCs is being questioned and the corporate governance aspect has become an important matter for the public. Thus, it is important to revisit corporate governance practices of the SIRCs in order to elucidate the operations, management and governance of the SIRCs which may assist to restore or enhance the public confidence against these institutions.

2. LITERATURE REVIEW

Generally, corporate governance in the conventional perspective refers to the method by which a corporation is directed, administered and controlled (Elasrag, 2014). It is also viewed as a performance monitoring process through the application of control measures in dealing with accountability, transparency and integrity. Corporate governance includes the ways corporations are accountable to its stakeholders, as well as monitoring the management of the organizations in running their businesses (ibid). On the other hand, the concept of corporate governance from the perspective of Islamic does not have a significant difference with the conventional definition of corporate governance. However, the concept of corporate governance in the Islamic perspective presents a unique distinction whereby it is a broader decision-making system that is premised on the divine oneness of God (Choudhury and Hoque, 2004). Corporate governance within Islamic framework works as to protect the stakeholders’ interest as a whole through Tawhid (oneness of God) concept, ethics and Shariah or Islamic law as the foundation.

Due to the distinction between the two concepts of conventional and Islamic corporate governance, there is a need for research to investigate further into the corporate governance from an Islamic perspective. Often found in the literature is the issue of corporate governance in the context of commercial corporations, frequently looking at the aspect of corporate governance factors. For example, Afrifa and Tauringana (2015) conducted a research on the effect of corporate governance factors on the performance of UK listed small and medium enterprises who found that corporate governance factors such as board size, CEO age and tenure, and directors’ remuneration have a significant impact on the performance of the said enterprises. However, research has shown that there is a growing interest in the corporate governance from the perspective of Islam. Many researchers have investigated the corporate governance aspect in an Islamic context, which is majorly focused on financial institutions (Safieddine, 2009; Haider et al., 2015; Samra, 2016). However, little is written regarding the corporate governance structure, especially in religious institutions. Moreover, research on corporate governance in the context of emerging economy is still scarce, providing limited information and understanding of these organisations particularly in Malaysia.

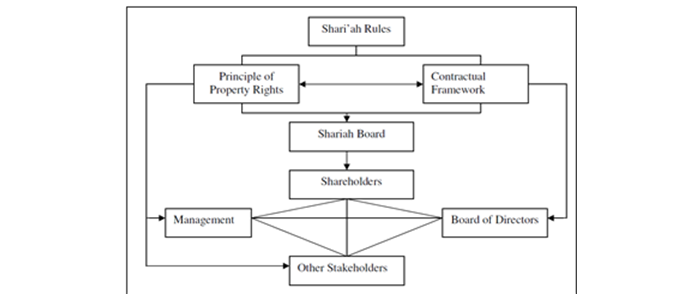

Thus, this research attempts to discuss the corporate governance structure of the SIRCs in Malaysia. The research adopts an Islamic corporate governance model based on the stakeholder model proposed by Iqbal and Mirakhor (2004) to portray the corporate governance structure of the SIRCs. Figure 1 summarised the Islamic corporate governance based on the stakeholders-oriented model proposed by Iqbal and Mirakhor (2004). The model portrays a governance structure that is to protect the interest and rights of all stakeholders. The model comprises six components which are (1) Shariah rules, (2) Shariah board, (3) shareholders, (4) Board of Directors, (5) management, and (6) other stakeholders.

The first component is the Shariah rules that have already been prescribed in Islam, which are divided into two fundamental concepts: (i) principle of property rights; and (ii) contractual frameworks. Firstly, the principle of property rights in Islam provides a clear and comprehensive framework to help identify, recognize, respect and protects the interest and rights of every individual, community, the state or corporation (Hasan, 2008). In Islam, Allah is the sole owner of all properties in this world and human being is just acting as a trustee and custodian, who then are recognised to use and manage the properties in accordance with Shariah rules. Next, the second concept is a contractual framework which represents the basic foundation that every individual, society, corporation and the state are bound by their contracts, therefore establishing the rights and obligations of the parties to perform the contractual obligations in accordance with the term stipulated in the contract directly or indirectly. Therefore, the principle of contract in Islam establishes a guideline to identify and qualify who is a rightful stakeholder.

Figure-1. Islamic corporate governance based on stakeholders-oriented model (Iqbal and Mirakhor, 2004)

Then, based on these fundamental concepts, the second component which is the Shariah Board governs the corporation by overseeing the operations of the corporation, ensuring that it complies with Shariah rules. Under the Board is the third component which is the shareholders, those who provide capital to run a business. The fourth component is the Board of Directors who oversees all the stakeholders including the fifth component which is the management who has the duty to manage the firm and protects the interest of all stakeholders. The final component is the other stakeholders who may include non-investor or any party that has direct or indirect participation in the corporation (ibid). By incorporating this model, the research aims to reflect the corporate governance structure of the SIRCs in Malaysia.

3. RESEARCH METHODOLOGY

To gain insights into the corporate governance structure of the SIRCs, several SIRCs in Malaysia were included in this study. The SIRCs involved in this study were from the state of Pulau Pinang (MAINPP), Perak (MAIPk), Kedah (MAIK), Selangor (MAIS), Kuala Lumpur (MAIWP) and Johor (MAIJ). The study utilises qualitative approach as it offers an effective way of understanding the corporate governance structure of the SIRCs. Qualitative methods allow the researchers to ‘get under the skin’ of the organisations, permitting the researchers to see the informal reality which can only be perceived from the inside (Gillham, 2000). Hence, data is drawn primarily from interviews and reviews of documents. The interviews were conducted by engaging senior managers who were selected based on their experience and knowledge in each of the respective SIRCs. A semi-structured interview was employed with English and Malay languages as the main mediums of communication. The interview lasted about one to two hours, recorded and then transcribed. In order to enrich the findings derived from the interviews, the research reviewed available documents to triangulate the overall research findings.

4. FINDINGS AND DISCUSSIONS

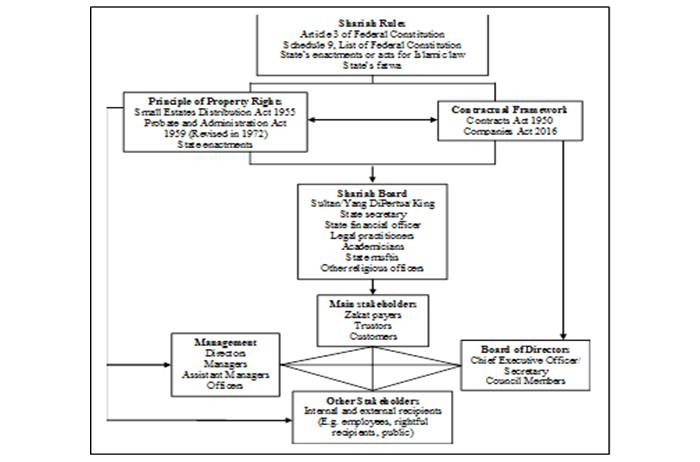

The study found that the SIRCs involved in this study have similar corporate governance structure as in the model proposed by Iqbal and Mirakhor (2004). Every SIRC has to follow Shariah rules in their daily operation, management and administration. The respondents had mentioned in the interviews that they must abide the Shariah rules and be cautious especially in managing the Muslim wealth. Thus, the first component in the model which consists of the two fundamental concepts of property rights and contractual framework are being practised and emphasised in their operation and management, as illustrated in the comments below:

For the case of special waqf, this waqf has its own special beneficiary where we are only the trustee. We cannot follow the normal accounting treatment for zakat and waqf because we are subjected to Shariah rules.

[MAIPK]Our core product is will. MAIS is appointed as executor in which we will help the applicant to complete the will documentation from the start to the end. The will document will be in force as long as the applicant is still alive. After the applicant dies, we will then continue to manage the applicant’s properties where we will charge our service based on the properties’ valuation.

[MAIS]Based on the comments, the principle of property rights provides the guideline that allows SIRCs to act as the trustee and then manages the properties in accordance with Shariah rules. Therefore, this concept helps the SIRCs to identify, recognise, respect and protects the rightful owner of the properties as a means to prevent mismanagement of the properties or funds. Next, the concept of a contractual framework is illustrated in the second comment, which portrays an example of a contractual obligation between the SIRCs and the applicant. Both parties have their contractual obligations i.e. the applicant needs to pay for the services and complete necessary documentation, and the SIRCs need to process the documentation and execute the necessary work of managing the properties when the time comes. Both concepts are embedded in various Islamic laws that vary according to the respective states the SIRCs operate.

Next, in context of the SIRCs, the Shariah Board component is represented by whom they call as the Council or Council Members. They are the highest governing board in the SIRCs who advise and supervise the operations of the SIRCs while ensuring it is in compliance with Shariah principles. The Council is the advisor to the Sultan in Islamic religious matter, and also carries the responsibility as policymakers, as mentioned by the following comment:

The State Islamic Religious Council is then divided into two parts: one part is the Council whose members report directly to the Sultan. Then, the second part is the administrative function who manages zakat, baitulmal and waqf. The Council is the policymakers. This is the hierarchy.

[MAIJ]We have a Council who is the policy makers and also an advisor to the Sultan. Many people do not understand when we mention about the Council. The State Religious Council is the administrative function which is limited to the operations and activities related to zakat, waqf and baitulmal. Then, there is a Council who makes the policy, and this is what we refer as the Board.

[MAIPK]The members of the Councils, however, vary among the SIRCs. Some of the Council members include the highest authority which is the Head of Islam Religion who is the Sultan or king and for the states without Sultan, the Board is led by the Yang DiPertua. The Council members come from diverse backgrounds but the members are usually amongst the state secretaries, state legal advisors, Shariah chief judges, state financial officers, muftis, lecturers, police chiefs and other religious officers. Hence, any decision made by the SIRCs will be discussed and brought to the Council before finally being endorsed or approved by the Sultan.

Moving on to the third component, a shareholder is typically defined as a person or an organisation who invests capital to run a business which in return, they will receive corporate ownership of the company. But it is important to note that the SIRC is a statutory body who reports directly to the Sultan, and is not placed under the federal or state government. Therefore, they do not receive funds from the federal or state government, and they do not issue shares to the public in return for ownership of the corporation. Thus, they need to generate income to run their operations.

In general, the main activities of the SIRCs are the collection of zakat, waqf and baitulmal. Most of the collected fund would then be redistributed to the rightful recipients. These activities, therefore, consume a huge amount of operating costs. Thus, the SIRCs sustain their operation through income-generating means by providing services such as wealth management. An example of an income-generating means can be illustrated by the following comment:

We manage hibah mutlak (absolute grant) which is a gift of a person to another person on the basis of compassion and affection without expecting anything in return. For instance, if a person would like to give something to another person, the person can appoint MAIS as the administrator and MAIS will then manage the documentation and administrative works relating to the hibah.

[MAIS]The above comment demonstrates how the SIRCs generate their income through the public. The SIRCs charge the public with a reasonable service fee, in return for the services they had provided. Therefore, the conventional definition of shareholders may not be suitable for the SIRCs as unlike the normal private corporations, the SIRCs do not offer corporate ownership. Alternatively, the research suggests the component to be renamed as main stakeholders. The main stakeholders suit to represent the third component in the context of SIRCs, which consist of the zakat payers, trustors and customers as the one who provides the means for SIRCs to run their operations.

The fourth component is the Board of Directors. In practice, most of the SIRCs are led by a Chief Executive Officer (CEO) who represents the Board of Directors in the corporate governance model. Notably, there are some SIRCs which are led by a Secretary who then shares a similar role as the CEO. In general, SIRCs engage with a variety of activities such as collection, distribution, management and consultation. The CEO or the Secretary, therefore, has the duty to monitor and oversee these activities. In addition, there are CEOs who are also acting as the Secretary for the Council. In other words, the CEOs are also involved in the supervision duties of the Council. This is clarified in the following comment:

The new enactment states that the CEO is also acting as the Secretary of the Council. It means that the CEO has two roles. In the Board (Council), he will become the Secretary of the Board. But, when it comes to the administrative function (SIRC), he will be the CEO.

[MAIPK]Then, the CEO is assisted by the management. There are many divisions or units in the SIRCs, and it differs among them. Some SIRCs still have zakat and waqf divisions, while SIRC such as MAIS has already separated and corporatised their zakat and waqf functions. Despite the differences in the division, each of the division is led by a director or a manager. These positions represent the fifth component which is the management in the corporate governance model. The directors may then be assisted by managers, assistant managers or officers, varying according to the respective SIRCs as mentioned in the comments below:

The highest position here is the CEO. Then, he is assisted by two Chief Assistant Directors who lead the Management Services Division the Zakat, Baitulmal and Waqf Division.

[MAIJ]The highest authority in MAIS is the Secretary. Then, under the Secretary are few directors such as Baitulmal Director. Then, the Baitulmal Director is assisted by Baitulmal Manager and several Assistant Managers.

[MAIS]Finally, the sixth component is the other stakeholders who may include non-investor or any party who has direct or indirect participation in the corporation, such as employees and the public (Hasan, 2008). The employees can be considered as the stakeholders as they play a significant and crucial role in carrying out their responsibility and social duties to the public in running the daily operation and activities of the SIRCs. Therefore, they receive monthly remunerations and bonuses in return for their services. Thus, the employees have their own interests and at the same time, carrying the responsibility to protect the public’s interest by ensuring the funds are being managed properly and the interest of the rightful owners of the fund or properties is protected. The public, too, has both direct and indirect interest with the SIRCs and can demonstrate a powerful governance mechanism through constant monitoring or scrutiny of the operation, management and administration of the SIRCs.

Hence, the research findings demonstrate that the corporate governance structure of the SIRCs is similar to the model proposed by Iqbal and Mirakhor (2004) with some modification of the terms in the corporate governance model. The corporate governance structure of the SIRCs is summarised in Figure 2.

5. CONCLUSION

The research aims to study the corporate governance structure of the SIRCs in Malaysia, by incorporating an Islamic corporate governance stakeholder model proposed by Iqbal and Mirakhor (2004). The research concludes that the corporate governance structure of the SIRCs is similar to the proposed model. Even though there are slight differences in the administrative structures among the SIRC such as having a

CEO or a Secretary as the highest level executive or having a director or a manager to lead a division, the differences are insignificant as the functions and responsibilities are actually similar. Moreover, the research findings show that the conventional definition of a shareholder as an individual or organisation that provides capital to a business in return for corporation ownership may be unsuitable in the context of the SIRCs. Therefore, the research suggests replacing the shareholders component to main stakeholders component consisting the zakat payers, trustors and customers. Finally, future research may employ quantitative methods in gathering the data as to get a better understanding and a broad view of the corporate governance structure of the SIRCs in Malaysia.

Figure-2. Corporate governance structure of the State Islamic Religious Councils in Malaysia, adapted from Iqbal and Mirakhor (2004)

(Source: Islamic Development Bank)

| Funding: The authors acknowledge the financial support from the Malaysia Ministry of Higher Education on FRGS fund (FRG0442-SS-1/2016: Islamic corporate governance practice: Comparative case studies between corporated and non-corporated Baitulmal in Malaysia). |

| Competing Interests: The authors declare that they have no competing interests. |

| Contributors/Acknowledgement: A special acknowledgment to all SIRCs that involved in this research for their assistance, making this research workable. |

REFERENCES

Afrifa, G.A. and V. Tauringana, 2015. Corporate governance and performance of UK listed small and medium enterprises. Corporate Governance, 15(5): 719-733.View at Google Scholar | View at Publisher

Berita Harian Online, 2017. CEO, Zakat officer Penang was charged with bribery. Retrieved from https://www.bharian.com.my/berita/kes/2017/07/303661/ceo-pegawai-zakat-pulau-pinang-didakwa-rasuah .

Choudhury, M.A. and M.Z. Hoque, 2004. An advanced exposition of islamic economics and finance. Edwin Mellen Pr, 25.

Elasrag, H., 2014. Corporate governance in Islamic financial institutions. Munich Personal RePEc Archive (MPRA Paper No. 56326). Retrieved from https://mpra.ub.uni-muenchen.de/56326/3/MPRA_paper_56326.pdf.

Gillham, B., 2000. Case study research methods. Oxford, UK: Bloomsbury Academic.

Haider, N., N. Khan and N. Iqbal, 2015. Impact of corporate governance on firm financial performance in islamic financial institution. International Letters of Social and Humanistic Sciences, 51: 106-110. View at Google Scholar | View at Publisher

Hardy, L. and H. Ballis, 2013. Accountability and giving accounts: Informal reporting practices in a religious corporation. Accounting, Auditing & Accountability Journal, 26(4): 539-566. View at Google Scholar | View at Publisher

Hasan, Z., 2008. Corporate governance of islamic financial institutions. Conference on Malaysian Study of Islam, Lamperter, United Kingdom.

Iqbal, Z. and A. Mirakhor, 2004. Stakeholders model of governance in islamic economic system. IRTI: Islamic Development Bank, 11(2): 43-63. View at Google Scholar

Mohd, N.A.H., M.S.A. Rasool, R. M. Yusof, S.M. Ali and R. A. Rahman, 2015. Efficiency of islamic institutions: Empirical evidence of zakat organisations’ performance in Malaysia. Journal of Economics, Business and Management, 3(2): 282-286. View at Google Scholar | View at Publisher

Safieddine, A., 2009. Islamic financial institutions and corporate governance: New insights for agency theory. Corporate Governance: An International Review, 17(2): 142-158. View at Google Scholar | View at Publisher

Samra, E., 2016. Corporate governance in islamic financial institutions. International Immersion Program Papers. University of Chicago Law School.

Srairi, S., 2015. Corporate governance disclosure practices and performance of islamic banks in GCC countries. Journal of Islamic Finance, 4(2): 001-017. View at Google Scholar | View at Publisher